One-Person Business Guide

Start a one person business with 30.4 million others. Step-by-step guide covering LLC formation, self-employment tax, free SBA resources, and tools to run solo.

In This Article

- Key Takeaways

- Step-by-Step

- What a One Person Business Actually Means

- How to Start a One Person Business (Step by Step)

- Recommended Tools for Running a One Person Business

- 5 Mistakes That Sink One Person Businesses

- Free Government Resources for Solo Business Owners

- Tax and Legal Essentials You Cannot Ignore

- Your Next Steps This Week

- FAQ

StartupOwl may earn a commission when you use links on this page to sign up for business tools and services. This does not affect our editorial ratings or recommendations. Our opinions are our own.

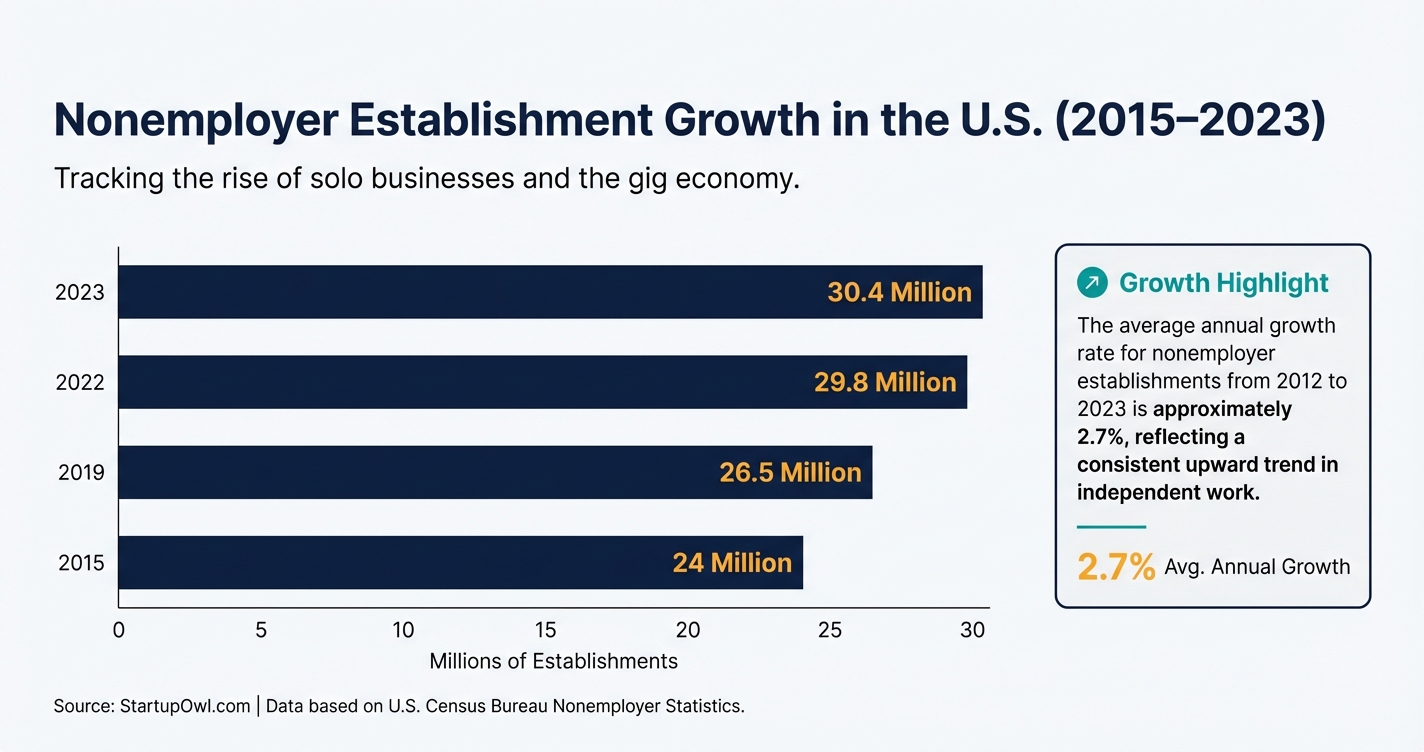

The United States had 30.4 million nonemployer businesses in 2023, generating $1.8 trillion in total receipts, according to the Census Bureau's 2023 NES-D release. That number has grown an average of 2.7% annually since 2012, consistently outpacing employer business growth.

If you are starting a one person business, you are entering a category that now accounts for the majority of all U.S. businesses. This guide walks you through the exact steps to set up your legal structure, manage your taxes, access free government resources, and build a sustainable solo operation.

What a One Person Business Actually Means

A one person business is any company owned and operated by a single individual with no employees on payroll. The Census Bureau classifies these as "nonemployer establishments," and they range from freelance consultants to e-commerce sellers to licensed tradespeople.

Sole proprietorships make up 86.3% of all nonemployer firms, according to the SBA's 2024 FAQ report. The rest operate as single-member LLCs, S-Corps, or other structures. Your legal structure matters because it determines your liability exposure and tax treatment.

Running solo does not mean running small. Nonemployer businesses contributed approximately 6.4% ($1.8 trillion) of 2023 U.S. current-dollar GDP, according to Census Bureau data. You can build a six-figure or seven-figure operation without ever hiring a W-2 employee if you use the right tools and structure.

If you are weighing whether to stay solo or eventually hire, read our comparison of solopreneur vs entrepreneur models.

How to Start a One Person Business (Step by Step)

The steps below take you from zero to operational. Each one links to the detailed tools and resources you will need. If you have already started and want business ideas, check out our solopreneur business ideas list.

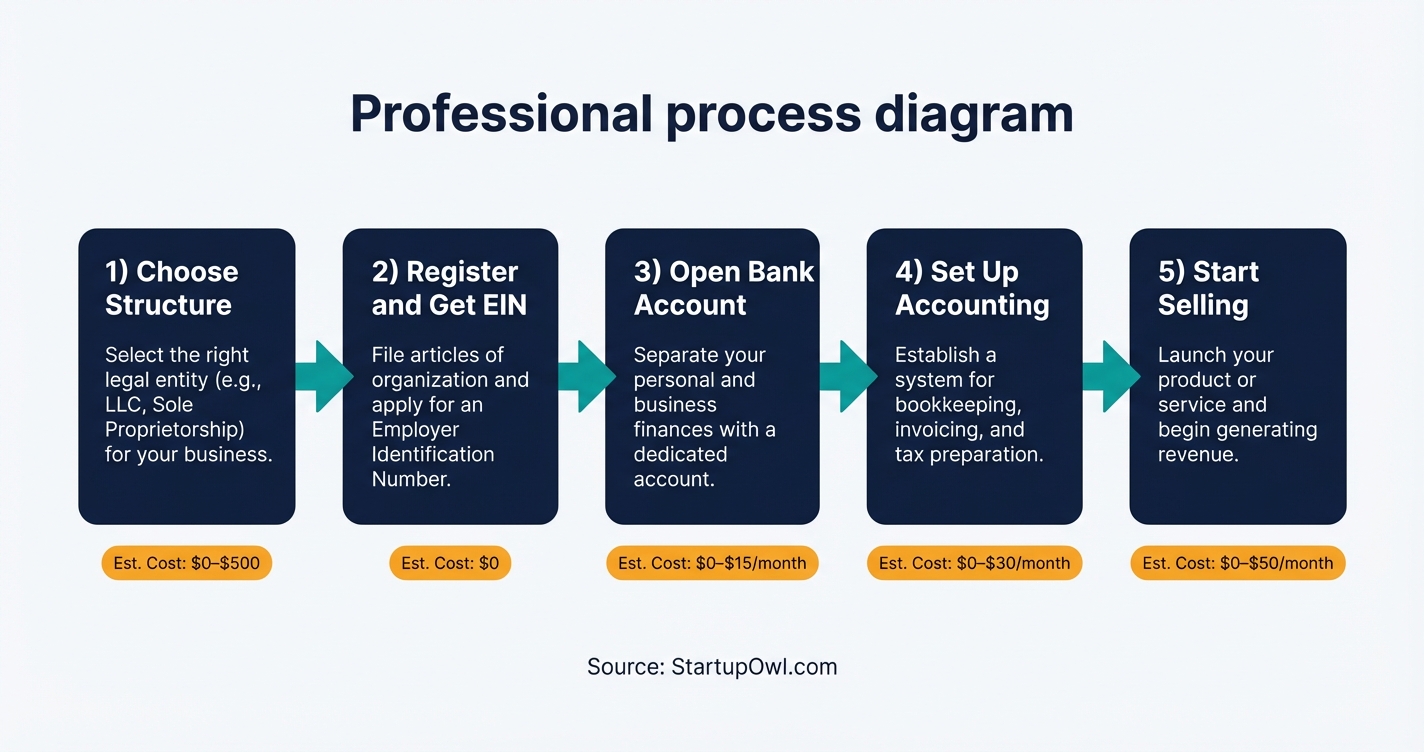

Step 1. Pick your legal structure. A sole proprietorship costs nothing to start but gives you no liability shield. A single-member LLC typically costs $50 to $500 in state filing fees and protects your personal assets if someone sues your business. Read our full breakdown of sole proprietorship vs LLC to decide.

Step 2. Register your business. File your LLC with your state's Secretary of State (or simply start operating as a sole prop). Get a free EIN from the IRS online portal. Our guide on how to register a business covers every state requirement.

Step 3. Open a business bank account. Separate finances from day one. See our ranked list of best business bank accounts for solopreneurs.

Step 4. Set up bookkeeping and tax planning. The IRS self-employment tax rate is 15.3% on your net earnings (12.4% Social Security plus 2.9% Medicare). Set aside 25–30% of income for combined federal and state taxes. Use accounting software to automate the process.

Step 5. Start generating revenue. Focus on a single offer, validate it with paying customers, and build from there. Create a small business marketing plan and set up a local SEO presence if you serve a geographic area.

If you want a structured LLC formation process handled for you, compare LLC formation services rated by price and speed.

Recommended Tools for Running a One Person Business

You do not need a large tech stack. These four categories cover the operational foundation for most solo businesses.

- The QuickBooks Simple Start plan (starting around $30/month) handles invoicing, expense tracking, and Schedule C tax prep for sole proprietors and single-member LLCs. Compare it against alternatives in our accounting software guide.

- The Relay business checking account offers $0/month fees, no minimum balance, and automatic profit-first budgeting. See all options at best business bank accounts.

- Northwest Registered Agent provides LLC formation starting at $39 plus state fees, with a free year of registered agent service. Compare in our best LLC services roundup.

- A free SCORE mentor gives you one-on-one business advising at no cost. SCORE has 10,000+ volunteer mentors nationwide. Request one at score.org/find-mentor.

5 Mistakes That Sink One Person Businesses

1. Skipping liability protection. Operating as a sole proprietor means your personal home, car, and savings are on the line if a client sues. An LLC filing costs a fraction of what one lawsuit would. If you are unsure how to form an LLC, start there.

2. Ignoring self-employment tax until April. The 15.3% SE tax hits many first-time solopreneurs hard. Set up quarterly estimated payments from your first profitable quarter. The IRS charges penalties for underpayment, and those add up fast.

3. Mixing personal and business finances. Commingling funds can "pierce the corporate veil" of your LLC, eliminating the liability protection you paid for. Open a dedicated business checking account before you deposit your first payment.

4. Trying to do everything yourself. A one person business does not mean you handle every task solo. Outsource bookkeeping, graphic design, or content creation to contractors so you can focus on revenue-generating work. Review entrepreneur burnout warning signs before you hit a wall.

5. Having no written contracts. Verbal agreements lead to disputes about scope, payment, and deadlines. Use a legal service to create standard client contracts. Templates start at $0 from services like LegalZoom and Rocket Lawyer.

Free Government Resources for Solo Business Owners

You have access to several no-cost programs designed to help one person businesses get off the ground and grow. These are funded by the federal government and available to all U.S. business owners.

- The SCORE Mentoring Network provides free, confidential one-on-one mentoring through 10,000+ volunteer mentors. Since 1964, SCORE has helped more than 17 million entrepreneurs, according to SCORE.org. Mentored businesses have an 87% one-year survival rate versus 75% for non-mentored businesses, per SBA data.

- Small Business Development Centers (SBDCs) offer free business advising across nearly 1,000 locations nationwide, according to America's SBDC. SBDCs are hosted by universities and state agencies, and they specialize in business plans, financial projections, and market research.

- The SBA Microloan Program offers loans up to $50,000 (average loan is about $13,000) through nonprofit intermediary lenders, according to SBA.gov. Interest rates typically range from 8% to 13%, and terms can extend up to six years.

For grant opportunities, explore our guides to small business grants and startup funding options.

Tax and Legal Essentials You Cannot Ignore

Your tax obligations as a one person business depend on your legal structure. A sole proprietor reports business income on Schedule C of their personal 1040 return. A single-member LLC does the same by default (it is a "disregarded entity" for tax purposes).

The self-employment tax rate is 15.3%, consisting of 12.4% for Social Security (on the first $176,100 of net earnings in 2026) and 2.9% for Medicare (no cap), according to the IRS. You can deduct 50% of your self-employment tax from your adjusted gross income.

Once your net profit consistently exceeds $60,000 per year, ask a CPA whether electing S-Corp tax treatment could reduce your self-employment tax liability. With an S-Corp, you split income into salary (subject to SE tax) and distributions (not subject to SE tax), which can save thousands annually.

You may also need to file quarterly estimated taxes using Form 1040-ES. If you owe $1,000+ in taxes for the year and have not withheld enough, the IRS can assess underpayment penalties. Consult a tax professional to determine the right structure and estimated payment schedule for your situation.

Your Next Steps This Week

Start with three concrete actions. First, decide on your business structure and form your LLC if liability protection matters to you (it should). Second, apply for a free EIN and open a business bank account so your finances are separated from day one.

Third, request a free SCORE mentor who has built the kind of business you want to build. This costs nothing, takes 10 minutes to set up, and gives you a sounding board for every decision ahead. If you want the full roadmap for going solo, read our Solopreneur Guide.

Step-by-Step Process

- 1

Choose your business structure

Your first decision is whether to operate as a sole proprietorship or form an LLC. A sole proprietorship requires no formal filing (you are automatically one when you start earning income), but it offers zero personal liability protection.

A single-member LLC separates your personal assets from business debts. Filing fees range from $50 to $500 depending on your state. If you plan to take on clients, sign contracts, or carry any risk, an LLC is the safer choice.

Tips

- Compare your state's LLC filing fee at your Secretary of State website before choosing.

- A single-member LLC is taxed the same as a sole proprietorship by default, so you get liability protection without extra tax complexity.

Common Mistakes

- Operating as a sole proprietor when you have significant liability exposure.

- Paying for an LLC formation service before checking if your state offers a simple online filing.

- 2

Register your business and get an EIN

Even as a one person business, you need a federal Employer Identification Number (EIN) if you form an LLC or plan to open a business bank account. The IRS issues EINs for free online in minutes.

Check your state and local requirements for business licenses or permits. Some cities require a general business license even for home-based solopreneurs.

Tips

- Apply for your EIN on IRS.gov during business hours (Mon–Fri, 7am–10pm ET) for instant approval.

- Keep your EIN confirmation letter in a safe place; you will need it for banking and tax filings.

Common Mistakes

- Paying a third party for an EIN when the IRS provides it free.

- Skipping local business license requirements and facing fines later.

- 3

Open a dedicated business bank account

Mixing personal and business funds is one of the fastest ways to lose your LLC's liability protection. Open a separate business checking account from day one.

Many banks and fintechs offer free or low-cost business checking for solopreneurs with no minimum balance requirements. Look for accounts with no monthly fees and free ACH transfers.

Tips

- Choose a bank that integrates with your accounting software to save hours on bookkeeping.

- Keep a separate business savings account for your quarterly tax payments.

Common Mistakes

- Using your personal checking account for business transactions.

- Choosing a bank with high monthly fees when free options exist for low-volume accounts.

- 4

Set up accounting and plan for self-employment tax

As a one person business, you owe 15.3% self-employment tax on your net earnings, according to the IRS. That breaks down to 12.4% for Social Security and 2.9% for Medicare. This is on top of your regular income tax.

Set aside 25–30% of every payment you receive for taxes. File quarterly estimated payments using IRS Form 1040-ES to avoid underpayment penalties. A CPA can help you evaluate whether electing S-Corp status makes sense once your net profit exceeds roughly $60,000 per year.

Tips

- Automate expense categorization with accounting software to make tax time painless.

- Track mileage, home office expenses, and health insurance premiums as deductible business expenses.

Common Mistakes

- Failing to save for quarterly estimated tax payments and facing a large bill in April.

- Not tracking deductible expenses throughout the year and overpaying on taxes.

- 5

Build your client pipeline and start selling

A one person business lives or dies by its ability to generate revenue consistently. Start with one core offer (a service, product, or digital good) and validate it with real paying customers before expanding.

Create a simple website, set up a Google Business Profile for local visibility, and build an email list from day one. Referrals and repeat clients will become your most reliable revenue source once you deliver consistently.

Tips

- Start with one service or product and get your first 10 paying customers before adding complexity.

- Ask every satisfied client for a referral or testimonial.

Common Mistakes

- Building an elaborate website before validating that people will pay for your offer.

- Trying to serve too many customer segments at once instead of focusing on one niche.

Frequently Asked Questions

You can start a sole proprietorship for $0 in federal costs (just begin earning income). An LLC costs $50 to $500 in state filing fees depending on where you register. Add $0–$30/month for accounting software and a free business bank account, and your total first-year setup cost can be under $200.

You do not legally need one, but an LLC protects your personal assets (home, car, savings) if your business gets sued or cannot pay its debts. A sole proprietorship offers no such protection. If you sign contracts with clients or carry any professional risk, an LLC is worth the filing fee. Learn how to form an LLC step by step.

The self-employment tax rate is 15.3% of your net earnings, according to the IRS. On $50,000 in net profit, that is roughly $7,065 in SE tax alone (before income tax). You can deduct half of this from your adjusted gross income. Plan to set aside 25–30% of all business income for combined taxes.

A single-member LLC is the most popular choice for one person businesses that want liability protection without corporate complexity. By default, it is taxed like a sole proprietorship (pass-through on your personal return), so there is no extra tax filing burden. Compare all your options in our sole proprietorship vs LLC guide.

Yes. The SBA Microloan Program provides loans up to $50,000 specifically designed for small and solo businesses, with an average loan size of about $13,000 and interest rates between 8% and 13%. You can also apply for SBA 7(a) loans up to $5 million. See our full guide on how to get a business loan.

SCORE provides free mentoring through a network of 10,000+ volunteer business professionals. Enter your ZIP code on score.org to get matched with a mentor in your industry. SBA data shows 87% of mentored businesses survive their first year, compared to 75% without a mentor.

The information on this page is for educational purposes only and does not constitute financial, legal, or investment advice. Loan terms, interest rates, and eligibility requirements vary by lender and change frequently. Always consult with a qualified financial advisor before making funding decisions. StartupOwl may earn a commission if you click our links at no extra cost to you.

Sources & References

- Census Bureau 2023 Nonemployer Statistics by Demographics (NES-D)

- Census Bureau: Nonemployer Business Growth 2012–2023

- SBA Office of Advocacy: Frequently Asked Questions About Small Business (2024)

- IRS: Self-Employment Tax (Social Security and Medicare Taxes)

- SBA Microloan Program

- SCORE: Free Small Business Mentorship

- America's SBDC: Find Your Local Center

- SBA: Small Business Development Centers (SBDC)

About the Author

Director of Entrepreneurial Strategy

Jennifer is a former founder who built and sold a boutique B2B logistics company in her thirties. She understands the emotional and strategic toll of building a business from the ground up without a massive safety net. She is deeply connected to the Atlanta startup ecosystem and is passionate about equitable funding.

Was this article helpful?

Questions about One-Person Business Guide

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment