How to Open a Business Bank Account for Your LLC

Open your LLC's business bank account in as little as 10 minutes online. Here is every document you need, what it costs, and how to pick the right bank.

In This Article

You can open a business bank account for your LLC in 10 to 30 minutes online for $0 at Mercury, Bluevine, or Relay. Traditional banks like Chase charge $15/month (waivable with a $2,000 balance). You need four documents: Articles of Organization, EIN letter, operating agreement, and government-issued photo ID.

6

Total Steps

$0–$15

Est. Cost

30 minutes to 2 business days

Timeline

Easy

Difficulty

Opening a business bank account costs $0 to $15 per month at most banks, and the entire process takes under 30 minutes if you have your documents ready. You can open one online through providers like Mercury or Bluevine with no minimum deposit, or walk into a Chase branch with your documents and fund your account the same day.

You will need your Articles of Organization, your IRS-issued EIN, a signed operating agreement, and a government-issued photo ID. If you skip this step and keep using your personal checking account, you risk losing your LLC's liability protection in court. This guide walks you through the full process, step by step, with real costs and provider links.

Before you fill out a single bank application, gather these four documents. Missing even one will delay your approval or get you denied.

- Articles of Organization (stamped) from your state's Secretary of State office. This is the document that proves your LLC legally exists. A draft or unsigned version will not work.

- EIN Confirmation Letter (Form CP 575) from the IRS. You can apply online for free and receive your EIN immediately. See our EIN application guide for a walkthrough.

- LLC Operating Agreement signed by all members. Most banks require this even if your state does not. See our operating agreement guide to create one.

- Two forms of government-issued ID for each member with 25% or more ownership. A driver's license plus a passport is the most common combination.

If you are a multi-member LLC, every member with an ownership stake of 25% or more must provide personal identification. Some banks require IDs from all members regardless of ownership percentage.

You do not need a business license to open a bank account (unless your local jurisdiction requires one for your industry). You also do not need revenue or a business plan.

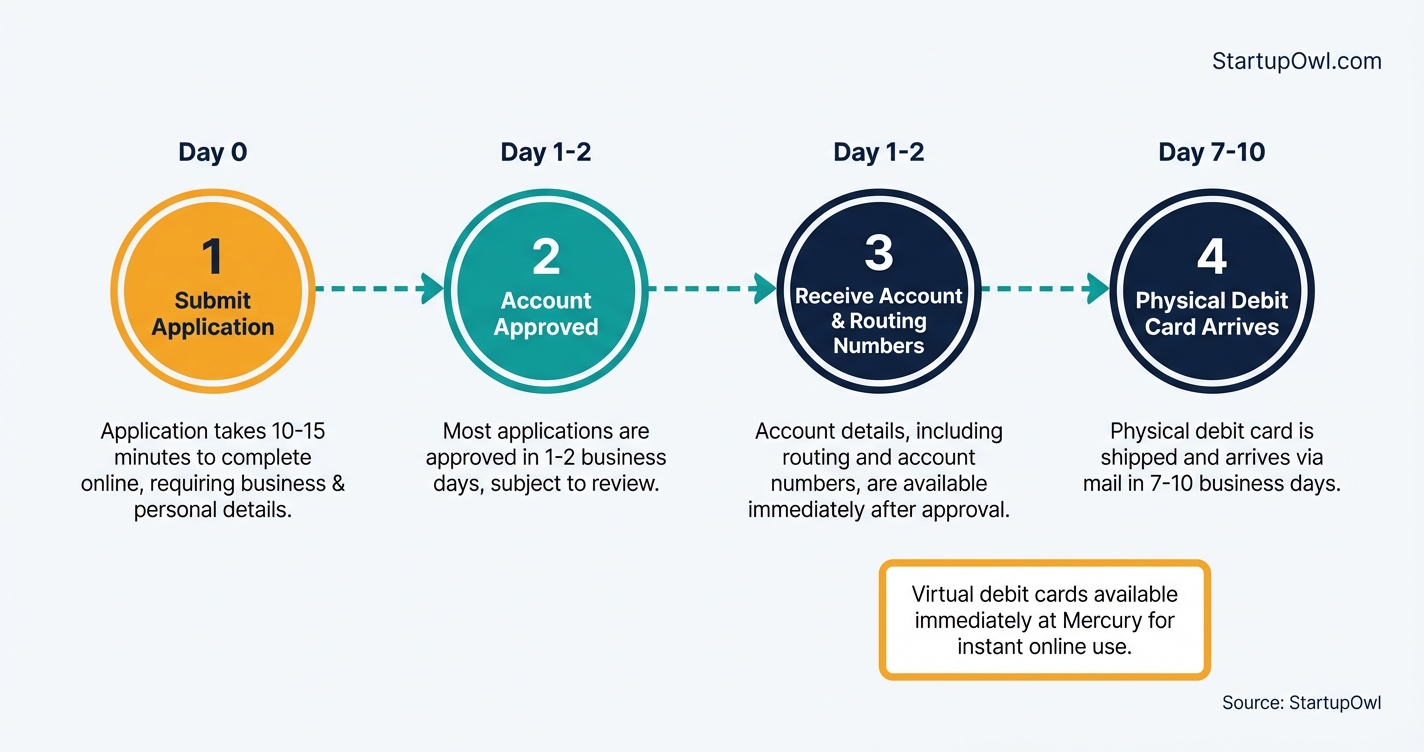

The application itself takes 10 to 15 minutes at most online providers. You will type in your LLC's legal name, EIN, business address, and your personal details (name, SSN, date of birth). Then you upload your documents.

At Mercury, approval typically takes 1 to 2 business days. Bluevine and Relay have similar timelines. Chase can approve you same-day if you apply in a branch with all required documents. If your application triggers a manual review (common for newer LLCs or complex structures), expect a 3 to 5 business day wait.

KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations have tightened in recent years. Banks now verify your identity, your LLC's registration, and your business address more thoroughly than they did five years ago. This means you should use your exact legal business name (matching your Articles of Organization) on every field. Even a small discrepancy like "LLC" vs. "L.L.C." can flag a manual review.

After approval, you will receive account details (routing number and account number) by email or within your online dashboard. A physical debit card typically arrives in 7 to 10 business days. At Mercury, you can create a virtual debit card immediately and start making purchases on the same day you are approved.

Step-by-Step Process

- 1

Confirm Your LLC Formation Is Complete

Before you apply for a business bank account, verify that your LLC is officially registered with your state. You need a stamped copy of your Articles of Organization (sometimes called a Certificate of Formation) from your Secretary of State. This document proves your business legally exists.

If you have not yet filed, visit your best LLC formation services guide to choose a provider. Most states process filings in 3 to 7 business days, though expedited options can cut this to 24 hours for an extra $50 to $100. Once you have the stamped document in hand (or a digital copy from your state's portal), you are ready to move forward.

Tips

- Download a digital copy of your Articles of Organization from your state's Secretary of State website so you have it ready to upload.

- If your LLC name has changed since formation, file a DBA (Doing Business As) certificate before opening the account.

- Multi-member LLCs should gather photo IDs for every member with 25% or more ownership before starting the application.

Common Mistakes

- Trying to open a bank account before your LLC is officially registered with the state, which will result in an automatic denial.

- Using a draft Articles of Organization instead of the state-stamped final version.

- 2

Apply for Your Free EIN from the IRS

Your Employer Identification Number (EIN) is your LLC's federal tax ID. You need it to open a bank account, file taxes, and hire employees. The good news: it is 100% free and takes under 5 minutes online through the IRS EIN Assistant.

The IRS issues your EIN immediately upon verification when you apply online. You can use it for banking purposes right away. Print or save the confirmation notice (Form CP 575) because banks will ask for it. If you already have an EIN from your EIN application, skip to the next step.

Tips

- Apply on IRS.gov directly. Never pay a third-party site for an EIN; the IRS does not charge a fee.

- Save the CP 575 confirmation letter as a PDF immediately; you cannot re-download it from the IRS later.

Common Mistakes

- Paying $50 to $200 on a third-party EIN filing site when the IRS application is completely free.

- Applying for an EIN before your LLC is registered with the state, which can cause delays per IRS guidance.

- 3

Draft or Finalize Your LLC Operating Agreement

Most banks require an LLC operating agreement when you open a business account, even for single-member LLCs. This document outlines who owns the LLC, how profits are distributed, and who has authority to manage the bank account. Without it, many banks will reject your application outright.

If you are a solo founder, your operating agreement can be a simple 1 to 3 page document naming you as the sole member and manager. Multi-member LLCs need a more detailed agreement covering capital contributions, voting rights, and dissolution terms. Free templates are available from your state's Secretary of State website, or you can use a service like LegalZoom for $0 to $99.

Tips

- Even if your state does not legally require an operating agreement, create one. Banks in most states will ask for it during account setup.

- Include a clause specifying who is authorized to open and manage bank accounts on behalf of the LLC.

Common Mistakes

- Skipping the operating agreement entirely because your state does not mandate one, only to have the bank reject your application.

- 4

Choose the Right Bank or Fintech for Your LLC

This is the biggest decision in the process. Your three main options are: online fintechs (Mercury, Bluevine, Relay), national banks (Chase, Bank of America), and local credit unions. Each tier comes with different fee structures, features, and trade-offs. See our full best business bank accounts comparison for details.

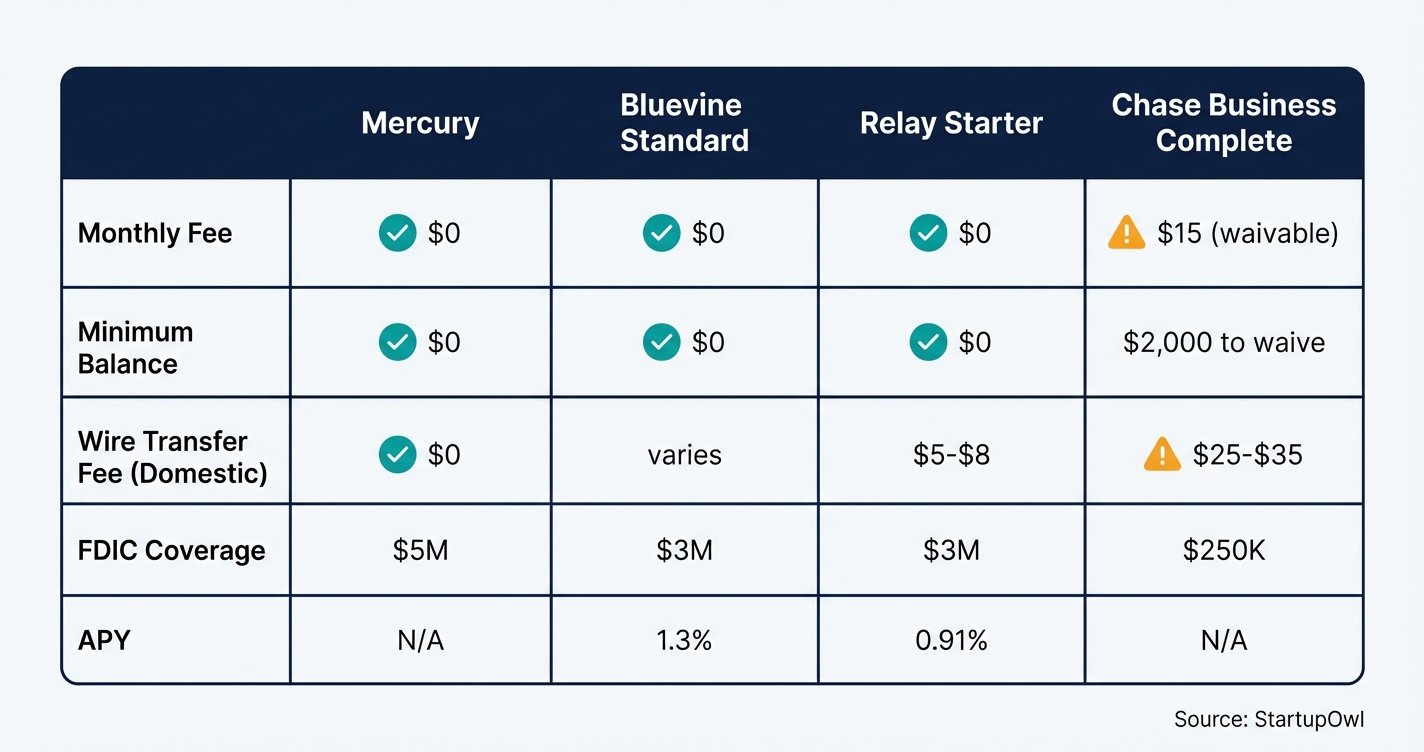

Mercury charges $0/month with no minimum balance, free domestic wire transfers, and FDIC coverage up to $5 million through partner banks and their sweep networks. Bluevine's Standard plan is also $0/month and pays 1.3% APY on balances up to $250,000, with FDIC insurance up to $3 million. Chase Business Complete Banking charges $15/month (waivable with a $2,000 minimum balance) but gives you access to over 4,900 branches and in-person cash deposits.

If your business handles cash daily (restaurants, retail), choose a bank with branch access. If you operate online, a fintech will save you money.

$0/month (Mercury, Bluevine, Relay) to $15/month (Chase) to $95/month (Bluevine Premier) 30 minutes of research mercury.comTips

- If you send wire transfers regularly, Mercury offers free domestic and international USD wires, saving you $15 to $35 per transfer vs. traditional banks.

- Cash-heavy businesses should pick Chase or a local credit union since Mercury, Bluevine, and Relay do not support cash deposits at branches.

- Check whether the bank integrates with your accounting software (QuickBooks, Xero, or FreshBooks) before you commit.

Common Mistakes

- Choosing a bank only because it is nearby without comparing monthly fees. A $15/month fee adds up to $180/year that you could avoid at a free online bank.

- Overlooking wire transfer fees. Traditional banks charge $15 to $35 per outgoing wire; Mercury charges $0 for domestic USD wires.

- 5

Submit Your Application Online or In-Branch

With your documents ready, the actual application takes 10 to 15 minutes. Most online providers (Mercury, Bluevine, Relay) accept entirely digital applications. You will upload your Articles of Organization, EIN confirmation, operating agreement, and a photo of your government-issued ID through the bank's secure portal.

For Chase and other traditional banks, you can apply online if your LLC has a single member or manager. Multi-member LLCs and other complex structures typically need to apply in person at a branch. Bring two forms of government-issued ID for each owner with 25% or more ownership. Approval at online providers usually happens within 1 to 2 business days. Chase can approve same-day in branch.

$0 (no application fees at any major provider) 10 to 15 minutes to apply; 1 to 2 business days for approval app.mercury.comTips

- Have all four documents (Articles of Organization, EIN letter, operating agreement, photo ID) saved as PDFs on your desktop before you start.

- If your application is denied, try a different provider. There is no credit impact from business bank account applications.

Common Mistakes

- Submitting blurry or cropped document uploads, which triggers manual review and delays approval by 3 to 5 business days.

- 6

Fund Your Account and Record the Initial Deposit

Once approved, fund your account with an initial deposit. Mercury and Bluevine have no minimum deposit requirement. Chase has no required minimum to open, but you must transfer money into the account within 60 days or the account will be closed. A common first deposit is $100 to $1,000 from your personal account.

Record this transfer as an "Owner Contribution" or "Member Contribution" in your bookkeeping software. This is not income and should not appear on your profit and loss statement. It goes on the balance sheet as owner's equity. Connect your new account to your accounting software right away so every future transaction is tracked automatically. Then set up your small business accounting system before you start spending.

$0 to $1,000 (initial deposit, which is your own money) 5 minutes to transfer funds; 1 to 3 business days for ACH to settle QuickBooksTips

- Transfer a round number (e.g., $500 or $1,000) to make your bookkeeping cleaner from day one.

- Label the initial deposit as Owner Contribution in QuickBooks or your accounting software to keep your books accurate.

- Order a debit card and set up online bill pay immediately so you are ready to make business purchases.

Common Mistakes

- Recording your initial deposit as income instead of owner's equity, which will inflate your reported revenue and create tax problems.

- Forgetting to fund a Chase account within 60 days, resulting in automatic account closure.

Opening and maintaining a business bank account can cost anywhere from $0 to $95 per month, depending on the provider you choose. For most new LLCs, the total year-one cost is $0. See our detailed business bank account fees breakdown for a full comparison.

Mercury charges no monthly fees, no minimum balance, no overdraft fees, and no fees for domestic or international USD wire transfers. Bluevine's Standard plan is also free with 1.3% APY on balances up to $250,000. Relay's Starter plan costs $0/month and includes up to 20 checking accounts.

Chase Business Complete Banking charges $15/month, but you can waive that fee by maintaining a $2,000 daily minimum balance, spending $2,000/month on a Chase Ink business card, or processing $2,000 in Chase QuickAccept transactions. Chase Performance Business Checking runs $30/month (waivable with $35,000 average balance), and Platinum is $95/month (waivable with $100,000 average balance).

The hidden cost most LLC owners miss is wire transfer fees. At Chase, each outgoing domestic wire costs approximately $25 to $35. At Mercury, it costs $0. If you send 5 wires per month, that is a $125 to $175/month difference.

Your bank account is open. Now protect yourself and set up the financial infrastructure around it.

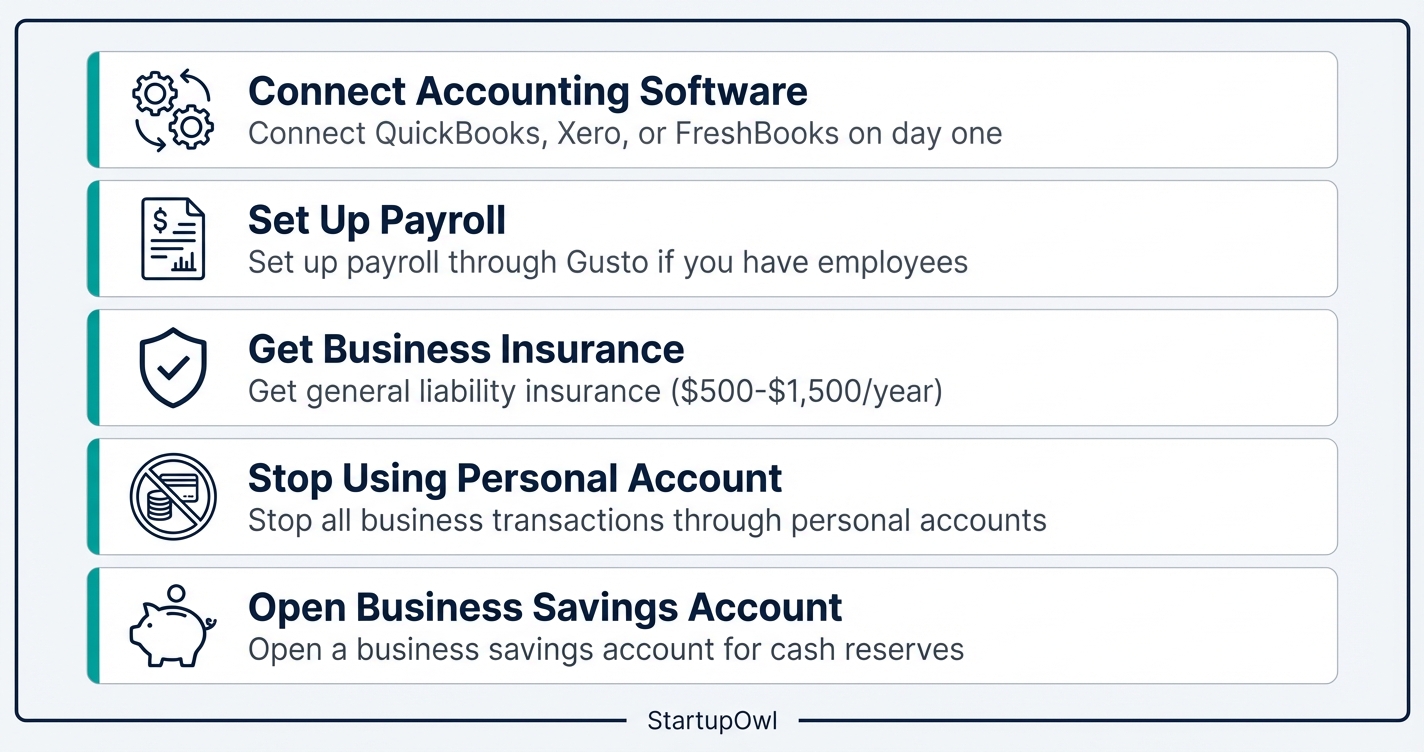

- Connect accounting software immediately. Link your new account to QuickBooks, Xero, or FreshBooks so transactions sync automatically. See our how to set up accounting guide for step-by-step instructions.

- Set up payroll if you have employees. Providers like Gusto connect directly to Mercury, Bluevine, and Chase. Our payroll setup guide walks you through the process.

- Get business insurance. General liability insurance costs $500 to $1,500/year for most small businesses and protects your LLC. See our best business insurance picks.

- Stop using your personal account for business expenses. Starting today, every business purchase, vendor payment, and client deposit should flow through this account. This protects your LLC's liability shield and makes tax time dramatically simpler.

- Consider a business savings account. If you expect to hold more than $10,000 in cash, open a business savings account at the same institution. Bluevine pays 1.3% APY on its Standard checking balances up to $250,000.

The Complete Checklist

- Verify LLC formation is complete with your Secretary of State01

Confirm you have a stamped copy of your Articles of Organization.

5 minutes$0 - Apply for a free EIN on IRS.gov02

Use the IRS EIN Assistant to get your number instantly online.

5 minutes$0 - Save your EIN confirmation letter (Form CP 575) as a PDF03

Banks require this document during the application.

1 minute$0 - Draft or finalize your LLC operating agreement04

Even single-member LLCs need one for most bank applications.

30 minutes to 2 hours$0 to $500 - Gather two forms of government-issued ID05

You need a driver's license, passport, or state ID for each owner with 25%+ stake.

5 minutes$0 - Compare at least 3 bank or fintech options06

Review monthly fees, wire transfer costs, FDIC coverage, and software integrations.

20 to 30 minutes$0 - Submit your bank application online or in-branch07

Upload your documents and complete the application form.

10 to 15 minutes$0 - Fund your new account with an initial deposit08

Transfer money from your personal account and record it as Owner Contribution.

5 minutes (1 to 3 days for ACH to settle)$0 to $1,000 - Connect your account to accounting software09

Link your bank to QuickBooks, Xero, or FreshBooks for automatic transaction syncing.

10 minutes$0 to $30/month - Order a business debit card10

Request a physical debit card for in-person purchases and ATM access.

7 to 10 business days to arrive$0

These are the most expensive mistakes LLC owners make when opening their first business bank account. Every one of them has real dollar consequences.

- Commingling personal and business funds. Using your personal checking account for business transactions puts your LLC's liability protection at risk. If a court determines you treated the LLC's money as your own, it can "pierce the corporate veil" and hold you personally liable for business debts. That is an unlimited financial exposure.

- Paying for an EIN. The IRS provides EINs for $0 at IRS.gov. Third-party sites charge $50 to $200 for the same 5-minute process. This is money thrown away.

- Skipping the operating agreement. Even for single-member LLCs, most banks require an operating agreement during account setup. If you show up without one, your application gets rejected and you lose a trip to the branch (or a week of back-and-forth with an online provider).

- Choosing a bank based on proximity alone. A bank with a $15/month fee and $25 wire transfer fees costs you over $300/year more than a free online alternative. Compare total cost of ownership, not just convenience.

- Ignoring FDIC coverage limits. Standard FDIC insurance covers $250,000 per depositor, per bank. If your LLC holds more than that, your excess deposits are uninsured unless you use a provider with sweep networks (Mercury covers up to $5M; Bluevine and Relay cover up to $3M).

- Not connecting accounting software on day one. Every week you delay syncing your bank account to accounting software is a week of transactions you will have to categorize manually later. At tax time, that manual work costs you $100 to $300 in extra bookkeeper hours.

Frequently Asked Questions

No. You cannot open a business bank account with only an EIN. Banks also require your Articles of Organization (or Certificate of Formation), a government-issued photo ID, and in most cases an operating agreement. Federal KYC (Know Your Customer) regulations require banks to verify both your business identity and your personal identity.

The application itself takes 10 to 15 minutes. Online providers like Mercury and Bluevine typically approve accounts within 1 to 2 business days. If you walk into a Chase branch with all your documents, you can open an account same-day. Complex LLC structures (multi-member, holding companies) may trigger a manual review that takes 3 to 5 business days.

Legally, no state requires a single-member LLC to open a separate business bank account. Practically, yes. Commingling personal and business funds is the fastest way to lose your LLC's liability protection. A court can pierce the corporate veil if you treat LLC money as your own. The cost of a free business checking account at Mercury or Bluevine is $0. The cost of a pierced corporate veil is potentially everything you own.

Mercury, Bluevine, and Relay all offer $0/month business checking with no minimum balance. Mercury stands out for free domestic and international USD wire transfers and up to $5 million in FDIC coverage through sweep networks. Bluevine offers 1.3% APY on balances up to $250,000. Relay lets you create up to 20 checking accounts for free, which is ideal for Profit First budgeting. See our full best business bank accounts comparison.

Yes, if you bank with an FDIC-insured institution. The standard limit is $250,000 per depositor, per insured bank, per ownership category as of 2026. Fintech providers like Mercury extend coverage to $5 million and Bluevine to $3 million by distributing your deposits across multiple FDIC-insured partner banks through sweep networks. Verify your bank's FDIC status at FDIC.gov.

Online applications are faster (approved in 1 to 2 days) and give you access to fee-free options like Mercury and Bluevine. In-branch applications at Chase or Bank of America let you walk out with an active account the same day and are better if your LLC has a complex ownership structure that might trigger online verification issues. Multi-member LLCs at Chase must apply in person.

Mercury disclosure. Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC. FDIC deposit insurance covers the failure of an insured bank. Deposits in checking and savings accounts are FDIC-insured through Choice Financial Group and Column N.A. and their Sweep Program Network Banks. Certain conditions must be satisfied for pass-through FDIC insurance to apply.

Sources & References

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about How to Open a Business Bank Account for Your LLC

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment