Solopreneur vs Entrepreneur: Key Differences

Solopreneur vs entrepreneur explained. 29.8 million U.S. solopreneurs generate $1.7 trillion in revenue. Find which path, tools, and structure fit your goals.

In This Article

StartupOwl may earn a commission when you sign up for services through links on this page. This does not affect our editorial recommendations or the order in which products appear. All opinions are our own.

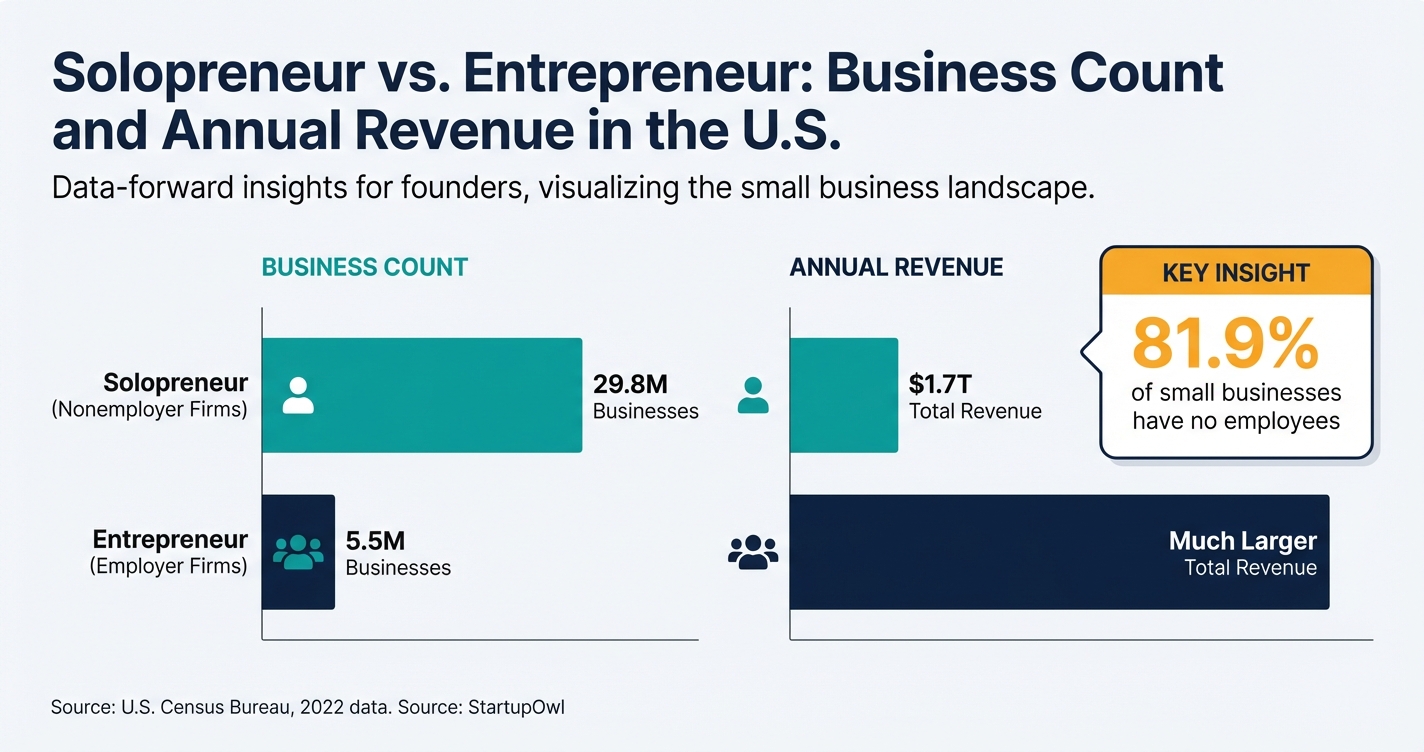

There are 29.8 million nonemployer businesses in the United States, generating roughly $1.7 trillion in annual revenue, according to the U.S. Census Bureau Nonemployer Statistics (2022 data, released 2026). That number equals about 6.4% of U.S. GDP.

More than 4 out of 5 small businesses operate without a single paid employee, per the SBA Office of Advocacy. If you are deciding between staying solo or building a team, this guide breaks down the real structural, financial, and lifestyle differences between solopreneurs and entrepreneurs so you can choose the right path.

What Makes a Solopreneur Different from an Entrepreneur

A solopreneur is a business owner who intentionally runs the entire operation alone, with no employees. You handle sales, marketing, delivery, and admin yourself (or outsource to contractors). A solopreneur deliberately structures the business around their own skill set, time, and lifestyle goals.

An entrepreneur builds a business designed to grow beyond the founder. You hire employees, develop management systems, and may raise outside capital. The goal is to create an organization that can operate without your constant involvement.

The distinction is not about ambition or income. About 20% of solopreneurs earn between $100K and $300K annually without hiring anyone, according to Leapmesh research cited by multiple industry sources (as of 2026). The difference is structural: who does the work, and how the business scales.

If you are still exploring what type of founder you want to be, read our full breakdown of solopreneur vs entrepreneur traits or start with our guide on how to become an entrepreneur.

Solopreneur vs Entrepreneur at a Glance

| Type / Provider | Rate | Notes |

|---|---|---|

| Team Size | Solopreneur: 0 employees | Entrepreneur: 1+ | Solopreneurs may use 1099 contractors |

| Startup Capital | Solo: Under $5,000 typical | Entrepreneur: $10K–$100K+ | 84% of solopreneurs self-fund (Gusto 2026) |

| Revenue Ceiling | Solo: Uncapped but time-bound | Entrepreneur: Uncapped and scalable | ~3.6% of solopreneurs hit $1M+ |

| Decision Speed | Solo: Instant | Entrepreneur: Requires alignment | No board, partners, or investors to consult |

| First-Year Profitability | Solo: 77% | Employer: 54% | Gusto 2026 New Business Formation Survey |

| Primary Risk | Solo: Burnout, income gaps | Entrepreneur: Payroll, cash flow, hiring | 41% of solopreneurs cite time management as top challenge |

| Common Structure | Solo: Sole prop or single-member LLC | Entrepreneur: LLC or S-Corp | 86.3% of nonemployers are sole proprietorships (SBA) |

| Exit Potential | Solo: Limited (tied to founder) | Entrepreneur: Higher (transferable systems) | Businesses with teams sell for higher multiples |

How to Decide Which Path Is Right for You

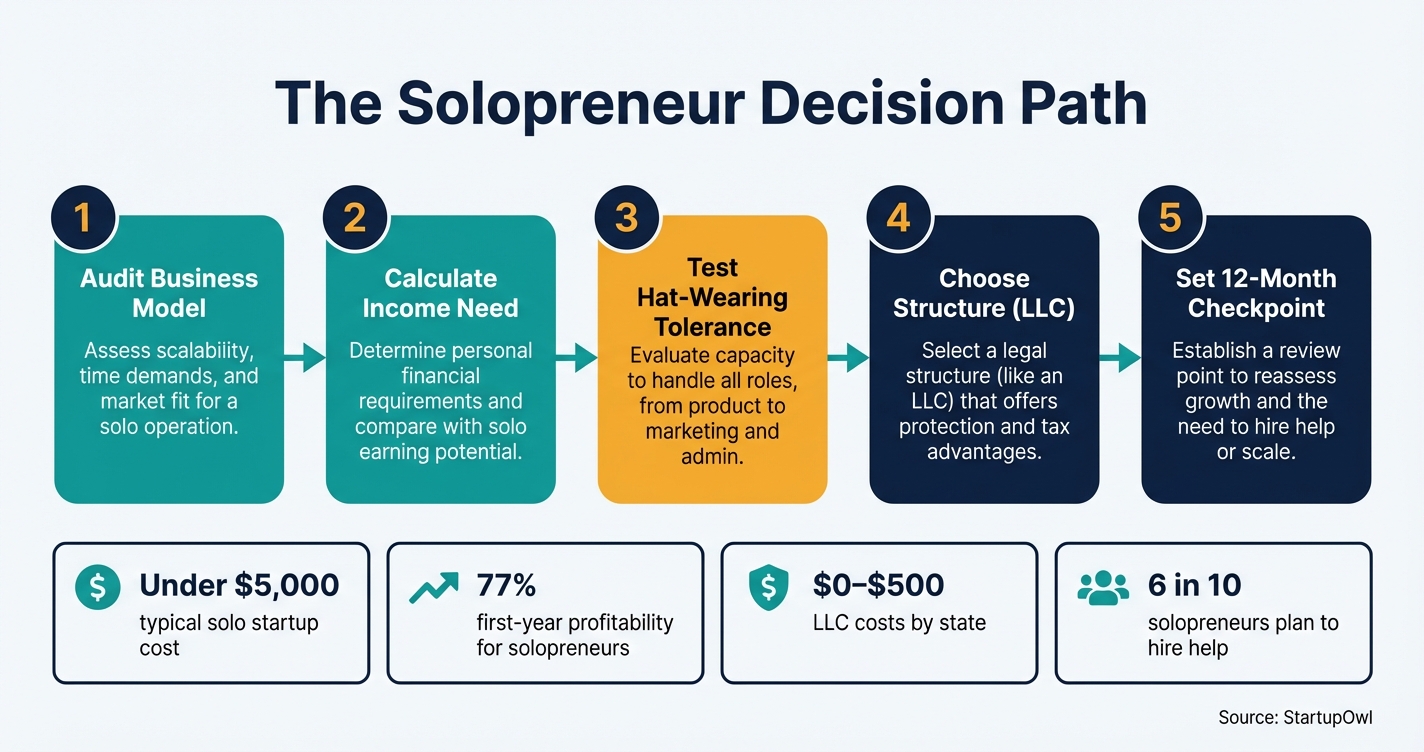

Your answer depends on three things: how you want to spend your time, how much risk you can absorb, and whether your business model requires a team. Here is a step-by-step framework to help you decide.

Step 1: Audit your business model. Service businesses (consulting, freelance writing, design, coaching) work well as solo operations. Product businesses that need manufacturing, inventory, or customer support often require a team. Check out our list of solopreneur business ideas if you want to stay lean.

Step 2: Calculate your minimum viable income. If you need $60,000 or more per year from day one, a solo model is realistic. Nearly half of solopreneurs started with under $5,000 in capital, and 77% were profitable in year one, according to the Gusto 2026 New Business Formation Survey.

Step 3: Test your tolerance for wearing every hat. Solopreneurs handle finance, marketing, fulfillment, and customer service. 41% of solopreneurs report time management as a top operational challenge, according to Leapmesh research. If that sounds unsustainable, the entrepreneur path (with hires) may be a better fit. Read about entrepreneur burnout before committing.

Step 4: Choose your business structure. Both solopreneurs and entrepreneurs benefit from forming an LLC to separate personal and business liability. An LLC costs between $0 and $500 depending on your state. Our guide on how to form an LLC walks you through the process, and you can compare sole proprietorship vs LLC to see which fits.

Step 5: Set a 12-month checkpoint. You do not need to commit forever. Many founders start solo and add team members later. According to the Intuit QuickBooks survey (2024), nearly 6 in 10 solopreneurs plan to hire help in the form of employees, freelancers, or contractors.

The Best Tools for Solopreneurs and Early Entrepreneurs

Your tool stack should match your path. A solopreneur needs lightweight, all-in-one tools. An entrepreneur building a team needs tools that scale with headcount. Here are our top picks for each.

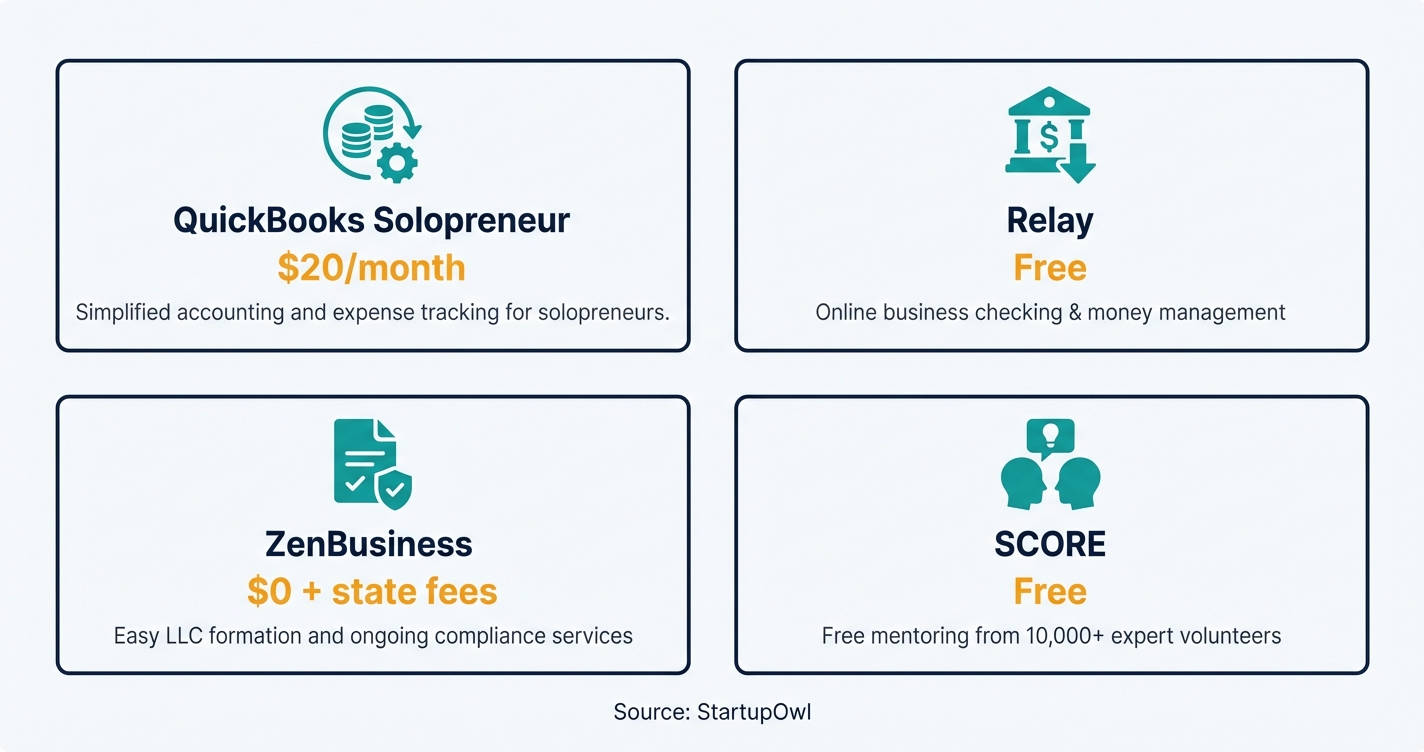

- QuickBooks Solopreneur starts at $20/month and is designed for one-person businesses filing Schedule C. It handles expense tracking, mileage, invoicing, and tax prep with TurboTax integration. Best for solopreneurs. If your business grows past one person, upgrade to QuickBooks Online or another accounting platform.

- Relay offers a free business checking account with no monthly fees, no minimum balance, and up to 20 separate checking accounts. It is ideal for solopreneurs using a Profit First cash-flow method. Compare it to other options in our best business bank accounts guide.

- LegalZoom and ZenBusiness are popular LLC formation services. ZenBusiness starts at $0 plus state fees. LegalZoom starts at $0 plus state fees for basic packages. See our full comparison of LLC formation services.

- SCORE provides free business mentoring through more than 10,000 volunteer mentors at over 300 chapters nationwide. According to SCORE, 87% of entrepreneurs with a mentor are still in business after one year. This is a must-use resource whether you are a solopreneur or an entrepreneur.

Five Mistakes Founders Make When Choosing Between Solo and Team

1. Assuming solopreneur means small. Nonemployer businesses generated $1.8 trillion in total receipts in 2023, according to the U.S. Census Bureau. Solo does not mean small-time.

2. Hiring before you have consistent revenue. Payroll is the fastest way to burn cash. If your monthly revenue is not covering at least 2x an employee's cost, you are not ready. Review our guide on startup funding options before taking on that commitment.

3. Skipping the LLC because you are "just freelancing." A single lawsuit or contract dispute can put your personal assets at risk if you operate as a sole proprietor with no LLC. 86.3% of nonemployer firms are sole proprietorships, according to the SBA Office of Advocacy (2024). Many of them are one accident away from personal liability. Form an LLC to protect yourself.

4. Not separating personal and business finances. Open a dedicated business bank account on day one. Mixing personal and business money creates tax headaches and makes you look unprofessional to clients.

5. Ignoring the transition point. Many successful solopreneurs eventually need to hire. One in three solopreneurs hired at least one contractor in 2024, and over half of those plan to grow their contractor base in 2026, according to the Gusto 2026 survey. Build your systems (documented processes, SOPs, and templates) now so you are ready when the time comes. Read about common first-time founder mistakes for more.

What to Do This Week

Pick one path and take the first step today. If you want to stay solo, start with our Solopreneur Guide and open a free business bank account. If you want to build a team, begin with our guide on how to register your business and explore small business grants for early capital.

Either way, protect yourself by forming an LLC. Our step-by-step guide on how to form an LLC takes you from start to finish in under 30 minutes. You can also grab our free business plan template to map out your first year.

Frequently Asked Questions

A solopreneur runs a business alone with no employees, keeping full control over decisions and operations. An entrepreneur builds a company designed to scale through hiring, management systems, and potentially outside investment. Both can earn six figures or more, but the structure and daily work look very different.

Yes. Many founders start solo and add a team later. According to the Gusto 2026 survey, one in three solopreneurs hired at least one contractor in 2024, and over half of those plan to expand that contractor base. The transition works best when you have documented processes and consistent revenue first.

Not necessarily. About 20% of solopreneurs earn between $100K and $300K per year without hiring, and roughly 3.6% hit $1M+ in annual revenue, per Leapmesh and industry data (as of 2026). Entrepreneurs with teams can scale revenue beyond what one person can deliver, but they also carry higher costs (payroll, benefits, office space).

About 81.9% of all U.S. small businesses have no paid employees, according to the SBA Office of Advocacy (2024 FAQ). That amounts to roughly 28.5 million nonemployer businesses. The share has grown from 76% in 1997 to about 84% today, per the Intuit QuickBooks Small Business Index.

You do not legally need one, but it is strongly recommended. Operating as a sole proprietorship exposes your personal assets (home, savings, car) to business liabilities. A single-member LLC costs between $0 and $500 in state filing fees and takes less than a day to set up. See our sole proprietorship vs LLC comparison for the full breakdown.

Nearly half of solopreneurs started with under $5,000 in capital, and 84% used personal savings as their primary funding source, according to the Gusto 2026 New Business Formation Survey. Service-based solopreneurs (consultants, writers, designers) can launch with a laptop, an internet connection, and a few hundred dollars for an LLC and basic tools.

The information on this page is for educational purposes only and does not constitute financial, legal, or investment advice. Loan terms, interest rates, and eligibility requirements vary by lender and change frequently. Always consult with a qualified financial advisor before making funding decisions. StartupOwl may earn a commission if you click our links at no extra cost to you.

Sources & References

- U.S. Census Bureau Nonemployer Statistics (2022 data, released 2026)

- U.S. Census Bureau: Number of U.S. Nonemployers Grew Faster Than Employer Businesses (July 2026)

- SBA Office of Advocacy: Frequently Asked Questions About Small Business (2024)

- SBA Office of Advocacy: 2026 Small Business Profile

- Gusto 2026 New Business Formation Survey: Behind the Boom in Solopreneurship

- Intuit QuickBooks: 2024 Trends in Self-Employment and Solopreneurship

- Federal Reserve Small Business Credit Survey: 2026 Report on Nonemployer Firms

- SBA: Grow Your Business Through Mentorship (SCORE)

- SCORE: Find a Mentor (Free Business Mentoring)

About the Author

Director of Entrepreneurial Strategy

Jennifer is a former founder who built and sold a boutique B2B logistics company in her thirties. She understands the emotional and strategic toll of building a business from the ground up without a massive safety net. She is deeply connected to the Atlanta startup ecosystem and is passionate about equitable funding.

Was this article helpful?

Questions about Solopreneur vs Entrepreneur

2 comments

Rosa

July 20, 2026

whats the actual difference between calling yourself a solopreneur versus an entrepreneur

Jennifer PayneStartupOwl team

Director of Entrepreneurial Strategy · July 22, 2026

The short version is team. A solopreneur runs the business alone with no employees and keeps full control of every decision. An entrepreneur builds a company meant to scale through hiring, systems, and sometimes outside investment. Both can earn well, the daily work just looks different. It is worth knowing that the vast majority of US small businesses, more than four in five, actually operate with no employees at all. So going solo is not the exception, it is the common path. Which fits depends on whether you want control or scale.

Leave a comment