Business vs Personal Bank Account and Why You Must Separate Them

Separating your business and personal bank accounts costs $0 to $30 per month and protects you from IRS audits, pierced liability, and lost deductions.

In This Article

You need a separate business bank account if you operate an LLC, corporation, or any business that wants clean books. It costs $0 to $30 per month at most providers, takes under 30 minutes to open online, and protects you from IRS audit risk and personal liability for business debts.

6

Total Steps

$0–$50

Est. Cost

1-3 hours

Timeline

Easy

Difficulty

Mixing your business and personal bank accounts can cost you thousands of dollars in lost deductions, IRS penalties, and even personal liability for business debts. Opening a separate business checking account takes about 10 to 30 minutes online and costs $0 per month at fintech providers like Mercury or Bluevine. This guide walks you through six steps to fully separate your finances, protect your LLC or corporation, and keep the IRS happy.

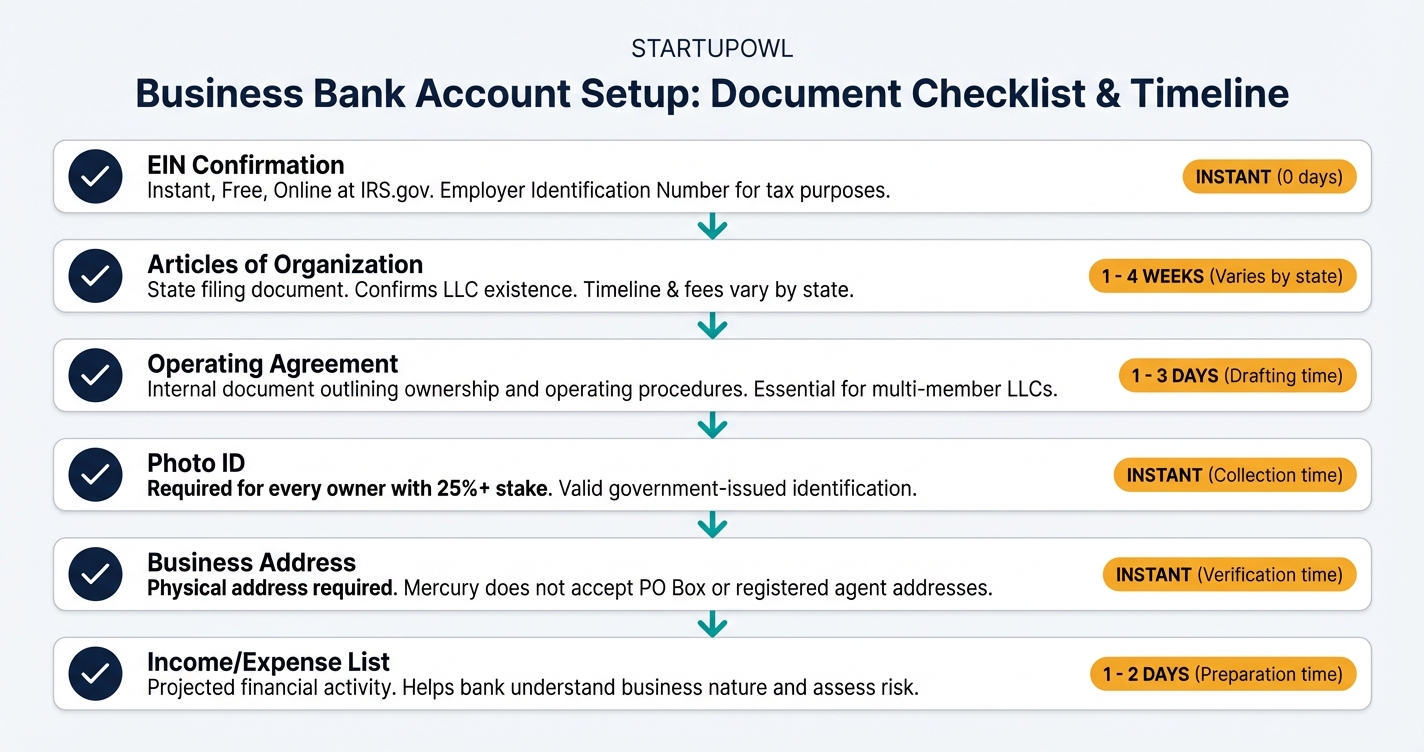

Before you open a business bank account and separate your finances, make sure you have the following items ready. Missing even one document can delay your application by days.

- Employer Identification Number (EIN) from the IRS, or your Social Security Number if you are a sole proprietor without employees. Apply free at IRS.gov. See our EIN application guide for a full walkthrough.

- Formation documents such as Articles of Organization (LLC) or Articles of Incorporation (corporation), filed with your state's Secretary of State.

- LLC operating agreement or corporate bylaws. Some banks will not open your account without one. Get started with our LLC operating agreement guide.

- Government-issued photo ID (driver's license or passport) for every owner holding 25% or more of the business.

- Business address and phone number that match your formation documents. A home address works for most fintechs, but Mercury does not accept registered agent or PO Box addresses.

- A list of all business income sources and recurring expenses currently running through your personal account. You will need this to complete the migration in Step 4.

The entire process of separating your business and personal finances takes 1 to 3 hours spread across a few days. The account application itself takes 10 minutes at most fintech providers. Approval timelines vary: Mercury typically approves within 1 to 2 business days, while traditional banks may take 3 to 5 business days and sometimes require an in-branch visit.

The most time-consuming part is Step 4: migrating all your income and expense flows. Expect to spend 1 to 2 hours logging into every payment processor, subscription service, and client portal to update your banking information. Some payment processors (like Stripe) require 1 to 2 business days to verify new bank details via micro-deposits.

You may feel tempted to keep "just a few" business expenses on your personal card for convenience. Do not. Even a single commingled transaction weakens your liability protection and creates bookkeeping headaches. Set a hard cutoff date and stick to it.

Step-by-Step Process

- 1

Get Your EIN and Gather Formation Documents

Before you can open a business bank account, you need your Employer Identification Number (EIN) from the IRS. If you have not already applied for one, you can get it instantly online at IRS.gov during business hours (Mon-Fri, 7am-10pm ET). Sole proprietors without employees can use their Social Security Number instead.

Gather your Articles of Organization (for LLCs) or Articles of Incorporation, your LLC operating agreement, and a government-issued photo ID for every owner with 25% or more ownership. You will also need your business address and phone number.

Tips

- Apply for your EIN online between 7am and 10pm ET to get it instantly; fax and mail applications take 4 to 6 weeks.

- Save your EIN confirmation letter (CP 575) as a PDF because you will need it for every bank application.

- If you formed your LLC through a service, your Articles of Organization are usually in your account dashboard.

Common Mistakes

- Paying a third-party service $50 to $150 for an EIN when the IRS issues them for free at IRS.gov.

- Not having your operating agreement ready, which some banks require before they will open your account.

- 2

Choose Between a Fintech or Traditional Business Bank

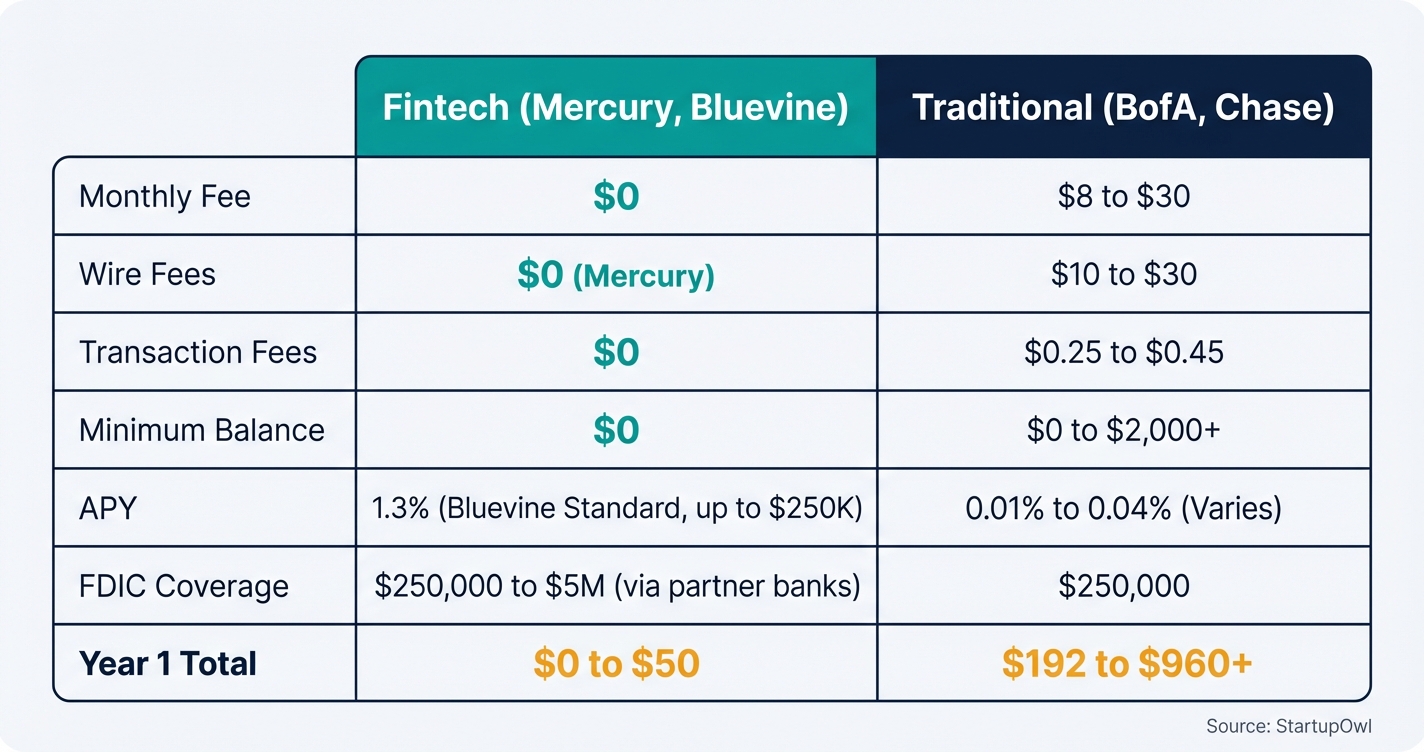

Your first big decision is whether to go with an online-only fintech bank or a traditional bank with branch access. Fintech options like Mercury and Bluevine charge $0 per month with no minimum balance. Traditional banks like Bank of America charge $16 to $29.95 per month unless you maintain $5,000 to $25,000 in minimum balances.

If you handle cash deposits regularly (restaurants, retail), you need a traditional bank. If your business is digital (consulting, e-commerce, SaaS), a fintech account saves you $192 to $360 per year in monthly fees alone. Compare options on our best business bank accounts page.

Tips

- Mercury offers free domestic and international USD wire transfers, which saves $15 to $30 per wire versus traditional banks.

- Bluevine's Standard plan pays 1.3% APY on balances up to $250,000 with no monthly fee if you meet activity requirements.

Common Mistakes

- Choosing a bank solely based on the monthly fee without calculating total cost including wire fees, transaction limits, and cash deposit charges.

- Picking a traditional bank with a $5,000 minimum balance when your average balance hovers around $2,000, costing you $16 to $30 monthly.

- 3

Open Your Business Checking Account Online or In-Branch

Apply for your business checking account using the documents you gathered in Step 1. Most fintech applications take 10 minutes online and are approved within 1 to 2 business days. Traditional bank applications can be completed in-branch or online, but approval may take 3 to 5 business days.

You will need to provide your EIN, formation documents, government ID for each owner, business address, and an initial deposit (some fintechs require $0; traditional banks may require $25 to $100). For a detailed walkthrough, see our how to open a business bank account guide.

Tips

- Mercury's application takes about 10 minutes and approvals typically come in 1 to 2 business days.

- Some banks like Chase offer sign-up bonuses of up to $500 for new business checking customers who meet deposit requirements.

- Open a business savings account at the same time to separate your operating cash from your tax reserve fund.

Common Mistakes

- Entering your personal address instead of your registered business address, which can delay approval.

- Forgetting to fund the account within the required timeframe, which some banks treat as grounds for automatic closure.

- 4

Move All Business Income and Expenses to the New Account

This is the most critical step. Update your payment processors (Stripe, PayPal, Square), client invoices, and any recurring revenue sources to deposit into your new business account. Then redirect all business expenses (software subscriptions, vendor payments, advertising) to pay from the business account or a linked business debit or credit card.

Set a firm cutoff date. After that date, zero business transactions should flow through your personal account. If you accidentally pay a business expense from your personal account, reimburse yourself from the business account and document it. This clean separation is what protects your LLC's liability shield and keeps your books audit-ready.

Tips

- Create a spreadsheet listing every recurring charge and income source so you do not miss any during the switch.

- Pay yourself a regular owner's draw or salary through a formal transfer rather than pulling cash as needed.

Common Mistakes

- Leaving one or two subscriptions on your personal card, which creates commingling that weakens your liability protection.

- Not updating your direct deposit information with clients, so payments continue landing in your personal account for months.

- 5

Connect Your Business Account to Accounting Software

Link your new business bank account to accounting software like QuickBooks ($35 per month) or Xero ($29 per month) within the first week. This creates an automatic transaction feed that categorizes your income and expenses in real time. Mercury syncs directly with QuickBooks, Xero, and NetSuite. Bluevine offers up to 6 months free Xero for Plus and Premier plan customers.

Automatic syncing eliminates manual data entry and reduces bookkeeping errors. Without it, you are stuck downloading CSV files and manually reconciling (which costs $50 to $150 per month in extra bookkeeper time). For more options, check our best accounting software for small business comparison.

Tips

- Set up bank rules in QuickBooks or Xero so recurring expenses auto-categorize, saving you 2 to 3 hours of bookkeeping per month.

- Review uncategorized transactions weekly rather than monthly to avoid a pile-up at tax time.

- Bluevine offers 3 to 6 months of free Xero depending on your plan tier.

Common Mistakes

- Connecting your personal bank account to your business accounting software, which imports personal transactions and creates a mess.

- 6

Set Up a Monthly Reconciliation Routine

Block 30 minutes on the last business day of each month to reconcile your business bank account against your accounting software. This means confirming every transaction in your bank statement matches your books. QuickBooks and Xero both have built-in reconciliation tools that make this a guided, check-the-box process.

Monthly reconciliation catches errors, duplicate charges, and unauthorized transactions before they snowball. It also means your books are always audit-ready. If you skip reconciliation for 3 or more months, expect to spend 2 to 4 hours (or $100 to $300 in bookkeeper fees) cleaning up the backlog. For deeper guidance on accounting workflows, see how to set up small business accounting.

Tips

- Set a recurring calendar reminder for the last business day of each month so reconciliation becomes habit.

- If your balance is off by even $1, track down the discrepancy immediately rather than adjusting it away.

Common Mistakes

- Skipping reconciliation for months, then scrambling at tax time when your books do not match your bank statements.

Separating your business and personal bank accounts can cost as little as $0 per month if you choose a fintech provider. Here is the realistic year-one cost breakdown.

A free fintech checking account (Mercury or Bluevine Standard) with free accounting software (Wave) brings your total annual cost to $0. If you choose QuickBooks Simple Start at $35 per month and a traditional bank at $16 per month, your annual cost is about $612. Most new businesses land somewhere in between at $300 to $600 per year for banking and accounting combined.

The real cost of not separating is far higher. Disallowed deductions during an IRS audit can add $2,000 to $10,000+ to your tax bill depending on your revenue. Pierced corporate veil liability can expose your personal home, savings, and other assets to business creditors. For a detailed fee comparison, see our business bank account fees breakdown.

Once your business bank account is open and all transactions are flowing through it, take these immediate next steps to maximize the value of your separation.

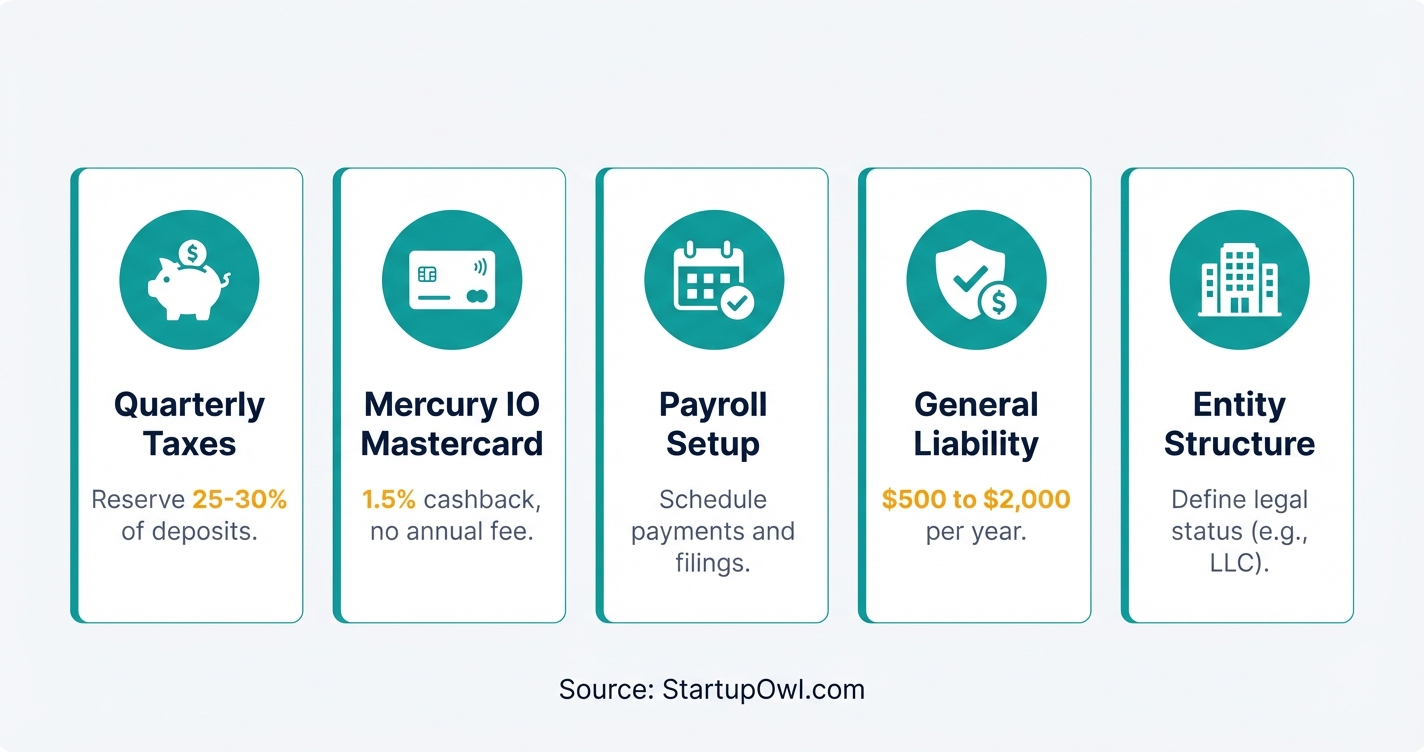

- Open a business savings account at the same bank. Transfer 25% to 30% of every deposit into it for estimated quarterly tax payments. This prevents the common cash crunch when IRS payments come due.

- Get a business credit card to separate business purchases further and build business credit. Mercury's IO Mastercard offers 1.5% cashback with no annual fee. Bluevine offers a Business Cashback Mastercard as well.

- Set up payroll if you plan to pay yourself a salary (required for S Corps). See our how to set up payroll guide. Best payroll services start at about $40 per month.

- Review your business insurance needs now that your finances are separated. A general liability insurance policy typically costs $500 to $2,000 per year and protects your business from third-party claims.

- Consider your entity structure. If you are still a sole proprietor, separating your bank accounts is a good first step, but it does not give you the liability protection of an LLC. Compare options in our LLC vs S Corp tax comparison.

The Complete Checklist

- Apply for an EIN at IRS.gov01

Get your Employer Identification Number online for free in under 10 minutes.

10 minutes$0 - Gather formation documents and owner IDs02

Collect Articles of Organization, operating agreement, and government photo IDs for all 25%+ owners.

15 minutes$0 - Compare fintech and traditional bank options03

Evaluate Mercury, Bluevine, Chase, and Bank of America based on fees, features, and cash deposit needs.

15-30 minutes$0 - Open your business checking account04

Apply online or in-branch and fund the account with your initial deposit.

10 minutes to apply; 1-5 days for approval$0 to $100 - Update payment processors to deposit into the business account05

Redirect Stripe, PayPal, Square, and all client payment sources to your new business account.

30 minutes$0 - Move all recurring business expenses to the business account06

Switch software subscriptions, vendor payments, and advertising spend to your business debit card or account.

30-60 minutes$0 - Set a firm cutoff date for personal account usage07

After this date, zero business transactions should touch your personal account.

5 minutes$0 - Connect your bank account to accounting software08

Link to QuickBooks, Xero, or Wave for automatic transaction syncing.

15 minutes$0 to $50 per month - Set up bank rules for auto-categorization09

Create rules in your accounting software so recurring transactions categorize automatically.

20 minutes$0 - Schedule your first monthly reconciliation10

Block 30 minutes on the last business day of the month to reconcile your bank statement against your books.

30 minutes per month$0

These are the most expensive mistakes new business owners make when separating (or failing to separate) their business and personal bank accounts.

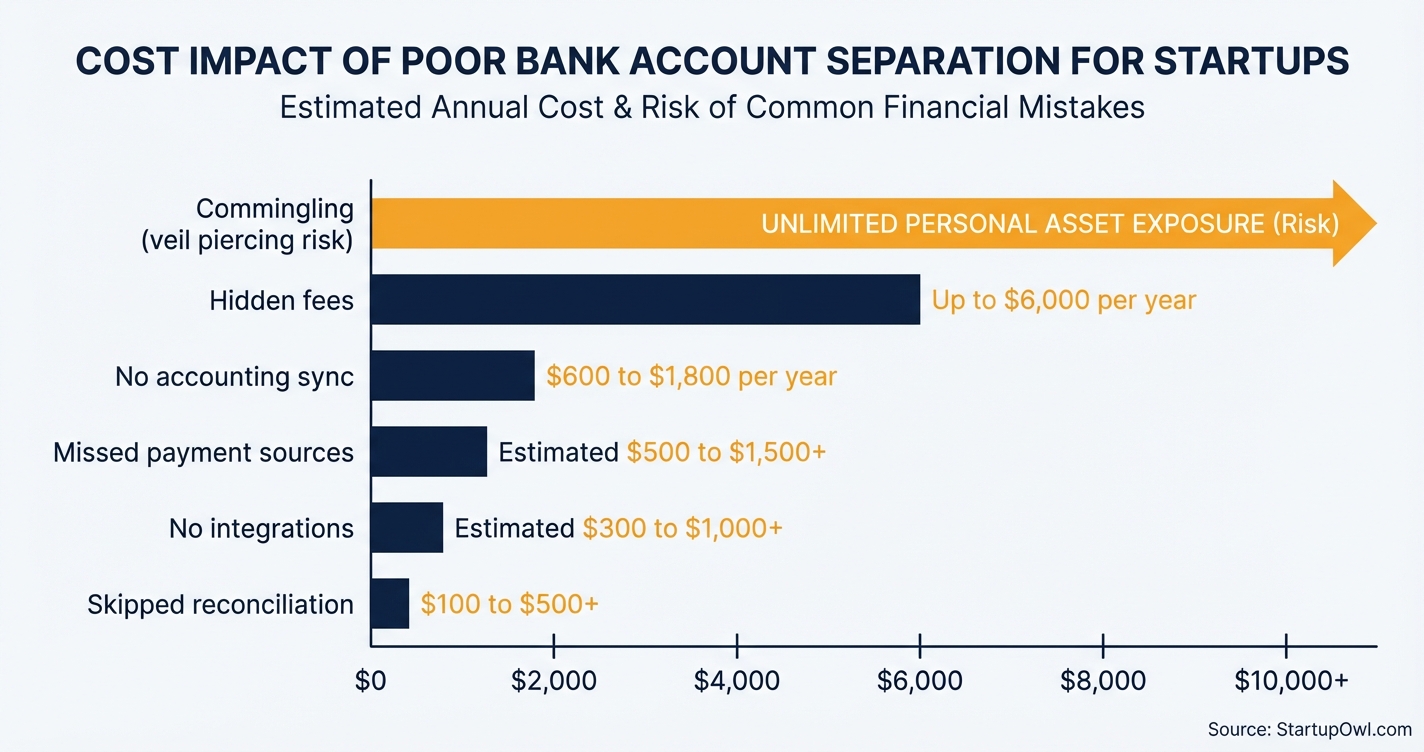

- Using your personal account "just for now." There is no such thing as temporary commingling. Every business transaction through your personal account weakens your LLC's liability shield. Courts have pierced the corporate veil of LLCs specifically because owners commingled personal and business funds, exposing the owner's home, savings, and personal assets to business creditors.

- Ignoring transaction fees beyond the monthly rate. A business checking account advertised at $15 per month can actually cost $45+ per month once you add wire transfer fees ($10 to $30 each), excess transaction charges ($0.30 to $0.65 each after your monthly limit), and cash deposit fees. Always calculate your total cost of banking, not just the headline fee. See our business bank account fees guide for details.

- Not connecting to accounting software. Without an automatic bank feed, you are stuck with manual data entry. That means more bookkeeper hours ($50 to $150 per month extra) and a higher risk of miscategorized expenses that trigger IRS questions.

- Failing to update all payment sources on migration day. If even one client keeps depositing into your personal account, you have commingled funds again. Create a comprehensive list of every income source and expense before you switch.

- Choosing a bank without integration support. If your bank cannot sync with QuickBooks, Xero, or your preferred accounting tool, you will waste hours on manual reconciliation every month. Verify software compatibility before you open the account.

- Skipping monthly reconciliation. Unreconciled accounts accumulate errors. After 3 months of skipped reconciliation, expect to spend 2 to 4 hours (or pay a bookkeeper $100 to $300) to clean up the backlog. After 12 months, the cleanup can cost $500+.

Frequently Asked Questions

Technically, yes. The IRS does not require sole proprietors to have a separate business bank account. But the IRS itself recommends keeping separate accounts because it makes tracking deductions easier. Commingling funds increases your audit risk, and any deduction you cannot clearly document may be disallowed. Open a free business account at Mercury or Bluevine and avoid the risk entirely.

Fintech accounts at Mercury and Bluevine cost $0 per month with no minimum balance. Traditional banks charge $8 to $30 per month, though you can often waive the fee by maintaining a $5,000 to $25,000 minimum balance. Hidden costs like wire transfer fees ($10 to $30 each) and excess transaction fees ($0.30 to $0.65 per transaction) can add up quickly at traditional banks.

The IRS may disallow your business deductions, assess back taxes, and add penalties plus interest. In more serious cases, they may open a fraud investigation. At a minimum, expect to provide detailed documentation proving each expense was legitimate. Disallowed deductions alone can add $2,000 to $10,000+ to your tax bill depending on your revenue.

Yes, it is one of the most common reasons courts pierce the corporate veil. When you mix personal and business funds, a court may decide your LLC is not a separate legal entity, which means creditors can pursue your personal assets (home, savings, car) to satisfy business debts. Single-member LLCs are especially vulnerable to veil-piercing claims.

The application takes 10 minutes at most fintech providers. Mercury approves most accounts within 1 to 2 business days. Traditional banks may take 3 to 5 business days and could require an in-person branch visit. Have your EIN, formation documents, and photo ID ready to avoid delays.

Both charge $0 per month on their base plans. Mercury offers free domestic and international USD wire transfers and up to $5 million in FDIC coverage through its sweep network, making it ideal for businesses that send frequent wires. Bluevine pays 1.3% APY on balances up to $250,000 (with activity requirements), so it wins if you want to earn interest on idle cash. Neither accepts cash deposits.

Sources & References

- IRS: Apply for an Employer Identification Number (EIN) Online

- IRS: Income & Expenses (Sole Proprietor Personal vs Business)

- IRS Internal Revenue Manual 4.10.4: Examination of Income (Commingling Analysis)

- Mercury Business Banking: Pricing

- Bluevine Business Checking: Plans and Pricing

- Bank of America: Business Schedule of Fees (February 2026)

- Nolo: Piercing the Corporate Veil (LLCs and Corporations)

- Business.com: Business Banking Fees

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Business vs Personal Bank Account

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment