What Is General Liability Insurance and How to Get It for Your Business

General liability insurance protects your business from third-party injury and property damage claims. Here is what it covers, what it costs, and how to buy it.

In This Article

General liability insurance protects your business if a customer gets hurt on your premises, you damage someone else's property, or you face an advertising injury claim like libel or slander. Most small businesses pay $45 to $104 per month, and you can buy a policy entirely online in under 10 minutes with coverage starting the same day.

6

Total Steps

$19–$300

Est. Cost

30 minutes to 2 hours

Timeline

Easy

Difficulty

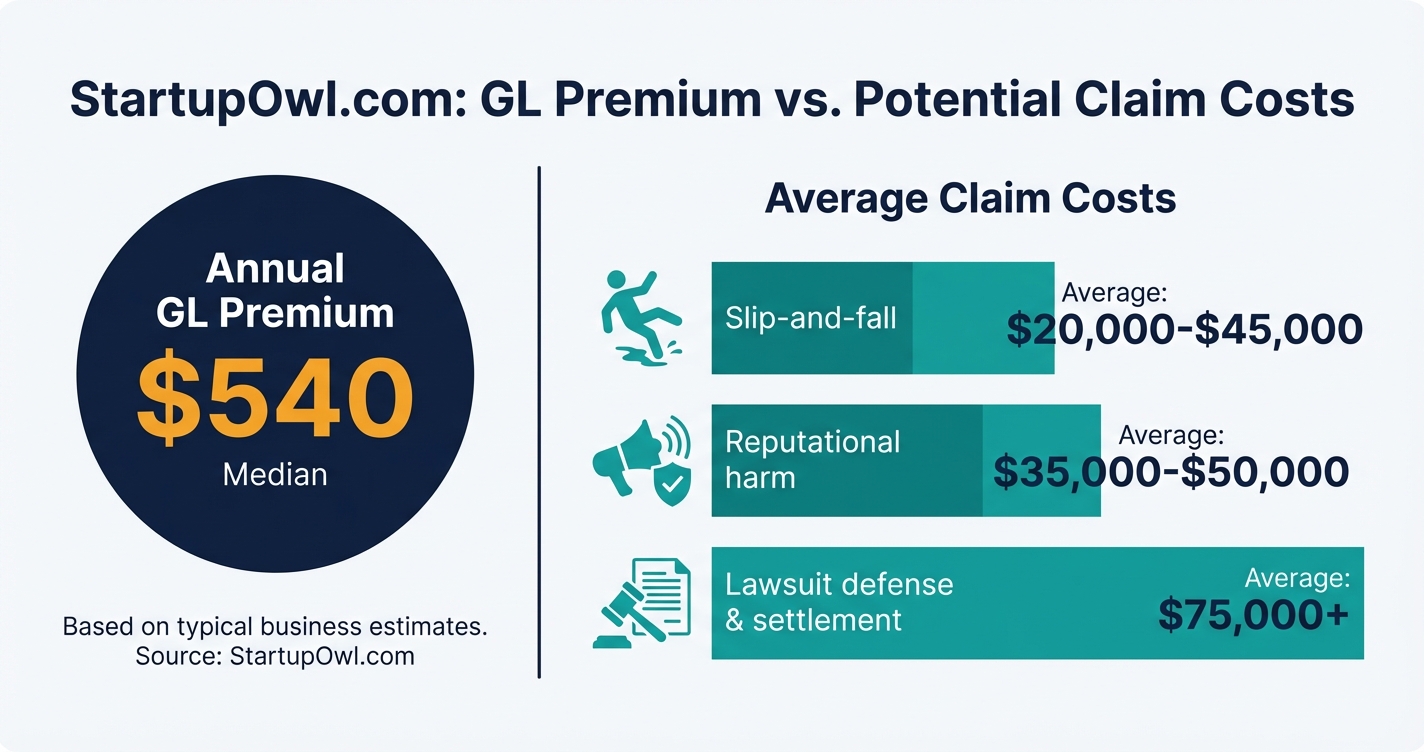

General liability insurance is the single most common policy small businesses buy, and it costs a median of $45 per month (about $500 to $540 per year) according to Insureon's 2026 data. It covers third-party bodily injury, property damage, and advertising injury claims that could otherwise cost you $20,000 to $75,000+ per incident. You can get a policy online in under 10 minutes from providers like NEXT Insurance, The Hartford, or Progressive, and most new businesses qualify immediately.

Before you shop for general liability insurance, gather these four items. Having them ready saves you from abandoned applications and delays.

- Your EIN or SSN (sole proprietors can use their SSN). If you do not have an EIN yet, see our EIN application guide to get one free from the IRS in about 10 minutes.

- Your estimated annual revenue for the current year. Insurers use this to gauge your exposure level. Be accurate because underreporting can lead to claim denials.

- Your employee count and payroll estimate. Businesses with 1-4 employees pay an average of $123/month nationally. Moving from 1-4 to 5-9 employees increases premiums by roughly 168%.

- Any contract or lease requirements. Many landlords and enterprise clients require $1M/$2M coverage limits and want to be listed as an additional insured on your policy.

If you have already formed your LLC or corporation, your business structure provides some personal liability protection. But as the SBA notes, that protection has limits, and insurance fills the gaps.

Getting general liability insurance is one of the fastest business setup tasks. Most online providers issue instant quotes, and you can have active coverage within 10 to 30 minutes. There is no waiting period, inspection, or approval delay for most low-to-medium risk businesses.

Here is what the process actually feels like. You fill out a short online form with your business details (industry, revenue, location, employee count). The system generates a quote instantly or within a few minutes. You review coverage limits, deductible, and exclusions, adjust as needed, and pay. Your policy and Certificate of Insurance (COI) are available immediately.

High-risk businesses like contractors or manufacturers may face a slightly longer process. Some insurers require additional underwriting review, which can take 1 to 3 business days. If you have a prior claims history, expect the review to take longer and your quotes to be 25% to 50% higher than the standard rate for 3 to 5 years after a claim.

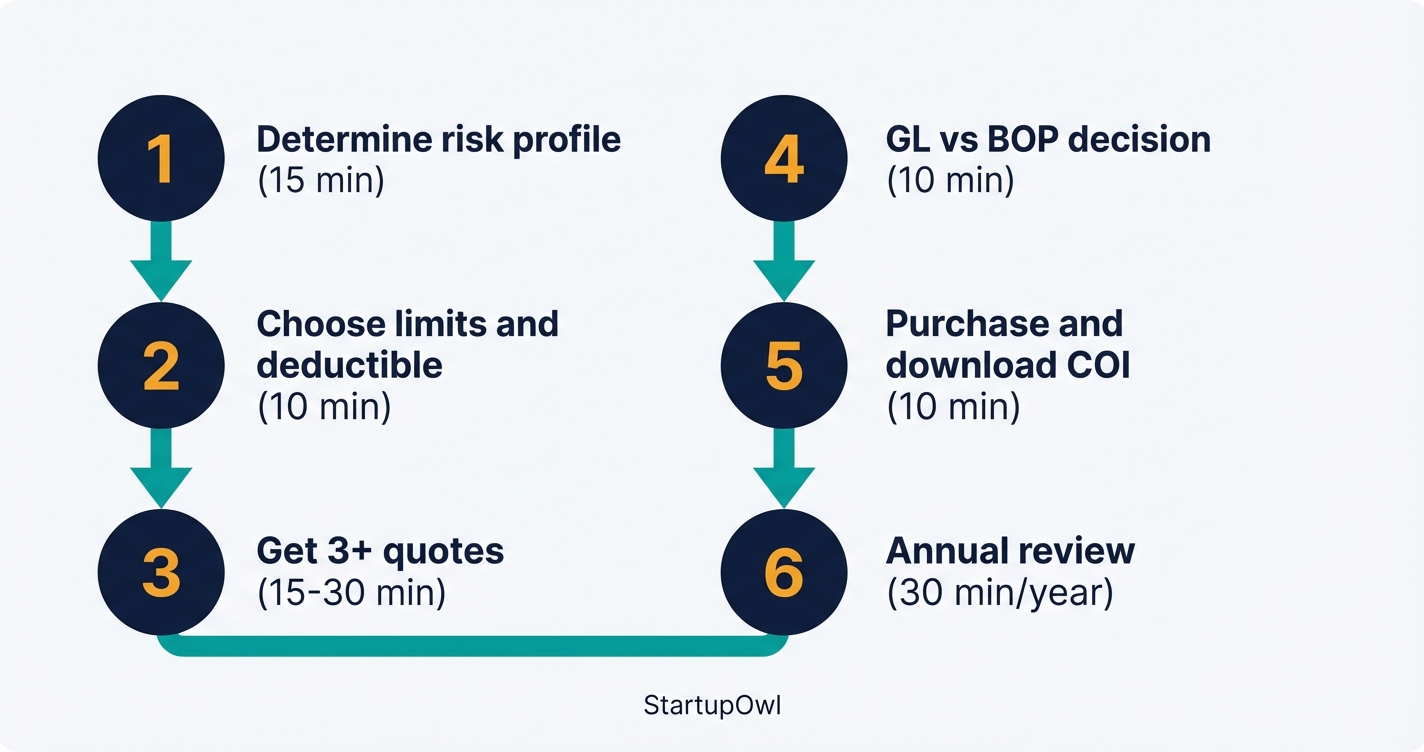

Step-by-Step Process

- 1

Determine Your Risk Profile and Coverage Needs

Your industry is the single biggest factor in what you will pay for general liability insurance. Low-risk businesses (consultants, IT companies, home-based businesses) pay $19 to $50 per month, while medium-risk businesses (retail, restaurants, salons) pay $50 to $150 per month. High-risk businesses like general contractors or roofers pay $150 to $417+ per month.

Write down your annual revenue, number of employees, business location, and the type of work you do. If you have a physical location with customer foot traffic, you face higher slip-and-fall risk. If you work from home as a solo consultant, your risk profile is low. Check whether any landlords, clients, or licensing boards require you to carry a specific coverage amount before you start shopping.

Tips

- If a client or landlord requires proof of insurance, ask them for the exact coverage limits they need before you buy a policy.

- Businesses with 1-4 employees pay an average of $123/month nationally for $1M/$2M limits, so use that as your benchmark.

- Check your state insurance commissioner website for any industry-specific GL requirements in your jurisdiction.

Common Mistakes

- Guessing your revenue or employee count when getting quotes leads to inaccurate pricing and potential claim denials later.

- Not checking client contract requirements before buying a policy, then needing to upgrade immediately at a higher cost.

- 2

Choose Your Coverage Limits and Deductible

The standard general liability policy uses $1 million per occurrence and $2 million aggregate limits. This means your insurer pays up to $1 million for a single claim and up to $2 million total during the policy year. Most Insureon customers choose these limits, and they are sufficient for the majority of small businesses.

Your deductible is what you pay out of pocket before coverage kicks in. The most common deductible is $500, but you can choose $1,000 to $2,500 to lower your monthly premium by 15% to 25%. Only raise your deductible if you can comfortably afford to pay it in a crisis. If you handle SBA-backed loans or sign contracts with enterprise clients, they may require minimum limits of $1M/$2M or higher.

Tips

- The $1M/$2M limit is the industry standard and what most landlords and clients expect to see on your Certificate of Insurance.

- Raising your deductible from $500 to $2,500 can save roughly $50/month, but make sure you have that cash available.

Common Mistakes

- Choosing the lowest possible limits to save $10-$20/month, then facing a $45,000 slip-and-fall claim that exceeds your coverage.

- 3

Get Quotes from at Least Three Providers

Every insurer uses its own pricing formula, so the same business can get quotes that differ by 30% to 50% across carriers. Start with at least three providers. NEXT Insurance starts at $19/month for low-risk businesses and nearly half their customers pay $45 or less. The Hartford averages about $67 to $83/month and is the cheapest option in 42 states according to MoneyGeek's 2026 analysis. Progressive averages $85/month.

Online brokerages like Insureon let you compare quotes from multiple carriers in a single application. You can also use Coverdash for instant quotes. Expect each application to take 5 to 10 minutes with basic business details.

Tips

- Use an online brokerage like Insureon to compare multiple carriers in one application rather than filling out separate forms for each insurer.

- Ask about multi-policy discounts. Bundling GL with workers' comp or property insurance can save 10% to 15%.

- Pay attention to exclusions, not just price. One policy might exclude a coverage scenario another policy includes.

Common Mistakes

- Buying the first quote without comparing. You could easily overpay by $200 to $600 per year.

- Focusing only on the premium and ignoring the deductible, exclusions, or aggregate limit differences between policies.

- 4

Decide Between Standalone GL or a Business Owner's Policy

A Business Owner's Policy (BOP) bundles general liability with commercial property insurance (and usually business interruption coverage) at a discount. The average BOP costs about $57 to $150 per month according to Homebase and Insureon data (as of 2026), compared to $45/month for standalone GL. If you have a physical location, inventory, or equipment, a BOP usually saves you 15% to 30% versus buying GL and property coverage separately.

If you are a home-based consultant or freelancer with no commercial property to insure, standalone GL is probably all you need. If you run a retail store, restaurant, or salon, a BOP is almost always the better deal. NEXT Insurance offers BOPs starting at $25/month.

Tips

- If you lease commercial space, your landlord likely requires both GL and property insurance. A BOP covers both in one policy.

- BOPs are typically available to businesses with 100 or fewer employees and under $5M in annual revenue.

Common Mistakes

- Buying standalone GL and standalone property insurance separately when a BOP would cost 15-30% less for the same coverage.

- 5

Purchase Your Policy and Download Your Certificate of Insurance

Once you pick a provider and policy, you can complete the purchase online. Most digital-first insurers like NEXT Insurance let you buy and activate coverage in about 10 minutes. You will need your EIN (or SSN for sole proprietors), business address, revenue estimate, and a payment method. Many insurers offer both monthly and annual payment options.

Paying annually instead of monthly saves you 8% to 12% in financing fees. On a $1,200/year policy, that is roughly $100 to $150 in savings. After purchase, immediately download your Certificate of Insurance (COI). You will need this to show landlords, clients, and licensing boards. Most online platforms generate the COI instantly. If you need to add an "additional insured" (a landlord or client who wants to be named on your policy), you can usually do that through your provider's online portal at no extra charge.

Tips

- Pay annually if you can afford it. You will save $100-$150/year on a typical policy by avoiding monthly installment fees.

- Download and save your COI immediately. Landlords and clients will ask for it, sometimes on short notice.

Common Mistakes

- Forgetting to add a landlord or general contractor as an additional insured, which can delay or void your lease or contract.

- 6

Review and Reassess Your Policy Annually

Your general liability needs change as your business grows. If you hire employees, increase revenue, add a physical location, or expand into new services, your coverage limits may need to increase. The SBA recommends reassessing your coverage every year. Filing a claim can raise your premiums by 25% to 50% for 3 to 5 years, so maintaining a clean claims history is worth the effort.

Shop around at renewal time. Insurance rates vary year to year, and you may find a better rate by switching carriers. Implementing documented safety programs (slip-resistant floors, maintenance logs, employee training) can earn 5% to 15% premium discounts from many carriers. Review your best business insurance options every 12 months to make sure you are not overpaying.

Tips

- Set a calendar reminder 30 days before your policy renewal to shop competing quotes.

- Document any safety improvements you have made. Many insurers offer 5-15% discounts for formal safety programs.

- If your revenue grew significantly, tell your insurer. Underreporting revenue can lead to claim denials.

Common Mistakes

- Auto-renewing without shopping around. Rates shift every year, and you could save $200-$600 annually by comparing.

- Failing to update your policy when you add employees or locations, leaving gaps in coverage.

General liability insurance costs vary enormously by industry, but here are the real benchmarks as of 2026. The median Insureon customer pays $45/month ($538/year) for a standard $1M per occurrence / $2M aggregate policy. The national average for businesses with 1-4 employees is $123/month ($1,474/year) according to MoneyGeek's analysis of 408 industries across all 50 states.

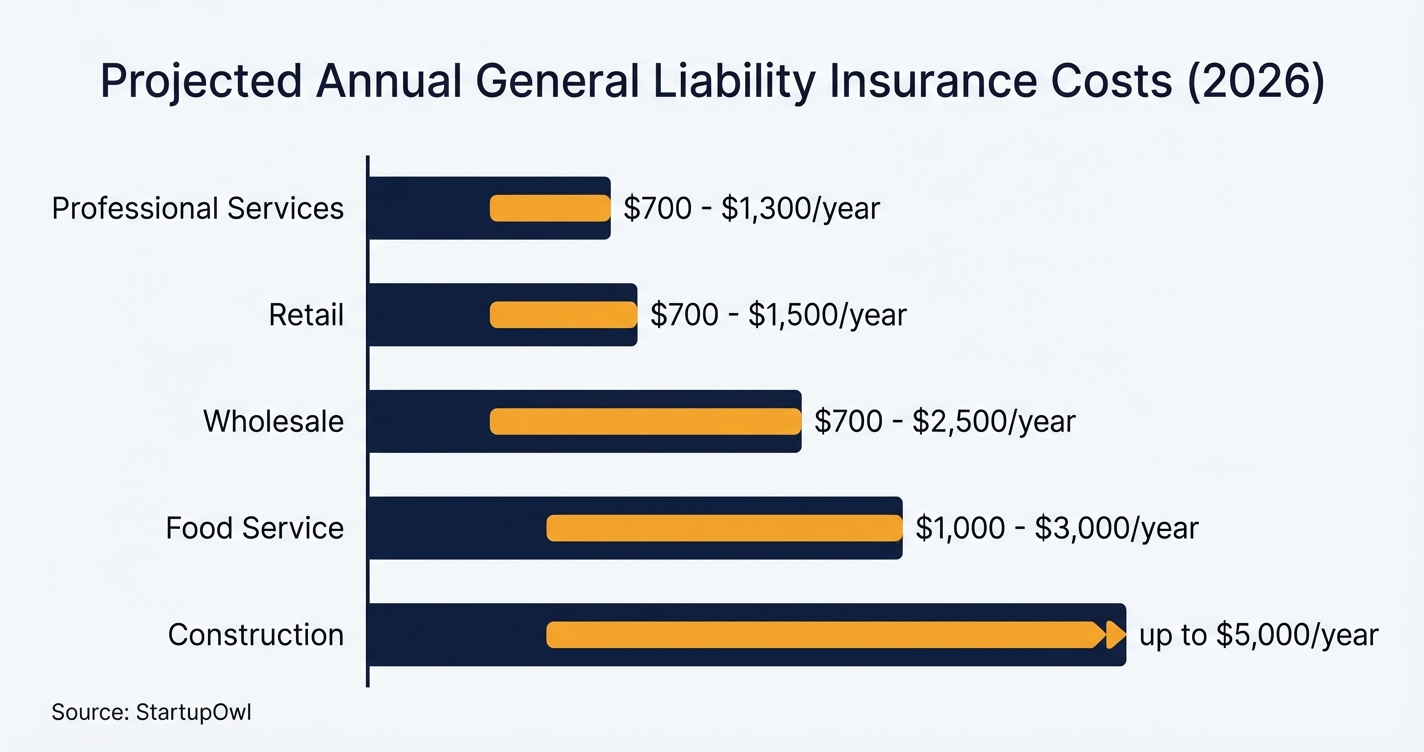

Industry-specific ranges for businesses under $1M in revenue (Coverdash/NerdWallet 2026 data):

- Professional services and tech: $700 to $1,300/year ($58 to $108/month)

- Retail: $700 to $1,500/year ($58 to $125/month)

- Wholesale trade: $700 to $2,500/year ($58 to $208/month)

- Food service and restaurants: $1,000 to $3,000/year ($83 to $208/month)

- Construction: Up to $5,000/year (up to $417/month)

Location matters too. New York businesses pay roughly $1,444/year for the same coverage that costs $1,076/year in Maine or North Carolina. States with higher litigation rates and court awards push premiums up by as much as 34%.

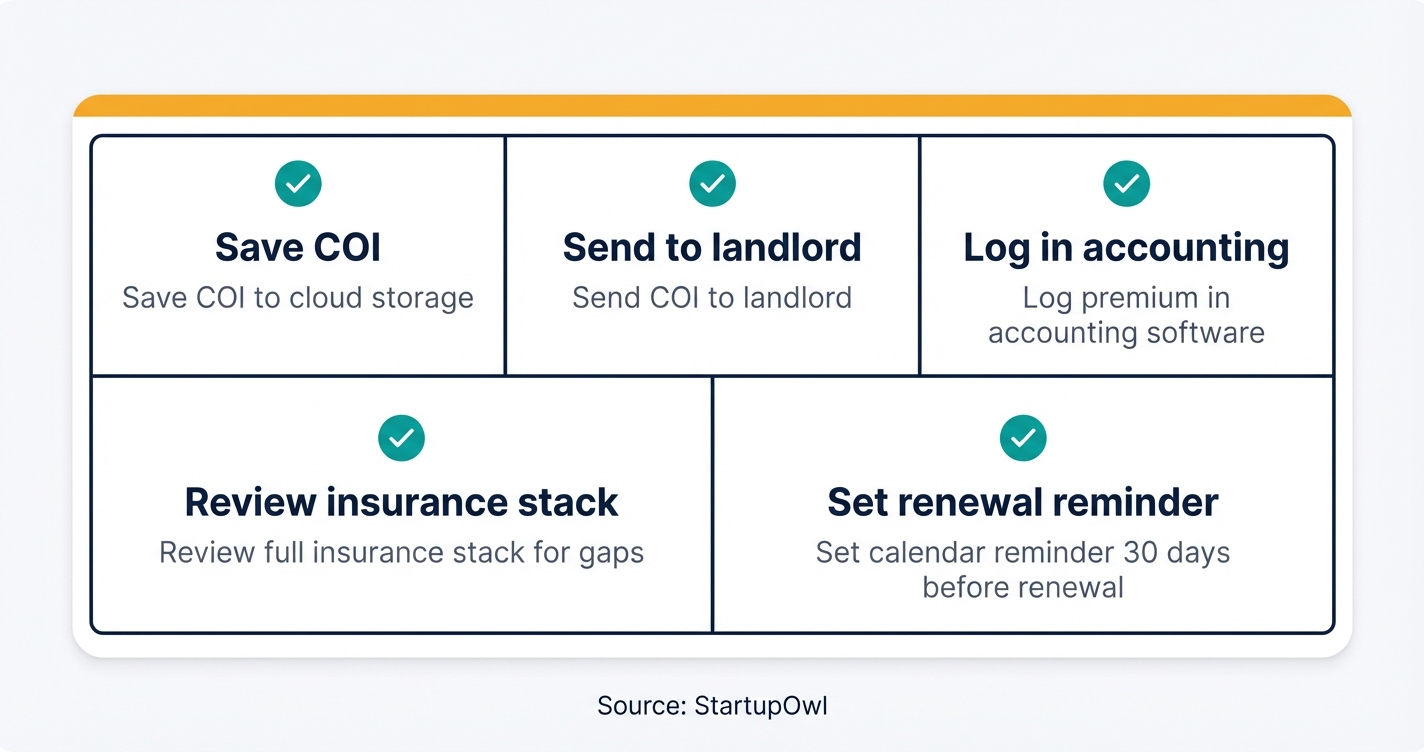

Once your general liability policy is active, take these follow-up steps in the next 24 hours to make sure your coverage actually works when you need it.

- Save your COI in cloud storage. Upload a copy to Google Drive or Dropbox so you can share it instantly when a client or landlord asks for proof of insurance.

- Send your COI to your landlord. If you lease commercial space, your landlord likely requires proof of GL coverage. Send it proactively to avoid lease compliance issues.

- Set up your accounting. Your GL premium is a tax-deductible business expense. Log it in your accounting software under insurance expenses.

- Review your full insurance stack. GL does not cover employee injuries (you need workers' comp), professional errors (you need E&O insurance), or your own property (you need commercial property insurance). Visit our best business insurance guide to identify any remaining coverage gaps.

- Add a renewal reminder. Set a calendar alert for 30 days before your policy renewal date to shop competing quotes and reassess your coverage needs.

The Complete Checklist

- Identify your industry risk category (low, medium, high)01

Your industry is the biggest factor in your premium and determines your starting price range.

5 minutes$0 - List your annual revenue, employee count, and business location02

Insurers use these three data points alongside industry to calculate your quote.

5 minutes$0 - Check client and landlord insurance requirements03

Review any contracts or lease agreements that specify minimum coverage limits or additional insured requirements.

10 minutes$0 - Choose coverage limits ($1M/$2M is standard)04

Select per-occurrence and aggregate limits that match your risk level and contract requirements.

5 minutes$0 - Choose your deductible ($500 is most common)05

Higher deductibles lower your premium but increase your out-of-pocket cost per claim.

5 minutes$0 - Get quotes from at least 3 providers06

Use Insureon, NEXT Insurance, and The Hartford as a starting set to compare pricing and coverage.

15-30 minutes$0 - Decide between standalone GL and a BOP07

If you have a physical location or inventory, a BOP bundles GL with property coverage at a 15-30% discount.

10 minutes$0 - Purchase your chosen policy08

Complete the online application and make your first payment. Coverage often starts the same day.

10 minutes$19 to $300+/month - Download your Certificate of Insurance (COI)09

Save a digital and printed copy of your COI to share with landlords, clients, and licensing boards.

2 minutes$0 - Add any required additional insureds to your policy10

Name your landlord, general contractor, or major client on the policy if their contract requires it.

5 minutes$0 (usually free)

These are the most expensive mistakes small business owners make with general liability insurance. Each one has a specific dollar consequence.

- Skipping GL entirely to save money. A single slip-and-fall claim averages $20,000 to $45,000. A general liability lawsuit can average over $75,000 to defend and settle. For a policy that costs $45 to $104/month, the math is simple.

- Choosing the cheapest policy without reading exclusions. Two policies at the same price can have very different exclusion lists. One may cover a specific scenario (like product liability or work on a customer's property) that another policy excludes. Always compare exclusions, not just premiums.

- Underinsuring with low coverage limits. If a claim exceeds your policy limits, you are personally liable for the difference. If your $300,000 limit meets a $500,000 claim, you owe $200,000 out of pocket. The standard $1M/$2M limit costs only marginally more than lower options.

- Not shopping around at renewal. Every insurer uses different pricing formulas. Failing to compare quotes annually means you could be overpaying by $200 to $600+ per year without knowing it.

- Underreporting revenue or employee count. If your insurer discovers you understated your business size, they can deny your claim entirely or rescind your policy. Always provide accurate numbers.

- Forgetting to add an additional insured. Many landlords and general contractors require it. Missing this step can breach your lease or contract, potentially costing you the relationship or your office space.

Frequently Asked Questions

The median cost is $45 per month according to Insureon, but the national average for businesses with 1-4 employees is $123/month per MoneyGeek's 2026 analysis. Low-risk businesses like consultants pay as little as $19 to $50/month, while construction businesses pay up to $417/month.

General liability insurance is not required by federal law for most businesses. However, many landlords, clients, and licensing boards require it before allowing you to work on their premises or sign a contract. Some SBA loans also require GL coverage as a condition of approval.

GL covers three main categories: bodily injury to non-employees (like a customer slip-and-fall), property damage caused by your business operations, and advertising injury (libel, slander, copyright infringement). It pays for medical bills, legal defense costs, and settlements up to your policy limits. It does not cover employee injuries, professional errors, or damage to your own property.

A Business Owner's Policy (BOP) bundles general liability with commercial property insurance at a discount of 15% to 30% compared to buying each separately. If you have a physical location, inventory, or equipment, a BOP is usually the better value. The average BOP costs $57 to $150/month, while standalone GL averages $45/month.

Yes. Sole proprietors and single-member LLCs routinely buy GL coverage. Solo businesses are typically the cheapest to insure, paying roughly 47% below the national average. You can use your SSN instead of an EIN on the application if you have not obtained an EIN yet.

Most online providers issue coverage in 10 minutes or less. NEXT Insurance, Insureon, and Coverdash all offer instant quotes and same-day coverage. High-risk businesses (contractors, manufacturers) may need 1 to 3 business days for additional underwriting review.

Yes. Expect a 25% to 50% premium increase for 3 to 5 years after filing a claim. Some insurers specialize in high-risk businesses with prior claims. Shopping multiple carriers after a claim is critical because each insurer evaluates your claims history differently.

Sources & References

- Insureon - Small Business Insurance Costs

- NerdWallet - Best General Liability Insurance (2026)

- MoneyGeek - Average General Liability Insurance Cost (2026)

- MoneyGeek - How Much Is General Liability Insurance (2026 Rates)

- SBA - Get Business Insurance

- NEXT Insurance - General Liability Insurance Cost

- The Hartford - General Liability Insurance Cost

- Progressive Commercial - General Liability Insurance Cost

- Homebase - Small Business Insurance Cost Guide 2026

- MoneyGeek - Cheapest General Liability Insurance (2026)

About the Author

Senior Legal Researcher & Business Analyst

Eliot combines decades of boots-on-the-ground small business management with deep expertise in legal consulting. Building his career in New Jersey, he spent years helping local, brick-and-mortar startups navigate the complex web of municipal, state, and federal regulations. He isn't a high-tower academic; he's a street-smart consultant who has personally walked hundreds of entrepreneurs through the structural and legal growing pains of running a business.

Was this article helpful?

Questions about What is General Liability Insurance

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment