Working Capital Loans: How They Work, Rates and Where to Get One

SBA caps working capital rates at prime plus 3.0%, a 9.75% ceiling today. Compare top lenders, credit score minimums (560-680+), and get funded in 1-30 days.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What a Working Capital Loan Is and When to Use One

- Who Qualifies for a Working Capital Loan

- How to Apply for a Working Capital Loan (Step by Step)

- What a Working Capital Loan Really Costs

- Top 5 Working Capital Lenders for 2026

- What to Do If You Do Not Qualify

- 5 Costly Mistakes to Avoid with Working Capital Loans

- FAQ

$0–$5,000,000

Est. Loan Cost

30 days

Timeline

5

Total Steps

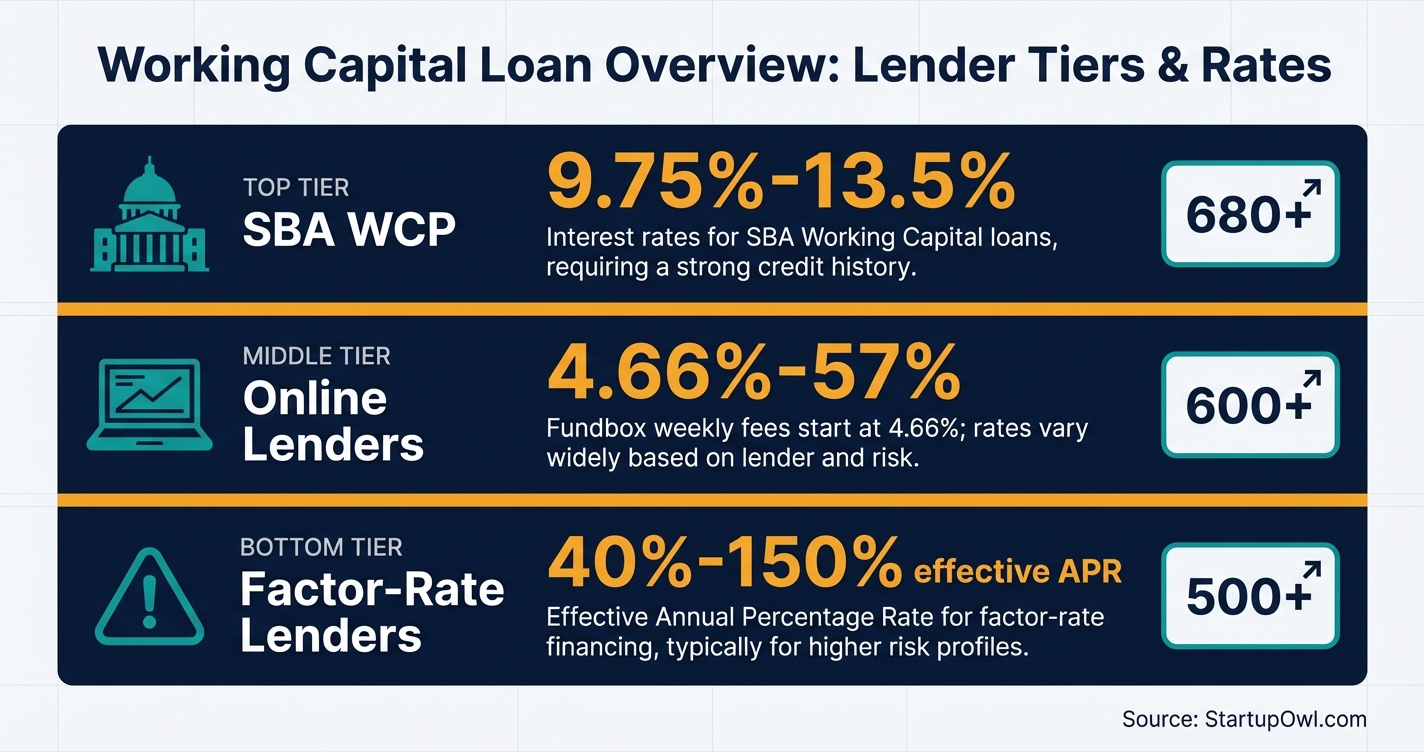

A working capital loan gives your business a revolving credit line to cover day-to-day expenses (payroll, inventory, rent) instead of handing you a single lump sum. You draw what you need, pay interest only on the amount you use, and replenish your credit as you repay. With the SBA Working Capital Pilot Program now capped at 9.75% on loans over $350,000 and loan amounts up to $5 million, this is the most accessible government-backed revolving credit program for small businesses in 2026.

Your cost depends entirely on your credit profile and which lender tier you qualify for. An established business with 680+ credit borrows under an SBA ceiling of 9.75% to 13.5%. A startup with 600 credit might pay Fundbox weekly fees starting at 4.66% on a 12-week draw. A business with a 500 score could end up paying factor rates that translate to 40%+ effective APR through lenders like Taycor Financial.

This guide covers the exact rates, credit minimums, and application steps for every tier. If you need a broader overview first, check out our guide on how to get a business loan or compare the best small business loans available right now.

What a Working Capital Loan Is and When to Use One

A working capital loan is a revolving line of credit (not a term loan) that funds your business's short-term operational needs. You draw against a pre-approved credit limit, use the funds for expenses like inventory, payroll, or supplier invoices, then repay and draw again. It works like a business credit card but at significantly lower interest rates for qualified borrowers.

The SBA's 7(a) Working Capital Pilot Program (WCP) is the first SBA program to combine domestic and international transaction financing in a single credit line. It operates under the 7(a) loan umbrella with terms up to 60 months and an 85% SBA guaranty for loans up to $150,000 (or 75% for larger loans).

You should consider a working capital loan when your business has predictable revenue but unpredictable timing. Seasonal retailers, B2B companies with 30-to-90-day payment terms, and manufacturers fulfilling large contracts are the primary use cases. If you need a one-time lump sum for equipment, our equipment financing guide covers those routes end to end. For real estate, a standard SBA loan or term loan is a better fit. And if revenue is strong but credit is not, revenue based financing providers approve on deposit health instead. Buyers of cash heavy businesses like gas stations lean on this, our station buyer guide shows where each product fits.

Platform sellers have their own routes too. See the Amazon seller loans guide and the Shopify Capital breakdown.

Practice owners, the practice loans guide covers your lane.Who Qualifies for a Working Capital Loan

Eligibility varies dramatically by lender. The table below shows what each lender tier requires.

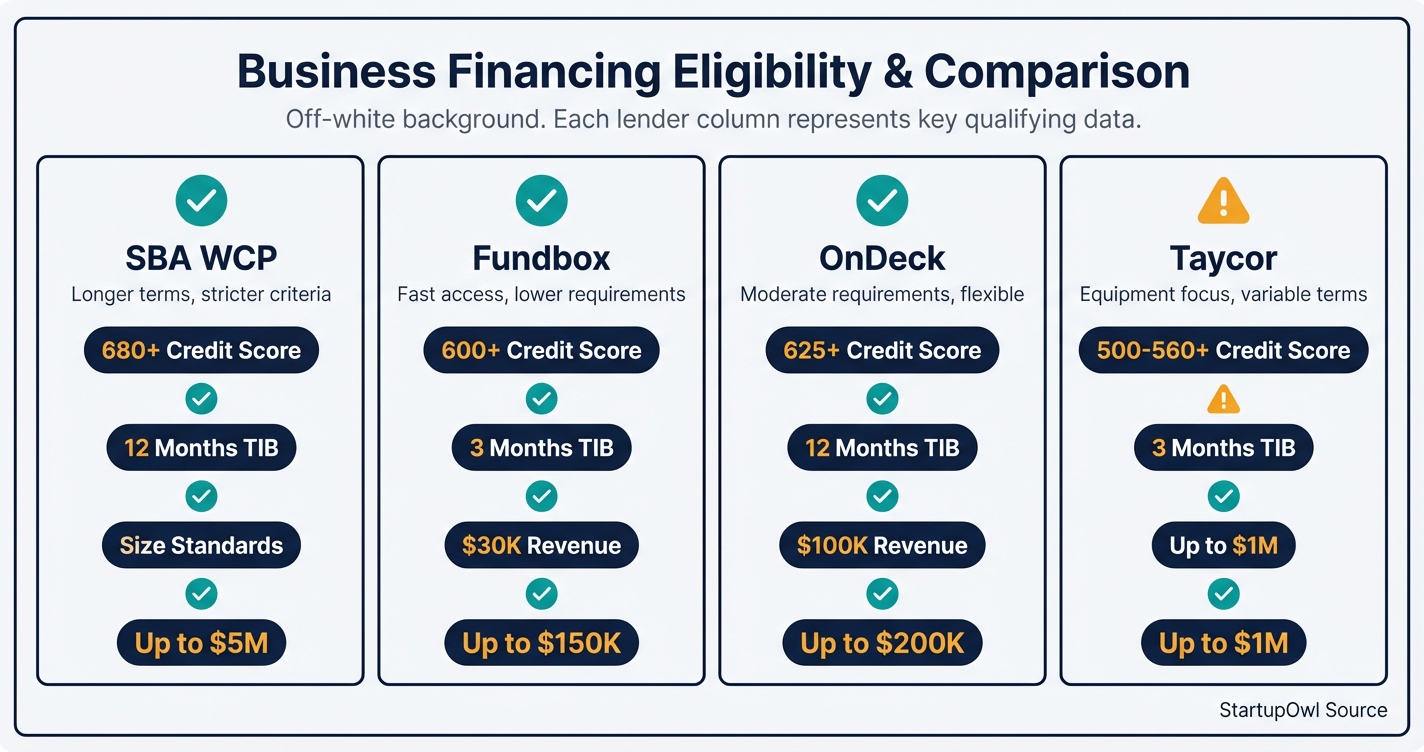

- SBA WCP: Personal credit score of 680+, at least 12 months in business, ability to produce accurate financial statements and receivable/payable reports, and your business must meet SBA size standards for your industry.

- Fundbox: Personal credit score of 600+, just 3 months in business, and $30,000 in annual revenue (per LendingTree, as of 2026). Maximum credit line of $150,000.

- OnDeck: Personal credit score of 625+, at least 12 months in business, and $100,000 in annual gross revenue. Lines of credit from $6,000 to $200,000.

- Taycor Financial: Personal credit score as low as 500 for some products (and 560+ for working capital lines), 3 months minimum in business. Factor rates starting at 1.01.

For SBA WCP specifically, your advance rates are capped by asset type. Domestic receivables qualify for up to 85% advance, insured foreign receivables up to 90%, uninsured foreign receivables up to 70%, and U.S. inventory up to 60%. If you are a brand-new business with no receivables, explore business loans for startups or microloans first.

How to Apply for a Working Capital Loan (Step by Step)

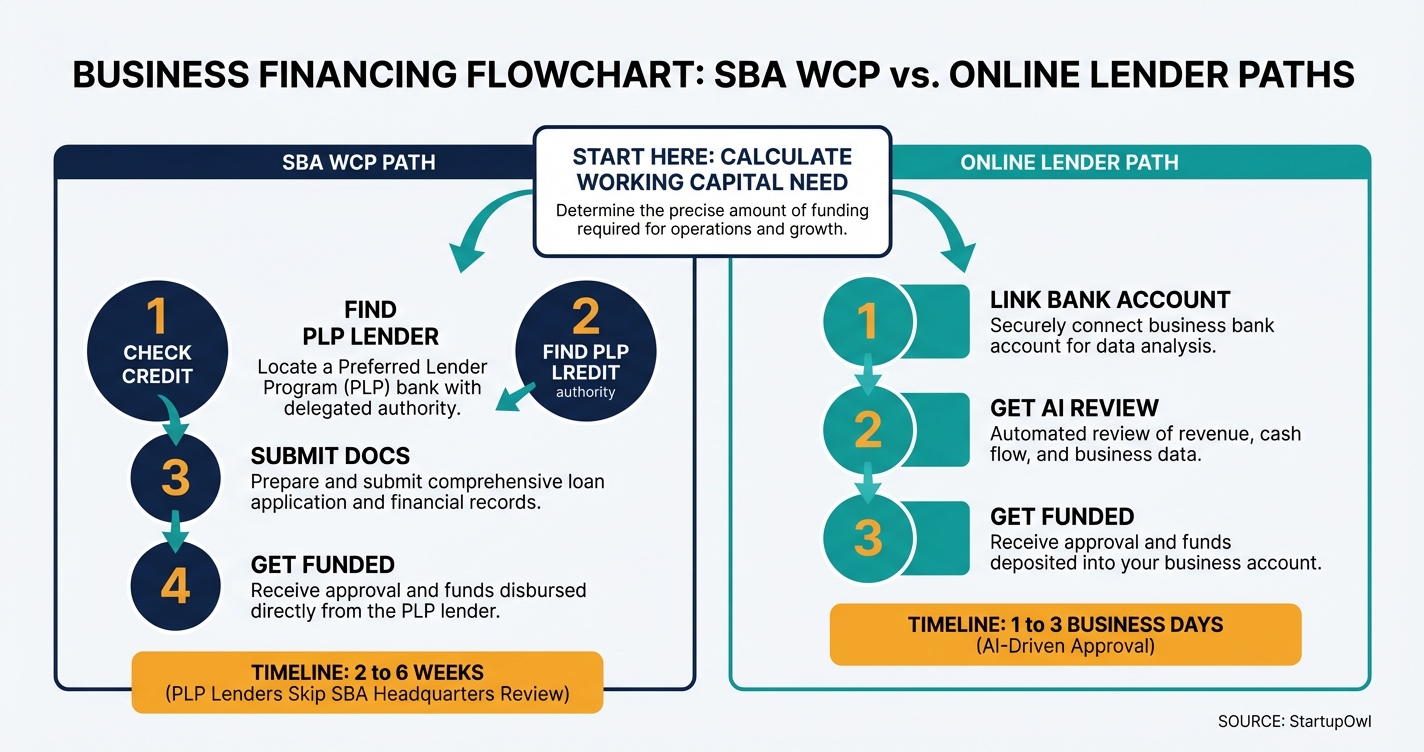

The application process differs based on whether you pursue an SBA-backed line or an online lender. Here is the general flow for both paths.

SBA WCP Path (2 to 6 weeks): Find a PLP-WCP lender through the SBA Lender Match tool. PLP lenders have delegated authority to approve your loan without SBA headquarters review, saving significant time. Prepare 2-3 years of tax returns, current financial statements, AR/AP aging reports, and any contracts or purchase orders. Loans over $2 million trigger a mandatory on-site field review. The SBA will review your application through the Loan Guaranty Processing Center if your lender does not have PLP authority.

Online Lender Path (1 to 3 days): Fundbox and OnDeck let you apply online in under 10 minutes. Fundbox links to your bank account or accounting software, uses AI to assess your financials, and can fund as soon as the next business day. OnDeck requires 3 months of bank statements and can fund within 24 hours for term loans up to $200,000 (same-day funding is available in many states for qualifying applicants). Both perform a soft credit check initially, so your score is not affected until you draw funds.

Regardless of which path you choose, get quotes from at least 3 lenders and compare the total cost of capital, not just the headline rate. A lower origination fee on one offer can offset a slightly higher interest rate on another.

What a Working Capital Loan Really Costs

The SBA WCP caps rates based on loan size, all tied to the prime rate (6.75% as of July 28, 2026, per the Federal Reserve FRED data). Here is the breakdown:

- Loans up to $50,000: Maximum 13.5% (Prime + 6.5%)

- Loans $50,001 to $250,000: Maximum 12.75% (Prime + 6.0%)

- Loans $250,001 to $350,000: Maximum 11.25% (Prime + 4.5%)

- Loans over $350,000: Maximum 9.75% (Prime + 3.0%)

SBA guarantee fees add 0.25% to 3.75% of the guaranteed portion, though small manufacturers (NAICS 31-33) pay 0% on 7(a) loans up to $950,000 through September 30, 2026. Online lenders cost significantly more. OnDeck's average APR for business lines of credit is approximately 57.10% (per Bankrate, as of 2026). Fundbox charges weekly fees starting at 4.66% for 12-week terms and 8.99% for 24-week terms, which appear low but are not annualized APR figures.

Factor-rate lenders like Taycor Financial charge rates from 1.01 to 1.40. A 1.36 factor rate on a $10,000 12-month loan means you repay $13,600 total, equivalent to roughly 70% APR. Always convert factor rates to APR before comparing offers. For a deeper look at factor-rate math, read our merchant cash advance guide.

Working Capital Loan Rates Compared (2026)

| Type / Provider | Rate | Notes |

|---|---|---|

| SBA WCP (over $350K) | 9.75% max | Prime + 3.0%. The lowest ceiling SBA sets. Requires 680+ credit, 12+ months in business. |

| SBA WCP (up to $50K) | 13.5% max | Prime + 6.5%. Best for small draws with strong credit. |

| Traditional Bank LOC | 9.75% to 14.75% | Prime + 3% to 8%. Typically requires 3+ years in business. |

| Fundbox | 4.66% to 8.99% (weekly fee) | 12-24 week terms. Not APR. Effective annualized cost is much higher. |

| OnDeck LOC | ~35% to 66% APR | Lines of $6K to $200K. Fast funding but expensive. |

| Taycor Financial | 1.01 to 1.40 factor rate | Roughly 40% to 70%+ effective APR. Accepts credit scores as low as 500. |

Top 5 Working Capital Lenders for 2026

1. SBA WCP through Preferred Lenders

The best option if you have 680+ credit and at least 12 months in business. Rates are capped at 9.75% to 13.5% on loans up to $5 million, backed by an 85% SBA guaranty for loans under $150K. PLP-WCP lenders can approve without SBA review, cutting weeks off the timeline. Find participating lenders at SBA Lender Match.

2. Fundbox (Best for Startups)

Requires just 3 months in business, a 600+ personal credit score, and $30,000 in annual revenue. Lines of credit up to $150,000 with 12-to-24-week terms. Weekly fees start at 4.66%. No origination fees, no prepayment penalties, and next-day funding. Performs only a soft credit check on application. Apply at Fundbox.com.

3. OnDeck (Best for Speed)

Lines of credit from $6,000 to $200,000 with 12-to-24-month terms. Minimum credit score of 625, 12 months in business, and $100,000 in annual revenue. OnDeck's average APR on lines of credit runs around 57%, so this is an expensive option suited for short-term needs. Same-day funding possible for qualifying applicants. Origination fee of 0% to 4%. Apply at OnDeck.com.

4. Taycor Financial (Best for Poor Credit)

Accepts personal credit scores as low as 500 for equipment products and 560+ for working capital lines. Factor rates start at 1.01 for lines of credit (with origination fees up to 3%) and go as high as 1.40 for term loans. Lines range from $10,000 to $1 million with 6-to-18-month terms. Funding in as little as 4 to 24 hours after approval. Apply at Taycor.com.

5. Bluevine (Best for Larger Lines with Fair Credit)

Offers lines of credit up to $250,000 with terms up to 12 months and weekly or monthly payment options. Bluevine has funded over $14 billion in financing since 2013. Not available in Nevada, North Dakota, South Dakota, or U.S. territories. If you need more than Fundbox's $150K cap but don't qualify for SBA rates, Bluevine fills the gap. Compare it against our full list of business line of credit options.

Factor Rates Are Not the Same as Interest Rates

A factor rate of 1.10 on a $100,000 loan means you repay $110,000 total regardless of how quickly you pay it back. Unlike interest rates, factor rates do not decrease with early repayment. A 1.10 factor rate on a 12-month term translates to roughly 20% APR, but on a 6-month term it is closer to 40% APR. Always ask the lender to provide the equivalent APR in writing before you sign.

What to Do If You Do Not Qualify

If your credit score is below 600 or you have been in business for less than 3 months, traditional working capital loans may not be an option yet. Here are your alternatives, ranked from lowest to highest cost:

- SBA Microloans: Up to $50,000 through nonprofit intermediaries. Rates of 8% to 13%. Available to startups and businesses that cannot get conventional financing.

- Business Credit Cards: Many offer 0% intro APR for 12-15 months. Good for bridging short-term gaps under $25,000. Build your business credit at the same time.

- Invoice Factoring: Sell your unpaid invoices for 80% to 90% of face value and receive cash in 1-3 days. Costs 1% to 5% of the invoice per month. No credit score minimum.

- Small Business Grants: Free money that does not require repayment. Highly competitive, but worth applying if you are a minority-owned, women-owned, or veteran-owned business.

- Merchant Cash Advance: Fastest approval (same day), but effective APR ranges from 40% to 150%+. Use only as a last resort for emergency cash.

If you are a very early-stage company still raising capital, our pre-seed funding and angel investors guide cover equity-based alternatives that do not require repayment at all.

5 Costly Mistakes to Avoid with Working Capital Loans

1. Borrowing more than your working capital supports. Most lenders cap your line at your current working capital amount (assets minus liabilities). A $50,000 working capital balance means your maximum line is typically $50,000, regardless of what a lender advertises. Borrowing beyond this increases your default risk and may trigger personal guaranty collection.

2. Ignoring advance rate caps on receivables. Even with an 85% advance rate on domestic receivables, you cannot access funds until qualifying invoices exist. Inventory advances cap at 60%. If you project $500,000 in receivables but only have $200,000 on the books today, your available draw is roughly $170,000 (85% of $200K), not $425,000.

3. Confusing factor rates with interest rates. A factor rate of 1.01 on a $50,000 advance costs $500 in fees. That looks cheap until you realize it is a 12-week product and the annualized cost exceeds 25% APR. Taycor's factor rates can go as high as 1.40, which on a $10,000 12-month loan equals $13,600 total repayment (roughly 70% APR).

4. Stacking hidden fees on top of interest. Some lenders charge origination fees (up to 5%), monthly maintenance fees ($20/month at OnDeck), and per-draw fees. On a $100,000 line with a 3% origination fee, you lose $3,000 before you even use the money. Read the full fee schedule and add every fee to your total cost calculation.

5. Failing to shop multiple lenders. The difference between the SBA WCP ceiling (9.75%) and an online lender's average APR (57%+) is enormous. Even if you only have fair credit, getting quotes from 3+ lenders can save thousands. Use the SBA's Lender Match tool and at least one online marketplace like Nav.com.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice. SBA WCP rates are based on a prime rate of 6.75% as of January 1, 2026, and will adjust as the prime rate changes.

Step-by-Step Process

- 1

Calculate your actual working capital need

Subtract your current liabilities from your current assets. The result is your working capital balance, and most lenders will cap your credit line at or near that number. If you have $100,000 in assets and $60,000 in liabilities, expect a maximum line of about $40,000.

Gather your most recent balance sheet or run the calculation from your accounting software. Lenders want to see that you can repay without over-leveraging your business.

Tips

- Use a 12-month rolling average of assets and liabilities for accuracy.

- Include accounts receivable in assets but only those under 90 days old.

- Ask your CPA to review the calculation before approaching lenders.

Common Mistakes

- Inflating asset values with stale receivables older than 90 days, which lenders will discount or reject.

- Confusing gross revenue with working capital, which leads to requesting far more than you can support.

- 2

Check your personal and business credit scores

SBA WCP lenders typically want a personal credit score of 680 or higher. Alternative lenders like Fundbox accept scores as low as 600, and Taycor Financial goes down to 500 for some products. Pull your free reports from AnnualCreditReport.com before you apply.

Your business credit score matters too. Lenders check Dun & Bradstreet, Experian Business, and Equifax Business. If you haven't started building business credit, open a business credit card and pay on time for at least 3 months before applying for a working capital line.

Tips

- Dispute any errors on your personal report before applying; corrections can take 30 days.

- Check your Dun & Bradstreet PAYDEX score at no cost through Nav.com.

Common Mistakes

- Applying to multiple lenders without checking your score first, triggering unnecessary hard inquiries.

- 3

Choose the right lender tier for your profile

Match your credit score, time in business, and revenue to the right lender. If you have 680+ credit and at least 12 months of operations, the SBA Working Capital Pilot Program gives you the lowest ceilings (9.75% to 13.5%, by loan size). For newer businesses, Fundbox requires just 3 months in business and $30,000 in annual revenue.

If your credit is below 600, look at Taycor Financial (minimum 500 for some products) or consider invoice factoring or a merchant cash advance as bridge options. Just know that factor-rate products can cost 40% to 150% in effective APR.

Tips

- Use the SBA Lender Match tool to find PLP-WCP lenders in your area.

- Get quotes from at least 3 lenders and compare total cost of capital, not just the advertised rate.

Common Mistakes

- Choosing the fastest lender without comparing total costs. A 1.01 factor rate on $50,000 costs $500 upfront plus weekly payments, which is far more expensive than a 12% annual loan.

- Assuming all SBA-approved lenders participate in the WCP program. Ask specifically about WCP eligibility.

- 4

Prepare your documentation package

SBA WCP loans require the most documentation. You will need 2 to 3 years of personal and business tax returns, current financial statements, accounts receivable and payable aging reports, and bank statements. Loans over $2 million require an on-site field review.

Alternative lenders need far less. Fundbox links directly to your business bank account or accounting software and can approve you in minutes. OnDeck requires just 3 months of bank statements and your tax ID. The less paperwork required, the higher the rate you will pay.

Tips

- Organize documents into a single PDF folder labeled by year and type before contacting lenders.

- Update your profit and loss statement and balance sheet to the most recent month.

- If you have government contracts or large purchase orders, include those as they can boost your advance rate.

Common Mistakes

- Submitting outdated financials. SBA WCP requires updated statements annually and a full credit analysis each year.

- Forgetting to include personal financial statements for all owners with 20% or more ownership.

- 5

Submit your application and negotiate terms

For SBA WCP, apply through a Preferred Lender Program (PLP-WCP) lender to skip the SBA review step entirely. PLP lenders have delegated authority to approve loans on their own, which saves weeks of processing time. Non-delegated applications must go through SBA review at the Loan Guaranty Processing Center.

For online lenders, the process is faster. Fundbox can approve you in minutes and fund by the next business day. OnDeck typically funds within 1 to 3 business days. Once you receive a term sheet, negotiate the origination fee (often 0% to 4%), draw fees, and maintenance fees before signing.

Origination fees of 0% to 5% of loan amount (varies by lender) 1 day (online lenders) to 2-6 weeks (SBA WCP) SBA.govTips

- Ask your SBA lender if they are a PLP-WCP lender with delegated authority for the fastest approval.

- Negotiate the origination fee down, especially if you bring strong financials or existing deposits to the lender.

Common Mistakes

- Signing a factor-rate agreement without converting it to APR first. A 1.10 factor rate on a 6-month $100,000 loan equals roughly 20% APR, not 10%.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| SBA WCP Interest (loans over $350K) | 9.75% (Prime + 3.0%) | A ceiling, not a quoted rate. Prime 6.75% per Federal Reserve H.15, July 28, 2026. Variable. |

| SBA WCP Interest (loans up to $50K) | Up to 13.5% (Prime + 6.5%) | Smaller loans carry higher spreads. Still cheaper than most alternatives. |

| SBA Guarantee Fee | 0.25% to 3.75% | 85% guaranty for loans up to $150K; 75% for loans over $150K. Waived for manufacturers under $950K in FY2026. |

| Online Lender Rates (Fundbox) | 4.66% to 8.99% (weekly fee, not APR) | 12-week to 24-week terms. Effective APR is much higher when annualized. |

| Factor-Rate Lenders (Taycor Financial) | 1.01 to 1.40 factor rate | Equivalent to roughly 40% to 70%+ effective APR depending on term length. |

| Origination Fees | 0% to 5% | OnDeck charges 0% to 4%. Taycor up to 3%. Some SBA lenders charge flat fees up to $2,500. |

| Draw and Maintenance Fees | $0 to $20/month | OnDeck charges a $20 monthly maintenance fee (waived with $5K+ initial draw). Fundbox charges no draw or maintenance fees. |

Frequently Asked Questions

It depends on the lender. SBA Working Capital Pilot Program lenders typically require a personal credit score of 680 or higher. Fundbox accepts scores as low as 600, and Taycor Financial goes as low as 500 for some products. The lower your score, the higher your cost of capital will be.

Online lenders like Fundbox can fund as soon as the next business day after approval. OnDeck can fund same-day for qualifying applications. SBA WCP loans through PLP lenders take 2 to 4 weeks on average because of the documentation requirements, though the lender handles approval without SBA review.

The SBA WCP allows loans up to $5 million. Fundbox caps lines at $150,000. OnDeck offers lines of credit up to $200,000. Taycor Financial provides lines from $10,000 to $1 million. Your actual limit depends on your working capital balance, receivables, and overall creditworthiness.

A working capital loan is a revolving line of credit where you draw funds as needed and repay to reuse the credit. A term loan gives you a one-time lump sum that you repay in fixed installments. Working capital lines are best for ongoing cash flow needs; term loans are better for one-time investments like equipment or real estate.

Yes, interest paid on business loans (including working capital lines) is generally tax-deductible as a business expense under IRS rules. The deduction applies to the interest portion of your payments, not the principal repayment. Consult your CPA or review IRS Publication 535 for specific rules on business interest deductions.

Yes, but not through the SBA WCP (which requires 12 months in business). Fundbox requires only 3 months in business and $30,000 in annual revenue. Taycor Financial also accepts businesses with just 3 months of operational history. For very early-stage startups, consider startup business loans or an SBA microloan instead.

Not always. Fundbox and OnDeck offer unsecured lines of credit (no collateral required), though they may file a UCC lien on business assets. SBA WCP loans are secured by your receivables, inventory, or contracts, with advance rates of 60% to 90% depending on asset type. Nearly all lenders require a personal guarantee regardless of collateral.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA 7(a) Working Capital Pilot Program

- SBA 7(a) Loans Overview

- Nav.com: SBA Working Capital Line of Credit Guide

- FRED: Bank Prime Loan Rate (MPRIME)

- LendingTree: Fundbox Business Loan Review

- Bankrate: OnDeck Business Loans Review

- LendingTree: Taycor Financial Business Loans Review

- SBA: 7(a) Fees Effective October 1, 2026 for FY2026

- SBA: Fee Waivers for Small Manufacturers FY2026

- IRS Publication 535: Business Expenses

- Bankrate: Taycor Financial Business Loans Review

- NerdWallet: Fundbox Business Loan Review

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Working Capital Loans

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment