Business Credit Score: How It Works, What the Ranges Mean and How to Improve Yours

Your business credit score ranges from 0 to 100 (or 0 to 300 for FICO SBSS). Learn score thresholds for PAYDEX, Experian, and Equifax plus 6 steps to raise yours.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Is a Business Credit Score and Why It Matters

- Business Credit Score Ranges and What "Good" Means at Each Bureau

- How to Build and Improve Your Business Credit Score

- What It Costs to Monitor and Build Your Business Credit

- Where to Check Your Business Credit Score

- What to Do If Your Business Credit Score Is Low

- 5 Common Business Credit Score Mistakes (and What They Cost You)

- FAQ

$0–$1,500

Est. Loan Cost

6 months

Timeline

6

Total Steps

Your business credit score is a number that lenders, suppliers, and partners use to judge how likely you are to pay your bills on time. Unlike your personal FICO score (which runs 300 to 850), business credit scores use completely different scales depending on which bureau created them. A "good" score at one bureau can look very different from a "good" score at another.

Four major scoring models exist, each with its own range and purpose. Understanding all four is the first step to controlling your cost of capital and your access to business loans, credit lines, and trade credit. If you only track one score, you are flying blind to what most lenders actually see.

The good news is that you can start building a scorable business credit file in as little as 3 to 6 months. A strong profile typically takes 12 to 18 months of consistent, on-time (or early) payments and responsible credit use.

What Is a Business Credit Score and Why It Matters

A business credit score rates how likely you are to pay on time. Three bureaus keep separate files on you. They are Dun & Bradstreet, Experian, and Equifax. The FICO Small Business Scoring Service (SBSS) blends data from all three into one number. SBA stopped requiring it in March 2026, though banks still use it.

Your scores affect more than loan approvals. Suppliers check them before offering you net-30 or net-60 payment terms. Landlords review them before signing a commercial lease. Insurance companies may factor them into your premiums. A weak business credit profile means you pay more for almost everything.

Unlike personal credit, business credit reports are not covered by the federal law that guarantees free annual reports. That means you need to actively monitor your file, because errors can sit there for years without anyone noticing. Services like Nav, Experian Business Credit Advantage, and D&B Credit Insights offer monitoring at varying price points.

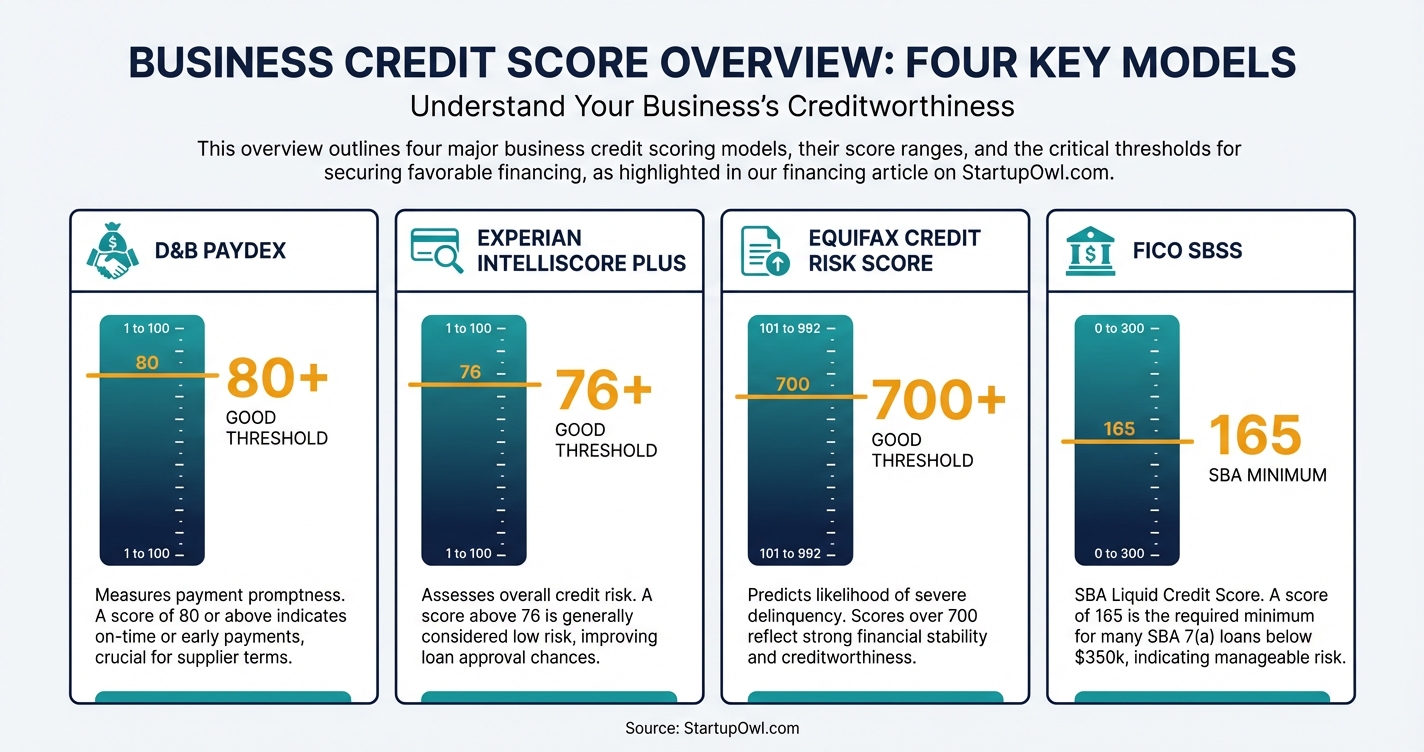

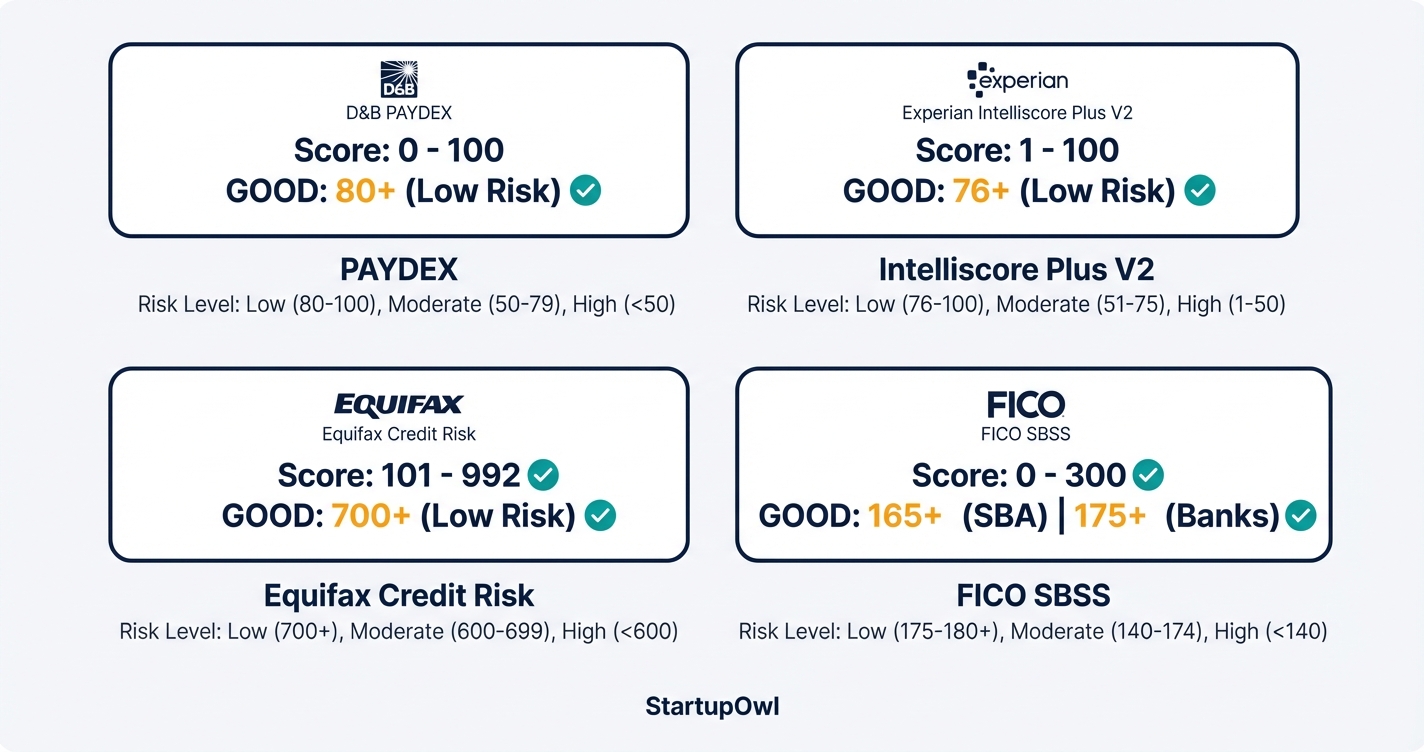

Business Credit Score Ranges and What "Good" Means at Each Bureau

Each bureau uses its own scale. Here is a breakdown of the four scoring models you need to know, with the "good" thresholds that most lenders consider low risk as of 2026.

- Dun & Bradstreet PAYDEX scores range from 1 to 100. A score of 80 or above signals low risk and indicates you pay on time or early. Scores of 50 to 79 reflect moderate risk, and below 50 flags high risk of late payment.

- Experian Intelliscore Plus (V2) ranges from 1 to 100. A score of 76 or above is generally considered good. The newer V3 version uses a 300 to 850 scale similar to personal credit, though most lenders still use V2 as of 2026.

- Equifax Credit Risk Score ranges from 101 to 992 (higher is better). Equifax also provides a Payment Index (0 to 100, with 90+ indicating all bills paid on time) and a Business Failure Score (1,000 to 1,880, with scores above 1,570 considered low risk).

- FICO SBSS ranges from 0 to 300. SBA used to set a floor here. It retired that floor for 7(a) small loans on March 1, 2026, so each lender now sets its own bar or skips scoring altogether.

The FICO SBSS is unique because it blends your personal credit history with business credit data, financial statements, and application details. If your personal credit is weak, it can pull your SBSS down even if your business payment record is excellent.

What Changed on March 1, 2026

SBA no longer requires lenders to prescreen 7(a) small loans with the FICO SBSS score. The change took effect on March 1, 2026 under Procedural Notice 5000-876777. Lenders run their own credit analysis instead. A 7(a) small loan file now has to show a debt service coverage ratio of at least 1.1 to 1. Some lenders still pull an SBSS score privately. Source, SBA Procedural Notice 5000-876777.

How to Build and Improve Your Business Credit Score

Building a business credit score follows a predictable path. The initial setup (legal entity, EIN, D-U-N-S Number) takes 1 to 30 days. Your first scorable file can appear within 3 to 6 months once you have active tradelines. A strong credit profile typically takes 12 to 18 months of consistent on-time or early payments, and excellent credit can take 2 to 3 years.

The detailed steps below walk you through the process from zero to a strong score. Each step includes the cost, timeline, and where to go. If you already have some business credit history, skip to the step that matches your current stage (for example, jump to monitoring if you already have tradelines).

One critical point: D&B's PAYDEX score rewards early payments, not just on-time ones. Paying invoices before the due date pushes your score above 80. Simply paying on the due date only gets you to 80. Keep credit utilization below 30% across all revolving accounts to help your Experian and Equifax scores. For more on strengthening your credit foundation, see our guide to how to build business credit.

What It Costs to Monitor and Build Your Business Credit

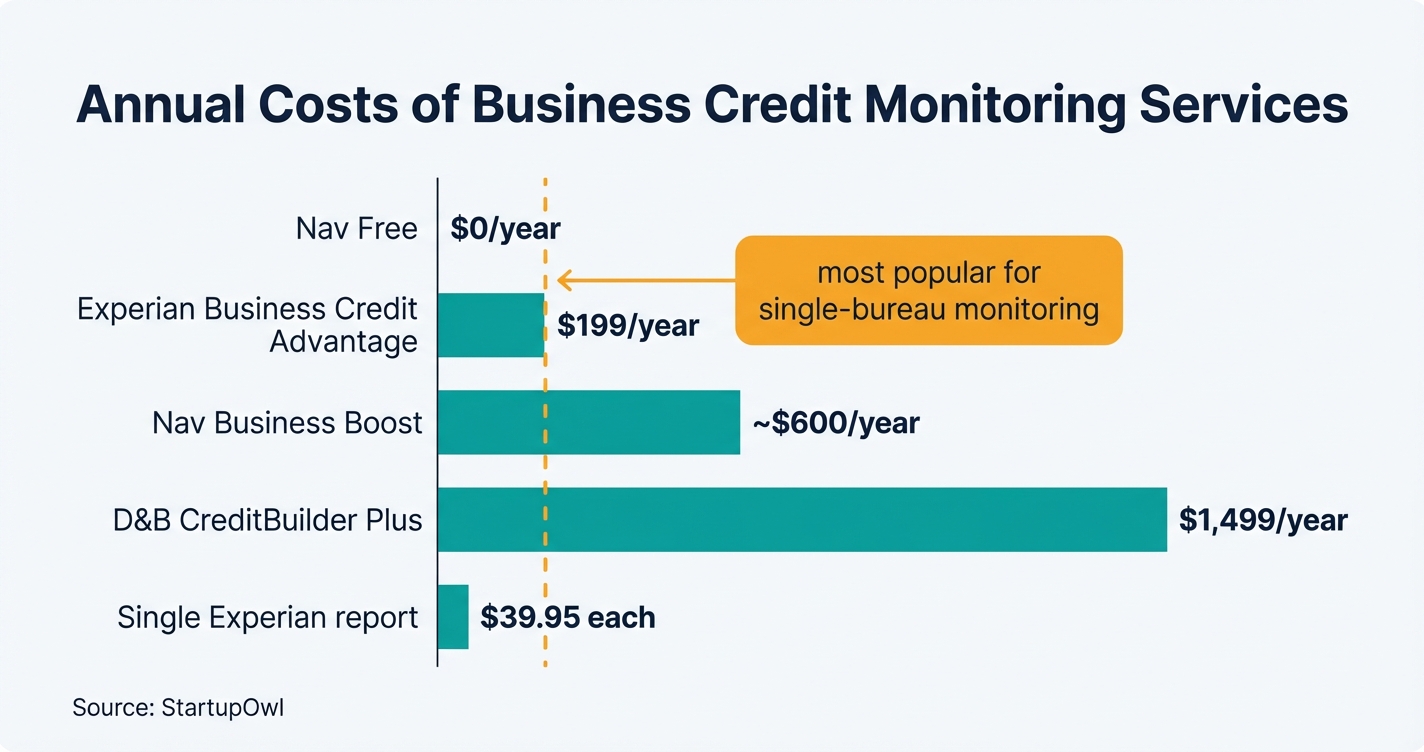

Checking your own business credit does not hurt your score. It counts as a soft inquiry. But unlike personal credit, you often have to pay for access. Here are the real costs as of 2026.

Experian's Business Credit Advantage subscription costs $199 per year and includes unlimited report access, email alerts on changes, and dark web monitoring (source: Experian). A single Experian business credit report costs $39.95 without a subscription.

D&B's CreditBuilder Plus costs $149 per month (or $1,499 per year) and lets you submit trade references and monitor your PAYDEX score with alerts (source: Nav review of D&B CreditBuilder). D&B also offers a free tier through D&B Credit Insights that gives limited access to some scores.

Multi-bureau tools like Nav let you see summary scores from multiple bureaus for free, with detailed reports starting at $49.99 per month under the Nav Business Boost plan. If you purchased individual reports from each bureau separately, you could easily spend $250+ for a single snapshot.

Business Credit Monitoring Costs Compared

| Type / Provider | Rate | Notes |

|---|---|---|

| Nav (Free tier) | $0/month | Summary credit grades from D&B, Experian, and Equifax. Limited detail. |

| Nav Business Boost | $49.99/month | Full reports from multiple bureaus in one dashboard. |

| Experian Business Credit Advantage | $199/year | Unlimited Experian report access, inquiry alerts, CyberAgent dark web monitoring. |

| D&B CreditBuilder Plus | $149/month ($1,499/year) | PAYDEX monitoring, trade reference submission, score alerts. |

| Experian single report | $39.95 per report | One-time Intelliscore Plus pull. No ongoing monitoring. |

Where to Check Your Business Credit Score

You can access your business credit data through the following services. Each covers different bureaus, so using more than one gives you the most complete picture.

- Dun & Bradstreet (D&B Credit Insights) offers a free tier with limited score visibility and paid plans for full PAYDEX access and alerts. You must have a D-U-N-S Number (free to register).

- Experian (smallbusiness.experian.com) sells individual reports at $39.95 each and its Business Credit Advantage monitoring plan at $199 per year. It tracks Intelliscore Plus and Financial Stability Risk Rating.

- Equifax provides business credit reports, including the Credit Risk Score, Payment Index, and Business Failure Score. You can access reports through select business credit monitoring services.

- Nav (nav.com) aggregates summary-level scores from D&B, Experian, and Equifax into a single dashboard, with free and paid tiers.

- FICO SBSS cannot be pulled directly by you. Only lenders can access your SBSS score during a loan application. You can improve it indirectly by strengthening both your personal and business credit profiles.

What to Do If Your Business Credit Score Is Low

Scores under 80 PAYDEX or under 76 Intelliscore still leave you options. You just have to match the product to your profile.

- Invoice factoring is based on your customers' creditworthiness, not yours. If you have outstanding invoices from reliable clients, a factoring company advances 80% to 90% of the invoice value upfront. Learn more in our invoice factoring guide.

- Merchant cash advances look at your daily credit card sales rather than your credit score. Expect factor rates of 1.1 to 1.5, which translates to effective APRs far higher than traditional loans. See our merchant cash advance guide for honest cost breakdowns.

- Microloans through the SBA microloan program offer up to $50,000 with more flexible credit requirements. Some intermediary lenders will approve borrowers with personal scores as low as 500 to 620. See our SBA microloan guide.

- Small business grants require no repayment and no credit check. Competition is fierce, but grants for small businesses exist at the federal, state, and private levels.

While you pursue short-term funding, keep building your business credit using the steps above. A few months of on-time tradeline payments can move your score significantly. If your personal credit is also weak, work on both simultaneously since models like FICO SBSS blend the two.

5 Common Business Credit Score Mistakes (and What They Cost You)

These errors are widespread, and each one can cost you real money in the form of higher rates, denied applications, or missed opportunities.

- Never registering with credit bureaus. If you do not have a D-U-N-S Number, D&B cannot generate a PAYDEX score. Without it, you are invisible to lenders who rely on that data. Getting one is free and takes minutes to start.

- Paying on time instead of early. D&B's PAYDEX score caps at 80 for on-time payments. To score above 80, you must pay before the due date. Many business owners hit a plateau at 80 because they do not realize early payment is the only path higher.

- Ignoring your credit reports. Errors are common on business credit reports, from incorrect addresses to misreported payment data. Failing to review and dispute mistakes can lower your score by dozens of points. Each bureau has its own dispute process.

- Keeping credit utilization above 30%. Experian and Equifax both factor in how much of your available credit you are using. Consistently carrying high balances signals financial stress, even if you make every payment on time.

- Relying only on personal credit. Using personal credit cards for business purchases means none of that activity builds your business credit file. Open accounts specifically in your business name that report to commercial bureaus to build a separate, standalone credit profile. Our guide to building business credit covers this in detail.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. Score ranges and monitoring costs reflect verified data as of early 2026 and may change without notice.

Step-by-Step Process

- 1

Register your business entity and get an EIN

You need a formal legal structure (LLC, corporation, or similar) and a federal Employer Identification Number (EIN) before any credit bureau will open a file on your company. The EIN is free from the IRS and takes about 5 minutes online. Without it, your business activity stays on your personal credit report.

Tips

- Apply for the EIN on IRS.gov during business hours (7 a.m. to 10 p.m. ET) to get it instantly.

- Use the business legal name exactly as it appears on your formation documents to avoid mismatches.

Common Mistakes

- Using your Social Security number instead of an EIN, which ties all business debts to your personal credit.

- 2

Claim your free D-U-N-S Number from Dun and Bradstreet

Your D-U-N-S Number is a unique nine-digit identifier that Dun & Bradstreet assigns to your business. It is required to build a PAYDEX score. You can register for one at no cost on dnb.com, though the free process can take up to 30 days.

Tips

- Request the free D-U-N-S Number well before you need financing to avoid the 30-day wait.

- Double-check that your legal business name, address, and phone number match your IRS records exactly.

Common Mistakes

- Paying a third-party service hundreds of dollars to get a D-U-N-S Number that D&B provides free.

- Not verifying your business information after registration, leading to mismatched records across bureaus.

- 3

Open trade accounts with vendors that report to credit bureaus

D&B needs at least two tradelines with three payment experiences before it can generate a PAYDEX score. Open net-30 accounts with vendors such as office supply companies, shipping services, or wholesale suppliers that report to D&B, Experian, or Equifax. Aim for 5 or more reporting trade accounts in your first 6 months.

Tips

- Ask each vendor before opening an account whether they report payment data to business credit bureaus.

- Pay invoices early (not just on time) to push your PAYDEX above 80, since early payments earn higher scores.

Common Mistakes

- Assuming all vendor accounts report to bureaus. Many do not, which means your payments build no credit history.

- 4

Get a business credit card that reports to commercial bureaus

A business credit card that reports to Experian, Equifax, or D&B is one of the fastest ways to generate tradeline data. Keep your credit utilization under 30% of the card limit. Pay the balance in full each month to avoid interest charges and to demonstrate reliable payment behavior.

Tips

- Request a credit limit increase after 6 months of on-time payments to lower your utilization ratio.

- Confirm with the issuer that they report to commercial (not just consumer) credit bureaus.

Common Mistakes

- Carrying a high balance relative to your credit limit, which can lower Experian and Equifax scores even if you pay on time.

- 5

Monitor your scores across all three bureaus

Check your business credit reports from D&B, Experian, and Equifax on a regular basis. Unlike personal credit, federal law does not guarantee you a free annual business credit report. Experian's Business Credit Advantage costs $199 per year. D&B's CreditBuilder Plus runs $149 per month. Multi-bureau tools like Nav offer free summary scores and paid plans starting around $49.99 per month.

Tips

- Start with Nav's free tier to see summary scores from multiple bureaus, then upgrade if you spot issues.

- Dispute errors immediately. Each bureau has its own dispute process (Experian: [email protected]; D&B: DUNS Manager; Equifax: small business website).

Common Mistakes

- Never checking your business credit and only discovering errors when a lender rejects your application.

- 6

Dispute errors and keep your file accurate

Errors on your business credit reports are common. Incorrect payment data, wrong addresses, and outdated legal filings can all drag your scores down. File disputes directly with each bureau. Experian accepts disputes at smallbusiness.experian.com. D&B allows corrections through its free D-U-N-S Manager tool. Include supporting documentation (bank statements, invoices) to speed resolution.

Tips

- Keep copies of every invoice and payment receipt so you have documentation ready if you need to dispute.

- Set calendar reminders to re-check your report 45 days after filing a dispute to confirm the correction posted.

Common Mistakes

- Filing disputes without supporting documentation, which leads to rejected claims and wasted time.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| D-U-N-S Number registration | $0 | Free from Dun & Bradstreet; takes up to 30 days. |

| D&B CreditBuilder Plus | $149/month or $1,499/year | Includes trade reference submission, score monitoring, and alerts. |

| Experian Business Credit Advantage | $199/year | Unlimited access to Experian business credit report and score plus identity monitoring. |

| Experian single business credit report | $39.95 per report | One-time pull of your Intelliscore Plus and related data. |

| Nav Prime (multi-bureau monitoring) | $49.99/month | Reports and scores from multiple bureaus in one dashboard. |

| Employer Identification Number (EIN) | $0 | Free from IRS.gov; instant online issuance during business hours. |

Frequently Asked Questions

It depends on the scoring model. For D&B PAYDEX, aim for 80 or above out of 100. For Experian Intelliscore Plus (V2), 76+ is good. For the Equifax Credit Risk Score, target 700+ out of 992. For FICO SBSS there is no SBA minimum any more. SBA retired it on March 1, 2026, and lenders that still use the score set their own bar.

You can generate your first scorable file in about 3 to 6 months after opening trade accounts that report to credit bureaus. A strong profile typically takes 12 to 18 months of consistent on-time or early payments. Excellent credit may take 2 to 3 years.

Nav offers free summary-level business credit scores from multiple bureaus. D&B Credit Insights also has a free tier with limited score visibility. Full detailed reports typically require paid subscriptions, such as Experian's Business Credit Advantage at $199 per year.

No. Checking your own business credit report is considered a soft inquiry and has no impact on your score. Only hard inquiries from lenders applying for credit on your behalf could potentially affect it. Monitor your reports as often as you like without concern.

None, as far as SBA is concerned. SBA retired the SBSS requirement for 7(a) small loans, meaning loans of $350,000 and under, on March 1, 2026. Your lender documents repayment ability instead. That includes a debt service coverage ratio of at least 1.1 to 1. Some lenders still pull an SBSS score on their own and set their own cutoff.

Business credit scores use different scales (often 0 to 100 or 0 to 300) instead of the personal 300 to 850 range. They are based on trade payment data, public records (liens, judgments), and company financials rather than consumer credit behavior. Anyone can access your business credit report (it is not protected by the same privacy laws as personal credit).

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA Procedural Notice 5000-876777, Sunset of SBSS Score

- What Is a Good Business Credit Score in 2026 (Nav)

- FICO SBSS Score in 2026: SBA Loan Credit Score Explained (Nav)

- SBA to Sunset FICO SBSS for 7(a) Small Loans (Nav)

- SBA 7(a) Loan Program (SBA.gov)

- SBA's SOP 50 10 8: SBSS 165 Increase (Windsor Advantage)

- What Is a Good Business Credit Score (American Express)

- Business Credit Score: What It Is, Ranges and How to Improve It (Capital One)

- What Is a Good Business Credit Score (OnDeck)

- Experian Business Credit Advantage FAQ

- D&B CreditBuilder Plus Review (Nav)

- How Long Does It Take to Build Business Credit (OnDeck)

- SBA Loan Credit Score Requirements (NerdWallet)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Business Credit Score

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment