Merchant Cash Advance: How It Works, Real Costs and Safer Alternatives

Merchant cash advances carry factor rates of 1.1 to 1.5 and effective APRs of 40-350%. Compare top MCA lenders, eligibility, real costs, and safer alternatives.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Is a Merchant Cash Advance and How Does It Work

- Who Qualifies for a Merchant Cash Advance

- How to Apply for a Merchant Cash Advance

- The Real Cost of a Merchant Cash Advance

- Top MCA Providers Compared

- Safer Alternatives If You Do Not Qualify or Want Lower Costs

- 5 Common MCA Mistakes That Cost Thousands

- FAQ

$1,000–$900,000

Est. Loan Cost

24 hours

Timeline

5

Total Steps

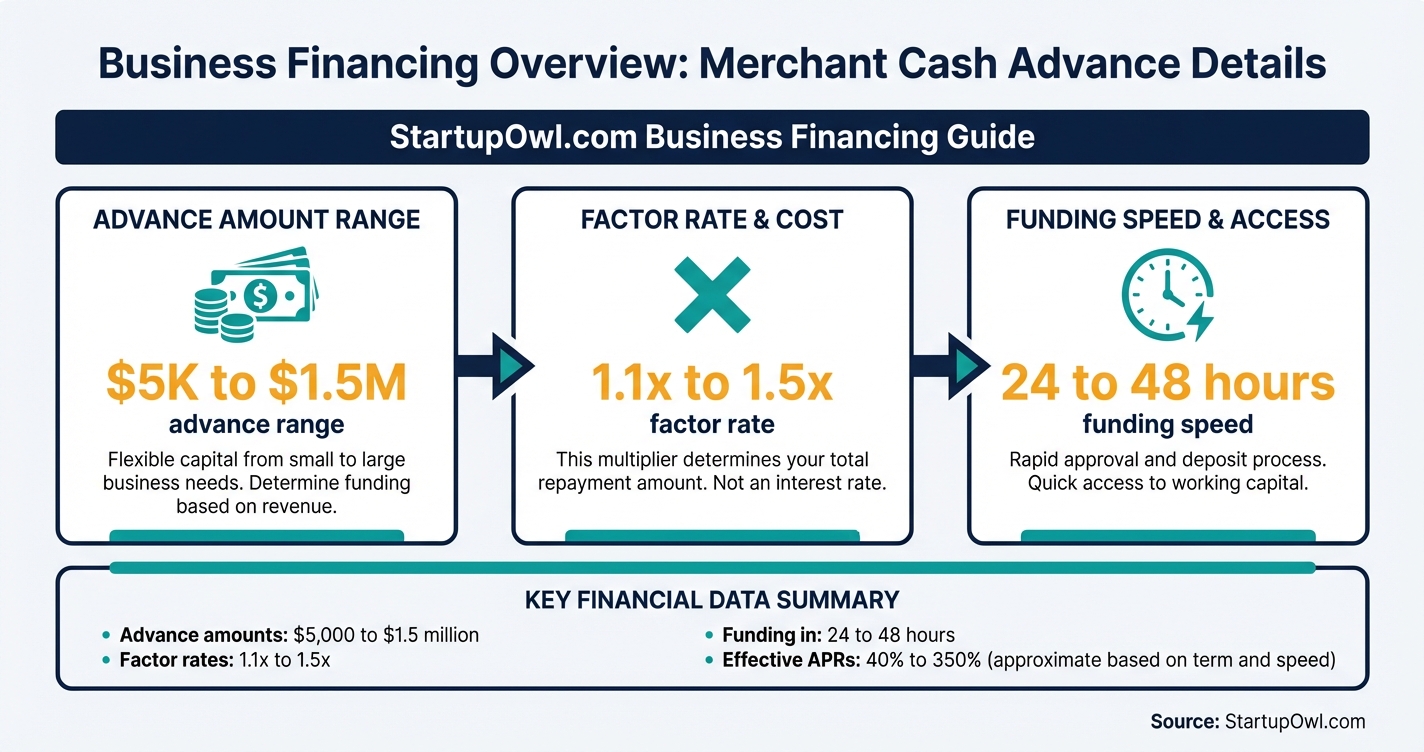

A merchant cash advance gives you a lump sum of capital today in exchange for a share of your future credit and debit card sales. Factor rates typically range from 1.1 to 1.5, which translates to effective APRs of 40% to 350% depending on how quickly your sales repay the balance. That makes MCAs one of the most expensive forms of business financing available.

So why do thousands of businesses use them every year? Speed and accessibility. Most MCA providers can fund your account in 24 to 48 hours, accept credit scores as low as 500, and require no collateral. If you have been declined by a bank and need cash this week, an MCA may be your only realistic option.

This guide breaks down exactly how MCAs work, what they really cost on a $50,000 and $100,000 advance, which providers offer the best terms, and which alternatives could save you 60-90% in financing costs. If you are considering a business loan or any other funding option, read this before you sign anything.

What Is a Merchant Cash Advance and How Does It Work

A merchant cash advance is technically not a loan. It is structured as a purchase of your future receivables, meaning a provider gives you a lump sum and collects repayment by taking a fixed percentage of your daily or weekly card sales (called the holdback) until the total payback amount is satisfied. Holdback rates typically range from 10% to 20% of daily card sales.

The total amount you owe is calculated at signing by multiplying the advance by a factor rate. For example, a $100,000 advance at a factor rate of 1.3 means you repay $130,000 total. Unlike a traditional loan where interest accrues over time, this total cost is locked in from day one. Paying early does not reduce what you owe (unless your contract includes a prepayment discount).

Repayment happens automatically through either a split of your credit card processing or direct ACH withdrawals from your business bank account. Most MCAs run for 3 to 18 months, though some providers extend terms up to 24 months. Because repayment fluctuates with your sales volume, your daily payment drops during slow periods and rises during busy ones.

This structure means MCAs are fundamentally different from a working capital loan or business line of credit, where you pay interest only on the outstanding balance and can reduce your total cost by repaying early.

If flexible payments appeal but daily card holdbacks do not, compare the best revenue based financing companies first. True RBF tracks monthly revenue instead of daily sales.

Selling on Amazon and weighing a shelf offer? Read our Amazon seller loans breakdown first. The program changed fully in March 2024.

Already stuck in an advance that no longer fits? Our MCA debt relief guide maps every honest exit and the rescue offers to avoid.

Who Qualifies for a Merchant Cash Advance

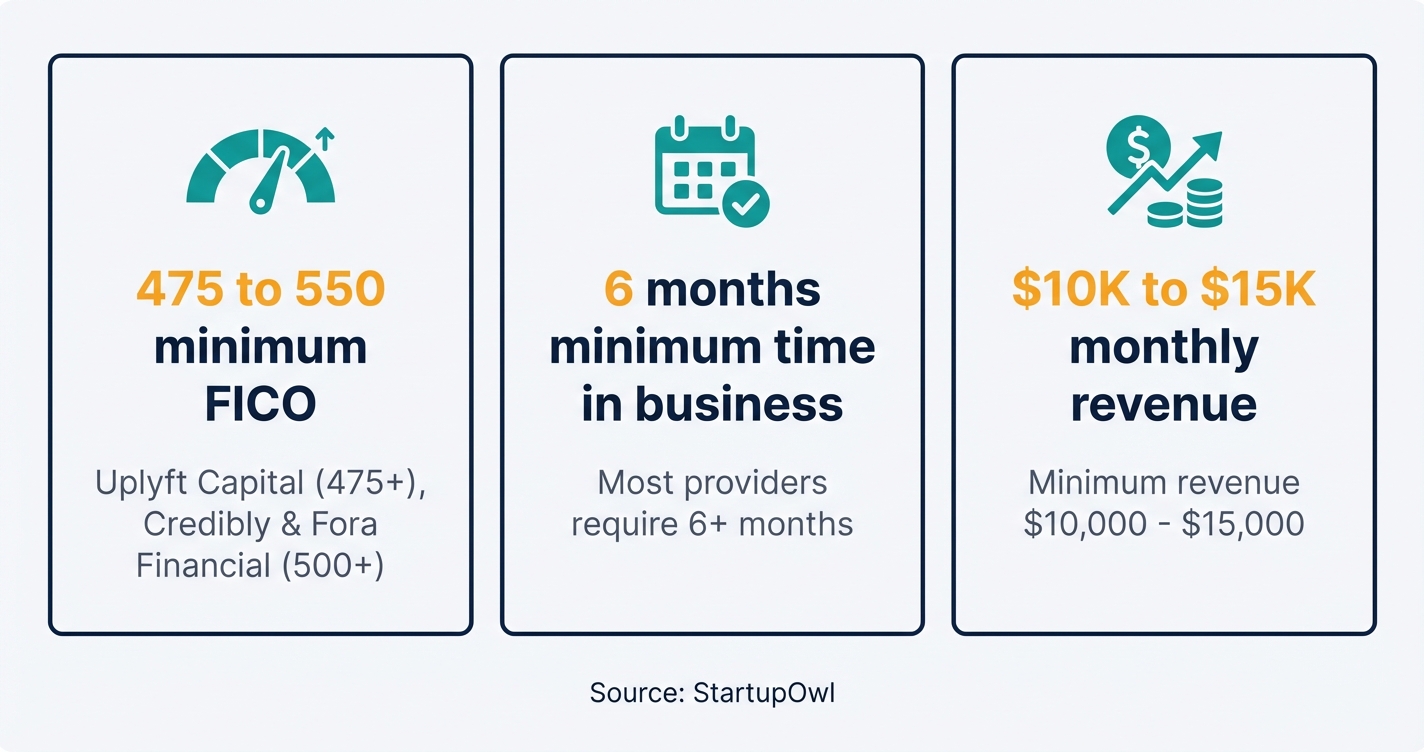

MCA eligibility is primarily based on your business revenue, not your credit score. Providers care most about your monthly deposits, card sales volume, and cash flow consistency over the past 3 to 6 months. That said, most providers set a minimum personal credit score threshold, which typically falls between 500 and 550.

Here are the baseline requirements you will see across most MCA providers as of 2026:

- Minimum credit score: 475 to 550 (varies by provider; Credibly and Fora Financial accept 500, Uplyft Capital accepts 475)

- Time in business: At least 6 months of operating history

- Monthly revenue: $10,000 to $15,000 minimum in monthly deposits or card sales

- Business bank account: Must show consistent deposits with minimal NSFs or overdrafts

- U.S.-based business: Most providers require a U.S. business entity and a U.S. bank account

Your business credit score plays a smaller role than with traditional loans, but negative marks like recent bankruptcies or excessive existing debt can still reduce your approval odds or push your factor rate higher. If you want to strengthen your profile before applying, start by learning how to build business credit.

How to Apply for a Merchant Cash Advance

Applying for an MCA is faster than almost any other form of business financing. Most providers offer fully online applications that take 10 to 15 minutes to complete, and you can receive approval in as little as a few hours. Here is the step-by-step process from application to funding.

Start by gathering your core documents: a government-issued photo ID, 3 to 6 months of business bank statements, proof of ownership (articles of organization or business license), and a voided business check. If your provider uses a card-sales split for repayment, you will also need your merchant processing statements. Missing any one of these documents will stall your application.

Submit your application through a lending marketplace like Lendio to compare multiple offers from one application, or apply directly with providers like Credibly or Fora Financial. After reviewing your bank statements, the underwriter will send an offer listing your advance amount, factor rate, holdback percentage, and total payback amount.

Review the contract carefully (see our contract-review step above), sign the agreement, and funding typically hits your bank account via ACH within 24 to 48 hours. Some providers like Credibly can fund in as fast as 4 hours after approval.

The Real Cost of a Merchant Cash Advance

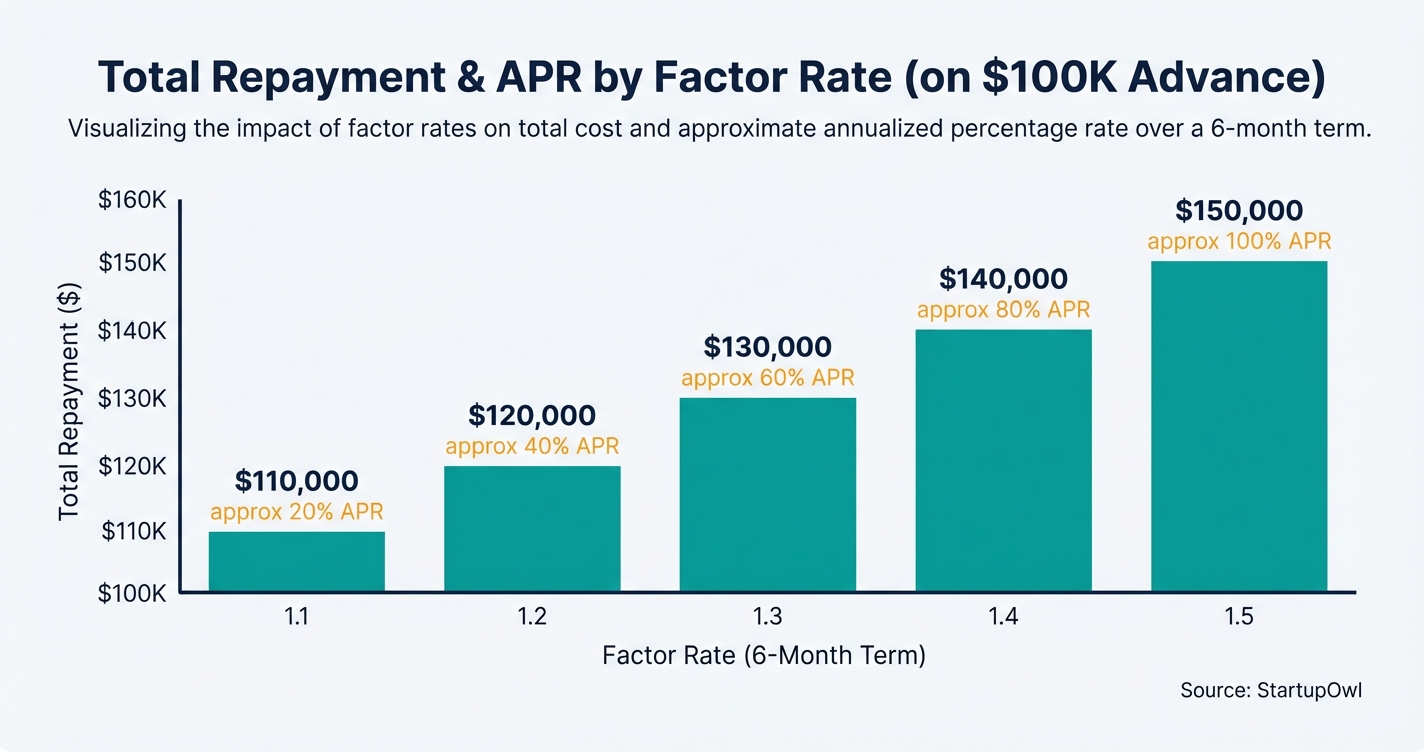

MCAs are one of the most expensive forms of business financing available, and the factor-rate pricing model makes the true cost difficult to compare against traditional loans. Here is what a merchant cash advance actually costs on a $100,000 advance at common factor rates.

- Factor rate of 1.1 = $110,000 total repayment (roughly 20% APR over 6 months)

- Factor rate of 1.2 = $120,000 total repayment (roughly 40% APR over 6 months)

- Factor rate of 1.3 = $130,000 total repayment (roughly 60% APR over 6 months)

- Factor rate of 1.4 = $140,000 total repayment (roughly 80% APR over 6 months)

- Factor rate of 1.5 = $150,000 total repayment (roughly 100% APR over 6 months)

These APR estimates assume a 6-month repayment period. If strong sales push you to repay in 4 months, the effective APR climbs significantly higher. Conversely, slow sales extend the timeline and lower the annualized rate, but you are still paying the same total dollar amount.

MCA Fee Breakdown Beyond the Factor Rate

| Type / Provider | Rate | Notes |

|---|---|---|

| Origination fee | 1% to 5% | Deducted from your advance upfront. On a $100,000 advance, a 2.5% fee means you receive $97,500 but owe the full payback amount. Credibly charges 2.5% as of 2026. |

| ACH processing fee | $25 to $50/month | Monthly fee for daily or weekly automated bank debits. Adds $150 to $600 over the life of most advances. |

| Administrative / servicing fee | $50/month (Credibly) | Not all providers charge this. Credibly discloses a $50/month administration fee. |

| Renewal / refinancing fee | Varies | Charged if you take a new advance to pay off an existing one. Stacking advances compounds costs rapidly. |

| UCC lien filing | $0 to you (provider files) | Creates a public record on your business. Must be removed after payoff. Can complicate future financing. |

Never Stack Multiple Merchant Cash Advances

Taking a second MCA to pay off the first (called "stacking") is the fastest path to a debt spiral. Each advance adds a new daily holdback to your bank account, and the combined deductions can exceed 30-40% of your daily revenue. The FTC has taken multiple enforcement actions against providers who encouraged stacking, including a $20.3 million judgment in 2024 against an MCA operator for deceiving small businesses and unlawfully seizing assets. If you are struggling to repay an existing MCA, explore refinancing with a business line of credit or speak with a financial advisor before taking on additional advances.

Top MCA Providers Compared

Not all MCA providers charge the same rates or have the same requirements. Here are five well-known providers with verified data as of 2026. Always confirm current terms directly with the provider before applying.

- Credibly offers advances from $5,000 to $600,000 with factor rates from 1.09 to 1.41. Minimum requirements include a 500 credit score, 6 months in business, and $15,000 monthly revenue. Credibly charges a 2.5% origination fee and $50/month admin fee. Funding can arrive in as little as 4 hours. (Credibly.com)

- Lendio is a marketplace that matches you with 75+ lenders from a single application. You need a minimum credit score of 570 and just $12,000 in monthly revenue. Funding can arrive in 24 hours after approval. (Lendio.com)

- Fora Financial provides revenue advances up to $1.5 million with a minimum credit score of 500. Terms extend up to 15 months, and there is a discount for early repayment. (ForaFinancial.com)

- Forward Financing offers $5,000 to $300,000 with terms from 3 to 12 months. Requires a 500 credit score, 1 year in business, and $10,000 monthly revenue. No personal guarantee required. (ForwardFinancing.com)

- Uplyft Capital stands out for its low minimum credit score of 475 and same-day approval through AI-powered underwriting. Requires 6 months in business and $96,000 annual revenue. Funding in 24 to 48 hours. (UplyftCapital.com)

For broader loan comparisons beyond MCAs, see our guide to the best small business loans.

Safer Alternatives If You Do Not Qualify or Want Lower Costs

If you can wait 3 to 7 days for funding (instead of 24 hours), you can likely find a financing option that costs 60-90% less than an MCA. Here are the main alternatives ranked by accessibility.

- Business line of credit: APRs of 12-30% from online lenders. Monthly payments (not daily). Draw only what you need and pay interest only on what you use. Most require a 600+ credit score. See our full business line of credit guide.

- SBA microloan: Up to $50,000 at rates of 8-13% APR through nonprofit intermediaries. Longer approval time (2 to 4 weeks) but dramatically cheaper. Read our SBA microloan guide.

- Invoice factoring: Sell your outstanding invoices to a factoring company for 80-90% of face value. You get cash in 1-3 days. Fees run 1-5% per invoice. Works well if your clients pay on net-30 or net-60 terms. See invoice factoring.

- Business credit cards: Introductory 0% APR offers last 9 to 15 months on many cards. Ongoing APRs of 18-26%, still far below MCA factor rates. Compare options in our best business credit cards guide.

- Small business grants: Free money with no repayment. Competitive and slow, but worth applying to in parallel. Browse opportunities in our small business grants guide.

If your credit score is the main barrier to traditional financing, start building it now. Our guide on how to build business credit walks you through the process step by step.

5 Common MCA Mistakes That Cost Thousands

- Ignoring the effective APR. A factor rate of 1.3 sounds modest, but it can translate to 60% APR or higher on a 6-month advance. Always ask for the APR-equivalent so you can compare against other financing options. In California and New York, providers are now legally required to disclose this on offers under $500,000.

- Accepting the first offer. Factor rates, holdback percentages, and fees vary significantly across providers. Not comparing at least 2 to 3 offers could cost you $5,000 to $20,000 in unnecessary fees on a $100,000 advance.

- Stacking multiple advances. Taking a second MCA to cover repayment on the first compounds your daily outflow and dramatically increases your risk of default. This is the number one path to MCA-related business failure.

- Missing the UCC lien. Most MCA contracts include a UCC filing that creates a public security interest in your business assets. This lien can block future financing from banks and SBA lenders. After payoff, confirm the lien is removed.

- Assuming you can negotiate mid-contract. Unlike a loan, the total payback amount is fixed at signing. If your sales drop, your daily payment decreases, but you still owe the full amount. There is no renegotiation unless your contract explicitly allows it.

MCA Disclosure Laws Are Expanding Rapidly

California's Commercial Financing Disclosure Law (effective December 2022) and New York's similar law (effective August 2023) now require MCA providers to give you standardized, plain-language cost disclosures on offers under $500,000 (California) and $2.5 million (New York). Utah, Virginia, and Connecticut have enacted similar requirements, and Florida introduced its own bill in early 2026. If your provider does not give you a clear disclosure showing the total repayment amount and an estimated APR, that is a red flag. Learn more at the CFPB's small business lending resources page.

Step-by-Step Process

- 1

Check your bank statements and credit score before applying

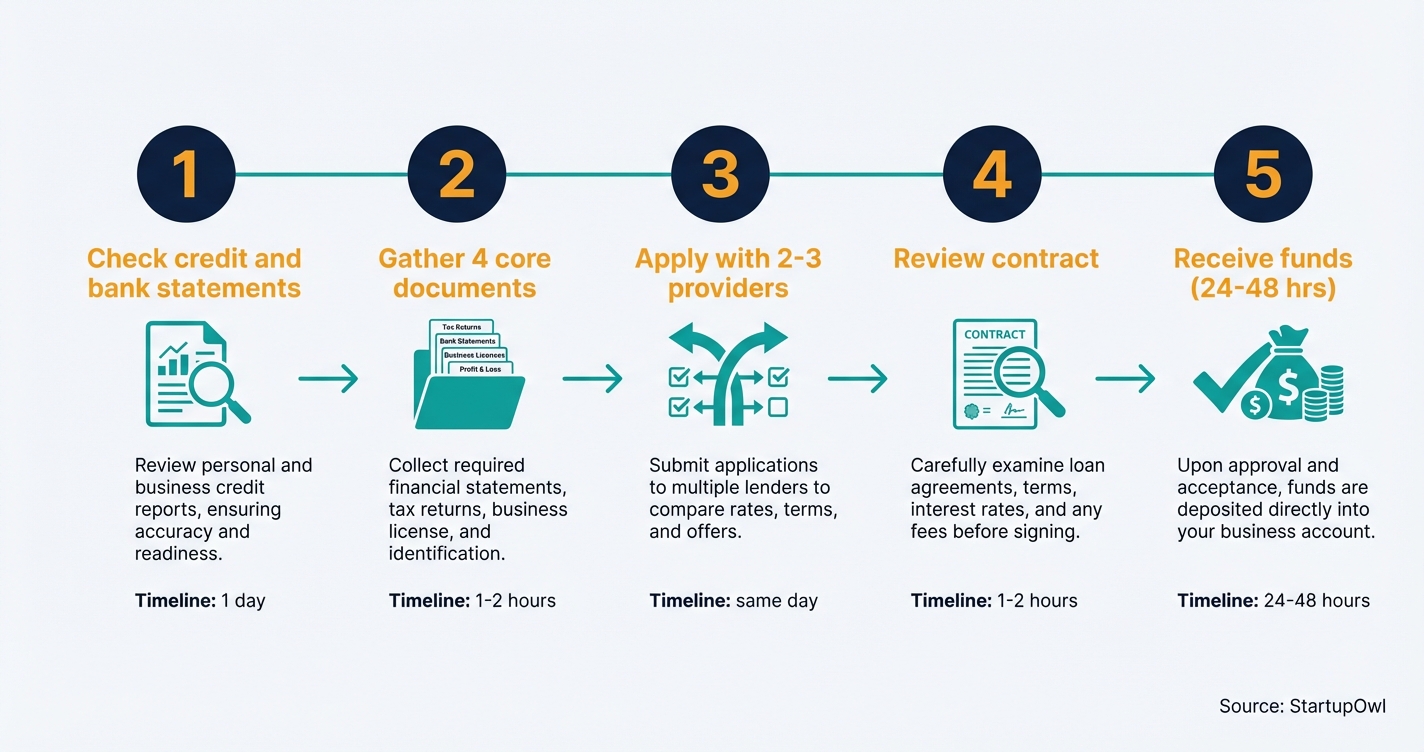

Pull your personal credit score from Experian or Equifax and review your last 3 to 6 months of business bank statements. MCA underwriters care most about deposit consistency, average daily balance, and NSF/overdraft frequency. If your account frequently dips below zero, you will either receive a higher factor rate or a smaller advance.

Most MCA providers accept scores as low as 500, but your score still influences pricing. A score above 600 typically unlocks better factor rates from providers like Credibly and Fora Financial.

Tips

- Clean up any NSFs or overdrafts on your bank statements before applying to improve your offer.

- Request a soft pull from providers like Credibly so the credit check does not impact your score.

- Check both your personal and business credit scores since some underwriters review both.

Common Mistakes

- Applying before reviewing your bank statements, which may reveal NSFs that weaken your offer.

- Letting multiple providers run hard credit pulls, which can lower your score.

- 2

Gather your documentation package

Every MCA application requires four core documents: a government-issued photo ID, 3 to 6 months of business bank statements, proof of business ownership (articles of organization or a business license), and a voided business check. Missing even one of these stops the process entirely.

If the MCA provider repays through a card-sales split, you will also need merchant processing statements showing your monthly credit card volume. Aim for at least $5,000 to $10,000 in monthly card sales to qualify with most providers.

Tips

- Download your bank statements as PDFs from your online banking portal to speed up submission.

- If you are part of a partnership, get written confirmation from all partners with 20% or more ownership.

Common Mistakes

- Submitting blurry or incomplete bank statements, which delays approval by 2 to 3 days.

- Forgetting proof of ownership, which is required for signing authority verification.

- 3

Apply with at least two or three MCA providers to compare offers

Submit applications to multiple providers so you can compare factor rates, holdback percentages, and total payback amounts side by side. Lendio connects you with 75+ lenders from a single application, which makes comparison easier. Direct lenders like Credibly and Fora Financial also offer quick online applications.

Ask each provider for the total repayment amount, the daily or weekly holdback percentage, and the estimated repayment timeline. In states like California and New York, providers are legally required to disclose an estimated APR on offers under $500,000.

Tips

- Use a lending marketplace like Lendio to get multiple offers from one application.

- Ask specifically for the APR equivalent of the factor rate so you can compare to a traditional loan.

- Confirm whether the provider offers a prepayment discount before signing.

Common Mistakes

- Accepting the first offer without comparing at least two others, which could cost you thousands more.

- Ignoring the holdback percentage, which determines how much cash leaves your account every day.

- 4

Read every clause of the MCA contract before signing

Review the contract for a confession of judgment clause, which lets the provider seize your assets without notifying you if you default. The FTC has taken enforcement action against MCA providers for deceptive practices including hidden personal guarantees and undisclosed upfront fees, resulting in a $20.3 million judgment in one 2024 case.

Look for UCC lien filing language, which creates a public record of the provider's security interest in your business assets. Confirm the exact holdback rate, total payback amount, and whether there are origination fees (typically 1-5%) or monthly ACH processing fees ($25 to $50 per month).

Tips

- Have a business attorney review your MCA contract if the advance is over $50,000.

- Reject any contract that includes a confession of judgment clause.

Common Mistakes

- Signing a contract with a personal guarantee you did not realize was included, which puts personal assets at risk.

- Overlooking origination fees that get deducted from your advance, reducing the cash you actually receive.

- 5

Receive your funds and manage daily repayment

After signing, most providers fund your business bank account via ACH within 24 to 48 hours. Some providers like Credibly can fund in as little as 4 hours. Daily or weekly holdback deductions begin immediately, typically taking 10-20% of your daily card sales or a fixed daily ACH withdrawal.

Track your holdback deductions closely using your provider's online portal. If you anticipate a slow sales period, contact your provider proactively. Build a cash reserve equal to at least 2 weeks of holdback payments to avoid overdraft fees during revenue dips.

Total repayment = advance amount x factor rate (e.g., $100,000 x 1.3 = $130,000) 3 to 18 months for full repayment NavTips

- Set up a separate account to track MCA repayment deductions against your daily sales.

- If your provider offers an early repayment discount, calculate whether paying early saves more than keeping the cash on hand.

Common Mistakes

- Failing to budget for daily holdback deductions, which can trigger overdrafts and cascade into additional bank fees.

- Stacking a second MCA on top of the first, which doubles your daily outflow and dramatically increases your risk of default.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Factor rate (multiplied by advance amount) | 1.1x to 1.5x | Determines total repayment. A $100,000 advance at 1.3x means $130,000 total owed. |

| Effective APR | 40% to 350% | Varies based on factor rate and repayment speed. Higher card sales accelerate repayment and raise effective APR. |

| Origination fee | 1% to 5% | Typically deducted from advance amount before funding. Credibly charges 2.5%. |

| ACH processing fee | $25 to $50 per month | Charged for automated daily or weekly bank account debits. |

| Renewal / refinancing fee | Varies by provider | Charged if you refinance or renew an existing advance. SBA loans can no longer refinance MCAs as of 2026. |

Frequently Asked Questions

Most MCA providers accept personal credit scores as low as 500, and some (like Uplyft Capital) go as low as 475. Your revenue and bank statement history matter more than your credit score. A higher score (above 600) will typically get you a lower factor rate, saving you money on the total repayment.

On a $100,000 advance with a factor rate of 1.3, you would repay $130,000 total. That translates to roughly 60% APR if repaid over 6 months. Add origination fees of 1-5% and monthly ACH fees of $25-50, and the all-in cost climbs higher. Effective APRs across the MCA industry typically range from 40% to 350%.

Technically, no. An MCA is structured as a purchase of your future receivables, not a loan. This distinction means MCAs are not subject to the same federal lending regulations as traditional loans, though states like California, New York, Utah, and Virginia have enacted disclosure laws requiring MCA providers to share standardized cost information. The CFPB has classified MCAs as "credit" under the Equal Credit Opportunity Act.

Most MCA providers fund within 24 to 48 hours of approval. Credibly can fund in as little as 4 hours. The approval process itself is typically same-day if you submit complete documentation (government ID, 3-6 months of bank statements, proof of ownership, and a voided check).

Yes, you can refinance an MCA with a new advance or a different financing product to lower your daily payments. However, as of 2026, the U.S. Small Business Administration no longer allows SBA loans to refinance MCAs. Your best refinancing path is typically a business line of credit at 12-30% APR, which replaces daily debits with monthly payments.

Most MCA providers do not report payment activity to personal or business credit bureaus. That means on-time MCA payments will not help you build credit. If you want to improve your credit profile while accessing capital, consider a business line of credit or business credit card that reports to bureaus.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- CFPB Small Business Lending Rule FAQs (Merchant Cash Advances)

- FTC Enforcement Actions on Merchant Cash Advances

- NerdWallet: Best Merchant Cash Advance Companies for 2026

- CNBC Select: Best Merchant Cash Advance Companies of 2026

- Nav.com: Merchant Cash Advance (MCA) Guide

- United Capital Source: Merchant Cash Advance Requirements 2026

- United Capital Source: How to Apply for a Merchant Cash Advance Online in 2026

- California DFPI: Commercial Financing Disclosures

- FitSmallBusiness: Best Merchant Cash Advance Companies

- Goodwin Law: CFPB Deems Merchant Cash Advances to Be Credit Under ECOA

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Merchant Cash Advance

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment