Invoice Factoring Explained for Small Business Owners

Turn unpaid B2B invoices into same-day cash. Learn how invoice factoring works in 2026, real costs (1 to 5%), APR equivalents, who qualifies, and when to use it vs other financing.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- The 30-second answer

- How invoice factoring works, with a real example

- What invoice factoring actually costs

- Calculate your invoice factoring cost

- The five types of invoice factoring

- Who qualifies and what factors look for

- How to apply, step by step

- Invoice factoring vs other financing

- When factoring makes sense and when it does not

- Industry rate benchmarks

- Contract red flags to watch for

- How to tell your customers you are factoring

- Accounting and tax treatment

- Invoice factoring glossary

- Common mistakes that cost you money

- FAQ

$100–$50,000

Est. Loan Cost

72 hours

Timeline

5

Total Steps

The 30-second answer

Invoice factoring is a financial transaction where a business sells unpaid B2B invoices to a third party (a factoring company) for immediate cash. The factor advances 80 to 100 percent of the invoice value within one business day after setup, then collects payment directly from the customer. When the customer pays, the factor keeps a fee (typically 1 to 5 percent per 30-day period) and sends you the remainder.

It is not a loan. No new debt hits your balance sheet, and qualification is based on your customers' credit, not yours. The industry average discount fee sits around 2.5 percent per 30 days, which works out to roughly a 26 percent annualized cost of money. Factoring fits best for B2B businesses with healthy margins and customers on net 30 to net 90 payment terms.

Roughly 60 percent of small businesses struggle with cash flow, according to PYMNTS research. Factoring bridges the gap when waiting 30, 60, or 90 days for payment would force you to miss payroll, postpone inventory, or pass on a new contract.

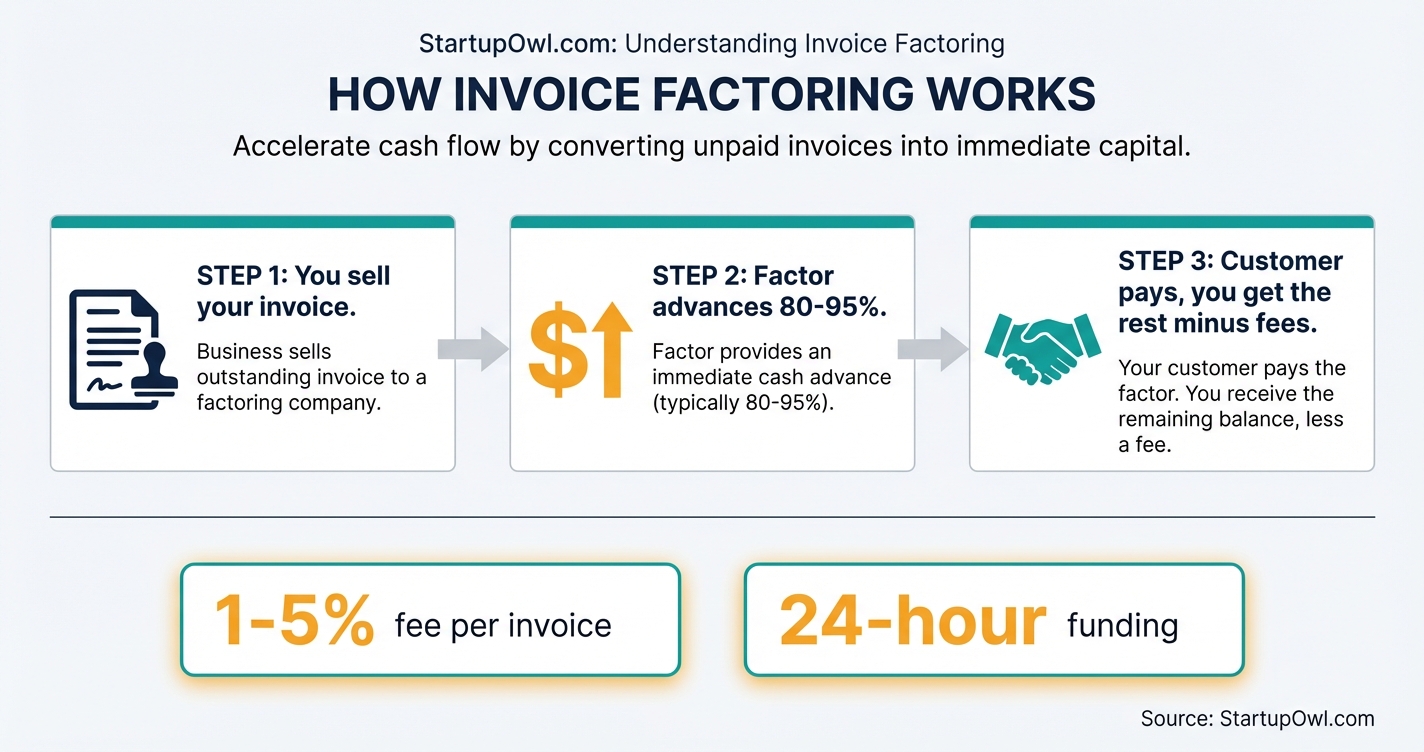

How invoice factoring works, with a real example

Invoice factoring (also called accounts receivable factoring) is straightforward once you see the cash flow.

- You deliver the work and invoice your customer on normal net-30 or net-60 terms.

- You submit the invoice to the factor along with proof of delivery.

- The factor verifies your customer's credit and the invoice, typically within a few hours.

- The factor advances you 80 to 100 percent of the invoice value, usually wired to your bank within one business day.

- The factor collects payment directly from your customer when the invoice is due, then releases the remaining balance minus its fee.

A real $10,000 example. You have a $10,000 invoice on net-30 terms. The factor offers a 90 percent advance rate and a 2 percent discount fee for the first 30 days.

- Day 1, factor wires you $9,000 (90 percent of $10,000).

- Day 30, customer pays the factor the full $10,000.

- Day 30, factor keeps its $200 fee (2 percent of $10,000) and sends you the remaining $800 reserve.

Total cost for getting paid 30 days early is $200, or 2 percent of invoice value. Annualized, that is a 26.1 percent APR, which is the honest comparison to a bank loan. Make this calculation for every factoring quote you receive.

A slow-pay example. Same $10,000 invoice, but your customer takes 60 days to pay. If your contract charges 2 percent per 30 days with tiered pricing, the fee on Day 60 is 4 percent, or $400. Your effective APR nearly doubles to roughly 26.3 percent for month one and a comparable rate stacking for month two, for a total annualized cost closer to 52 percent. Slow payers are what turn a reasonable product into an expensive one.

Factoring differs from a traditional business loan in three important ways. There is no interest rate or repayment schedule. Your customer's creditworthiness matters more than yours. And the transaction does not create new debt, since you are selling an asset rather than borrowing against one.

What invoice factoring actually costs

The headline cost is the discount fee (also called the factoring rate), which typically runs from 1 to 5 percent of invoice face value per 30-day period, per Porter Capital, United Capital Source, and Bankrate. The industry average hovers around 2.5 percent.

Here is the math nobody advertises clearly.

- A 1 percent fee on a 30-day invoice equals a 12.7 percent APR.

- A 2 percent fee on a 30-day invoice equals a 26.1 percent APR.

- A 3 percent fee on a 45-day invoice equals a 26.4 percent APR.

- A 4 percent fee on a 60-day invoice equals a 26.6 percent APR.

The pattern here is not a coincidence. A factor that charges "2 percent for 30 days" is effectively charging a 26 percent annualized rate for the privilege of getting paid early. If your bank would give you a working-capital line at 11 or 12 percent APR, factoring is almost always more expensive.

The fees beyond the headline rate. These are where margin quietly disappears.

Invoice factoring fee anatomy

| Type / Provider | Rate | Notes |

|---|---|---|

| Discount fee (primary cost) | 1 to 5% per 30 days | Industry average around 2.5%. Flat or tiered/variable. |

| Advance rate (cash upfront) | 80 to 100% of invoice | Higher advance usually means a higher fee. |

| Origination or setup fee | $150 to $500 | One-time. Some providers waive it. |

| ACH or wire fee | $0 to $30 per transfer | Negotiable. altLINE starts at $0. |

| Monthly minimum volume fee | Varies | Charged if your factored volume falls below the contract minimum. |

| Late payment penalty | +0.5% per 10 to 15 days late | Applies when your customer pays past invoice due. |

| Early termination fee | 1 to 3% of credit line | Applies only to contracts with minimum terms. |

| Lockbox or processing fee | $50 to $250 per month | Some factors charge for routing customer payments through a dedicated bank account. |

| Reserve release delay | 0 to 7 days | Factors may hold your reserve for a few days after customer pays. Negotiate same-day release. |

Calculate your invoice factoring cost

Plug in your invoice amount, advance rate, factor fee, and days until your customer pays. Cash upfront, total fee, net proceeds, and APR equivalent update live.

Tiered fees warning Many factors bill 2% for the first 30 days then add 0.5 to 1% per extra week. If your customer pays slowly, increase the factor fee input to model the realistic cost.

Cash upfront

$8,500

Received within 24 to 48 hours

Total factor fee

$250

2.5% of invoice

Reserve released

$1,250

Paid when customer pays

APR equivalent

35.8%

Bank loan at 10% APR would cost about $70 for the same 30 days

APR benchmark

0% to 80% scale

Verdict On the higher side, negotiate or shop around

Factoring a $10,000 invoice at a 2.5% fee and 85% advance puts $8,500 in your account now. When your customer pays in 30 days, you receive the $1,250.00 reserve. Total fee $250.00, which works out to an 35.8% APR.

Estimates only, not financial advice. Actual fees vary by factor, industry, invoice volume, and customer creditworthiness. APR formula used is fee divided by advance amount, annualized over days outstanding.

The five types of invoice factoring

Most articles talk about factoring as a single product. It is not. Picking the wrong type can double or triple your effective cost. Here are the five varieties you will encounter.

- Recourse factoring. You are responsible for buying back any invoice the customer fails to pay within an agreed period (usually 60 to 90 days). Cheaper discount fees because the factor's risk is lower. This is the default for most providers.

- Non-recourse factoring. The factor absorbs the loss if your customer becomes insolvent. Fees run 0.5 to 1.5 percent higher than recourse. Read the contract carefully, "non-recourse" usually only covers customer bankruptcy, not disputes or slow payment. Riviera Finance specializes in non-recourse deals.

- Spot factoring. You factor one invoice at a time with no ongoing commitment. Fees are 25 to 50 percent higher than contract factoring. Useful for a single large invoice or seasonal one-off cash crunches. FundThrough's no-contract model qualifies as spot factoring.

- Contract factoring. You commit to factoring all invoices from designated customers (or all your invoices) for a 12 to 24 month period. Lowest discount rates, but you lose flexibility. Best for businesses with consistent monthly volume.

- Non-notification factoring. Your customers are not told you are using a factor. You keep collecting payments to a lockbox that routes funds to the factor. Roughly 1 percent more expensive than standard notification factoring. Useful when customer relationships are sensitive.

A simple rule of thumb, start with recourse + contract factoring if you have steady monthly volume, switch to spot factoring if your need is one-off, and pay the premium for non-recourse only if you have serious doubts about a specific customer's solvency.

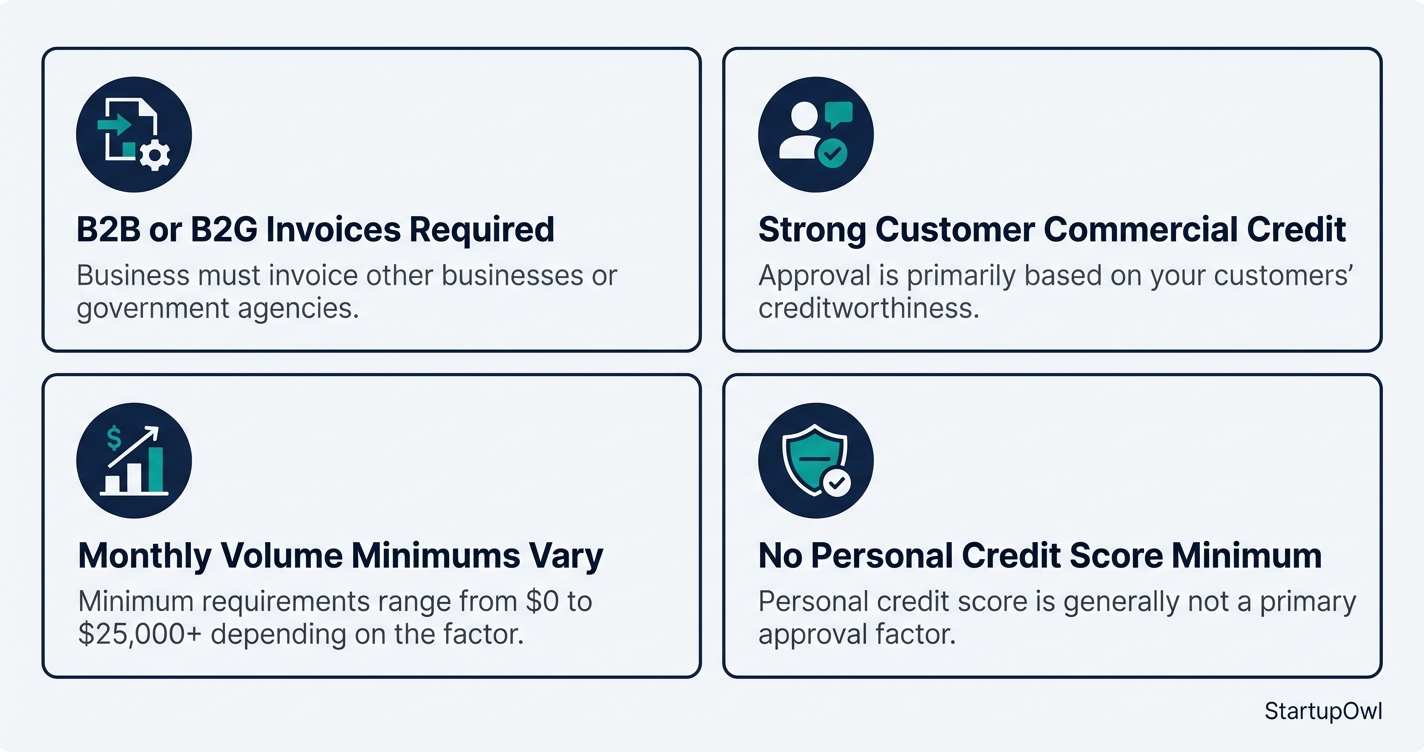

Who qualifies and what factors look for

Qualifying for invoice factoring is much easier than qualifying for a bank loan. Factors care primarily about your customers' credit, not yours. If your customers are creditworthy commercial businesses or government entities with a history of on-time payments, you are likely eligible.

Typical 2026 requirements across most providers.

- Business type. You must be B2B or B2G (business-to-government). Consumer invoices (B2C) are not eligible.

- Customer creditworthiness. Your customers need solid commercial credit. Government contracts are low-risk. Large corporations and established businesses with consistent payment histories get the best rates.

- Monthly invoice volume. Some factors require minimums. altLINE wants at least $15,000 per month. Gateway Commercial Finance starts at $25,000 per month. FundThrough and Riviera Finance have no monthly minimums, which makes them accessible for very small businesses.

- Your credit score. Most factors do not have a hard personal credit minimum. Your credit may be reviewed but carries far less weight than customer payment history. Businesses with poor or no credit history still qualify.

- Legal standing. You need a formalized business structure (LLC, corporation, etc.), a business bank account, and no open bankruptcies. Outstanding tax liens can complicate approval but are sometimes workable.

Startups without an established credit history can still qualify. Providers like altLINE work with startup staffing agencies, new distributors, and nonprofit startups, per LendingTree's reporting. For broader startup funding options, see our business loans for startups guide.

Different business profiles get different rates. The table below shows rough 2026 ranges by profile.

Rate ranges by business profile

| Type / Provider | Rate | Notes |

|---|---|---|

| Established B2B with Fortune 500 customers | 0.8 to 2.0% | Best rates. Large creditworthy customers and 2+ years of clean invoicing history. |

| B2B selling to mid-market companies | 1.5 to 3.0% | Typical small business range. Steady monthly volume expected. |

| Startup with small-business customers | 2.5 to 4.0% | Thin track record offset by customer diligence. Higher origination fee likely. |

| Staffing or agency with Fortune 500 contracts | 1.0 to 2.5% | Staffing is a preferred industry. Watch for volume minimums. |

| Owner-operator trucking | 2.0 to 3.5% | Fuel advances often available. Broker credit is the gating factor. |

| Freight broker | 3.0 to 5.0% | Broker factoring is a separate product with higher risk premiums. |

| Manufacturing or distribution | 1.5 to 3.0% | Clean delivery documentation (POD) drives approval speed. |

| Medical staffing or healthcare services | 1.0 to 2.5% | Preferred industry. Long payment cycles from hospitals factor into pricing. |

| Construction or trades | 2.5 to 4.5% | Progress billing and lien risk push rates higher. Mechanics liens matter. |

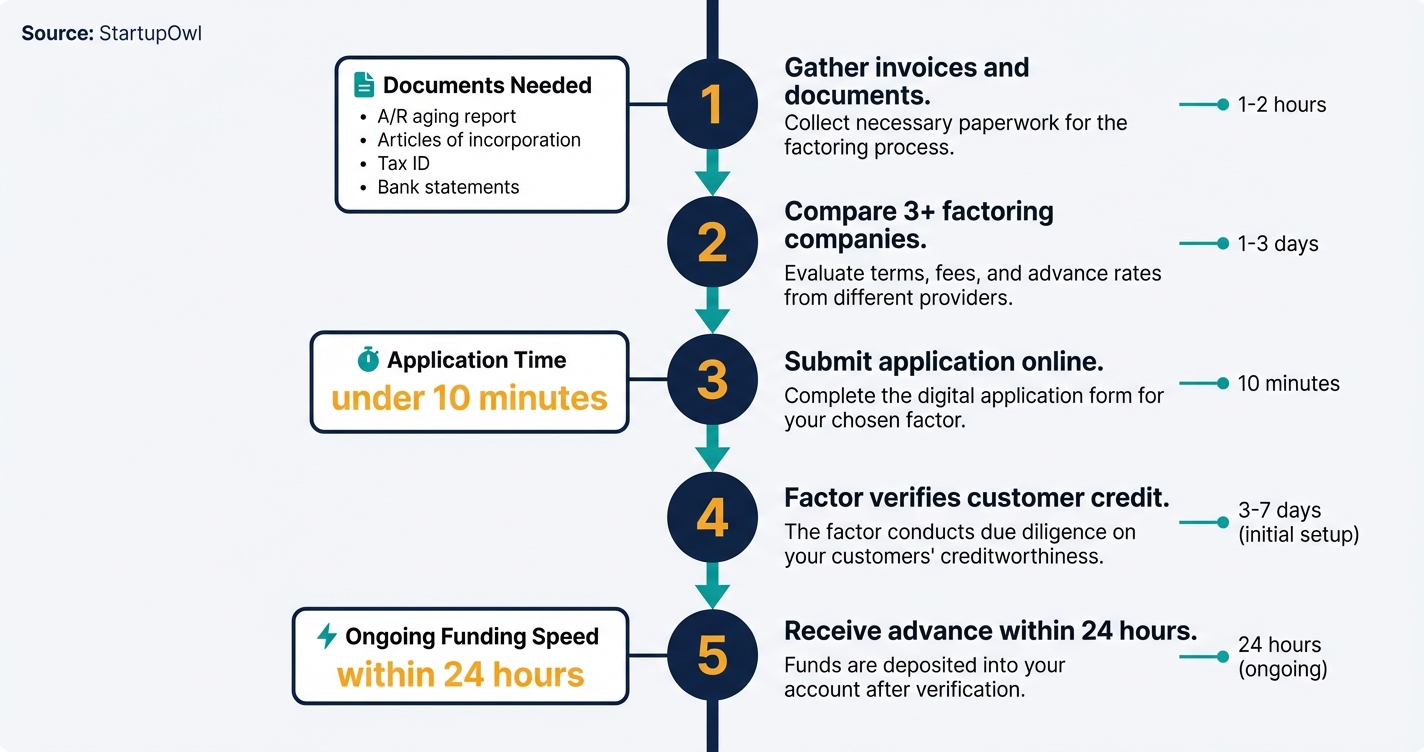

How to apply, step by step

The application is faster than almost any other business financing. Most factors let you apply online in under 10 minutes. Initial setup takes 3 to 7 business days. After that, ongoing invoice submissions fund within 24 hours.

- Pull your accounts receivable aging report. This shows the factor which invoices are outstanding, who owes what, and how long each has been open. Connect QuickBooks, Xero, or FreshBooks directly when the factor supports integration, that speeds up invoice verification dramatically.

- Gather your documents. Articles of incorporation, EIN letter, government-issued ID, the last 3 months of business bank statements, 3 to 5 sample customer invoices, and a list of customer contact names and emails.

- Submit the application. Most providers have a 5-question web form. A human underwriter typically reaches out within 24 hours to discuss rate and terms.

- Wait for customer credit checks. The factor pulls credit reports on your top customers. Any customer that fails the check will be excluded from what you can factor.

- Sign the agreement and receive the Notice of Assignment. The factor sends a Notice of Assignment to each approved customer, telling them to pay the factor directly. Once the NoA clears, you can submit invoices and expect funding within 1 business day.

For a full walkthrough on document preparation, see our how to get a business loan guide. The document prep overlaps substantially with factoring applications.

Documents checklist

- Accounts receivable aging report, current to within 7 days

- Articles of incorporation or LLC formation documents

- EIN confirmation letter from IRS

- Government-issued photo ID for each principal

- Last 3 months of business bank statements

- 3 to 5 sample customer invoices

- Customer contact list with names, emails, phone numbers

- Signed UCC-1 authorization (factor files this against your receivables)

- Most recent business tax return

- Proof of business address (utility bill or lease)

Invoice factoring vs other financing

Factoring is one of six main ways to cover short-term cash flow. The right choice depends on your margins, your credit, and whether you can wait.

How factoring compares to other financing

| Financing type | Rate | Notes |

|---|---|---|

| Invoice factoring | 12 to 60% APR equivalent | Same-day cash, no debt, customers notified, based on customer credit. |

| Invoice financing (discounting) | 15 to 50% APR equivalent | Similar cost, you keep collections, customers not notified, needs stronger credit. |

| Business line of credit | 8 to 25% APR | Cheapest flexible option. 600+ credit, 6+ months in business. Slower approval. |

| SBA 7(a) or microloan | 8 to 13% APR | Cheapest term capital. 30 to 90 day approval. Collateral required for 7(a). |

| Merchant cash advance | 40 to 150% effective APR | Fastest and most expensive. Daily repayment from sales. Avoid unless nothing else qualifies. |

| Business credit card | 18 to 29% APR | Fast, covers small expenses, great for travel and supplies. Not a scalable cash flow solution. |

When factoring makes sense and when it does not

Run through this 5-question scorecard before signing any factoring agreement. Score 1 point for every yes.

- Are your gross margins above 20 percent on the invoices you plan to factor?

- Do your customers typically pay on net 30 to net 90 terms (not net 7 or net 15)?

- Is waiting 30 to 90 days for customer payment actually choking your operations (missed payroll, delayed inventory, passed-up contracts)?

- Would a bank line of credit or SBA loan be unavailable, too slow, or significantly more expensive (after annualizing factoring)?

- Are you comfortable with your customers knowing you use a factor, OR can you afford the 1 percent premium for non-notification factoring?

5 out of 5, factoring is a strong fit. Move forward but compare 3 providers minimum.

3 or 4 out of 5, factoring might work but look at a business line of credit first. The APR gap is usually 15 to 20 points.

2 or fewer out of 5, factoring is probably the wrong tool. Consider a business line of credit, SBA microloan, or improving your collections process before financing.

The single biggest red flag is margin. If your gross margin on a project is 10 percent and the factoring fee is 3 percent, you just cut your profit by 30 percent. Factor invoices only when the cost of capital is small relative to the upside of getting paid early.

Industry rate benchmarks

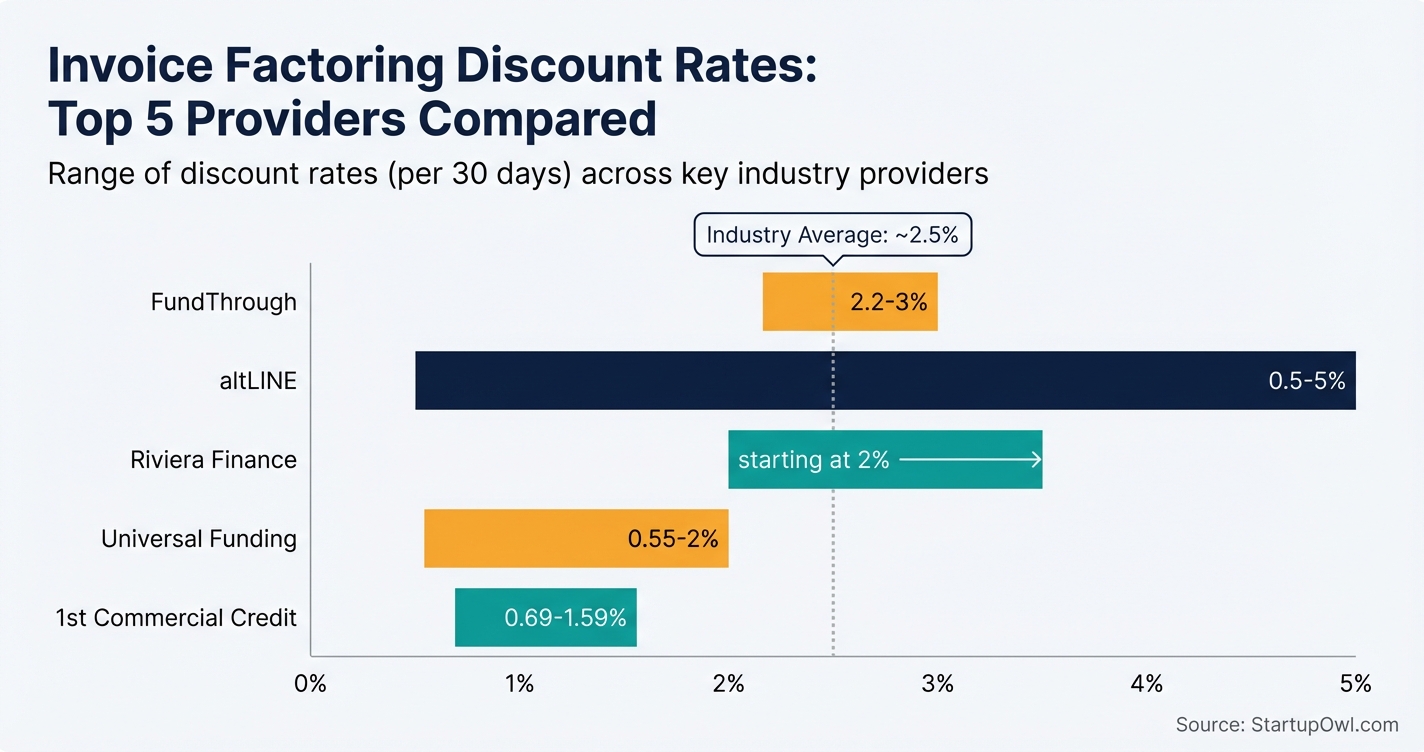

Invoice factoring rates vary more by industry than by provider. These ranges reflect publicly reported 2026 rates across the top 20 factoring companies, compiled from altLINE, Porter Capital, Bankrate, NerdWallet, and our own verification of provider pricing pages. Treat them as starting points for negotiation, not fixed quotes.

2026 industry rate benchmarks

| Industry | Rate | Notes |

|---|---|---|

| Staffing agencies | 1.0 to 2.5% / 30 days | Preferred industry. Clean invoicing and Fortune 500 customers drive rates down. |

| Medical and healthcare staffing | 1.0 to 2.5% / 30 days | Long payment cycles from hospitals and insurers are priced in. |

| Trucking owner-operator | 2.0 to 3.5% / 30 days | Fuel advance programs common. Broker credit drives the rate. |

| Freight broker | 3.0 to 5.0% / 30 days | Higher risk premium. Specialist broker-factoring providers only. |

| Manufacturing and distribution | 1.5 to 3.0% / 30 days | POD documentation drives speed and rate. Long-standing relationships price best. |

| Wholesale trade | 1.5 to 3.0% / 30 days | Volume discounts kick in above $100k/month factored. |

| Professional services (consulting, marketing) | 2.0 to 4.0% / 30 days | Service invoices can be disputed more easily, so factors price in chargeback risk. |

| Construction and trades | 2.5 to 4.5% / 30 days | Progress billing and mechanics liens complicate underwriting. Expect higher reserve requirements. |

| Oil and gas services | 2.0 to 3.5% / 30 days | Commodity price cycles drive rate volatility. Specialist providers preferred. |

| Janitorial and facilities services | 1.5 to 3.0% / 30 days | Recurring contracts with creditworthy property managers price well. |

Contract red flags to watch for

Factoring agreements are typically 15 to 30 pages of lender-friendly boilerplate. These 10 clauses deserve scrutiny and negotiation before you sign. A reputable factor will work with you on most of them.

Contract clauses to negotiate or reject

- Monthly minimum volume fees, negotiate the threshold or request a waiver for the first 3 months while you ramp

- Auto-renewal with long notice periods, cap at 30 days notice to cancel

- Termination notice longer than 60 days, shorten to 30 days

- Chargeback triggers broader than customer insolvency, limit to non-payment past agreed aging

- Interest charged on your held reserve, this should be zero

- ACH and wire fees per transfer, negotiate to $0 on ACH and $15 max on wires

- Lockbox routing fees, either eliminate or cap at $50/month

- Right of first refusal on future receivables, reject outright, keeps you dependent

- Personal guarantee scope beyond the factoring line, limit to factoring obligations only

- UCC-1 filing scope against all business assets, limit to accounts receivable only

How to tell your customers you are factoring

Customer notification is the single most overlooked cost of factoring. If handled badly, it looks like you are in financial trouble. Handled well, it looks like you have hired a modern receivables partner. Use the two templates below.

Template 1, proactive email to existing customers.

Subject, Updated payment instructions for [Your Company] invoices

Hi [Customer Name],

A quick heads-up. We have partnered with [Factor Name], a well-established commercial finance company, to manage our accounts receivable. Starting [date], please remit payment for invoices from [Your Company] to the address and bank details on the invoice (which will show [Factor Name] as the payee).

Nothing else changes. The same team delivers your work, the same contact handles your questions, and the payment terms on your contract stay exactly as we agreed. If you ever have a billing question, email [your AR email] and we will resolve it directly.

Thank you for being a great customer. If you have any questions about the new payment instructions, just reply to this email.

[Your Name]

Template 2, answer when a customer calls confused.

We have a standard arrangement with our finance partner, [Factor Name], to handle receivables. It is a common setup for growing businesses, it helps us invest in operations while we wait for payments to clear. You just pay the invoice per the instructions on it. If anything on the invoice is unclear or you want to dispute an item, reach out to me directly and we will sort it.

Two things to avoid. Do not frame the change as temporary ("just while cash flow stabilizes"), that signals trouble. And do not route billing questions through the factor, keep them direct with your AR team, since that is where customer trust lives.

Accounting and tax treatment

On your balance sheet, factoring is a sale of receivables, not a loan. When the factor advances cash, accounts receivable decreases and cash increases by the advance amount. The reserve the factor holds shows up as a receivable from the factor. When the customer pays and the factor releases the reserve, that receivable clears.

On your income statement, the factor's fee shows up as either a factoring fee line or an interest expense line. US GAAP tolerates either. Talk to your CPA about which line fits your existing chart of accounts. For tax purposes, factoring fees are deductible business expenses in the year incurred.

Two nuances worth knowing. First, if your factoring agreement is non-recourse and customer default risk genuinely transfers to the factor, the transaction is a true sale for GAAP purposes. If it is recourse, GAAP may treat it as a secured borrowing and you'd record a liability instead of derecognizing the receivable. Talk to your CPA. Second, your accounting software may have a specific factoring workflow, QuickBooks Online handles this through the "Invoice factoring" feature in its connected apps store.

Invoice factoring glossary

Eighteen terms you will hear during the sales call. Bookmark this section.

Advance rateThe percentage of invoice value the factor pays upfront, typically 80 to 100 percent. Aging reportA list of outstanding invoices grouped by how long they have been unpaid (0 to 30, 31 to 60, 61 to 90, 90+ days). ChargebackWhen the factor returns an unpaid invoice to you in a recourse arrangement, requiring you to buy it back. Concentration limitA cap on how much of your factored volume can come from a single customer, usually 20 to 40 percent. Discount feeThe factor's primary fee, expressed as a percentage of invoice value per 30-day period. FactorThe third-party company that buys your invoices. Ledgered lineA revolving factoring arrangement where you submit batches of invoices against an approved credit limit. LockboxA bank account dedicated to receiving customer payments, controlled by the factor. Non-notification factoringFactoring arrangement where customers are not told about the factor. Typically costs 0.5 to 1 percent more. Non-recourse factoringFactoring arrangement where the factor absorbs the loss if the customer becomes insolvent. Higher fees. Notification factoringStandard factoring where customers receive a Notice of Assignment and pay the factor directly. Notice of Assignment (NoA)The formal letter telling a customer to redirect payment to the factor. Recourse factoringFactoring arrangement where you are responsible for repayment if the customer does not pay. Lower fees. ReserveThe portion of invoice value held by the factor until the customer pays, typically 10 to 20 percent. Schedule of accountsThe list of invoices submitted for factoring in a given batch. Spot factorA factor that accepts one-off invoices without a long-term contract. Tiered rateA pricing structure where the discount fee increases in 10 or 15 day steps if the customer pays late. UCC-1The financing statement a factor files with your state to perfect its security interest in your receivables.Common mistakes that cost you money

1. Ignoring the total cost. Advertisers lead with low discount rates like "starting from 1.95 percent" but bury origination, wire, and minimum-volume fees. Always request a complete fee schedule and model your annual cost before signing.

2. Signing a long-term contract without understanding termination. Some agreements lock you in for 12 to 24 months with early termination fees of 1 to 3 percent of the credit line. If your cash flow improves and you no longer need factoring, you could be stuck paying for a service you don't use.

3. Factoring invoices with thin margins. If your margin on a project is 5 percent and the factoring fee is 3 percent, you just cut your profit by 60 percent. Factor only where the cost of early cash meaningfully benefits operations.

4. Failing to vet customer creditworthiness yourself. The factor does its own credit check, but you should track which customers pay on time and which do not. Factoring invoices from chronically late payers triggers tiered-rate penalties and erodes net recovery.

5. Taking the first quote without comparing. Rates, advance percentages, contract terms, and fees vary widely. Get quotes from at least 3 providers. The difference between the best and worst quote on a $500,000 annual volume is often $10,000 to $20,000.

6. Not negotiating the reserve release schedule. Some factors hold your reserve for 3 to 7 days after customer payment. Ask for same-day release. On a recurring flow, this difference is worth real money.

7. Listening only to your accountant. CPAs often recommend a factor they already work with. That relationship may be legitimate or it may reflect a quiet referral fee. Always shop independently. Our guide to building business credit can help you eventually qualify for lower-cost financing and exit factoring altogether.

Ready to pick a provider

When you are ready to compare the top factoring companies for 2026, our ranked guide to the best invoice factoring companies covers altLINE, FundThrough, Riviera Finance, Universal Funding, eCapital, Triumph Business Capital, RTS Financial, 1st Commercial Credit, Scale Funding, and Porter Capital with rates, advance percentages, contract terms, and who each one fits. altLINE wins overall, but six other providers win outright for specific personas including trucking, construction, same-day funding, and confidential factoring.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. Factoring rates and provider details reflect publicly available information as of April 2026 and may change without notice. The industry rate benchmarks are starting points for negotiation, not fixed quotes.

Step-by-Step Process

- 1

Gather your unpaid invoices and accounts receivable aging report

Pull together all outstanding B2B invoices you want to factor. You will need an accounts receivable (A/R) aging report that lists each unpaid invoice, the amount owed, and how long it has been outstanding. Most accounting software generates this report automatically.

You will also need your articles of incorporation, a government-issued photo ID, your business tax ID number, and recent bank statements. Having these documents ready before you apply can shave days off the approval process.

Tips

- Run your A/R aging report right before you apply so the data is current.

- Separate invoices from creditworthy customers (government contracts, Fortune 500 clients) from riskier ones, since the factor will likely offer better rates on stronger accounts.

Common Mistakes

- Submitting invoices that are already pledged as collateral to another lender, which disqualifies them from factoring.

- 2

Compare factoring companies and request quotes

Contact at least 3 factoring companies and request detailed pricing breakdowns. Ask each provider to spell out the discount rate, advance rate, any setup or origination fees, wire transfer charges, and early termination penalties. A provider advertising a 1% rate with hidden monthly minimums and wire fees may cost you more than one quoting 2.5% with no extras.

Pay special attention to whether the rate structure is flat or variable. A flat fee (for example, 3% per invoice) stays the same regardless of how long your customer takes to pay. A variable (tiered) rate might start at 2.5% for the first 30 days and then add 0.5% every 10-15 additional days the invoice stays unpaid.

Tips

- Request a full fee schedule in writing, including ancillary fees like ACH fees, lockbox fees, and credit check charges.

- Ask about spot factoring (choosing which invoices to factor) versus whole-ledger factoring (factoring all invoices), since spot factoring gives you more flexibility.

- Check whether the company offers recourse or non-recourse factoring and understand the cost difference.

Common Mistakes

- Signing a long-term contract without understanding early termination fees, which can run 1-3% of your credit line.

- Focusing only on the advertised discount rate while ignoring origination fees of $150-$500 and monthly minimums.

- 3

Submit your application and complete due diligence

Most factoring companies let you apply online in under 10 minutes. Upload your A/R aging report, articles of incorporation, tax ID, and bank account details. The factor will then run credit checks on your customers (not primarily on you) to verify they are creditworthy enough to pay their invoices on time.

Initial account setup for a new factoring relationship typically takes 3-7 business days. Some providers like FundThrough claim approval in under 5 minutes through automated integrations with QuickBooks and other accounting platforms.

Tips

- Connect your accounting software during signup to speed up invoice verification.

- Ask the factor how they will communicate with your customers, since some businesses worry about the perception of using a factoring company.

Common Mistakes

- Forgetting to check for existing UCC filings or tax liens against your business, which can delay or block approval.

- 4

Submit invoices and receive your advance

Once your account is active, you select the invoices you want to factor and submit them to the factoring company. The factor verifies each invoice with your customer (confirming the goods or services were delivered and the amount is correct). After verification, you receive your advance, typically 80-95% of the invoice value, deposited into your bank account.

Ongoing funding after your first transaction is usually much faster. Most established factoring relationships fund within 24 hours of invoice submission. Some providers offer same-day funding if you submit invoices before a specific cutoff time (for example, Porter Capital funds next-day for invoices submitted by noon Central Time).

Tips

- Submit invoices as early in the business day as possible to avoid missing same-day funding cutoffs.

- Track your factoring costs monthly in your accounting software to make sure the fees stay within your profit margins.

Common Mistakes

- Factoring invoices with razor-thin margins, where the 1-5% discount fee wipes out your profit on the job.

- 5

Collect the remaining balance after your customer pays

When your customer pays the full invoice amount to the factoring company, the factor releases the remaining balance (the reserve) to you, minus the discount fee. For example, on a $10,000 invoice with a 90% advance rate and a 2% factoring fee, you receive $9,000 upfront. When the customer pays, the factor keeps $200 (2% of $10,000) and sends you the remaining $800.

If you chose a variable-rate structure and your customer pays late, the fee can increase. Track your customers' payment timelines closely. If a customer routinely pays at 60+ days, consider whether invoice factoring is still cost-effective for those specific invoices.

$0 (reserve released minus fees already accounted for) 30-90 days (depends on customer payment terms) altline.sobanco.comTips

- Use a factoring calculator to model total costs before committing to a provider.

- Negotiate volume-based discounts if you plan to factor more than $50,000 per month in invoices.

Common Mistakes

- Ignoring late-payment penalties in your factoring agreement, which can add 0.5-1% for every additional 10-15 day period past the original terms.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Discount (Factoring) Fee | 1-5% of invoice face value per 30 days | The primary cost. Flat or variable structure. Average is around 2.5%. |

| Origination / Setup Fee | $150-$500 (or up to 1% of credit line) | One-time fee charged by some providers like altLINE at account opening. |

| ACH / Wire Transfer Fee | $5-$30 per transaction | Charged each time funds are transferred. Some providers waive this. |

| Monthly Minimum Fee | Varies by provider | Charged if you factor less than the monthly minimum volume. |

| Late Payment Penalty | 0.5-1% per additional 10-15 day period | Applies if your customer pays past the agreed invoice terms. |

| Early Termination Fee | Varies (typically 1-3% of credit line) | Triggered if you exit a long-term contract before the term ends. |

Frequently Asked Questions

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- NerdWallet, Invoice Factoring Guide

- Porter Capital, Invoice Factoring Rates and Fees

- United Capital Source, Factoring Rates Comparison

- altLINE, Invoice Factoring Homepage

- Gateway Commercial Finance

- Riviera Finance, Factoring Calculator

- Universal Funding, Factoring Rates

- FundThrough, Pricing

- NerdWallet, altLINE Factoring Review

- NerdWallet, Factoring Company Guide

- LendingTree, Factoring Companies

- eCapital, Invoice Factoring

- US Chamber, Understanding Factoring Receivables

- Bankrate, How Invoice Factoring Works

- PYMNTS, Small Business Cash Flow Research

- Federal Reserve, Small Business Credit Survey

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Invoice Factoring Explained for Small Business Owners

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment