SBA Microloan Program: How to Apply, Rates and Eligibility Requirements

SBA microloans offer up to $50,000 at 8-13% interest with a 620+ credit score. Learn eligibility, application steps, top lenders and costs for 2026.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Is an SBA Microloan and When Should You Use One

- Who Qualifies for an SBA Microloan

- How to Apply for an SBA Microloan Step by Step

- How Much an SBA Microloan Actually Costs

- Top SBA Microloan Intermediary Lenders to Consider

- What to Do If You Do Not Qualify for an SBA Microloan

- 5 Common SBA Microloan Mistakes That Cost You Time and Money

- FAQ

$0–$50,000

Est. Loan Cost

45 days

Timeline

5

Total Steps

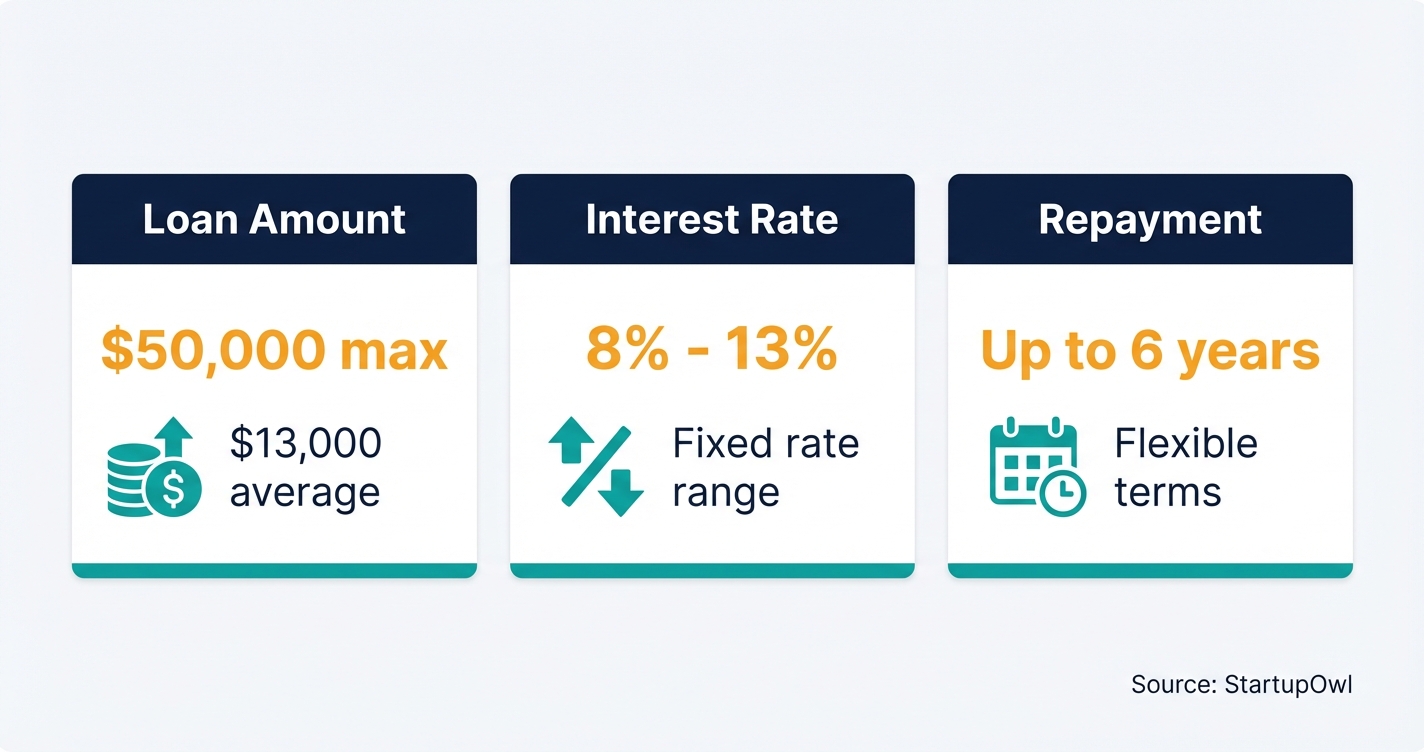

SBA microloans provide up to $50,000 in funding with interest rates between 8% and 13%, and the average loan size is about $13,000. The program is run through nonprofit community-based intermediaries (not the SBA directly), which means eligibility criteria are more flexible than a standard SBA loan.

About 24% of all SBA microloans issued in fiscal year 2024 went to startups (businesses operating for two years or fewer), making this one of the few government-backed lending programs that genuinely welcomes brand-new ventures. If you need less than $50,000 for equipment, supplies, or working capital, this guide covers exactly how to qualify, where to apply, and what it will cost you.

You cannot use SBA microloan proceeds to pay off existing debts or purchase real estate. For those needs, look at the SBA 7(a) program or a working capital loan from an online lender.

What Is an SBA Microloan and When Should You Use One

An SBA microloan is a small business loan of up to $50,000 offered through the SBA's Microloan Program and issued by SBA-approved nonprofit intermediary lenders. The SBA itself does not lend the money directly to you. Instead, it provides funds at a discounted rate to roughly 158 intermediary organizations across all 50 states, Washington D.C., and Puerto Rico, and those intermediaries then lend to eligible small businesses.

You can use the proceeds for working capital, equipment, inventory, supplies, furniture, and fixtures. Many intermediaries also provide free business training, mentoring, and technical assistance as part of the loan package. That built-in support makes SBA microloans especially valuable if you are in the early stages of building your business.

Consider this program if you need less than $50,000, have a personal credit score of 620 or above (some lenders go lower), and can wait 2-6 weeks for funding. If you need more capital, the best small business loans page compares larger options side by side. If your credit is below 580, you may want to explore invoice factoring or a merchant cash advance as a bridge while you build your business credit.

Who Qualifies for an SBA Microloan

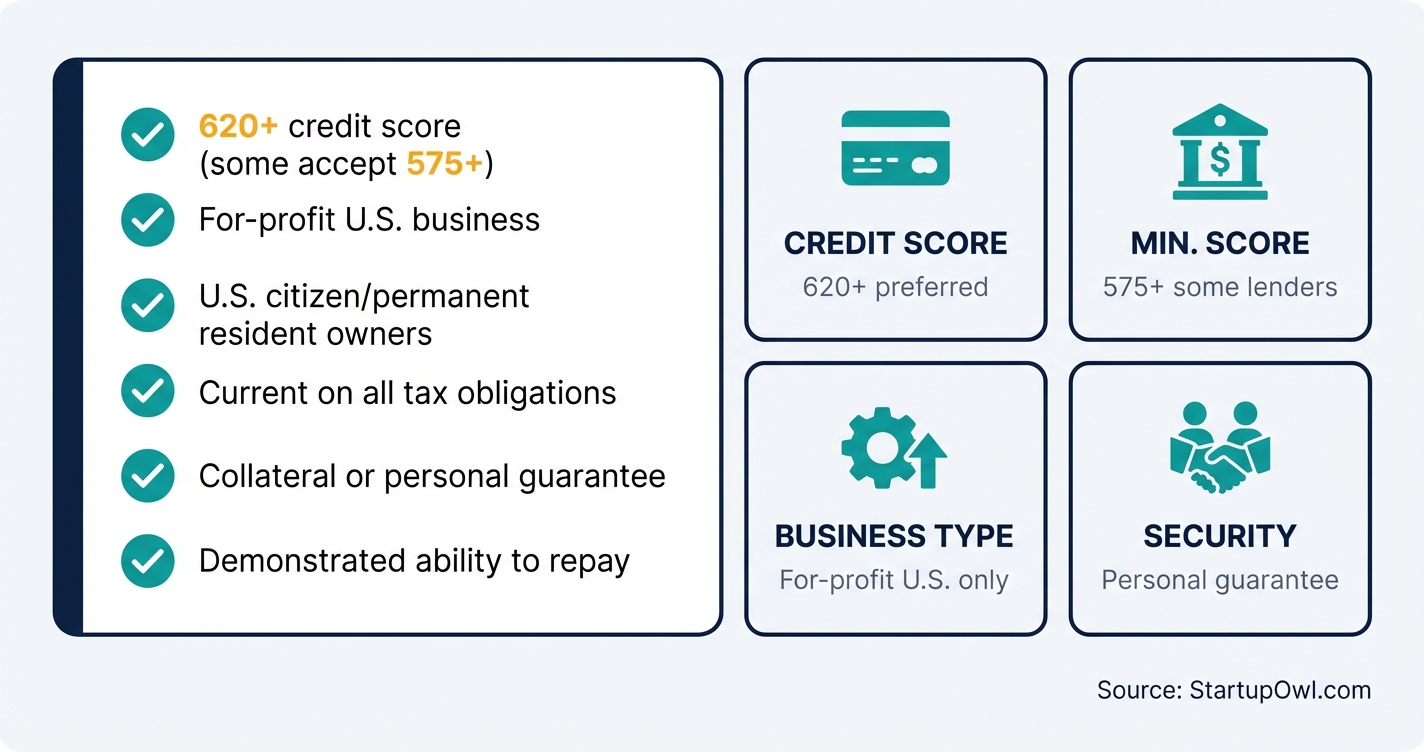

The SBA sets broad program rules, but each intermediary lender establishes its own specific credit and documentation requirements. Here is what you generally need to qualify:

- Business type: For-profit small business or qualifying nonprofit child care center operating in the United States.

- Ownership: All direct and indirect owners (and guarantors) with 20% or more stake must be U.S. citizens, U.S. nationals, or lawful permanent residents.

- Credit score: Most intermediaries prefer 620+, but some (like Ascendus) accept scores as low as 575. Merchant Maverick reports that many lenders target a score of around 640 or higher as of 2026.

- Tax compliance: Current on all federal, state, and local taxes with required filings completed.

- Government debt: No defaults on prior federal debt obligations, including existing SBA loans.

- Criminal history: No owner currently incarcerated, on parole, on probation, or under indictment for a felony involving moral turpitude.

- Collateral: Most lenders require some form of collateral (business assets, equipment, or personal property) plus a personal guarantee from the business owner.

- Ability to repay: You must demonstrate positive cash flow or provide realistic cash flow projections.

Time-in-business requirements vary dramatically. Some intermediaries work with day-one startups, while others may want two years of operating history. If you are a startup without revenue, a detailed business plan is your single most important document. Your business credit score will also be reviewed if you have one.

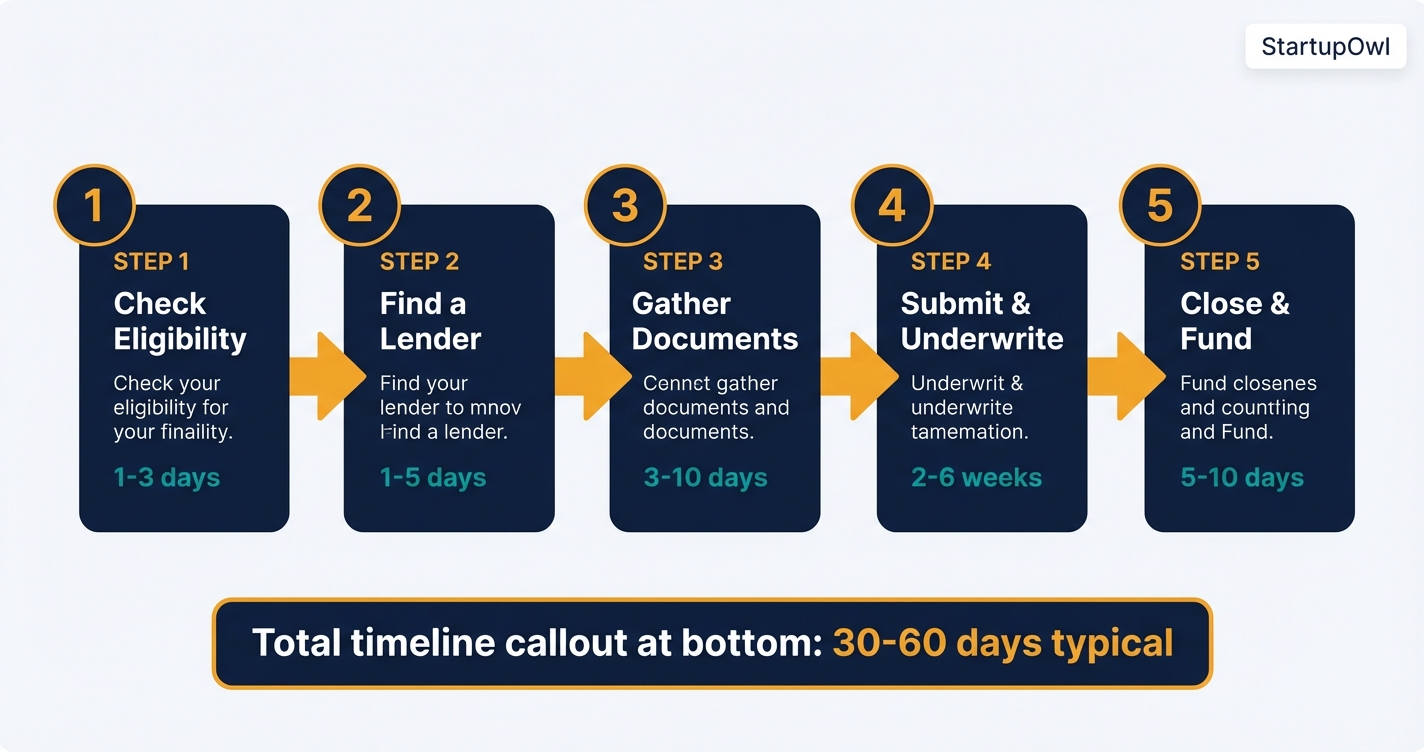

How to Apply for an SBA Microloan Step by Step

The application process is simpler than a standard SBA 7(a) loan because the intermediary lender makes all credit decisions without an additional SBA review layer. Here is the typical flow from start to funding:

Step 1: Check your eligibility. Verify your business structure, citizenship status, credit score, and tax compliance before you begin. Pull your free credit report at AnnualCreditReport.com.

Step 2: Find an intermediary lender. Use the SBA microlender directory to search by state. Contact at least two lenders to compare rates and terms.

Step 3: Gather your documents. You will typically need a business plan, personal and business tax returns (at least 2 years), financial statements, cash flow projections, a list of collateral, a debt schedule, and your business license or operating agreement.

Step 4: Submit and underwrite. Most lenders require you to apply in person or by phone. Faster intermediaries like Pursuit report decision times of two business days after receiving a complete application. The broader range is 2-6 weeks for most intermediaries.

Step 5: Close and fund. Sign your loan agreement and personal guarantee, pledge collateral, and receive funds. Total time from application to cash in hand typically runs 30-60 days.

How Much an SBA Microloan Actually Costs

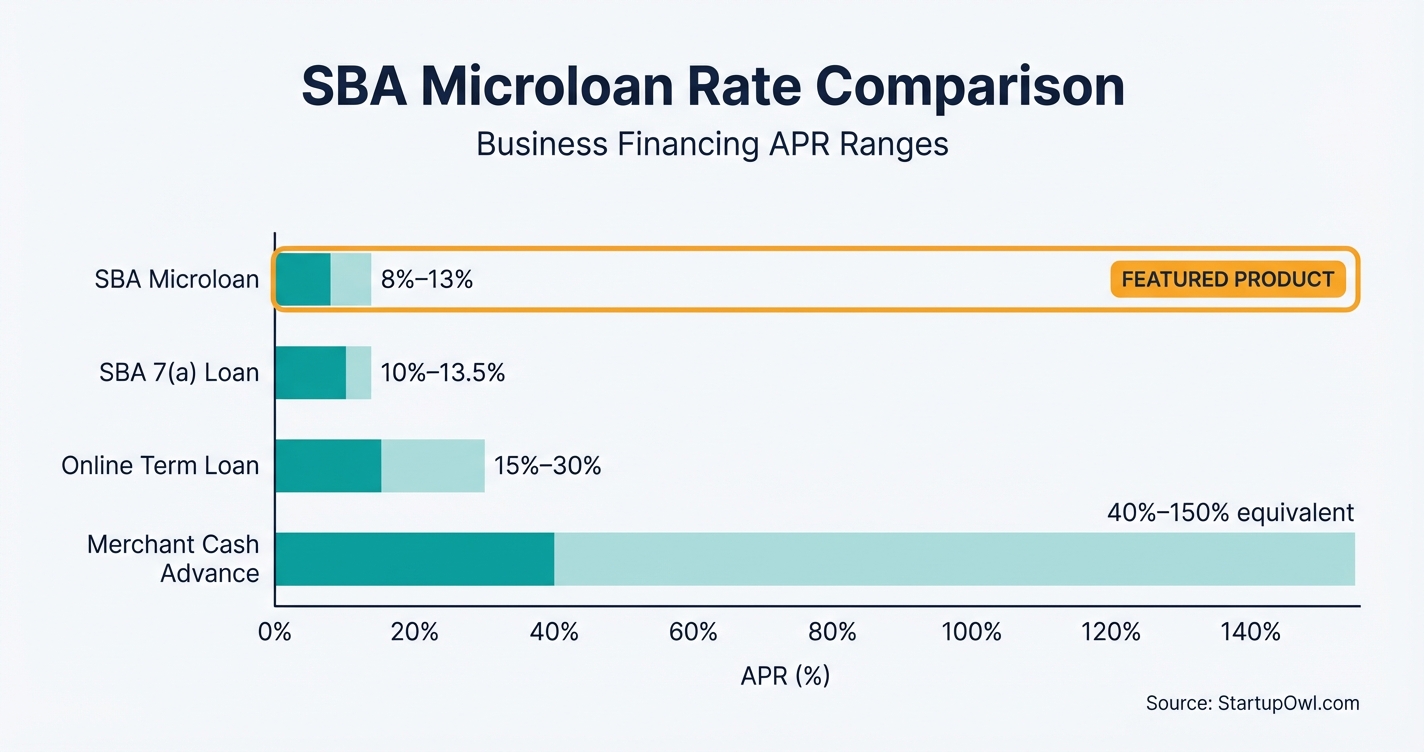

SBA microloan interest rates typically range from 8% to 13% as of 2026, according to Lendio, Bankrate, and Clarify Capital. The rate you receive depends on the intermediary's cost of funds (tied to the 5-year U.S. Treasury rate), your creditworthiness, your collateral, and the loan amount.

Behind the scenes, the SBA charges intermediaries a base rate tied to the 5-year Treasury Bill rate, minus 1.25% (or minus 2% for specialized intermediaries with average loan sizes of $10,000 or less). Intermediaries can then add up to 8.5 percentage points to whatever rate they pay the SBA. In practice, this caps rates at roughly 12-13% for most borrowers at most lenders.

Beyond the interest rate, intermediaries may charge fees of up to 3% of the loan amount plus additional closing costs that vary by lender. On the average $13,000 microloan, that is roughly $390 in fees at the maximum rate. Most SBA microlenders do not charge prepayment penalties, so you can pay your loan off early and save on interest.

For comparison, an online business line of credit typically charges 10-25% APR, and a merchant cash advance can cost the equivalent of 40-150% APR. The SBA microloan is among the cheapest small-dollar financing options available.

SBA Microloan Cost Breakdown (2026)

| Type / Provider | Rate | Notes |

|---|---|---|

| Interest Rate Range | 8% - 13% | Set by each intermediary lender; varies by credit profile and loan size |

| Maximum Repayment Term | 6 years (72 months) | Per SBA Standard Operating Procedure; monthly payments required |

| Loan Amount Range | $500 - $50,000 | Average loan is approximately $13,000 |

| Origination/Processing Fee | Up to 3% | Charged by the intermediary; some lenders charge $0 |

| Closing Costs | $100 - $500 | Document prep, filing fees; varies by lender |

| Prepayment Penalty | $0 at most lenders | Pay off early to reduce total interest cost |

| SBA Guarantee Fee | $0 | SBA does not charge fees to intermediaries under this program |

Top SBA Microloan Intermediary Lenders to Consider

Every SBA microlender is a nonprofit, so you will not find traditional banks on this list. Here are five established intermediaries worth contacting, each with slightly different strengths and geographic coverage:

- Justine Petersen (Missouri, Kansas, Illinois) issued $3.7 million in SBA microloans during fiscal year 2024, the most of any single intermediary. If you are in the Midwest, start here.

- LiftFund (Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Missouri, Mississippi, New York, New Mexico, Oklahoma, South Carolina, Tennessee, Texas) specializes in startups with limited credit, collateral, or experience. You must be at least 21 years old with no active bankruptcy.

- Pursuit (New York, New Jersey, Pennsylvania) offers one of the fastest turnaround times in the program: a decision within two business days of a complete application, with funding within 5 business days of approval. No prepayment penalty.

- Accion Opportunity Fund (45 states) offers loans from $5,000 to $250,000 with no minimum credit score requirement, though a score of 600+ improves your odds. They provide business coaching in English and Spanish.

- Ascendus (nationwide except Vermont and California) accepts credit scores as low as 575 and offers microloans up to $50,000. They also provide training, educational support, and childcare business loan programs.

To find every intermediary in your state, use the SBA's official microlender search tool. Rates, terms, and required documentation will differ from one lender to the next, so compare at least two before you commit.

Compare at Least Two Lenders Before You Apply

Because each intermediary sets its own rates (within the SBA's maximum caps), your interest rate on the same loan amount could differ by 3-5 percentage points between two lenders. On a $50,000 loan over 6 years, that difference adds up to thousands of dollars in total interest. Take the time to shop.

What to Do If You Do Not Qualify for an SBA Microloan

If you are denied or if the SBA microloan program does not fit your situation, you have several strong alternatives:

- Startup business loans from online lenders can fund faster (sometimes within 24-48 hours), though rates are typically 15-30% APR or higher.

- Small business grants offer debt-free funding that you never repay, though competition is intense and application timelines can stretch months.

- Business credit cards give you quick access to a revolving credit line, often with a 0% intro APR for 12-18 months on purchases.

- Invoice factoring lets you convert unpaid invoices into immediate cash (typically 80-90% of the invoice value) without a traditional credit check.

- Other microloans from non-SBA sources like Kiva (interest-free loans up to $15,000) or Grameen America (focused on women entrepreneurs) may have even more flexible eligibility.

If you were denied, note that you can reapply after a 90-day waiting period. Use that time to strengthen your business plan, build up savings, or improve your business credit score.

5 Common SBA Microloan Mistakes That Cost You Time and Money

- Applying without a business plan. Startups especially need a written plan with month-by-month cash flow projections. Without one, most intermediaries will reject your application outright, regardless of your credit score.

- Using proceeds for prohibited expenses. SBA microloan funds cannot be used to pay existing debts or purchase real estate. Violating these restrictions can trigger immediate loan default and repayment in full.

- Submitting incomplete documentation. Missing a single document (like a recent tax return or debt schedule) can stall underwriting for weeks. Prepare every item on the lender's checklist before you submit.

- Ignoring the lender's training requirement. Some intermediaries require you to complete a workshop or mentorship program before (or as a condition of) receiving funds. Skipping this step means no funding.

- Borrowing the maximum when you need less. The average SBA microloan is $13,000 for a reason. Borrowing more than you need means paying interest on capital that sits in your bank account. Request only what your business accounting setup tells you that you need.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Step-by-Step Process

- 1

Confirm your eligibility for the SBA microloan program

You need to operate a for-profit small business (or a qualifying nonprofit child care center) inside the United States. All owners with 20% or more stake must be U.S. citizens, U.S. nationals, or lawful permanent residents. You also need to be current on all federal, state, and local taxes with no open bankruptcies, and you cannot be incarcerated, on parole, or on probation for a felony.

Most intermediary lenders prefer a personal credit score of 620 or higher, though some will approve borrowers with scores in the 500s if you show strong business potential and sufficient collateral. Startups are welcome (about 24% of microloans in fiscal year 2024 went to businesses operating for two years or fewer), so time-in-business requirements vary widely by lender.

Tips

- Pull your free personal credit report at AnnualCreditReport.com before you start so you know exactly where your score stands.

- If your score is below 620, some intermediaries like Ascendus accept scores as low as 575.

Common Mistakes

- Assuming you need years of operating history when many microlenders work with brand-new businesses.

- Overlooking the citizenship requirement for all owners with 20% or more stake.

- 2

Find an SBA-approved intermediary lender in your area

SBA microloans are not issued by the SBA directly. Instead, you work with one of roughly 158 nonprofit intermediary lenders across all 50 states, D.C., and Puerto Rico. Each intermediary sets its own credit, collateral, and documentation requirements, so your experience (and your rate) can vary significantly by lender.

Use the SBA's official microlender directory to search by state. Major national or multi-state intermediaries include Justine Petersen (serving Missouri, Kansas, and Illinois), LiftFund (14 southern and eastern states), Pursuit (New York, New Jersey, Pennsylvania), and Ascendus (nationwide except Vermont and California).

Tips

- Contact at least two intermediaries to compare rates and requirements since each lender sets its own terms.

- Ask whether the lender requires you to complete a business training program before funding (some do).

Common Mistakes

- Applying to only one lender without shopping around for better rates or more flexible eligibility.

- 3

Gather your application documents

Expect to provide a thorough documentation package even though microloans have lighter paperwork than standard SBA 7(a) loans. At most intermediaries, you will need personal identification, your business license and operating agreement, a written business plan, at least two years of personal tax returns, business tax returns (if applicable), a balance sheet and income statement, cash flow projections, your business lease and contracts, a list of collateral and business assets, and an existing debt schedule.

If you are a startup without business tax returns, a detailed business plan with realistic financial projections becomes your most important document. Lenders use it to evaluate your ability to repay, so focus on clear revenue assumptions and a month-by-month cash flow forecast for at least 12 months.

Tips

- Prepare your cash flow projections in a spreadsheet with monthly detail for the first year and quarterly detail for years two and three.

- Have your personal and business bank statements from the last 3-6 months ready since many lenders ask for them during underwriting.

Common Mistakes

- Submitting incomplete documents, which can delay your approval by weeks.

- Inflating revenue projections in your business plan, which erodes lender trust.

- 4

Submit your application and complete underwriting

Most intermediary lenders require you to apply in person or over the phone rather than online. Some lenders, like Pursuit, offer a streamlined online application with a decision in as few as two business days after you submit all required documentation. Others may take 2-6 weeks from application to approval.

During underwriting, the lender will verify your credit history, evaluate your collateral, and assess your ability to repay. Unlike standard SBA 7(a) loans, the SBA itself does not review or approve your microloan application (that is entirely up to the intermediary), which speeds up the process.

$0-$1,500 (intermediaries may charge fees up to 3% of the loan amount plus closing costs) 2-6 weeks for most lenders SBA.govTips

- Respond to any document requests from your lender within 24-48 hours to keep the process on track.

- Ask your lender upfront about all fees so you can factor them into your total borrowing cost.

Common Mistakes

- Not responding promptly to lender follow-up requests, which is the number-one cause of application delays.

- 5

Close the loan and receive your funds

Once approved, you will sign a loan agreement, provide your personal guarantee, and finalize any collateral pledges. Most intermediaries require a personal guarantee from every owner with 20% or more ownership. Funds are typically disbursed within 5 business days of final loan approval at faster lenders, though the total timeline from first application to cash-in-hand is usually 30-60 days.

Your repayment schedule will begin according to the terms of your loan agreement. SBA microloans require at least monthly payments, balloon payments are not allowed, and the maximum repayment term is six years (per SBA Standard Operating Procedure). Some lenders may offer deferred payments for an initial period.

Tips

- Set up automatic payments from the start to avoid late fees and protect your credit.

- There is generally no prepayment penalty on SBA microloans, so pay it off early if cash flow allows.

Common Mistakes

- Using loan proceeds for prohibited expenses like paying off existing debt or purchasing real estate, which violates your loan agreement.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Interest rate | 8% - 13% APR | Set by each intermediary lender based on their cost of funds and your credit profile (as of 2026) |

| Origination or processing fee | Up to 3% of loan amount | Varies by intermediary; some charge $0 |

| Closing costs | $100 - $500 | May include document preparation and filing fees |

| Prepayment penalty | $0 | Most SBA microlenders do not charge prepayment penalties |

| Total interest on a $13,000 loan at 10% for 6 years | Approximately $4,300 | Based on average microloan size with standard monthly payments |

Frequently Asked Questions

Most SBA microloan intermediaries prefer a personal credit score of 620 or higher, though this is not an SBA-mandated minimum. Some intermediaries, like Ascendus, accept scores as low as 575, especially if your business shows strong cash flow or growth potential. If your score is below 600, expect to provide more collateral and pay a rate closer to the 13% ceiling.

Most applicants receive funds within 30-60 days of starting the application. Faster intermediaries like Pursuit can issue a decision in two business days and fund within 5 business days of approval. The biggest variable is how quickly you provide complete documentation.

Yes. About 24% of SBA microloans issued in fiscal year 2024 went to businesses operating for two years or fewer. The program was specifically designed for startups and underserved businesses. You will need a solid business plan with cash flow projections to compensate for your limited operating history.

You can use the funds for working capital, equipment, inventory, supplies, furniture, and fixtures. You cannot use SBA microloan proceeds to pay existing debts, purchase real estate, or cover personal expenses. Some intermediaries may allow debt refinancing at their discretion if it improves your cash flow.

The maximum SBA microloan is $50,000, and no borrower may owe an intermediary more than $50,000 at any one time. The average loan is about $13,000. If you need more than $50,000, look into the SBA 7(a) loan program, which goes up to $5 million.

Most intermediary lenders require some collateral (business assets, equipment, or personal property) plus a personal guarantee from the business owner. The specific collateral requirements vary by lender. If you are purchasing equipment with the loan, that equipment typically serves as the collateral.

SBA microloans at 8-13% are significantly cheaper than most alternatives for borrowers with limited history. Online business term loans typically run 15-30% APR, and merchant cash advances can cost the equivalent of 40-150% APR. Only standard SBA 7(a) loans (currently around 10-13.5% for variable rates) compete on price.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- U.S. Small Business Administration - Microloans

- SBA - List of Microlenders

- SBA - Operate as an Intermediary (Rate Structure)

- Lendio - Current SBA Loan Interest Rates (February 2026)

- Lendio - SBA Microloans: Rates, Requirements, and How to Apply

- Clarify Capital - Current SBA Loan Rates (2026)

- Bankrate - SBA Microloans

- NerdWallet - SBA Microloan: What It Is and How to Apply

- Merchant Maverick - SBA Microloans: Terms, Rates & Eligibility Guide

- Paychex - SBA Microloan Program: Eligibility & How To Apply

- Pursuit Lending - SBA Microloans

- United Capital Source - Current SBA Loan Interest Rates (January 2026)

- 13 CFR Part 120 Subpart G - Microloan Program (eCFR)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about SBA Microloan Program

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment