Startup Business Loans: Best Options for New Businesses With No Revenue History

Startup business loans range from 0% to 13% APR depending on the program. Compare SBA microloans, CDFIs, Kiva, and online lenders for new businesses with no revenue.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Startup Business Loans Are and When You Need One

- Credit Scores, Revenue, and What Lenders Actually Require

- How to Apply for a Startup Business Loan Step by Step

- What Startup Loans Actually Cost You

- Top 5 Startup Loan Options for Pre-Revenue Businesses

- What to Do If You Cannot Qualify for a Startup Loan

- 5 Expensive Mistakes New Business Owners Make With Startup Loans

- FAQ

$0–$50,000

Est. Loan Cost

30 minutes

Timeline

4

Total Steps

Getting a business loan with no revenue feels impossible, and for good reason: most traditional banks require 1 to 2 years of tax returns, established revenue, and strong business credit before they will even consider your application. But several government-backed and nonprofit programs exist specifically for your situation.

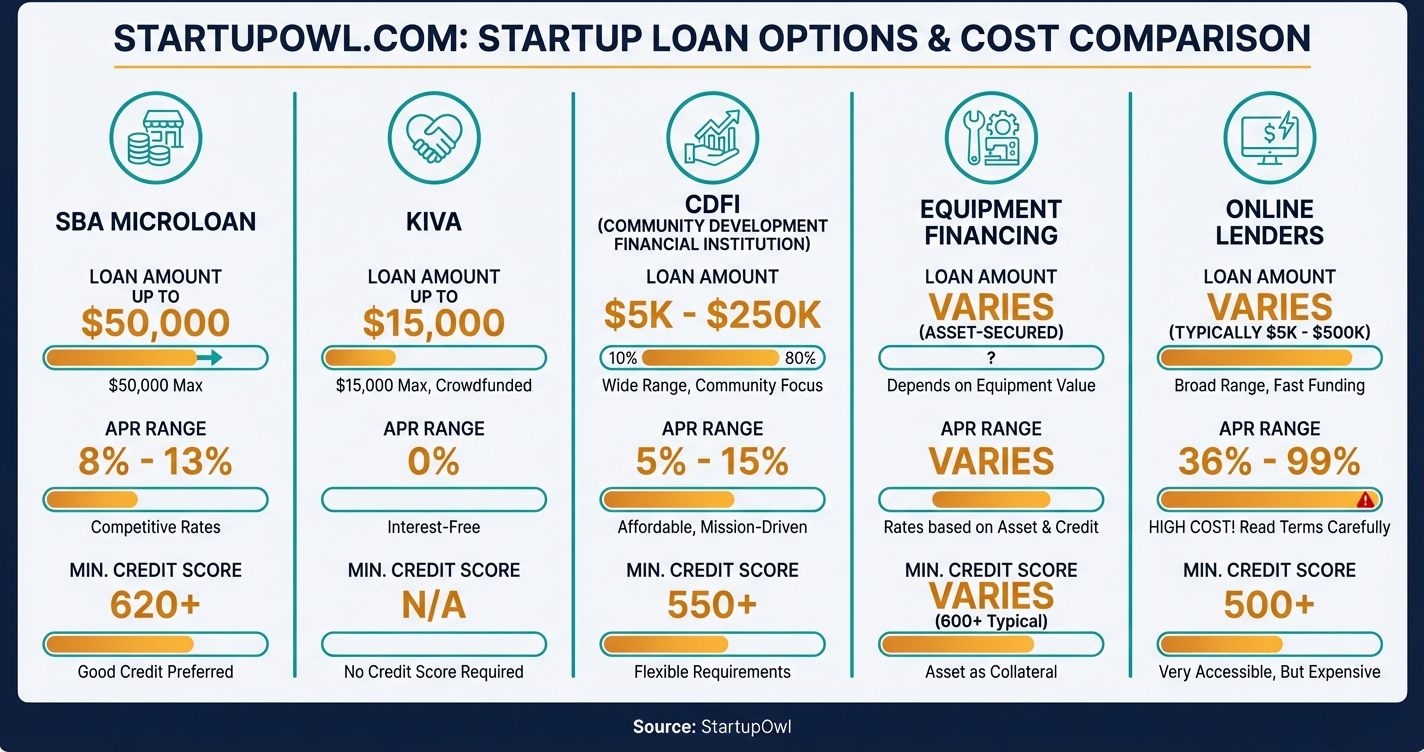

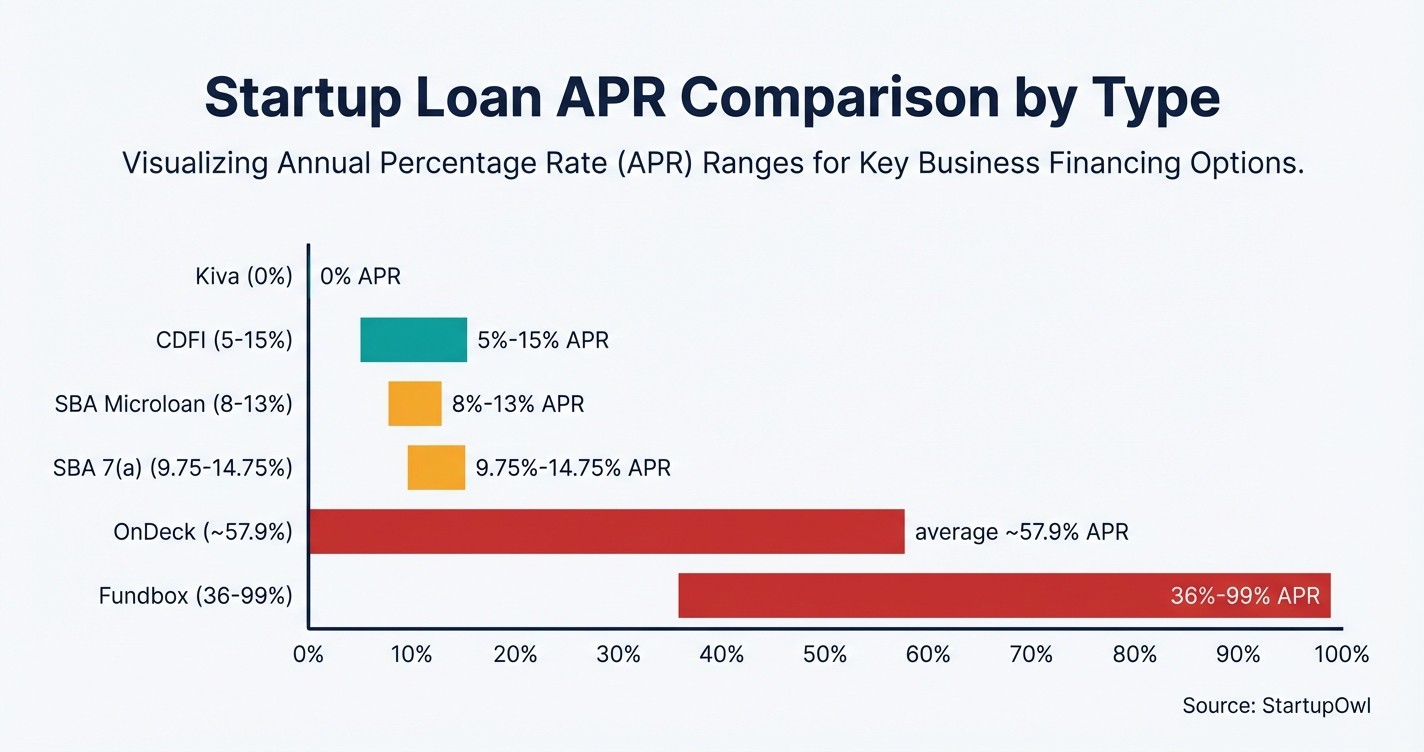

SBA microloans provide up to $50,000 at 8% to 13% interest through nonprofit intermediaries that evaluate your business plan quality over your revenue history. Some founders skip the startup phase and buy a running business instead, our how to buy a laundromat guide walks that path. Kiva offers 0% interest crowdfunded loans up to $15,000 with no minimum credit score requirement. CDFIs (Community Development Financial Institutions) lend $5,000 to $250,000 at rates that average 5% to 6% according to CDFI Fund data.

This guide covers every realistic startup loan option, with verified rates, credit score requirements, and step-by-step instructions so you know exactly where to apply first. If you are still deciding on your business structure, check out our LLC formation guide before applying for financing.

What Startup Business Loans Are and When You Need One

A startup business loan is any financing you use to launch a new business before you have consistent revenue. Unlike loans for established companies, startup loans rely heavily on your personal credit score, the strength of your business plan, and your willingness to provide a personal guarantee or collateral.

According to Gallup, 77% of small business owners use personal savings as their initial capital source. But personal savings alone rarely covers the full cost of launching. You need a startup loan when your launch costs (inventory, equipment, marketing, lease deposits) exceed what you can self-fund and you are not ready to give up equity to angel investors.

The SBA closed fiscal year 2026 with a record $44.8 billion in guaranteed loans, with over 50% of 7(a) loans under $150,000. That shift toward small-dollar lending means more startup-friendly programs than ever. Your best options as a pre-revenue founder fall into five categories: SBA microloans, Kiva crowdfunded loans, CDFI loans, equipment financing, and business credit cards.

Credit Scores, Revenue, and What Lenders Actually Require

Without revenue, lenders focus almost entirely on your personal financial profile. Here is what each loan type requires from a pre-revenue startup:

- SBA Microloans typically want a personal credit score of 620 to 680. Each intermediary lender sets its own requirements, but most use more relaxed credit standards than traditional business loan programs. You do not need perfect credit, but a past bankruptcy or foreclosure makes approval harder.

- Kiva has no minimum credit score, no minimum revenue, and no minimum time in business. Qualification is based on your story, community support, and a soft credit inquiry. You cannot be in foreclosure, bankruptcy, or under any liens.

- CDFIs have flexible credit requirements. For example, Accion Opportunity Fund requires only a 620 credit score and $100,000 in annual revenue with 12 months in business. Many CDFIs will lend to true startups with shorter track records.

- Equipment Financing may have no minimum revenue and no minimum time in business, because the equipment itself serves as collateral. You will need decent personal credit.

- Online Lenders like Fundbox require at least 3 to 6 months in business, a 600+ credit score, and $30,000 in annual revenue. OnDeck requires 12 months in business, a 625 credit score, and $100,000 in annual revenue.

Across all startup loan types, expect to provide a personal guarantee. This means if your business cannot repay, you are personally liable. For a deeper look at how your credit profile affects borrowing, see our guide on business credit scores.

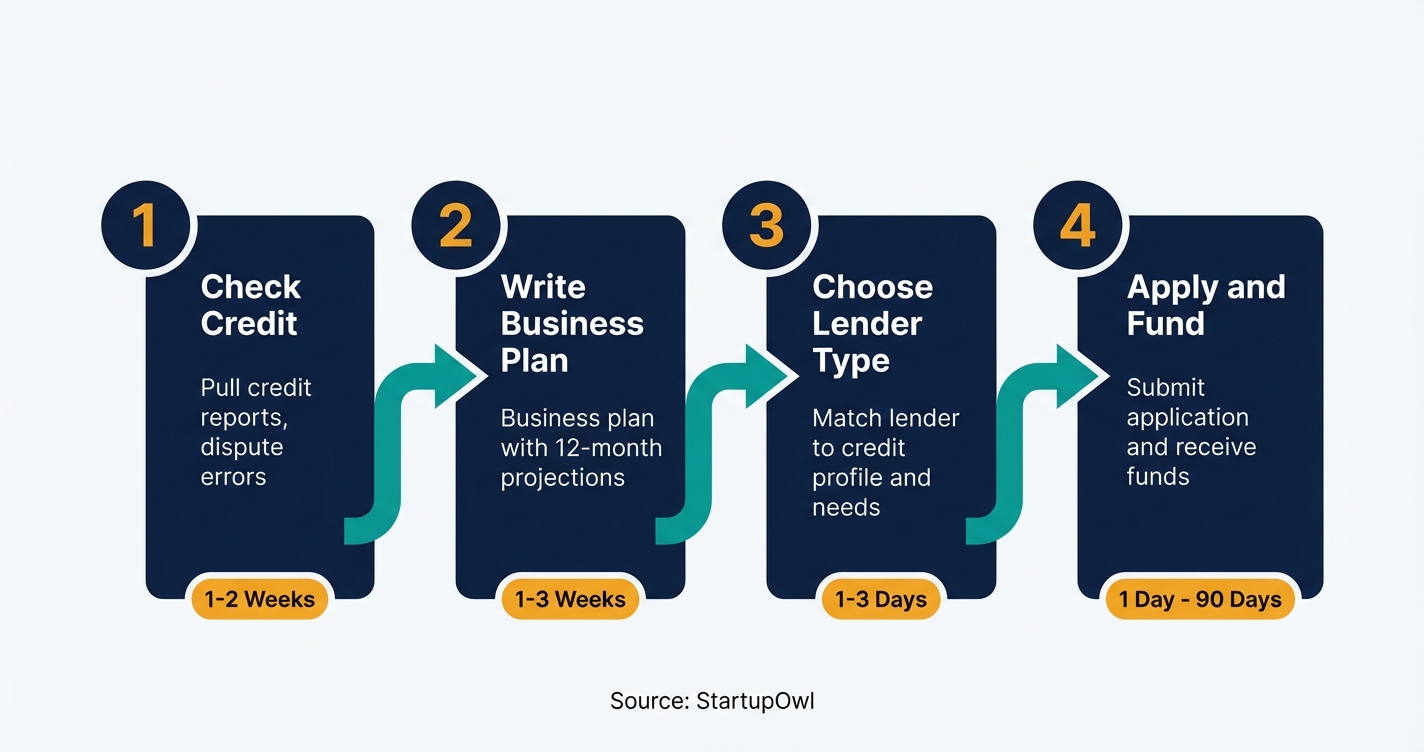

How to Apply for a Startup Business Loan Step by Step

The application process varies by lender type, but the fundamentals are the same: prove you are a good credit risk despite having no revenue history. Here is the general flow.

Step 1: Pull your personal credit reports from all three bureaus at AnnualCreditReport.com. Dispute any errors and pay down revolving balances below 30% utilization. This single step can raise your score by 20 to 50 points within 30 days.

Step 2: Write a detailed business plan that includes 12-month financial projections, a clear explanation of fund use, and your break-even timeline. The SBA's free template is a solid starting point. For pre-revenue businesses, this document replaces your revenue history in the eyes of the lender.

Step 3: Choose the right lender type. Use the SBA microloan intermediary locator for government-backed options. For CDFIs, use the CDFI Fund's searchable database or the Opportunity Finance Network's CDFI locator. For a marketplace approach, Lendio matches you with over 75 lenders in about 15 minutes.

Step 4: Gather documents and submit. Have your personal tax returns (2 years), government ID, bank statements (3 months), business plan, and collateral list ready. SBA microloans take 30 to 90 days from application to funding. Online lenders and Kiva can fund in 1 to 45 days depending on the platform. For the full application walkthrough, read our how to get a business loan guide.

What Startup Loans Actually Cost You

The total cost of a startup loan varies dramatically based on the program you choose. Here is a realistic breakdown:

SBA microloans carry interest rates of 8% to 13%, set by the intermediary lender, with repayment terms of up to 6 years (7 years per some intermediaries). On a $13,000 loan (the average SBA microloan) at 10% over 5 years, you would pay roughly $3,500 in total interest.

SBA 7(a) loans range from 9.75% to 14.75% as of February 2026, based on a prime rate of 6.75% plus the SBA's allowable spread. Guarantee fees for loans of $150,000 or less are just 0.25% of the guaranteed portion in fiscal year 2026.

Kiva loans cost $0 in interest and $0 in fees. Repayment terms extend up to 36 months. The only cost is your time recruiting supporters during the crowdfunding period.

Online lenders are the most expensive option. OnDeck's average APR for term loans is approximately 57.9%, and Fundbox charges weekly fees starting at 4.66% for 12-week terms. These rates are appropriate only when you need fast capital and cannot qualify for SBA or CDFI programs. See our best small business loans comparison for rate details by lender.

Startup Loan Rates and Terms Compared

| Type / Provider | Rate | Notes |

|---|---|---|

| SBA Microloan | 8% - 13% APR | Up to $50,000; avg. $13,000; terms to 6 yrs; nonprofit intermediaries |

| SBA 7(a) Loan | 9.75% - 14.75% APR | Up to $5M; prime + 2.75%-6%; requires 680+ credit score |

| Kiva Crowdfunded Loan | 0% APR, $0 fees | $1,000-$15,000; 36-month term; crowdfunding takes 15-45 days |

| CDFI Loan | 5% - 15% APR | $5,000-$250,000; flexible credit; mission-driven lenders |

| Fundbox Line of Credit | 36% - 99% APR | Up to $150,000; 600 credit score; 3 months in business; $30K revenue |

| OnDeck Term Loan | ~57.9% avg. APR | Up to $250,000; 625 credit; 12 months in business; $100K revenue |

Top 5 Startup Loan Options for Pre-Revenue Businesses

1. SBA Microloan Program (Best Overall for True Startups)

The SBA microloan is purpose-built for new and underserved businesses. You can borrow up to $50,000 at 8% to 13% interest through nonprofit intermediary lenders. The average loan is about $13,000. These lenders often include free business counseling and technical assistance. You cannot use microloans for real estate purchases or to pay off existing debt. Apply through an SBA-approved intermediary.

2. Kiva (Best for Zero-Cost Capital Under $15,000)

Kiva offers 0% interest, zero-fee, zero-collateral crowdfunded loans from $1,000 to $15,000 with up to 36 months to repay. There is no minimum credit score, no minimum revenue, and no minimum time in business. You must recruit supporters from your personal network to partially fund your loan before it goes public on Kiva's platform. The process takes 15 to 45 days. Apply at kiva.org/borrow.

3. CDFI Loans (Best for Underserved Communities)

CDFIs are mission-driven lenders certified by the U.S. Department of the Treasury. They offer competitive rates that average 5% to 6% per CDFI Fund data, with loan amounts from $5,000 to $250,000+. CDFIs focus on serving minority, women, and veteran-owned businesses, as well as those in low-income areas. Many CDFIs will lend to true startups. Find one near you through the CDFI Fund's searchable database.

4. Lendio Marketplace (Best for Comparing Multiple Offers)

Lendio matches you with over 75 lenders, including those that offer startup-specific products. You can apply online in about 15 minutes and potentially receive funding within 24 hours depending on the lender. There is no minimum credit score from Lendio itself, but individual lenders in the marketplace set their own requirements (typically 650+ for most products). Apply at lendio.com.

5. Fundbox (Best for Very New Businesses With Some Revenue)

Fundbox offers business lines of credit up to $150,000 with just 3 months in business, a 600 credit score, and $30,000 in annual revenue. Weekly fees start at 4.66% for 12-week terms. Funding can arrive as fast as the next business day. This is not a zero-revenue option, but it has the lowest revenue threshold among online lenders. Consider Fundbox as a bridge once you start generating early sales. For card-based alternatives, see our best business credit cards roundup. And consider the sideways move, buying an existing business can finance at 8.5% to 9% because lenders price its proven cash flow, not your projections.

Apply to SBA and CDFI Programs First

Always start with the cheapest capital. Apply for an SBA microloan or a CDFI loan before turning to online lenders. Even if the SBA process takes 30 to 90 days, you could save thousands in interest compared to an online lender charging 36% to 99% APR. Only turn to online lenders if you need emergency capital or cannot meet SBA/CDFI requirements.

What to Do If You Cannot Qualify for a Startup Loan

If your credit score is below 600 and you have zero revenue, traditional startup loans (even SBA microloans) may be out of reach right now. Here are your best alternatives:

- Kiva crowdfunded loans have no credit score minimum. If you can recruit 10 to 25 supporters from your personal network, you can access up to $15,000 at 0% interest.

- Small business grants do not require repayment. Federal, state, and private programs exist for women, minority, and veteran-owned startups. The competition is fierce, but the capital is free.

- Business credit cards evaluate your personal creditworthiness rather than business revenue. Many offer 0% intro APR periods of 12 to 18 months. You can use them for inventory, software, and marketing while building your business credit history.

- Equipment financing uses the purchased asset as collateral, so some lenders have no minimum revenue and no minimum time in business. You will need decent personal credit.

- Pre-seed funding from angel investors or friends and family is equity-based (not debt), which means no monthly payments. The trade-off is giving up partial ownership of your company.

If debt feels too risky at your current stage, consider microloans for small business starting at just $1,000 to test your concept before scaling up.

5 Expensive Mistakes New Business Owners Make With Startup Loans

1. Applying to traditional banks first. Most banks require 1 to 2 years of business tax returns, established revenue, and strong business credit. Applying to a bank with no revenue wastes time and results in hard credit inquiries that lower your score. Start with SBA intermediaries, CDFIs, or Kiva instead.

2. Skipping the business plan. For no-revenue startups, your business plan replaces your financial track record. SBA microloan intermediaries and CDFIs weigh your plan heavily. Without one, your application will likely be denied regardless of your credit score.

3. Not understanding personal guarantee implications. Nearly every startup loan requires a personal guarantee. This means your personal assets (savings, home equity, vehicle) are at risk if the business cannot repay. Know exactly what you are pledging before you sign.

4. Borrowing more than your first-year projections support. If your realistic revenue projection shows $60,000 in year one, do not borrow $50,000. Aim to keep your total annual debt service below 25% of projected revenue. Over-leveraging a pre-revenue startup is the fastest path to personal financial trouble.

5. Choosing fast funding over affordable funding. Online lenders like OnDeck can fund within 24 hours, but their average APR runs around 57.9%. An SBA microloan at 10% on the same amount could save you thousands over the loan term. Patience pays.

Watch for Predatory Lending Warning Signs

The SBA warns that some lenders impose unfair terms through deception and coercion. Red flags include interest rates significantly higher than competitors, fees exceeding 5% of the loan value, pressure to sign immediately, and requests to leave signature boxes blank. Always compare at least 3 offers before committing.

Step-by-Step Process

- 1

Check your personal credit score and fix errors

Most startup lenders evaluate your personal credit because your business has no track record. Pull your free credit reports from all three bureaus and dispute any errors. A score of 620 or higher opens SBA microloan eligibility, while 680+ qualifies you for SBA 7(a) loans.

If your score is below 600, focus on Kiva (no minimum credit score) or secured business credit cards to build credit before applying for traditional startup loans.

$0 (free credit reports at AnnualCreditReport.com) 1-2 weeks to pull reports and dispute errors annualcreditreport.comTips

- Pull reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com for free once per year.

- Dispute errors in writing and keep copies of all correspondence.

- Pay down revolving credit balances below 30% utilization to boost your score quickly.

Common Mistakes

- Applying for multiple loans before checking your credit, which triggers hard inquiries that lower your score.

- Ignoring personal credit entirely and assuming business credit alone matters for startup loans.

- 2

Write a detailed business plan with financial projections

When you have no revenue, your business plan is your strongest asset. SBA microloan intermediaries and CDFIs prioritize the quality of your plan over your financial history. Include a clear explanation of how funds will be used, a 12-month cash flow projection, and your market analysis.

The SBA offers free business plan templates on its website. At minimum, cover your revenue model, target customers, marketing strategy, and how quickly you expect to break even.

Tips

- Include a realistic 12-month cash flow projection showing exactly when you expect revenue to start.

- Explain specifically how you will use every dollar of the loan proceeds.

- Have a SCORE mentor review your plan for free before submitting it to lenders.

Common Mistakes

- Submitting a vague plan without specific dollar amounts for expenses and projected revenue timelines.

- Overestimating first-year revenue, which makes lenders question your judgment.

- 3

Identify the right loan type for your situation

Your credit score, funding amount, and timeline determine which loan type fits. If you need under $15,000 and can wait 15 to 45 days, Kiva offers 0% interest with no credit score requirement. For up to $50,000, an SBA microloan charges 8% to 13% and includes business mentoring.

If you need more than $50,000 and have a credit score of 680+, the SBA 7(a) program lends up to $5 million at rates of 9.75% to 14.75% as of February 2026. CDFIs are your best bet if you are in an underserved community, with rates as low as 5% to 6% on average.

Tips

- Start with SBA microloans or Kiva if you have zero revenue; they are designed for pre-revenue businesses.

- Use the SBA Lender Match tool to find approved intermediaries in your area.

Common Mistakes

- Applying to a traditional bank first; they rarely approve startups with no revenue and typically require 1-2 years of tax returns.

- 4

Gather your documents and apply

Most startup loan applications require your personal tax returns (2 years), government-issued ID, business plan, financial projections, and a list of how you will use the funds. SBA microloan intermediaries may also ask for a personal guarantee and collateral description.

For online applications through platforms like Lendio, you can apply in about 15 minutes and potentially get matched with multiple lenders. SBA microloan applications take longer (typically 30 to 90 days from application to funding) but offer significantly lower rates.

$0 to apply (most lenders do not charge application fees) 15 minutes to 90 days depending on lender type SBA.govTips

- Have your last 3 months of bank statements ready; most lenders want to see your personal cash flow.

- Apply to multiple lenders at the same time to compare offers without committing.

- Ask each lender about personal guarantee requirements before signing anything.

Common Mistakes

- Not reading the full loan agreement, especially sections on personal guarantees and prepayment penalties.

- Borrowing more than you can realistically repay within the first 12 months of business operations.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| SBA Microloan Interest | 8% - 13% APR | Up to $50,000; average loan is $13,000; terms up to 6 years (as of 2026) |

| SBA 7(a) Loan Interest | 9.75% - 14.75% APR | Up to $5 million; based on prime rate of 6.75% as of February 2026 |

| CDFI Loan Interest | 5% - 15% APR | Varies widely by institution; average hovers around 5%-6% per CDFI Fund data |

| Kiva Microloan | 0% APR, $0 fees | $1,000 - $15,000; crowdfunded; repayment up to 36 months |

| Online Lenders (Fundbox, OnDeck) | 36% - 99% APR | Fast funding but expensive; require 6-12 months in business and $30K-$100K revenue |

| SBA 7(a) Guarantee Fee | 0.25% of guaranteed portion | For loans of $700,000 or less as of fiscal year 2026 |

| OnDeck Origination Fee | 0% - 4% | Charged on term loans; deducted from loan proceeds |

Frequently Asked Questions

Yes, but your options are limited to a handful of programs. Kiva offers 0% interest loans up to $15,000 with no revenue requirement. SBA microloans (up to $50,000 at 8% to 13%) evaluate your business plan rather than revenue history. Equipment financing lenders may also work with zero-revenue startups because the equipment itself serves as collateral.

Most startup-friendly lenders want a personal credit score of 620 or higher. SBA microloans typically require 620 to 680, while SBA 7(a) loans generally need 680+. Kiva has no minimum credit score. Online lenders like Fundbox accept scores as low as 600, but charge significantly higher rates.

Timing varies by lender type. Online lenders like OnDeck and Fundbox can fund in 1 to 3 business days. Kiva's crowdfunding process takes 15 to 45 days. SBA microloans typically take 30 to 90 days from application to funding. Plan your cash needs accordingly and apply well before you need the money.

Kiva offers the cheapest capital at 0% interest with zero fees on loans from $1,000 to $15,000. After Kiva, CDFI loans average 5% to 6% interest, and SBA microloans charge 8% to 13%. Avoid merchant cash advances and high-APR online lenders unless you have no other option.

It depends on the program. Kiva requires no collateral. SBA microloan intermediaries may ask for collateral and a personal guarantee, but requirements vary by lender. Equipment financing uses the purchased asset as collateral. Online lenders like OnDeck typically require a blanket lien on business assets and may require a personal guarantee.

A personal loan can work as a temporary bridge if you cannot qualify for a business loan for your startup, but it has drawbacks. Personal loan interest is generally not tax-deductible as a business expense, while business loan interest typically is. Personal loans also do not help you build a business credit score. Use this route only if SBA, CDFI, and Kiva options are unavailable.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA Microloan Program

- SBA Loan Programs Overview

- Kiva U.S. Loan Application

- CDFI Fund (U.S. Department of the Treasury)

- Current SBA Loan Interest Rates (Lendio, February 2026)

- SBA Loan Rates 2026 (NerdWallet)

- SBA Loan Interest Rates for 2026 (Fundwell)

- CDFI Loans: What They Are (NerdWallet)

- OnDeck Business Loans Review (NerdWallet)

- Kiva Business Loans Review (Bankrate)

- Startup Business Loans With No Revenue (LendingTree)

- CDFIs: A Funding Guide for Small Businesses (Hello Alice)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Startup Business Loans

2 comments

Miguel

July 23, 2026

can you actually get a business loan for a startup that has no revenue yet

Richard MooreStartupOwl team

Senior Finance & Banking Editor · July 25, 2026

Yes, but your choices narrow. A few programs look at your plan instead of your sales history. Kiva offers 0% interest loans up to $15,000 with no revenue requirement. SBA microloans, up to $50,000 at roughly 8 to 13 percent, weigh your business plan and character more than past revenue. Equipment financing can also work because the equipment itself is the collateral. What you usually will not get with zero revenue is a big bank term loan. Start with the plan based options and build from there.

Leave a comment