How to Build Business Credit Fast: Step-by-Step Guide for New and Existing Businesses

Build business credit in 3-6 months with net-30 vendor accounts, business credit cards, and a D-U-N-S number. Step-by-step guide with score ranges and costs.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- Why Building Business Credit Is the Smartest Free Move You Can Make

- What Business Credit Is and Why It Matters

- What You Need Before You Start Building Business Credit

- Step-by-Step Process to Build Business Credit

- How Much It Actually Costs to Build Business Credit

- What SBA Looks At Now Instead of a Credit Score

- Best Tools and Accounts for Building Business Credit

- What to Do If You Cannot Build Business Credit Yet

- 5 Mistakes That Can Wreck Your Business Credit

- FAQ

$0–$500

Est. Loan Cost

6 minutes

Timeline

7

Total Steps

Why Building Business Credit Is the Smartest Free Move You Can Make

Business credit decides your price. It can be the difference between a 7% APR term loan and a 25%+ APR merchant cash advance. Most owners skip the step and pay thousands more in interest. You can start in 3 to 6 months for close to nothing.

Business credit is separate from personal credit. Three bureaus track it, Dun and Bradstreet, Experian Business, and Equifax Business. Each uses its own model, running 0-100 or 101-992 depending on the bureau. You do not need perfect personal credit or real revenue to start.

This guide gives you every step, score range, vendor name, and dollar figure. It takes you from zero. If you are shopping funding too, our how to get a business loan guide shows how scores move your approval odds.

What Business Credit Is and Why It Matters

Business credit measures your company's creditworthiness. It is separate from your personal FICO score. When a lender or vendor sizes you up, they pull your business credit report. It shows how reliably you pay, how much debt you carry, and whether you have liens or judgments.

Each bureau scores differently. Dun and Bradstreet's PAYDEX runs 1 to 100, and 80+ means you pay on time. Experian's Intelliscore Plus runs 1 to 100, and 76+ is low risk. Equifax's Credit Risk Score runs 101 to 992. The FICO SBSS runs 0 to 300 and used to gate SBA loans. SBA retired that requirement for 7(a) small loans on March 1, 2026, though some lenders still pull it.

Strong business credit buys better loan rates, higher vendor lines, and lower insurance premiums. It also drops the personal guarantee. A brand new business might get $5,000 in trade credit. The same company a year later can reach $50,000 or more.

Your Personal Credit Score Is Not Your Business Credit Score

Personal credit runs 300-850 under FICO or VantageScore. Business credit uses bureau models instead. Anyone can pay to pull your business report without asking you. There are fewer consumer protections than on a personal report, which is why monitoring matters. Your personal score still counts. The FICO SBSS blends personal and business data into one number. SBA stopped requiring it on 7(a) loans of $350,000 and under in March 2026, but plenty of lenders still run it.

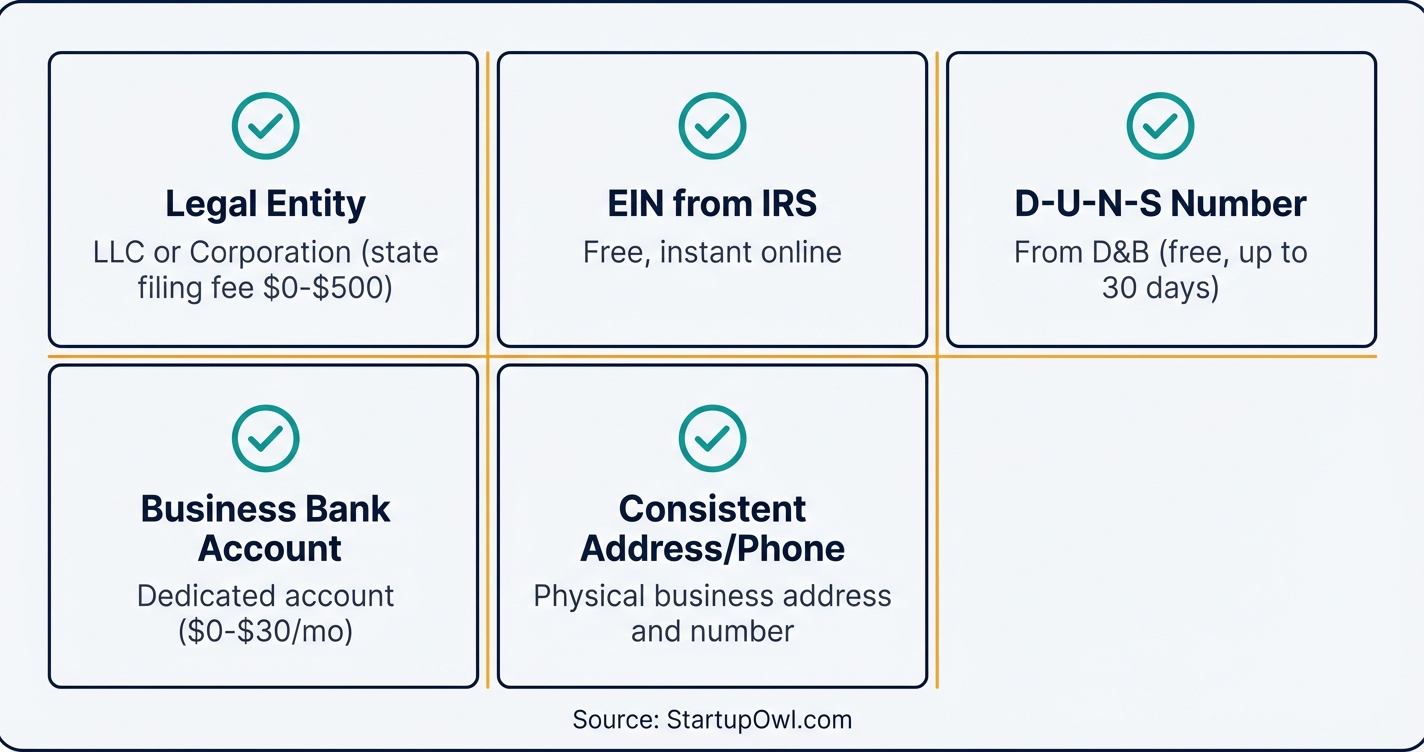

What You Need Before You Start Building Business Credit

Revenue, staff, and a clean personal score can all wait. You need five things first.

- Legal business entity (LLC or corporation preferred). Some vendors and lenders will not work with sole proprietorships.

- Employer Identification Number (EIN) from the IRS. Free and instant online.

- D-U-N-S Number from Dun and Bradstreet. Free, and it takes up to 30 business days.

- Business bank account in your company's legal name.

- Business address and phone number, listed the same way everywhere.

Have no entity yet? Start with LLC formation and work the steps in order. The whole foundation, entity plus EIN plus D-U-N-S plus bank account, takes 30 to 45 days if you plan ahead.

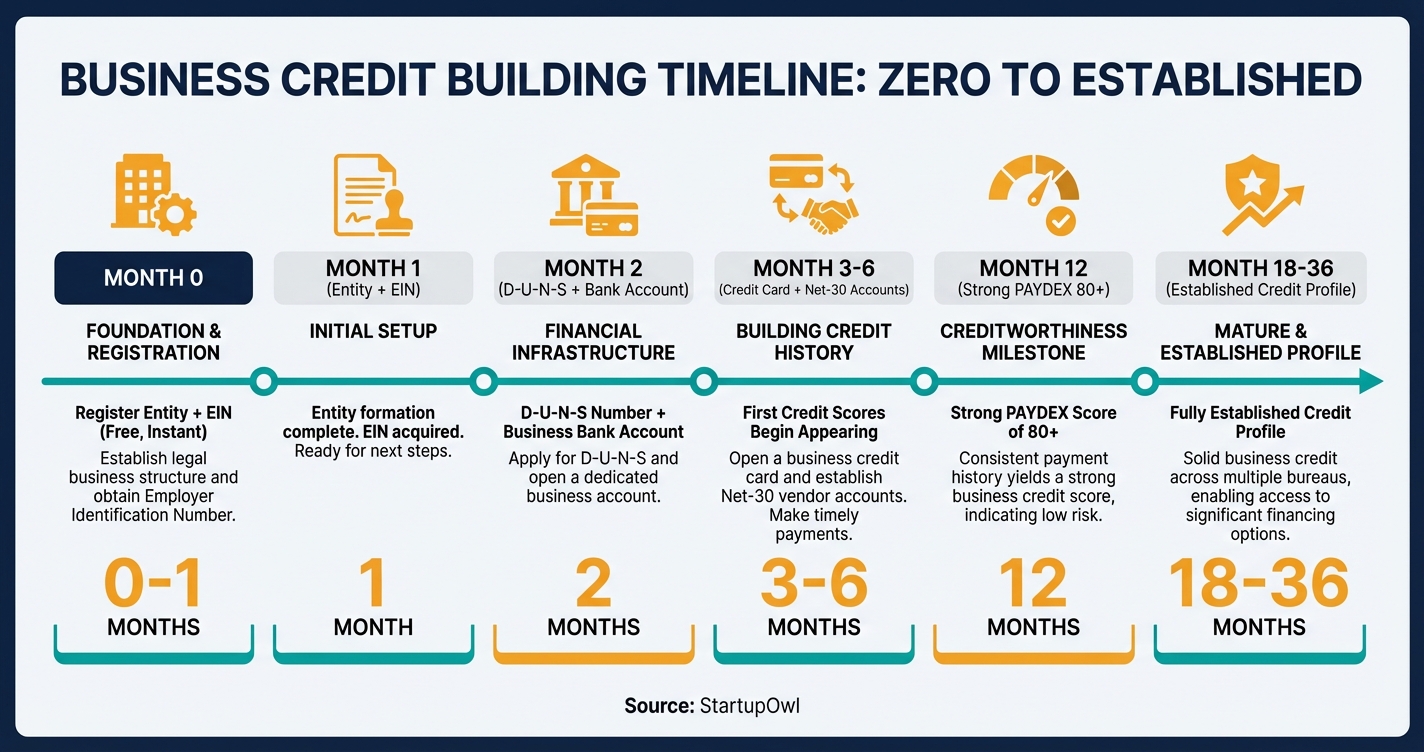

Step-by-Step Process to Build Business Credit

The order below is the one credit-building professionals use. Each step rests on the one before it. Do not skip ahead. Steps 1-4 fit in your first two weeks, steps 5-7 in your first 90 days.

The step cards above carry the costs, timelines, and links. One thing matters more than all of it. Pay on time or early. Payment history is the biggest single factor in every business credit model.

PAYDEX rewards early payment, not just punctual payment. A score of 80 means you pay on time. Above 80 means you pay early. Aim for 80+ in your first year.

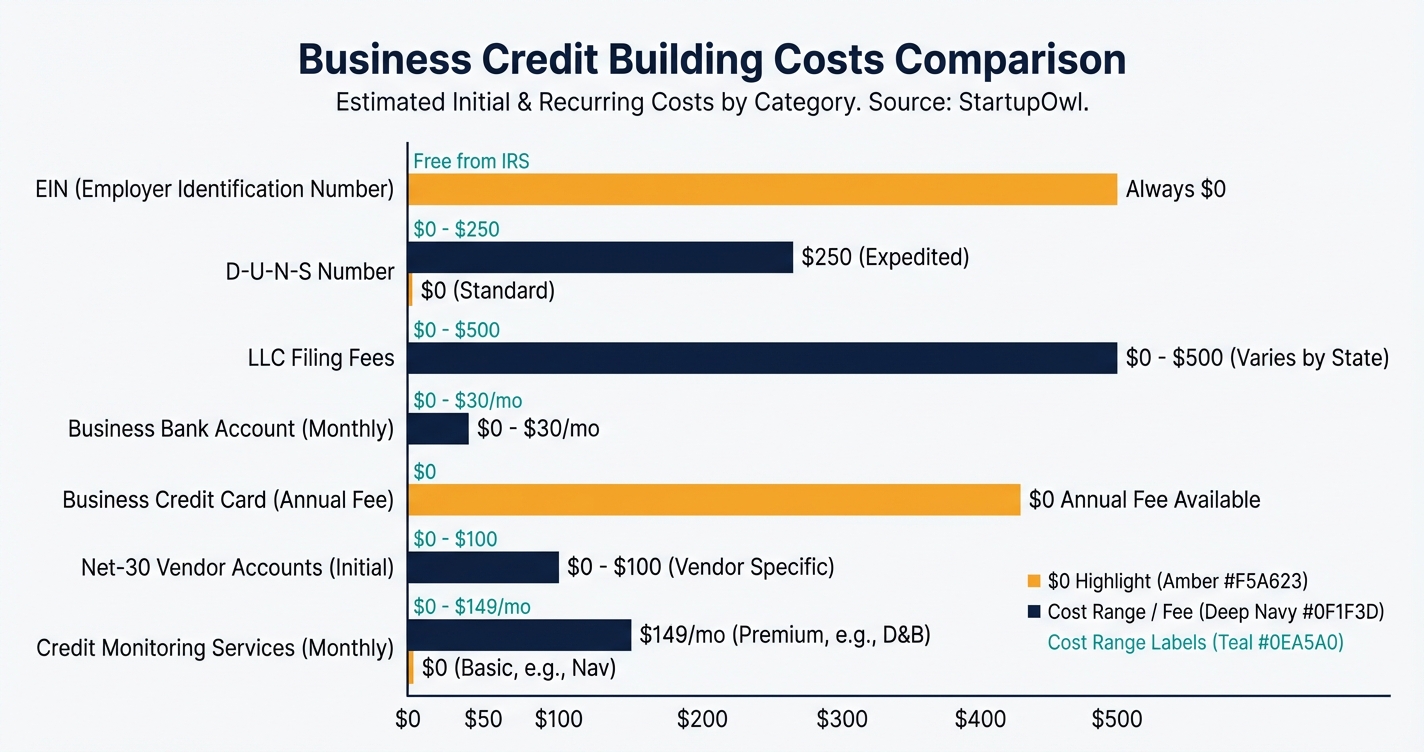

How Much It Actually Costs to Build Business Credit

This is cheap. Setting up your credit foundation runs $0 to $500, depending on your state's LLC fee and whether you expedite the D-U-N-S Number. Ongoing costs stay near zero if you pick no-fee cards and free monitoring.

The real cost is time. You need 6 to 12 months of on-time payments across several reporting accounts before a solid profile appears. A strong PAYDEX usually lands at 12 to 18 months. For the established credit that wins the best SBA terms, plan on 18 to 36 months.

Paid monitoring runs $39.95 for a single Experian report up to $149 per month for D&B CreditBuilder Plus. Nav.com is free. It shows summary grades from several bureaus.

Business Credit Score Ranges by Bureau (as of 2026)

| Type / Provider | Rate | Notes |

|---|---|---|

| D&B PAYDEX Score | 1-100 | 80+ is considered good (on-time payments); above 80 signals early payments |

| Experian Intelliscore Plus | 1-100 | 76+ is low risk; average business score is 62 |

| Equifax Credit Risk Score | 101-992 | Higher is better; predicts likelihood of 90+ day delinquency |

| Equifax Payment Index | 1-100 | 90+ indicates all creditors paid on time |

| FICO SBSS (SBA loans) | 0-300 | SBA dropped this requirement on March 1, 2026, some lenders still use the score privately |

What SBA Looks At Now Instead of a Credit Score

SBA used to screen 7(a) small loans, meaning loans of $350,000 and under, with one FICO SBSS score. That ended on March 1, 2026 under SBA Procedural Notice 5000-876777. The gate did not disappear. It moved to your lender.

Your lender now has to show reasonable assurance you can repay. That means a look at your credit history and your guarantors', your two most recent months of business bank statements, and a debt service coverage ratio of at least 1.1 to 1. Lenders may use their own scoring models. They cannot lean on consumer credit scores alone, and they do not have to score you at all.

What changes for you is simple. Cash flow outweighs any single number now. Keep clean bank statements, stay current on the debt you already carry, and be ready to say what the money is for. SBA Express loans are not affected.

Best Tools and Accounts for Building Business Credit

The right mix of cards and vendor accounts builds your profile faster. Here are the 2026 picks.

Business Credit Cards That Report to Bureaus

- Chase Ink Business Unlimited. 0% intro APR for 12 months on purchases, then 16.74%-24.74% variable, $0 annual fee, and a $750 bonus after $6,000 of spend in 3 months.

- American Express Blue Business Plus. 0% intro APR for 12 months, then 16.74%-26.74% variable, $0 annual fee. It reports to business bureaus.

- Brex. No personal guarantee, no credit check. It judges revenue and cash on hand instead, so it suits startups holding $50,000+ in the bank.

- Ramp. Also no personal guarantee. It reports to the major business bureaus and gives you unlimited cards with live expense tracking.

Net-30 Vendors That Report to Credit Bureaus

- Uline (shipping and packaging supplies) reports to Dun and Bradstreet.

- Quill (office supplies) reports to D&B. The net-30 account costs $99.99 a year.

- Grainger (industrial supplies) reports to D&B, Experian, and Equifax. No personal credit check on the application.

- Crown Office Supplies reports to all three major bureaus. A small membership fee applies.

For more routes, see our guides on business lines of credit and business loans for startups.

What to Do If You Cannot Build Business Credit Yet

Business under 30 days old? Sole proprietor with no LLC yet? You still have ways to build creditworthiness and reach capital.

- Secured business credit cards take a deposit of $500 to $5,000. That deposit becomes your limit. Use it well for 6 to 12 months and many issuers move you to an unsecured card.

- Personal cards used for business build no business credit. They keep cash moving. Switch to a business card once your EIN is live.

- Invoice factoring turns unpaid invoices into cash now. There is no credit score test, the factor checks your customers instead.

- Small business grants are free capital. No repayment, no credit check.

- Microloans from nonprofit lenders may take personal scores as low as 500-620.

Is your personal score below 620? Work on it while you build business credit. SBA lenders now read your credit history directly instead of leaning on one blended score.

5 Mistakes That Can Wreck Your Business Credit

1. Missing even one payment. One late payment can drop your PAYDEX from 80 to below 50. That moves you from low risk to high risk overnight. Set up autopay on every account.

2. Not separating personal and business finances. Expenses on personal accounts build nothing for your business file. Open a business bank account and card on day one.

3. Choosing vendors that do not report. If your supplier skips D&B, Experian, and Equifax, your payment history is invisible. Ask before you open a trade account.

4. Letting utilization climb above 30%. High utilization reads as financial stress at both business and personal bureaus. On a $10,000 limit, stay under $3,000 even when cash flow allows more.

5. Ignoring your credit reports. Errors are common, and anyone can view these reports. An uncorrected mistake costs you rate or gets you denied. Check all three bureaus every 90 days.

How to Accelerate Your Credit-Building Timeline

Run these in parallel, not in sequence. Open 3-5 reporting trade accounts in your first 60 days. Apply for a card that reports to bureaus. Pay every invoice early rather than merely on time, because early payment lifts PAYDEX above 80 faster. Ask for limit increases after 6 months of clean history, which drops your utilization without changing what you spend.

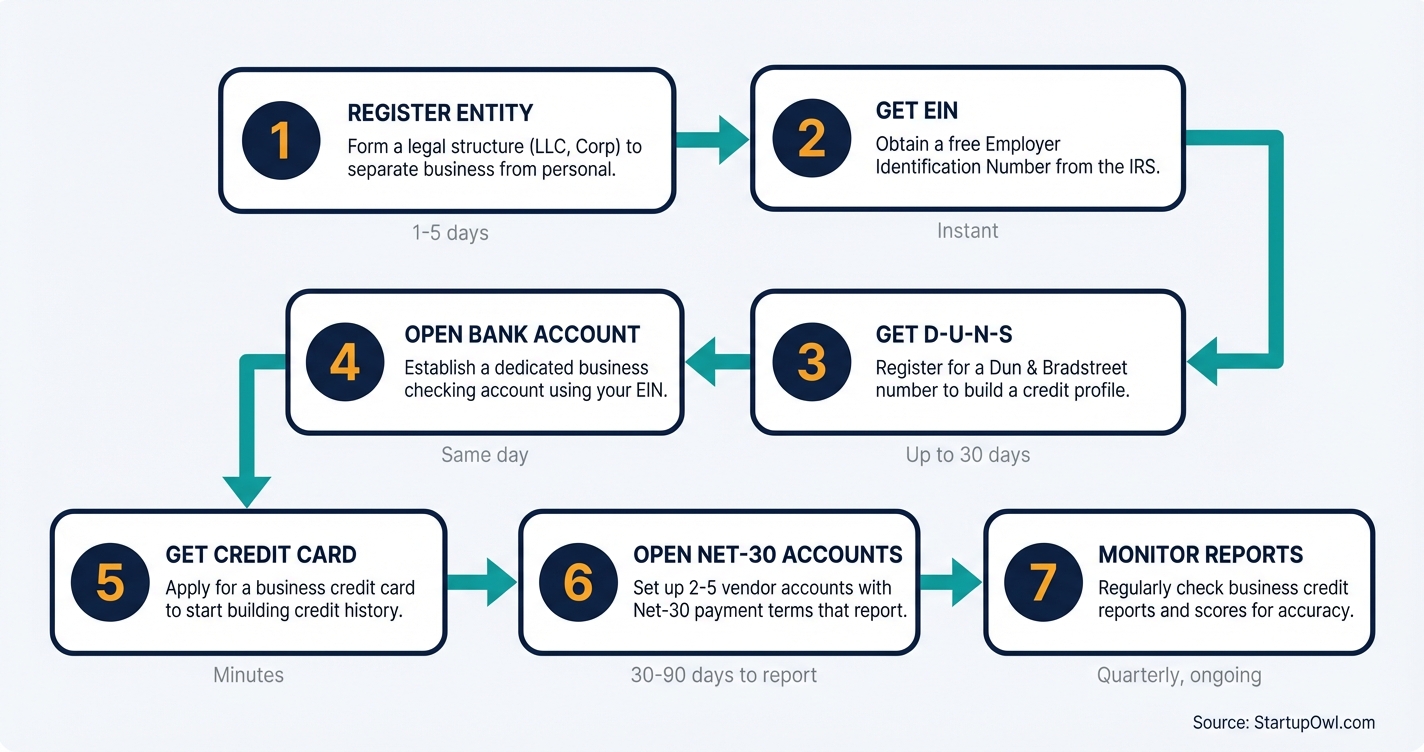

Step-by-Step Process

- 1

Register your business as a legal entity

File as an LLC or corporation with your state's Secretary of State. This creates a legal separation between you and your business, which is critical because some lenders and vendors will not extend credit to sole proprietorships. You can form your entity through an LLC formation service for as little as $0 plus state filing fees.

$0 to $500 (state filing fees vary) 1-5 business days (online filing) to 4 weeks (mail filing) SBA.govTips

- Choose an LLC or corporation rather than a sole proprietorship to maximize credit-building potential.

- Get a dedicated business phone number and list it with directory assistance to help bureaus verify your business.

Common Mistakes

- Operating as an unregistered sole proprietorship, which limits vendor credit approvals and prevents building a separate business credit file.

- 2

Get your free EIN from the IRS

Apply for an Employer Identification Number (EIN) directly on IRS.gov and receive it instantly at no cost. Your EIN functions as a Social Security number for your business and is required to open a business bank account, apply for credit cards, and file taxes. Never pay a third-party service for an EIN.

Tips

- Complete the online application in a single session as it expires after 15 minutes of inactivity.

- Print and save your EIN confirmation letter immediately for your records.

Common Mistakes

- Paying a third-party site $50 to $150 for an EIN that is completely free from the IRS.

- Using your personal SSN for business accounts instead of an EIN, which tangles personal and business credit.

- 3

Request a free D-U-N-S Number from Dun and Bradstreet

Your D-U-N-S Number is a unique nine-digit identifier that creates your credit file with Dun and Bradstreet, the largest business credit bureau. Apply for free at dnb.com. The free process typically takes up to 30 business days, or you can pay for expedited processing to get it in 8 business days.

$0 (free) or approximately $250 for expedited 5-8 day processing Up to 30 business days (free) or 8 business days (expedited) dnb.comTips

- Check whether your business already has a D-U-N-S Number using D&B's free lookup tool before applying.

- Request removal from D&B's marketing list during your application to reduce unsolicited calls.

Common Mistakes

- Waiting until you need a loan to apply for a D-U-N-S Number, which delays your credit-building timeline by a month or more.

- 4

Open a dedicated business bank account

Use your EIN to open a business checking account at your preferred bank or credit union. This creates a clear financial trail separating personal and business income, which lenders and bureaus look for. Some banks like Bank of America provide free access to your Dun and Bradstreet credit scores through their Business Advantage 360 platform. Set up your business accounting at the same time.

$0 to $30 per month depending on the bank Same day (in person) or 1-3 business days (online) SBA.govTips

- Choose a bank that offers free business credit monitoring as an account perk.

- Route all business income and expenses through this account from day one to establish a clear financial trail.

Common Mistakes

- Using a personal checking account for business transactions, which makes it nearly impossible to separate business and personal credit.

- 5

Apply for a business credit card that reports to bureaus

A business credit card is one of the fastest ways to start building credit history. The Chase Ink Business Unlimited offers 0% intro APR for 12 months on purchases (then 16.74%-24.74% variable), no annual fee, and reports to business credit bureaus as of 2026. If your personal credit is limited, a secured business credit card (with a $500 to $5,000 deposit) can get you started. See our best business credit cards guide for full comparisons.

$0 annual fee (unsecured) or $500-$5,000 deposit (secured card) Approval in minutes; card arrives in 7-10 business days nerdwallet.comTips

- Pay your statement balance in full every month to avoid interest and demonstrate responsible usage.

- Keep your credit utilization below 30% of your limit to protect your score.

Common Mistakes

- Carrying a high balance that pushes utilization above 30%, which signals financial stress to credit bureaus.

- Choosing a card that does not report to business credit bureaus, gaining you zero credit-building value.

- 6

Open 2-5 net-30 vendor accounts that report to credit bureaus

Net-30 accounts let you buy supplies now and pay within 30 days, and when the vendor reports your on-time payments to credit bureaus, you build tradelines. Top vendors that report to Dun and Bradstreet, Experian, and Equifax include Uline (shipping supplies), Quill (office supplies), Grainger (industrial supplies), and Crown Office Supplies. Aim for at least 2-3 reporting accounts within your first 90 days. It typically takes 1-3 billing cycles (30-90 days) for a new account to appear on your credit report.

$0 to $100 (some vendors charge a small annual or membership fee) 1-3 billing cycles (30-90 days) for payments to appear on reports NavTips

- Confirm each vendor reports to at least one major business credit bureau before opening an account.

- Pay invoices early (not just on time) to boost your D&B PAYDEX score above 80.

Common Mistakes

- Opening accounts with vendors that do not report to any credit bureau, which wastes your credit-building effort entirely.

- 7

Monitor your business credit reports every quarter

Check your reports with all three major business credit bureaus (Dun and Bradstreet, Experian Business, and Equifax Business) at least every 90 days. You can use Nav.com for free summary reports from multiple bureaus, or pay for detailed reports directly. D&B's free Credit Insights plan shows your PAYDEX, delinquency, and failure scores. An Experian single report costs $39.95, while D&B's paid monitoring starts at $49 per month as of 2026. Learn more about reading your reports in our business credit score guide.

$0 (free summaries) to $49-$149 per month (paid monitoring) Ongoing (review quarterly at minimum) NavTips

- Dispute errors directly with the reporting bureau and provide supporting documentation to speed resolution.

- Set calendar reminders for quarterly reviews so errors do not go unnoticed for months.

Common Mistakes

- Never checking reports, which allows errors or fraudulent accounts to drag down your score undetected.

- Assuming your personal credit score and business credit score are the same thing.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| LLC or Corporation Filing | $0 to $500 | State filing fees vary; some LLC services charge $0 plus state fee |

| EIN (Employer Identification Number) | $0 | Always free from the IRS; never pay a third party |

| D-U-N-S Number | $0 to $250 | Free standard processing (30 days) or ~$250 for expedited (5-8 days) |

| Business Bank Account | $0 to $30 per month | Many banks offer free business checking with minimum balance |

| Business Credit Card | $0 to $375 annual fee | Many no-fee cards available; secured cards require $500-$5,000 deposit |

| Net-30 Vendor Accounts | $0 to $100 per vendor | Some vendors charge membership fees; most have no cost to open |

| Credit Monitoring (optional) | $0 to $149 per month | Free summaries via Nav; paid D&B plans from $49/mo, Experian from $39.95 one-time |

Frequently Asked Questions

You can establish a basic credit profile in 3 to 6 months with 2-3 reporting accounts and on-time payments. Building a strong profile (PAYDEX 80+) typically takes 12 to 18 months. Excellent, well-established credit that qualifies you for top-tier financing generally requires 18 to 36 months of consistent credit management.

Yes, but options are more limited when your business is brand new. Cards from Brex and Ramp require no personal guarantee and no personal credit check. Most traditional business credit cards, however, will check your personal credit during the application. Once your business credit is established with multiple reporting tradelines, you gain more opportunities to secure financing based solely on your company's track record.

On D&B PAYDEX (1-100), 80 or higher is good. On Experian Intelliscore Plus, 76+ is low risk. The FICO SBSS is different now. SBA retired its minimum for 7(a) small loans on March 1, 2026, so lenders that still use the score set their own bar.

The foundation costs $0 to $500 total. Your EIN is free. Your D-U-N-S Number is free (or about $250 to expedite). State LLC filing fees range from $0 to $500. Many business credit cards have no annual fee, and most net-30 vendor accounts cost $0 to $100 to open. Optional credit monitoring runs $0 to $149 per month.

Yes, but only if the vendor reports your payment history to at least one major business credit bureau (Dun and Bradstreet, Experian, or Equifax). Vendors like Uline, Grainger, Quill, and Crown Office Supplies are known to report. New tradelines typically appear on your credit report within 1-3 billing cycles (30-90 days) after your first payment.

A D-U-N-S Number is a unique nine-digit identifier that Dun and Bradstreet assigns to your business. You need one to generate a PAYDEX score, which is one of the most widely checked business credit scores. It is free to apply at dnb.com and takes up to 30 business days to receive.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA Procedural Notice 5000-876777, Sunset of SBSS Score

- Establish Business Credit - U.S. Small Business Administration

- Get an Employer Identification Number (EIN) - IRS.gov

- Claim Your Free D-U-N-S Number - Dun and Bradstreet

- Business Credit Score Ranges - Capital One

- How Long Does It Take to Build Business Credit - OnDeck

- FICO SBSS Score Explained - Nav.com

- 7(a) Loan Program - SBA.gov

- Net-30 Vendors That Report to Credit Bureaus - altLINE

- What Is a Good Business Credit Score - OnDeck

- How to Build Business Credit - Chase for Business

- The 3 Major Business Credit Bureaus - Ramp

- Best Business Credit Cards of March 2026 - NerdWallet

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about How to Build Business Credit Fast

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment