Minority Business Resources

Minority-owned businesses now represent 22.6% of U.S. employer firms. Find SBA programs, NMSDC certification, grants, and free tools to start and grow yours.

In This Article

- Key Takeaways

- Step-by-Step

- Why Minority Business Resources Matter Right Now

- How to Access Minority Business Resources Step by Step

- The Three Certifications You Should Evaluate

- Funding Programs for Minority-Owned Businesses

- Free Government Resources You Should Use This Week

- Recommended Tools for Minority Business Owners

- Five Mistakes That Cost Minority Business Owners Time and Money

- What to Do This Week

- FAQ

StartupOwl may earn a commission when you use links on this page to sign up for business tools or services. This does not affect our editorial recommendations. We only recommend products we have researched or used. Read our full disclosure policy for details.

Minority-owned businesses represented 22.6% of the 5.9 million U.S. employer firms as of 2022, according to the Census Bureau's Annual Business Survey. Black-owned employer businesses alone generated $211.8 billion in annual receipts that year and employed 1.6 million people.

Despite that growth, minority-owned businesses account for only 6.1% of small business revenue while representing 11.4% of all small businesses, per Census Bureau data. This page breaks down every program, certification, and tool that can help you close that gap.

Why Minority Business Resources Matter Right Now

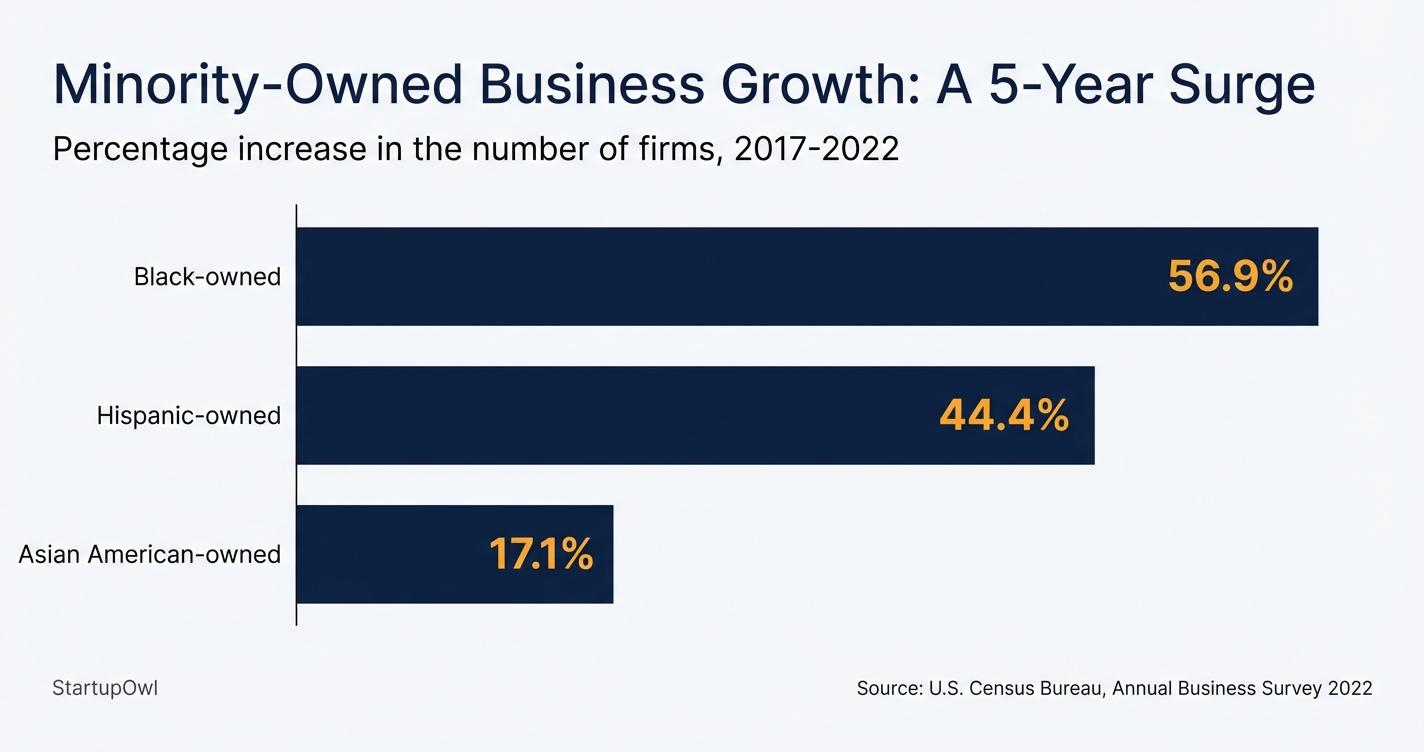

Black-owned businesses experienced a 56.9% increase in the number of employer firms between 2017 and 2022, accounting for more than half of all new business growth during that period, per the Census Bureau. Approximately 70,000 new Black-owned employer businesses were created in those five years.

Hispanic-owned businesses grew at 44.4% during the same timeframe, and Asian American-owned businesses grew at 17.1%. Black-owned firms' gross revenue jumped 66%, from $127.9 billion in 2017 to $211.8 billion in 2022.

Yet significant gaps persist. Hispanic entrepreneurs represent 7.9% of employer business owners compared to 18.7% of the U.S. population. Non-minority male-owned businesses still account for 58.6% of all small businesses and 76.0% of small business revenue. The resources below help you access capital, contracts, and mentoring designed to narrow these disparities.

How to Access Minority Business Resources Step by Step

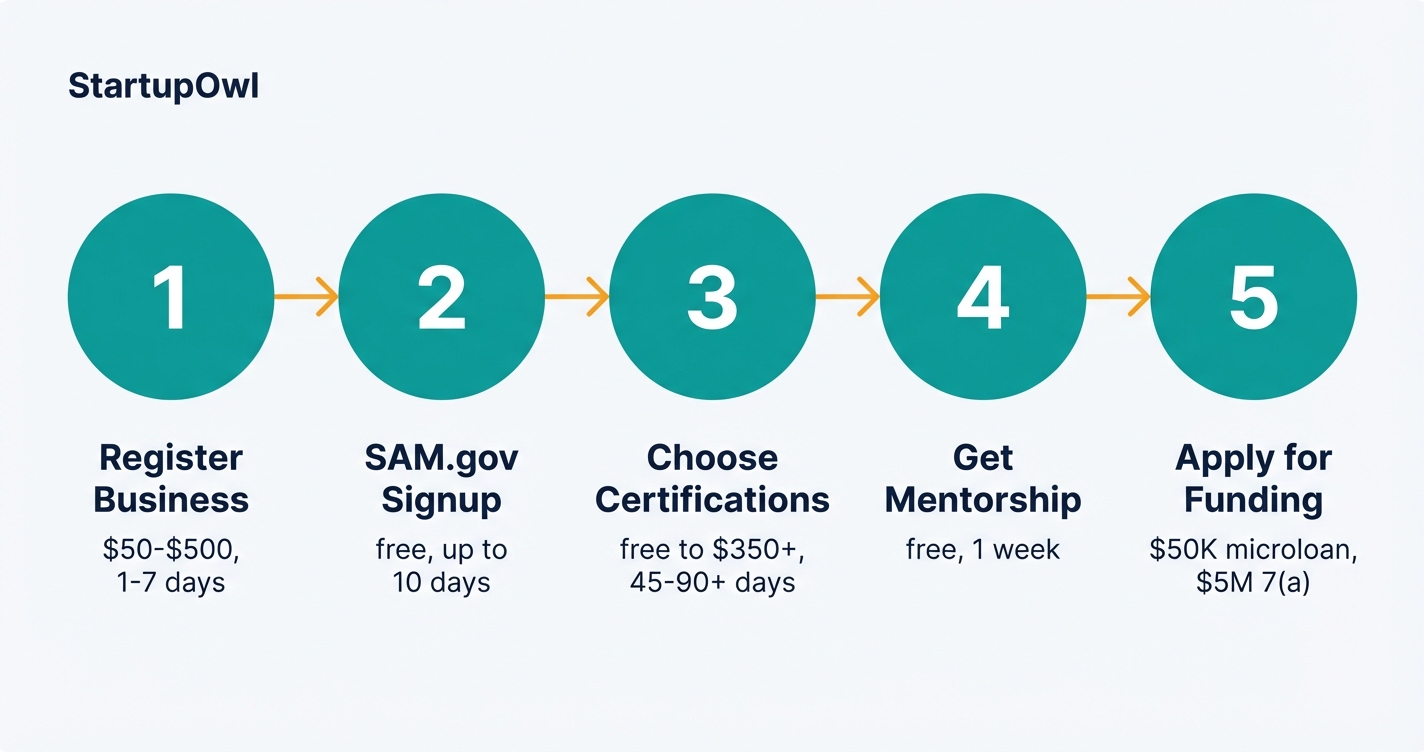

Getting started does not require any paid consultant. Every SBA certification is free to apply for, and the best mentoring programs cost nothing. Below is the sequence that keeps you moving without wasting time.

First, form an LLC or corporation. Most certifications require a formal legal entity, and an LLC protects your personal assets from business liabilities. If you are weighing your options, our guide to sole proprietorship vs LLC explains the tax and liability differences.

Second, register at SAM.gov for free. This is required for federal contracting programs including 8(a) and HUBZone. Do not pay anyone to do this for you.

Third, open a business bank account the same week you receive your EIN. Separating personal and business finances is essential for any future certification or loan application.

Fourth, schedule a free SCORE mentorship session. SCORE's 10,000+ volunteer mentors provide confidential, one-on-one business advice at no cost. According to SCORE data, 87% of mentored entrepreneurs are still in business after one year.

Fifth, evaluate whether you qualify for 8(a), HUBZone, or NMSDC MBE certification (details in the sections below). You can hold multiple certifications at the same time.

If you are concerned about common first-time founder mistakes, work through these steps in order and consult a CPA before making tax elections.

The Three Certifications You Should Evaluate

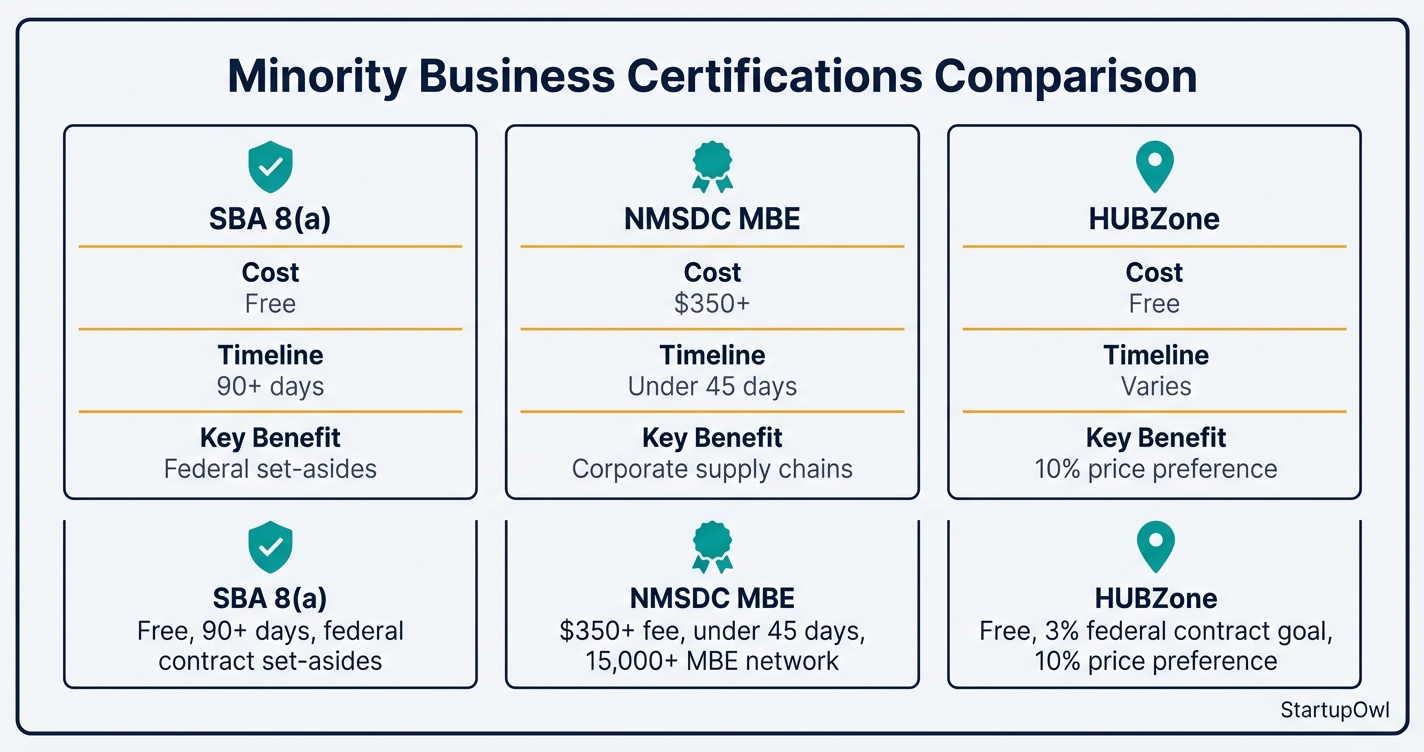

The SBA 8(a) Business Development program is a nine-year program that limits competition on certain federal contracts to participating businesses. As of January 2026, the SBA requires a race-neutral, fact-specific showing of social disadvantage for 8(a) eligibility. The agency admitted only 65 new firms in 2026 under heightened scrutiny. Apply at certifications.sba.gov at no cost.

The NMSDC MBE certification requires that your business be at least 51% owned, operated, and controlled by one or more U.S. citizens who are Asian-Indian, Asian-Pacific, Black, Hispanic, or Native American. NMSDC connects certified firms to over 15,000 MBEs and 1,750+ corporate members through 23 regional councils. Processing fees start at $350, and typical review takes under 45 days. Apply at nmsdc.org.

The HUBZone program targets businesses in economically distressed areas with a federal goal of awarding at least 3% of contract dollars to HUBZone-certified companies each year. In FY2024, HUBZone awards totaled approximately $17.6 billion (2.75% of prime contracts). Your principal office must be in a HUBZone, and at least 35% of your employees must reside in one. Check the SBA HUBZone map for eligibility.

Funding Programs for Minority-Owned Businesses

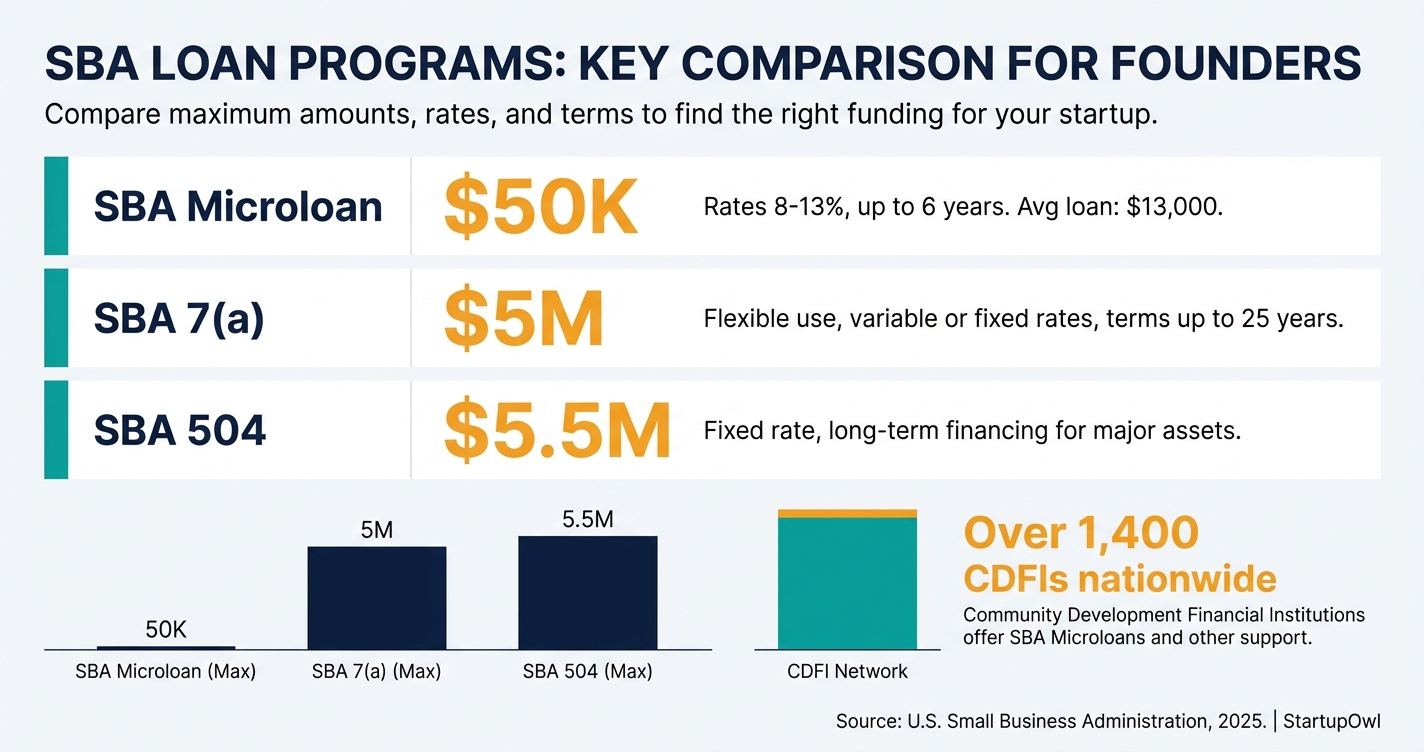

The SBA Microloan program provides loans up to $50,000 through nonprofit intermediary lenders, with the average loan at approximately $13,000, per the SBA. Interest rates typically fall between 8% and 13%, and repayment terms can extend up to six years. These loans are specifically designed for startups and underserved businesses. Find an intermediary lender at sba.gov/microloans.

The SBA 7(a) loan program is the most common SBA loan, offering up to $5 million for working capital, equipment, and expansion. While not specifically for minority-owned businesses, it is a primary funding tool for small businesses of all backgrounds.

Community Development Financial Institutions (CDFIs) specialize in serving underserved communities. There are over 1,400 certified CDFIs in the U.S., including banks, credit unions, and loan funds, per the U.S. Treasury. Many offer more flexible eligibility than traditional banks.

For grants, the federal government does not provide startup grants directly. However, Grants.gov lists over 1,000 federal grant opportunities, some of which target underserved communities. The NMSDC Business Consortium Fund provides working capital loans and grant funding to certified MBEs. Explore our full list of minority business grants and startup funding options.

Free Government Resources You Should Use This Week

SCORE operates over 250 chapters and has helped more than 17 million entrepreneurs since 1964, according to SCORE. SCORE clients created 143,623 jobs in FY2024 and returned $45.42 to the U.S. Treasury for every dollar allocated to the program. Request a mentor at score.org/find-mentor.

Small Business Development Centers (SBDCs) provide free consulting and low-cost training through a network of more than 900 service locations in every state and territory, according to the SBA. SBDCs make special efforts to reach minority members of socially and economically disadvantaged groups. SBDCs counseled and trained over 250,000 clients in a recent reporting year.

The Minority Business Development Agency (MBDA) is the only federal agency dedicated to the growth and global competitiveness of minority business enterprises. In FY2023, MBDA facilitated access to $1.5 billion in capital and helped create or maintain 19,000 jobs. However, note that in March 2026, an executive order directed eliminating MBDA to the maximum extent consistent with law. Check mbda.gov for the latest program availability.

The SBA T.H.R.I.V.E. Emerging Leaders Reimagined program provides intensive executive-level training for high-potential small businesses. Participants create a three-year strategic growth action plan with benchmarks and performance targets. Check sba.gov/minority-owned-businesses for current enrollment.

Recommended Tools for Minority Business Owners

You need the same core tools as any founder, but some services are especially relevant when you are building financial records for certification applications and loan packages.

- Use accounting software from day one. QuickBooks Online starts at $35/month and Wave is free. Clean financial records are required for 8(a) recertification and NMSDC applications.

- File your LLC through a trusted formation service. ZenBusiness starts at $0 plus state fees, and Northwest Registered Agent starts at $39 plus state fees.

- Use online legal services for contracts, operating agreements, and trademark filings. LegalZoom and Rocket Lawyer both offer plans under $40/month.

- For ongoing marketing, build your small business marketing plan and invest in local SEO to reach customers in your community. Both are free to start.

If you are exploring business concepts, review our list of solopreneur business ideas or read the solopreneur guide for lean startup strategies.

Five Mistakes That Cost Minority Business Owners Time and Money

1. Assuming the SBA gives startup grants. The SBA does not provide grants to start or expand a business. Programs like the EIDL Advance during COVID-19 were one-time emergency measures. If someone promises you an SBA startup grant, they are misinformed or running a scam.

2. Paying for SAM.gov registration. SAM registration is free. Scam companies charge hundreds of dollars for a service the government provides at no cost. The only legitimate SBA phone number for certifications is 1-866-443-4110.

3. Relying on a single certification. You can hold 8(a), HUBZone, NMSDC MBE, and state-level certifications simultaneously. Each opens different doors to different types of contracts and corporate supply chains.

4. Mixing personal and business finances. Every certification and loan application requires clean financial records. Open a separate business bank account before your first transaction.

5. Skipping free mentorship. SCORE and SBDCs exist specifically to help you avoid costly mistakes. These programs are funded by the federal government and cost you nothing. Not using them puts you at a disadvantage compared to founders who do.

What to Do This Week

Start by forming your legal entity. Register your business with your state, get your EIN from the IRS, and open a business bank account. These three actions take less than a day and unlock access to every program on this page.

Next, schedule a free SCORE session at score.org and visit americassbdc.org to find your local SBDC. Then review our guides to small business grants and small business loans for a full picture of your funding options.

If you are a woman, veteran, or immigrant as well as a minority founder, explore our female founders guide, veteran entrepreneur resources, and immigrant entrepreneur guide for additional identity-specific programs.

Step-by-Step Process

- 1

Register your business legally

Before you apply for any minority business certification or program, you need a legally registered entity. An LLC or corporation is required for most certifications, though sole proprietors can qualify for some grant programs.

Visit your state's Secretary of State website to file, or use an LLC formation service to handle the paperwork for you.

Tips

- Get your EIN from the IRS immediately after forming your entity.

- Open a business bank account on the same day you receive your EIN.

Common Mistakes

- Skipping the EIN step and mixing personal and business finances.

- Choosing sole proprietorship when you plan to seek government contracts or certifications.

- 2

Get your SAM.gov registration completed

Every business that wants to pursue federal contracts or SBA certifications must register in the System for Award Management (SAM.gov). Registration is free and takes about 30 minutes, but activation can take up to 10 business days.

SAM registration is a prerequisite for the 8(a) program, HUBZone certification, and most federal grant applications. Do not pay a third party for SAM registration.

Tips

- Have your EIN, DUNS number (now UEI), and bank account info ready before starting.

- Set a calendar reminder to update your SAM registration annually.

Common Mistakes

- Paying a third-party service for SAM registration when it costs nothing.

- Letting your SAM registration lapse and losing eligibility for contracts.

- 3

Evaluate your certification options

The two primary certifications for minority-owned businesses are the SBA 8(a) Business Development program and the NMSDC MBE certification. The 8(a) program is a nine-year federal contracting program for socially and economically disadvantaged business owners. NMSDC certification connects you to over 1,750 corporate members seeking diverse suppliers.

If your business is in a distressed area, check the SBA HUBZone map to see whether you qualify for HUBZone certification as well.

SBA certifications are free; NMSDC fees start at $350 processing plus annual fees based on revenue 8(a) approval takes 90 days or longer; NMSDC certification typically under 45 days SBA.govTips

- You can hold multiple certifications simultaneously (8(a), HUBZone, NMSDC MBE).

- The 8(a) program now requires a fact-specific showing of social disadvantage, not a race-based presumption.

Common Mistakes

- Assuming the 8(a) program still uses race-based presumptions for eligibility.

- Starting the NMSDC application without gathering three years of tax returns and financial documents.

- 4

Connect with free mentorship and counseling

SCORE provides free business mentoring through its network of over 10,000 volunteer mentors at more than 250 chapters nationwide. According to SCORE, 87% of entrepreneurs with a mentor are still in business after one year.

Small Business Development Centers (SBDCs) operate more than 900 service locations across every state and territory, providing free consulting and low-cost training.

Tips

- Request a SCORE mentor who has experience in your specific industry.

- SBDCs make special efforts to reach minority and socially disadvantaged business owners.

Common Mistakes

- Waiting until you have a crisis to seek mentorship instead of building the relationship early.

- Not following up after your first SCORE session to schedule a recurring cadence.

- 5

Apply for funding through SBA loans and grants

The SBA Microloan program provides loans up to $50,000 through nonprofit intermediary lenders, with the average microloan at approximately $13,000. Interest rates typically range from 8% to 13%, and repayment terms can extend up to six years.

The SBA 7(a) loan program offers up to $5 million for qualified businesses. For grant opportunities, search Grants.gov, which lists over 1,000 federal grants. You can also explore minority business grants for programs specific to your background.

Loan application is free; interest rates vary by program SBA Microloans can fund in 30 to 60 days; 7(a) loans take 60 to 90 days SBA.govTips

- Community Development Financial Institutions (CDFIs) have more flexible eligibility than traditional banks.

- Prepare a solid business plan before applying for any SBA loan.

Common Mistakes

- Confusing SBA disaster loans and COVID-era programs with current grant availability.

- Applying to only one lender instead of comparing terms across multiple SBA-approved intermediaries.

Frequently Asked Questions

A minority-owned business is typically one that is at least 51% owned, operated, and controlled by one or more individuals who identify as Black, Hispanic, Asian American, Asian-Indian, Native American, or Pacific Islander. The owner must be a U.S. citizen for most federal and NMSDC certifications.

Yes, the 8(a) Business Development program is still active, but as of 2026 it operates on a race-neutral basis. The SBA no longer presumes social disadvantage based on race. You must provide a fact-specific showing that you have experienced social disadvantage. Only 65 firms were admitted in 2026 under the new criteria, down from over 2,100 in prior years.

The initial application has a non-refundable processing fee starting at $350. Annual certification fees vary by your company's revenue and the regional council handling your application. The typical review process takes under 45 days for complete applications. Visit nmsdc.org for current pricing.

The federal government does not offer startup grants to individual businesses. However, Grants.gov lists over 1,000 federal grant opportunities, and some private organizations like the NMSDC Business Consortium Fund and the First Nations Development Institute provide grants to certified MBEs. State and local programs vary widely, so check your state's economic development office.

The SBA Microloan program provides loans up to $50,000 through nonprofit intermediary lenders. The average microloan is about $13,000, with interest rates between 8% and 13% and repayment terms up to six years. These loans are available to for-profit small businesses and certain nonprofit childcare centers. Find an intermediary at sba.gov/microloans.

No. SBA 7(a) and Microloan programs are open to all qualifying small businesses regardless of minority status or certification. Certification helps primarily with federal contracting set-asides (8(a), HUBZone) and corporate supply chain access (NMSDC). Many private grant programs also do not require certification, just proof of ownership.

The information on this page is for educational purposes only and does not constitute financial, legal, or investment advice. Loan terms, interest rates, and eligibility requirements vary by lender and change frequently. Always consult with a qualified financial advisor before making funding decisions. StartupOwl may earn a commission if you click our links at no extra cost to you.

Sources & References

- U.S. Census Bureau Annual Business Survey (2022 data)

- SBA Minority-Owned Businesses Resources

- SBA 8(a) Business Development Program

- SBA HUBZone Program

- SBA Microloan Program

- NMSDC Certification Process

- SCORE Find a Mentor

- America's SBDC Network

- Minority Business Development Agency (MBDA)

- SBA 8(a) Program Guidance (January 2026)

- SBA Small Business Development Centers (SBDC)

About the Author

Director of Entrepreneurial Strategy

Jennifer is a former founder who built and sold a boutique B2B logistics company in her thirties. She understands the emotional and strategic toll of building a business from the ground up without a massive safety net. She is deeply connected to the Atlanta startup ecosystem and is passionate about equitable funding.

Was this article helpful?

Questions about Minority Business Resources

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment