LLC for Freelancers

Find out whether an LLC actually saves you money as a freelancer, with real tax numbers and state-by-state costs.

In This Article

- LLC formation costs $35 to $500 depending on your state, plus $50 to $300 per year in ongoing fees.

- A single-member LLC is taxed identically to a sole proprietorship by default (Schedule C).

- At $80K+ net profit, an S Corp election can save $5,000 to $15,000 per year in SE tax.

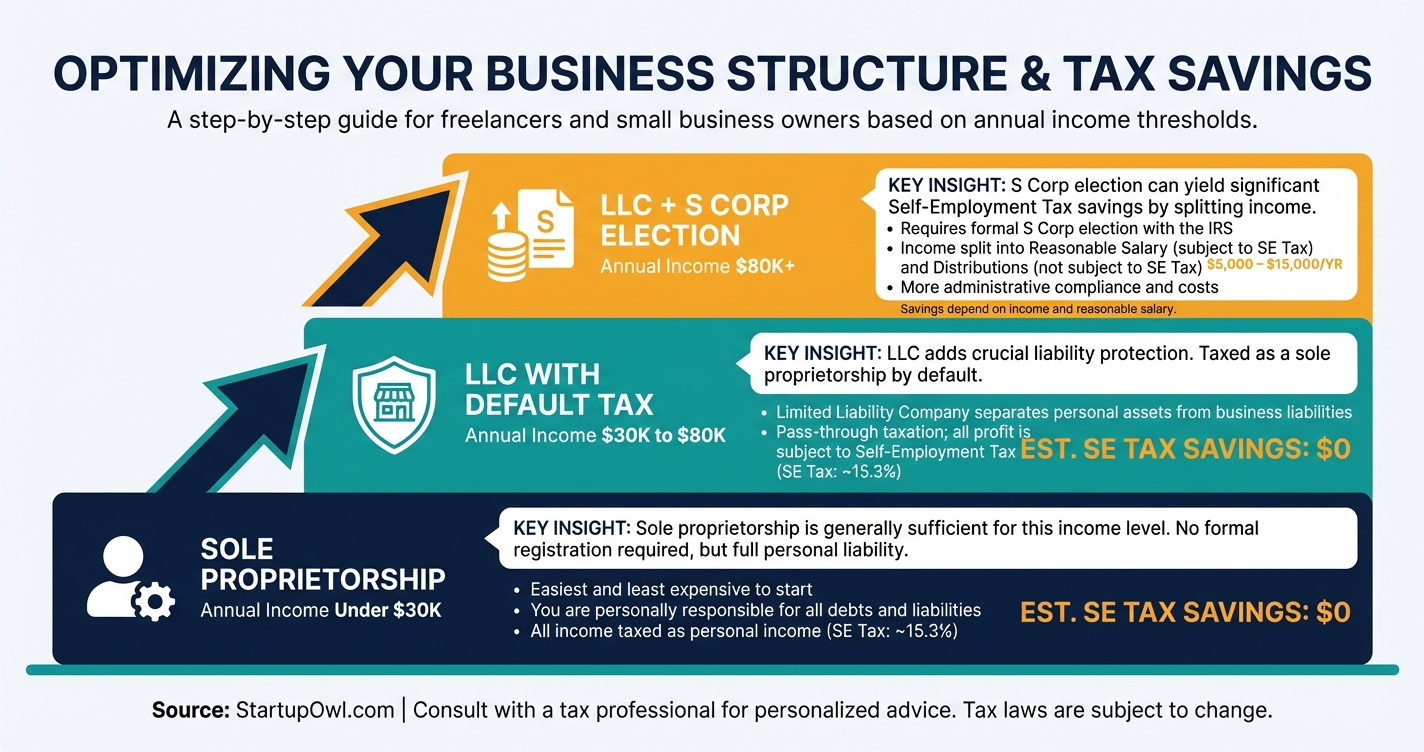

- Below $30K net profit, a sole proprietorship usually makes more sense financially.

Most freelancers earning under $30,000/year in net profit do not need an LLC yet. Between $30,000 and $50,000, an LLC adds meaningful liability protection for $35 to $500 in formation fees. Above $80,000, pair the LLC with an S Corp election (Form 2553) to potentially save $5,000 to $15,000/year in self-employment tax.

Common Freelancers Concerns

- Personal assets are exposed to lawsuits and client disputes without an LLC's liability shield

- 15.3% self-employment tax on every dollar of net profit adds up fast above $50K

- Mixing personal and business finances creates bookkeeping chaos at tax time

- Clients (especially enterprise companies) may require you to operate as a registered business entity

- Confusion about whether an LLC actually changes your tax situation (it does not by default)

- Fear of overpaying for LLC formation services that charge $200+ for a $50 to $150 state filing

A single-member LLC costs $35 to $500 to form (depending on your state) and changes nothing about your federal taxes by default. That is the most important thing to understand before you spend a dime. Your LLC is taxed identically to a sole proprietorship unless you actively elect otherwise, so the real benefits are liability protection and credibility, not an automatic tax break.

This guide walks you through the honest math on when an LLC makes financial sense for freelancers, when it does not, and what to do after you form one. If your net freelance income is above $50,000 per year, an LLC starts earning its keep. Above $80,000, an S Corp election on top of the LLC can save you thousands in self-employment tax annually.

You pay 15.3% self-employment tax on every dollar of net freelance income. That is 12.4% for Social Security (on income up to $184,500 in 2026) plus 2.9% for Medicare with no cap, as outlined by the IRS self-employment tax guidance. At $75,000 in net profit, that is roughly $10,597 in SE tax alone, before income tax.

An LLC does not reduce that tax by default. A single-member LLC is a "disregarded entity" to the IRS, meaning it is taxed exactly like a sole proprietorship. Your income still flows to Schedule C on your Form 1040. So why bother?

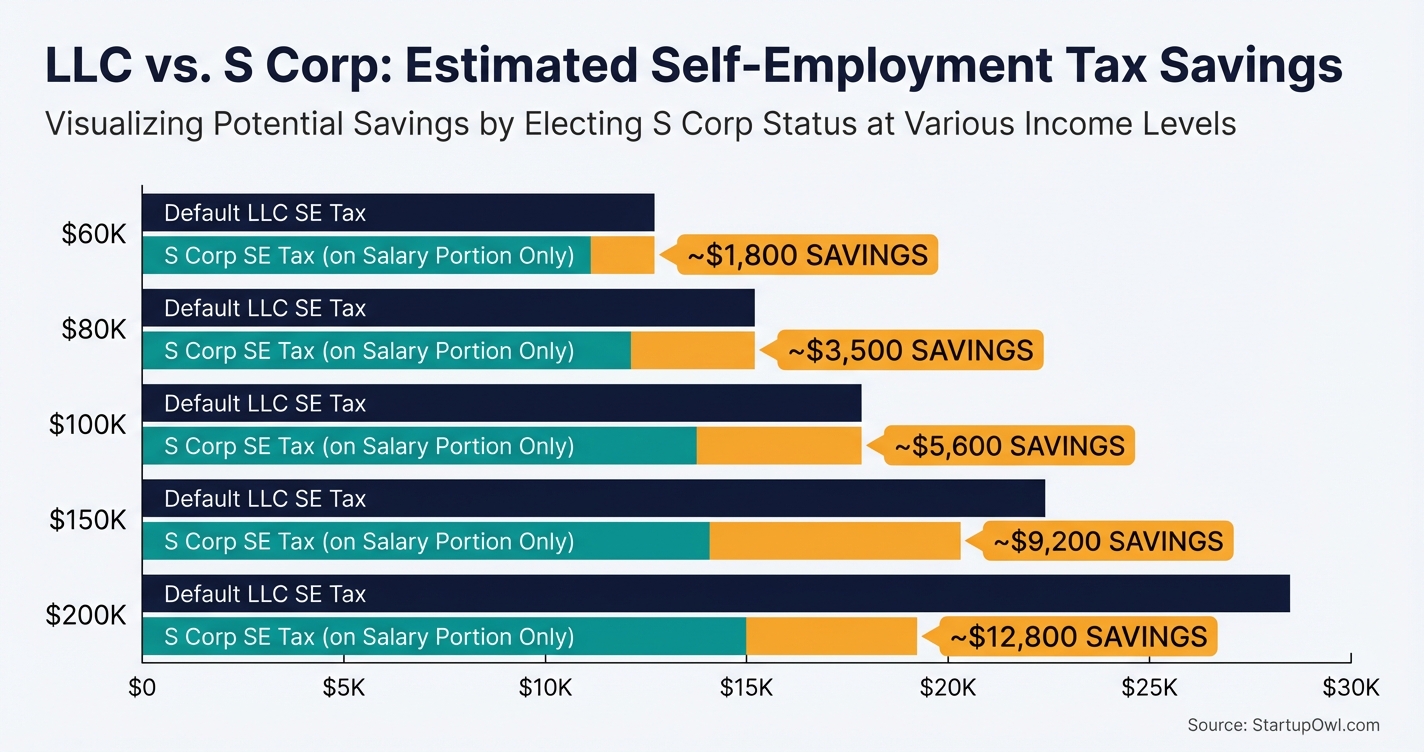

Two reasons. First, liability protection. Without an LLC, every client contract, every missed deadline, every potential lawsuit puts your personal bank account, your car, and your home at risk. Second, tax flexibility. Once your LLC exists, you can elect S Corp taxation (Form 2553) to split income between salary and distributions. At $100,000 in net profit, that split can save you roughly $5,600 per year in SE tax.

The core question is not "should I get an LLC?" but rather "at what income level does the cost justify the benefit?" The answer depends on your state filing fees, your risk exposure, and your net profit. For most freelancers, the crossover point is somewhere between $30,000 and $50,000 in annual net income for basic liability protection, and $80,000+ for meaningful tax savings through an S Corp election. For a detailed look at how different structures compare, see our complete guide to business entity types.

Your freelance LLC delivers value across four dimensions: liability, taxes, credibility, and flexibility. Here is how each one translates to real dollars.

Liability protection is the foundational benefit. If a client sues you over a deliverable, or a vendor claims breach of contract, the LLC shields your personal assets. Without it, a single lawsuit could put your savings, your house, and your retirement accounts at risk. For freelancers in web development, consulting, or any project-based work, this protection matters more than you might think.

Tax savings through the S Corp election scale with income. Here is the estimated annual SE tax savings when you elect S Corp status and pay yourself a reasonable salary (roughly 60% of net profit):

- $60,000 net profit (salary $36,000, distribution $24,000): save roughly $1,800 in SE tax

- $80,000 net profit (salary $48,000, distribution $32,000): save roughly $3,500 in SE tax

- $100,000 net profit (salary $60,000, distribution $40,000): save roughly $5,600 in SE tax

- $150,000 net profit (salary $80,000, distribution $70,000): save roughly $9,200 in SE tax

- $200,000 net profit (salary $100,000, distribution $100,000): save roughly $12,800 in SE tax

These estimates assume a single filer with no other W-2 income and use the 2026 SE tax rate of 15.3% on 92.35% of net earnings. S Corp payroll costs ($500 to $2,000/year for payroll software and additional tax filings) reduce the net savings, which is why the election rarely makes sense below $60,000 in net profit.

Credibility with enterprise clients is an underrated benefit. Many companies with formal vendor onboarding require a W-9 from a registered entity, not an individual. An LLC with its own EIN signals professionalism and can help you land contracts with larger organizations.

Tax classification flexibility is unique to the LLC. You can be taxed as a sole proprietor (default), an S Corporation, or even a C Corporation, all without changing your legal structure. No other entity type gives you that range of options. Read our LLC vs S Corp comparison for the full breakdown.

Honesty saves you money. If you are earning under $30,000 per year in net freelance income, working in a low-risk field like writing, graphic design, or virtual assistance, and have no employees, a sole proprietorship is probably fine for now.

Here is why. LLC formation costs $35 to $500 depending on your state, plus $50 to $300 in annual fees to stay compliant. In California, you will owe an $800 annual franchise tax regardless of whether your LLC earns a single dollar, as required by the California Franchise Tax Board. If your total profit is $20,000, spending $800 to $1,000 per year on LLC maintenance represents 4 to 5% of your income with no tax benefit.

The liability protection argument is weaker than you think in low-risk fields. A freelance writer producing blog posts faces minimal lawsuit risk compared to a freelance developer building production software. If your exposure is low, a professional liability insurance policy ($300 to $600/year) may give you comparable protection at a lower total cost than an LLC in a high-fee state.

The bottom line: do not form an LLC because you think you are "supposed to." Form one when the math supports it, typically when your net income crosses $30,000 to $50,000 and you want the liability shield, or when a major client requires it. You can always convert from a sole proprietorship to an LLC later without disrupting your business.

The real comparison for most freelancers is straightforward: sole proprietorship vs. single-member LLC. Here is how they stack up on the dimensions that matter to you.

Taxes are identical by default. Both a sole proprietor and a single-member LLC owner report business income on Schedule C of Form 1040. Both pay 15.3% SE tax on net earnings. The LLC does not change your tax bill by one cent unless you elect S Corp or C Corp treatment. For a detailed comparison of when each approach works best, see our single-member vs multi-member LLC guide.

Liability is the biggest difference. A sole proprietor has zero separation between personal and business assets. If you are sued, your personal bank account, your house, and your car are all fair game. An LLC creates a legal wall between your personal assets and your business obligations. That wall holds up in court only if you treat the LLC as a separate entity (separate bank account, proper records, no commingling funds).

Formation cost favors the sole proprietor. A sole proprietorship requires no state filing, no formation fee, and no annual report. You simply start working. An LLC requires filing Articles of Organization ($35 to $500), designating a registered agent, and paying annual fees in most states. The national average filing fee is roughly $132.

Ongoing compliance is heavier for the LLC. Most states require annual or biennial reports (typically $50 to $300). You will also want an LLC operating agreement, even as a single member, to document your management structure and strengthen your liability protection. A sole proprietor has none of these obligations.

If your freelance income is below $30,000/year and your work is low-risk, the sole proprietorship wins on simplicity and cost. Once you cross $50,000/year or take on clients with meaningful contract values, the LLC's liability protection is worth every penny of the filing fee.

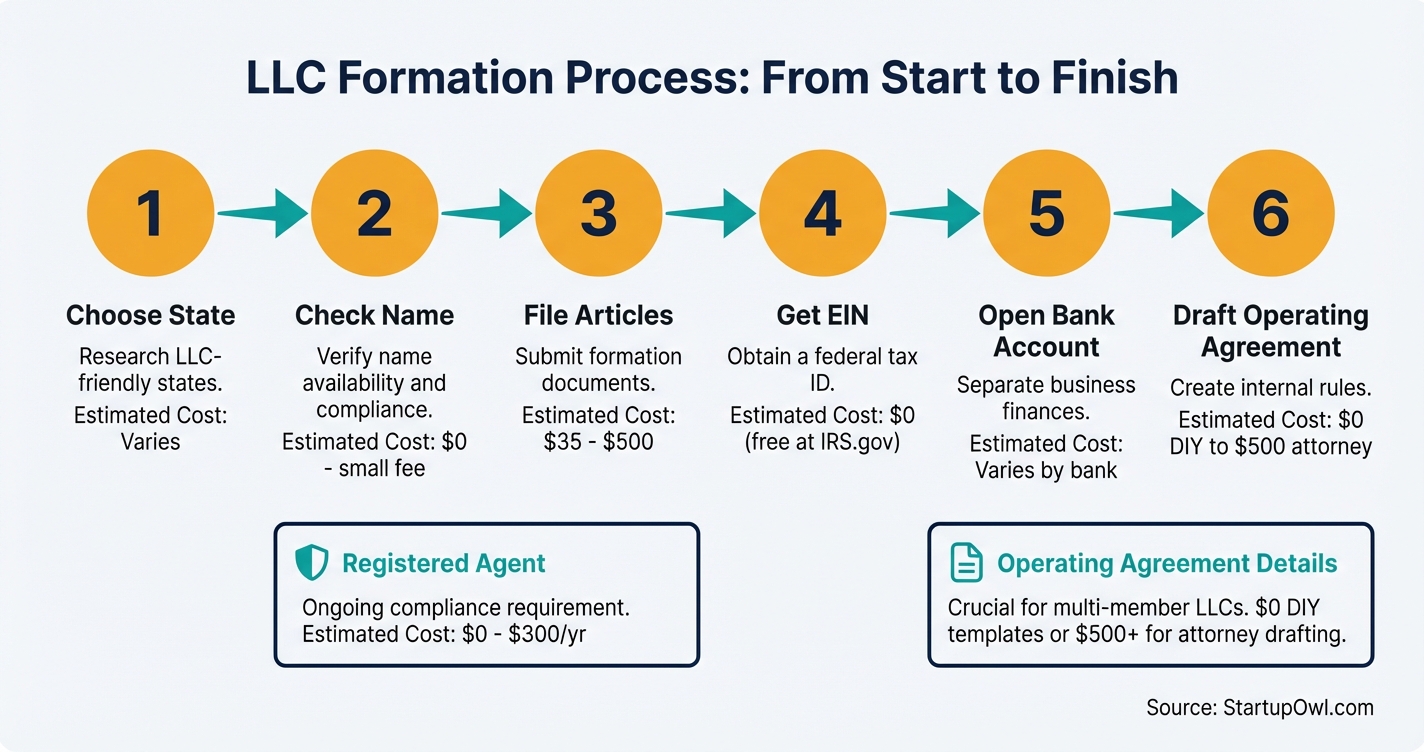

Forming your freelance LLC is a 6-step process that takes 1 to 4 weeks in most states. Here is exactly what to do, in order.

Step 1: Choose your state. File in the state where you physically work and live. Forming in Delaware or Wyoming to "save money" usually backfires for freelancers because you will still need to register as a foreign LLC in your home state, paying fees in both places.

Step 2: Check name availability. Search your state's Secretary of State database to confirm your desired LLC name is available. Also run a free search on the USPTO trademark database (TESS) to avoid infringing on an existing trademark. For detailed naming rules, see our guide on how to choose a business name.

Step 3: File Articles of Organization. Submit your formation document to your state's Secretary of State along with the filing fee. State-specific costs as of 2026:

- Florida: $125 (filed at Sunbiz.org)

- California: $70 filing fee (plus $800 annual franchise tax)

- Texas: $300 (filed via SOSDirect)

- New York: $200 (plus $300 to $1,500 in mandatory publication fees)

- Delaware: $90 (Certificate of Formation)

Step 4: Get your EIN. Apply for a free Employer Identification Number at IRS.gov/EIN. This takes under 15 minutes and is completely free. Do not pay a third-party service $50 to $200 for something the IRS provides at no cost. See our EIN application guide for a step-by-step walkthrough.

Step 5: Open a business bank account. Bring your Articles of Organization, EIN confirmation letter, and a photo ID to any bank. Many banks offer free business checking for small accounts. Separating your finances from day one protects your liability shield. Check our list of best business bank accounts for freelancer-friendly options.

Step 6: Draft an operating agreement. Even as a single-member LLC, an operating agreement documents your ownership, management structure, and profit distribution. Most states do not require you to file it, but it strengthens your liability protection. DIY templates cost $0; attorney-drafted agreements run $200 to $500. Our LLC operating agreement guide has free templates and a clause-by-clause walkthrough.

If you want professional help with the filing process, our best LLC formation services comparison covers options from $0 + state fee to full-service packages.

Your LLC is approved. Now you need to handle five things to stay compliant and set yourself up for clean tax filing.

1. Update your client contracts and invoices. Every contract, invoice, and W-9 should now list your LLC's legal name (including "LLC") and your EIN instead of your Social Security Number. Notify existing clients of the name change in writing. This is not optional; it protects your liability shield.

2. Set up quarterly estimated tax payments. If you expect to owe $1,000 or more in taxes for the year, the IRS requires quarterly payments due April 15, June 15, September 15, and January 15. Use IRS Direct Pay or EFTPS.gov. Missing these deadlines triggers penalties and interest.

3. File your taxes correctly. As a single-member LLC with default tax treatment, you file Schedule C (Profit or Loss from Business) attached to your personal Form 1040. You do not file a separate business return. Your self-employment tax is calculated on Schedule SE. If you elected S Corp status, you file Form 1120-S for the business and receive a K-1 for your personal return.

4. File your state's annual report. Most states require an annual or biennial report to keep your LLC in good standing. Fees range from $0 (Ohio, Missouri, New Mexico) to $300+ (Tennessee, Delaware). Miss the deadline and your state can dissolve your LLC. See our LLC annual report guide for state-specific deadlines and fees.

5. Consider the S Corp election when the time is right. If your net profit passes $60,000 to $80,000, talk to a CPA about filing IRS Form 2553 to elect S Corp taxation. For 2026, the deadline for calendar-year filers is March 17, 2026. The form must be mailed or faxed (no online filing as of 2026). The IRS sends a confirmation letter (CP261) within 60 days. Learn more about the process in our how to start an S Corp guide.

Bonus: File your BOI report. The FinCEN Beneficial Ownership Information report is required for most LLCs. Filing is free and takes about 10 minutes at FinCEN's online portal.

Mistake 1: Assuming an LLC automatically reduces your taxes. It does not. A single-member LLC is a disregarded entity. Your SE tax bill is exactly the same as a sole proprietor's. The tax savings only come if you actively elect S Corp status via Form 2553, and even then, only above roughly $60,000 in net profit.

Mistake 2: Paying a third-party service for a free EIN. The IRS provides EINs at $0 through its online application at IRS.gov. Services charging $50 to $200 for this are adding zero value. The process takes under 15 minutes.

Mistake 3: Mixing personal and business bank accounts. This is the fastest path to losing your LLC's liability protection. Courts call it "piercing the corporate veil," and it happens when you treat the LLC like a personal piggy bank. Open a dedicated business account the same week you receive your EIN.

Mistake 4: Forgetting annual report filings. Your state will administratively dissolve your LLC if you miss annual report deadlines. In Florida, for example, the annual report costs $138.75, but a late filing triggers a $400 penalty. Set a calendar reminder 30 days before each deadline.

Mistake 5: Forming in a "cheap" state instead of your home state. Filing your LLC in Wyoming or New Mexico to save on fees sounds smart, but if you live and work in California, you still need to register as a foreign LLC in California, pay the $800 franchise tax, and comply with California rules. You end up paying fees in two states instead of one.

Mistake 6: Setting an unreasonably low salary with an S Corp election. The IRS requires S Corp owner-employees to pay themselves "reasonable compensation." If you earn $150,000 and pay yourself a $30,000 salary, expect scrutiny. A good rule of thumb is setting your salary at 50 to 60% of net profit, or matching what you would pay someone else to do the same work.

Frequently Asked Questions

Sources & References

- IRS: Self-Employment Tax (Social Security and Medicare Taxes)

- IRS: About Form 2553, Election by a Small Business Corporation

- IRS: Topic No. 554, Self-Employment Tax

- SBA: Choose a Business Structure

- California Franchise Tax Board: Limited Liability Company

- Florida Division of Corporations: LLC Fees

- Delaware Division of Corporations

About the Author

Legal & Compliance Analyst

Daniel grew up in the shadow of Silicon Valley but chose the legal route over engineering, working as a paralegal for a corporate law firm specializing in mergers and acquisitions. He realized that early-stage founders were constantly making catastrophic legal mistakes because they couldn't afford a $500/hour attorney, prompting his move to B2B media.

Was this article helpful?

Questions about this guide

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment