C Corp vs S Corp

C Corp vs S Corp compared side by side on taxes, ownership limits, formation costs, and compliance. Find the right structure for your business with real numbers.

In This Article

- S Corps avoid double taxation; C Corps pay 21% corporate tax plus shareholder dividend tax.

- S Corps cap at 100 U.S. shareholders with one stock class; C Corps have no limits.

- S Corp election saves $5K to $15K/year on self-employment tax above $80K profit.

- C Corps are required for VC funding, foreign investors, and QSBS capital gains exclusion.

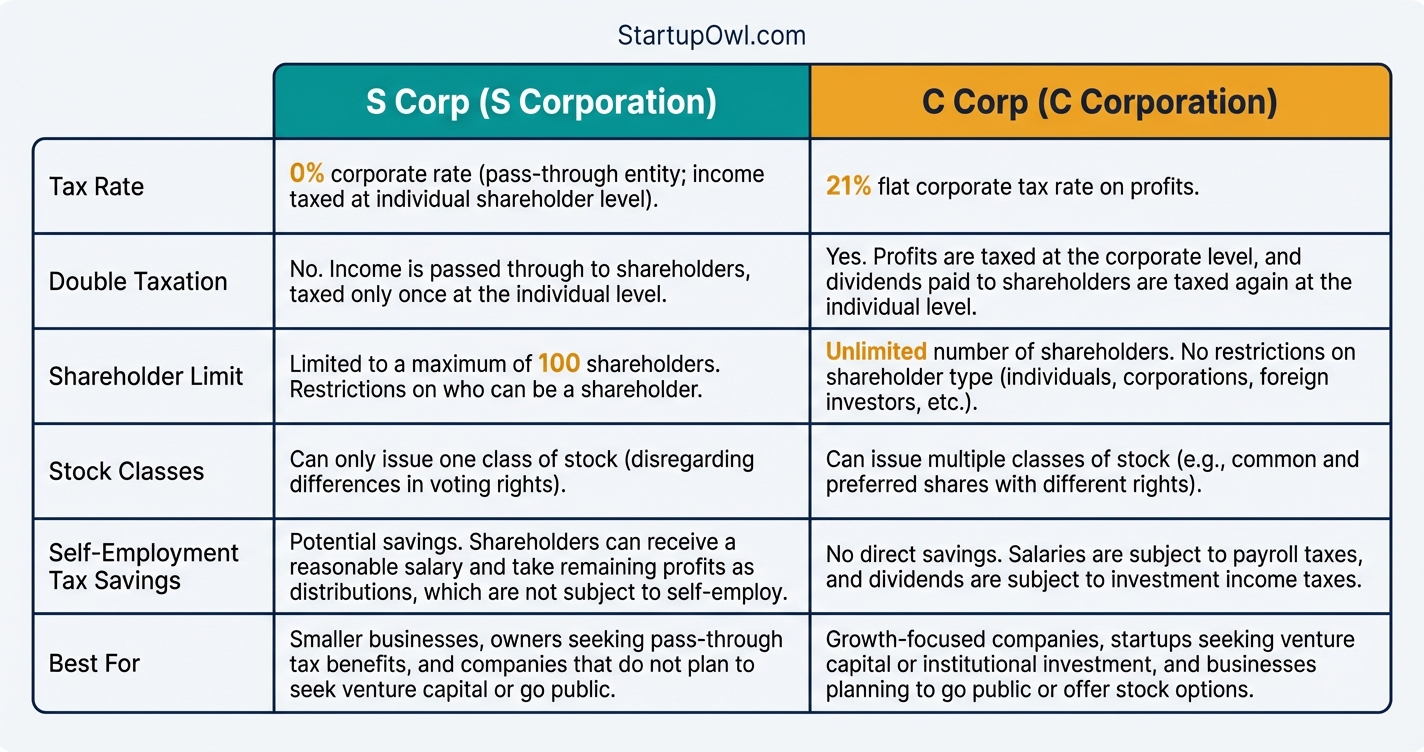

The choice between a C Corp and an S Corp boils down to one thing: how you want your profits taxed. A C Corp pays a flat 21% federal tax on profits, then shareholders pay tax again on dividends (at 15% to 23.8%). An S Corp skips that corporate-level tax entirely and passes everything to your personal return.

On $150,000 in profit, that difference can mean keeping $18,000 to $30,000 more per year. But the S Corp comes with strict ownership rules (max 100 shareholders, U.S. residents only, one class of stock) that make it a dealbreaker if you plan to raise venture capital. This guide walks through every dimension so you can pick the right structure.

C Corporation

- Taxation

- Flat 21% federal corporate tax, plus 15%-23.8% on dividends (double taxation).

- Liability

- Full personal asset protection. Shareholders only risk their investment.

- Formation Cost

- $50-$500 state filing fee. Delaware charges $89; California $100.

- Best For

- VC-backed startups, companies with foreign investors, high-growth exits.

S Corporation

- Taxation

- Pass-through. No corporate tax. Profits taxed on your personal return only.

- Liability

- Full personal asset protection. Same corporate veil as a C Corp.

- Formation Cost

- $50-$500 state filing plus free IRS Form 2553 election.

- Best For

- Profitable small businesses over $80K wanting self-employment tax savings.

A C Corporation is the default corporate structure under Subchapter C of the Internal Revenue Code. Every corporation formed at the state level starts as a C Corp unless you file for S Corp election. It is a separate legal entity that pays its own federal income tax at a flat 21% rate.

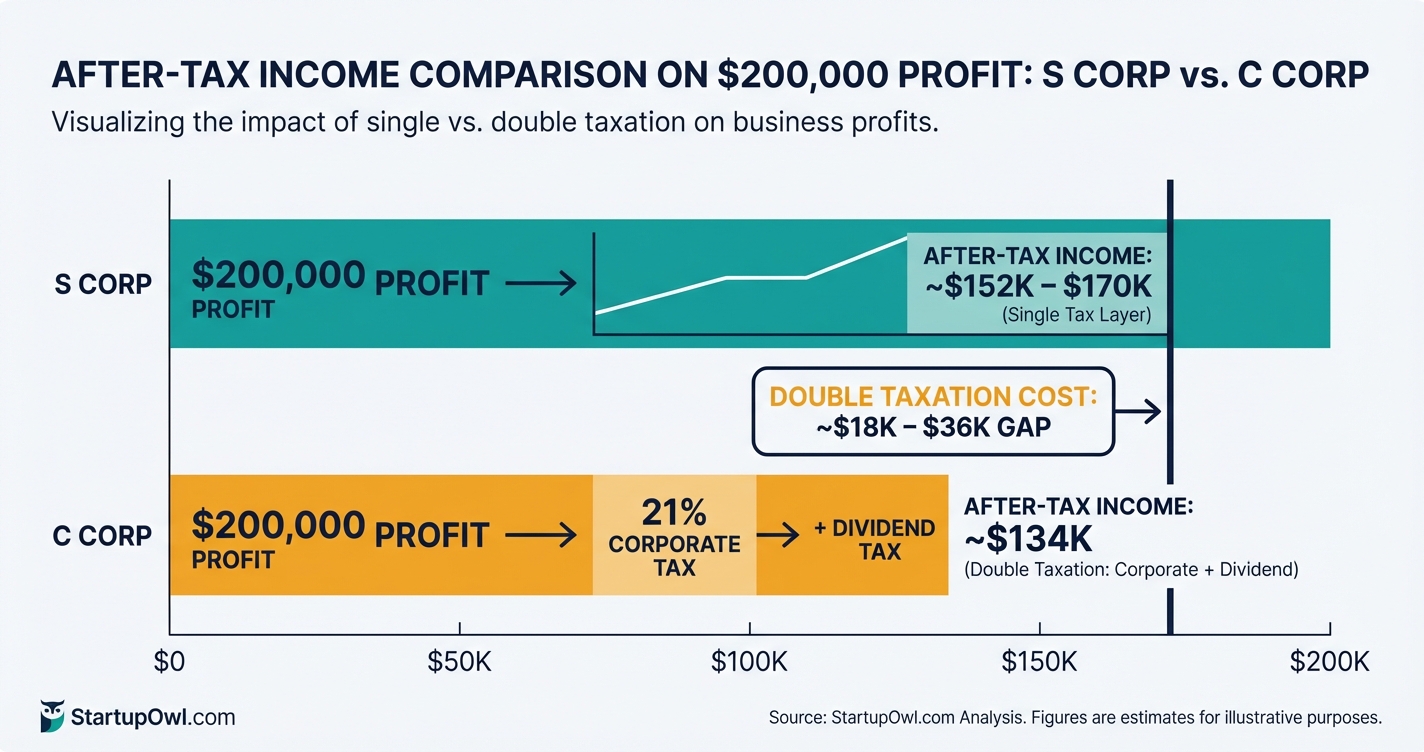

The defining feature is double taxation. Profits are taxed once at the corporate level, then shareholders pay tax again at 15% to 23.8% when dividends are distributed. On $200,000 in fully distributed profit, double taxation costs roughly $65,700 in combined federal taxes, compared to about $30,000 through an S Corp.

So why would anyone choose a C Corp? Three reasons stand out:

- Unlimited investors of any type (individuals, funds, foreign entities, other corporations)

- Multiple stock classes (common, preferred, convertible) for complex fundraising

- QSBS eligibility (Section 1202) that can exclude up to $15 million in capital gains at sale

If you are exploring other structures, check out our complete guide to business entity types to see how C Corps compare to LLCs, partnerships, and sole proprietorships.

An S Corporation is not a different type of company. It is a tax election you make with the IRS by filing Form 2553. Your state sees the same corporation. The IRS sees a pass-through entity taxed under Subchapter S.

The big advantage: no corporate-level federal income tax. All profits and losses pass through to shareholders' personal returns, avoiding the double taxation that hits C Corps. You file Form 1120-S as an information return and issue each shareholder a Schedule K-1.

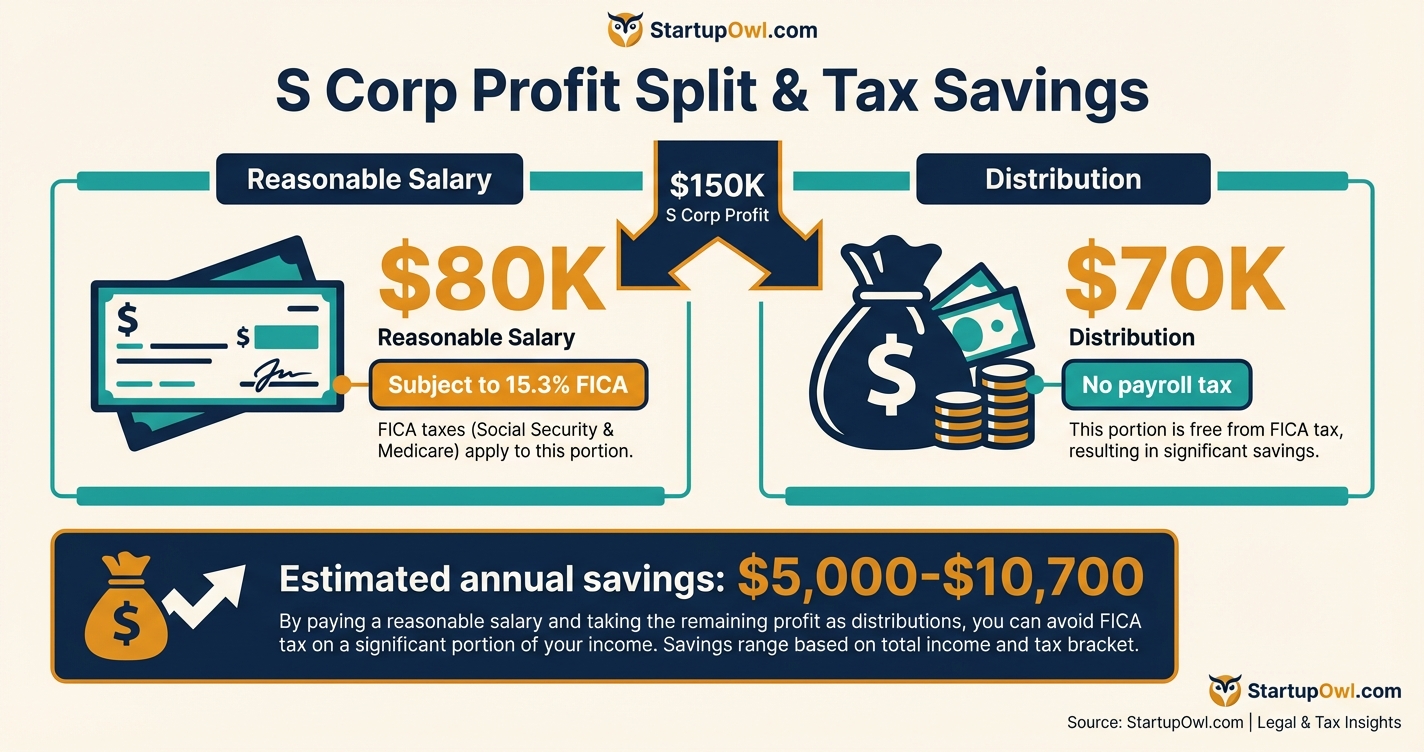

The second advantage is the salary-distribution split. You pay yourself a market-rate W-2 salary (subject to 15.3% FICA), then take remaining profits as distributions (not subject to payroll tax). On $150,000 in profit with a $70,000 salary, you skip FICA on $80,000, saving roughly $5,000 to $12,000 per year.

The trade-off is strict eligibility rules: maximum 100 shareholders, all must be U.S. individuals or qualifying trusts, and only one class of stock is allowed. If you need to learn more about S Corp formation, read our step-by-step guide to starting an S Corp.

Tax treatment is the biggest difference between these two structures, and it is where your money is won or lost. Here is a breakdown across all five dimensions.

Tax Treatment

C Corps pay a flat 21% federal income tax on all corporate profit. When those profits are distributed as dividends, shareholders pay again at 0%, 15%, or 20% depending on income, plus a potential 3.8% Net Investment Income Tax. The combined effective rate on fully distributed C Corp profit ranges from 32% to about 40%.

S Corps pay $0 in federal corporate tax. All income flows to shareholders' personal returns and is taxed at individual rates (10% to 37%). S Corp owners may also claim the QBI deduction, reducing taxable pass-through income by up to 20%.

Liability Protection

Both structures provide identical liability protection. Shareholders' personal assets are shielded from business debts and lawsuits. The corporate veil applies the same way regardless of tax election. You lose this protection only if you fail to maintain corporate formalities (commingling funds, skipping board meetings, or undercapitalizing the business).

Formation and Paperwork

Both require the same state-level incorporation: file Articles of Incorporation with your Secretary of State, pay a filing fee of $50 to $500, and designate a registered agent. The S Corp adds one extra step: filing IRS Form 2553 within 2 months and 15 days of the start of your tax year. For calendar-year businesses in 2026, that deadline is March 17, 2026 (March 15 falls on a Sunday).

Management and Ownership

C Corps can have unlimited shareholders of any type (individuals, other corporations, partnerships, foreign entities) and issue multiple classes of stock (common, preferred, convertible). S Corps are capped at 100 shareholders, limited to U.S. citizens or resident aliens (plus certain trusts and estates), and restricted to one class of stock.

Ongoing Compliance

C Corps file Form 1120, hold annual board meetings, keep corporate minutes, and face potential accumulated earnings tax (20% penalty on retained earnings over $250,000 without documented business need). S Corps file Form 1120-S, issue K-1s, and must run payroll for shareholder-employees at a reasonable salary. The IRS actively audits S Corps for underpayment of owner compensation, so keep your salary documentation airtight.

C Corporation Pros

- Unlimited fundraising flexibility. Issue preferred stock, convertible notes, and equity to any investor type in any country. This is non-negotiable for VC-backed companies.

- 21% corporate rate on retained earnings. If you reinvest all profits and never distribute dividends, you pay only 21% (vs. up to 37% individual rate).

- QSBS capital gains exclusion. Under Section 1202 (updated by OBBBA 2026), founders can exclude up to $15 million in gains when selling qualifying C Corp stock held for 5+ years.

- Full fringe benefit deductions. C Corps can deduct health insurance, group life insurance, and disability insurance premiums for all shareholder-employees. S Corps limit this for shareholders owning more than 2%.

C Corporation Cons

- Double taxation is expensive. On $200,000 in distributed profit, you lose about $65,700 in combined corporate and dividend taxes.

- Accumulated earnings tax. The IRS charges 20% on retained earnings above $250,000 ($150,000 for personal service corporations) if you cannot document a business need.

- Higher accounting costs. Separate corporate tax return (Form 1120), board minutes, and shareholder meeting requirements add $2,000 to $5,000/year in professional fees.

S Corporation Pros

- No double taxation. Profits are taxed once at your individual rate. Period.

- Self-employment tax savings. The salary-distribution split saves $5,000 to $15,000/year for owners earning $80K+ in profit.

- QBI deduction eligibility. Up to 20% of qualified business income can be deducted, effectively lowering your tax bracket.

- No accumulated earnings tax. Since all income passes through to shareholders regardless of distribution, the AET does not apply.

S Corporation Cons

- Strict ownership limits. Max 100 shareholders, U.S. individuals only, one stock class. This blocks VC fundraising and complex investor structures.

- Reasonable salary requirement. The IRS requires market-rate compensation for shareholder-employees. Underpayment triggers reclassification of distributions as wages, plus back payroll taxes, 20% accuracy penalties, and interest.

- Payroll overhead. Running W-2 payroll costs $500 to $2,000/year through services like Gusto or ADP, plus the complexity of quarterly payroll tax filings.

- Form 1120-S complexity. The S Corp tax return is significantly more involved than a sole proprietor's Schedule C, adding $1,000 to $3,000 in annual CPA fees.

Your choice depends on your specific scenario. Use these if/then rules to find your match.

If you earn over $80,000 in annual profit and plan to distribute income to yourself, the S Corp almost always wins. The salary-distribution split saves real money on payroll taxes, and the QBI deduction shaves up to 20% more off your taxable income. A sole proprietor making $150,000 pays about $21,000 in self-employment tax. An S Corp owner with a $70,000 salary pays about $10,700 in FICA and takes the rest as distributions.

If you plan to raise venture capital or bring on institutional investors, choose the C Corp. VCs invest using preferred stock with liquidation preferences, anti-dilution clauses, and board seats. S Corps cannot issue multiple stock classes, so this structure is off the table. Nearly every accelerator and institutional fund requires a Delaware C Corp.

If you have or expect foreign shareholders, the C Corp is your only option. S Corps require all shareholders to be U.S. citizens or resident aliens. Adding even one foreign national terminates your S Corp status retroactively.

If your business is in the early stage, pre-revenue, and reinvesting all cash, the C Corp's 21% rate beats the top individual rate of 37%. As long as you do not distribute dividends, double taxation does not apply. You build entity value for QSBS eligibility at exit.

If you are a small service business (consulting, freelancing, agency) earning $50K to $300K, the S Corp is likely your best bet. Run the numbers: subtract the cost of payroll ($500-$2,000/year) and extra CPA fees ($1,000-$3,000/year) from your estimated payroll tax savings. If the savings exceed the costs, the S Corp wins. Our sole proprietorship vs LLC comparison covers whether you even need to incorporate.

If you plan to sell the business within 5 years for a significant gain, compare QSBS benefits (C Corp only) against the simplicity of an S Corp sale. A C Corp founder selling $10 million in QSBS stock could save over $2 million in capital gains tax. But if the sale price is modest, the ongoing double taxation costs may outweigh exit savings.

The incorporation process is identical for both C Corps and S Corps at the state level. The S Corp simply adds one extra IRS filing.

Steps for Both Structures

- Choose your state of incorporation. Delaware is the standard for VC-backed startups (filing fee: $89). If you operate locally, incorporate in your home state to avoid foreign qualification fees. California charges $100, Florida $70, Texas $300, and New York $125.

- Reserve your business name. Check availability with your state's Secretary of State. If you need a DBA, see our DBA filing guide. To change your name later, read our how to change your LLC name guide (the process is similar for corporations).

- File Articles of Incorporation. Include your corporation name, registered agent, authorized shares, and incorporator details. Processing takes 1 to 5 business days online in most states; up to 4 weeks by mail.

- Get an EIN. Apply free at IRS.gov. You need this for bank accounts, payroll, and tax filings.

- Draft bylaws and hold an organizational meeting. Appoint directors and officers, authorize stock issuance, and adopt bylaws. Keep minutes of this meeting.

- Open a business bank account. Bring your EIN, Articles of Incorporation, and organizational minutes.

Additional Step for S Corp Only

File IRS Form 2553 within 2 months and 15 days of the start of your tax year. For new businesses, the clock starts on your formation date. All shareholders must sign. The IRS accepts Form 2553 by mail or fax only (no e-filing as of 2026). Faxing gives you instant confirmation. Expect a CP261 acceptance letter within about 60 days.

If you miss the deadline, late election relief is available under Rev. Proc. 2013-30 for up to 3 years and 75 days after the intended effective date. Want help with the filing? Our best LLC formation services comparison covers providers that handle S Corp elections too.

For businesses that need to register in multiple states, see our foreign LLC registration guide (the foreign qualification process applies to corporations too). If your business structure no longer fits, our how to dissolve an LLC guide covers the wind-down process. And do not forget your annual report requirements, which apply to corporations in most states.

Frequently Asked Questions

Sources & References

- IRS: S Corporations

- IRS: About Form 2553, Election by a Small Business Corporation

- IRS: Wage Compensation for S Corporation Officers (Fact Sheet 2008-25)

- SBA: Choose a Business Structure

- PwC: United States Corporate Tax Summary

- Cornell Law LII: 26 U.S. Code Subchapter S

- FinCEN: Beneficial Ownership Information Reporting

About the Author

Legal & Compliance Analyst

Daniel grew up in the shadow of Silicon Valley but chose the legal route over engineering, working as a paralegal for a corporate law firm specializing in mergers and acquisitions. He realized that early-stage founders were constantly making catastrophic legal mistakes because they couldn't afford a $500/hour attorney, prompting his move to B2B media.

Was this article helpful?

Questions about this guide

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment