Equipment Financing for Small Business in 2026

Equipment financing rates range from 4% to 45% APR in 2026. Compare top lenders, credit score minimums (580+), and learn whether to lease or buy equipment.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- How Do I Finance Business Equipment

- What Equipment Financing Is and When to Use It

- Who Qualifies for Equipment Financing

- How to Apply for Equipment Financing

- The Real Cost of Equipment Financing in 2026

- Top Equipment Financing Lenders Compared

- Equipment Financing by Industry

- What to Do If You Do Not Qualify

- 5 Equipment Financing Mistakes That Cost You Money

- FAQ

$0–$5,000,000

Est. Loan Cost

21 days

Timeline

5

Total Steps

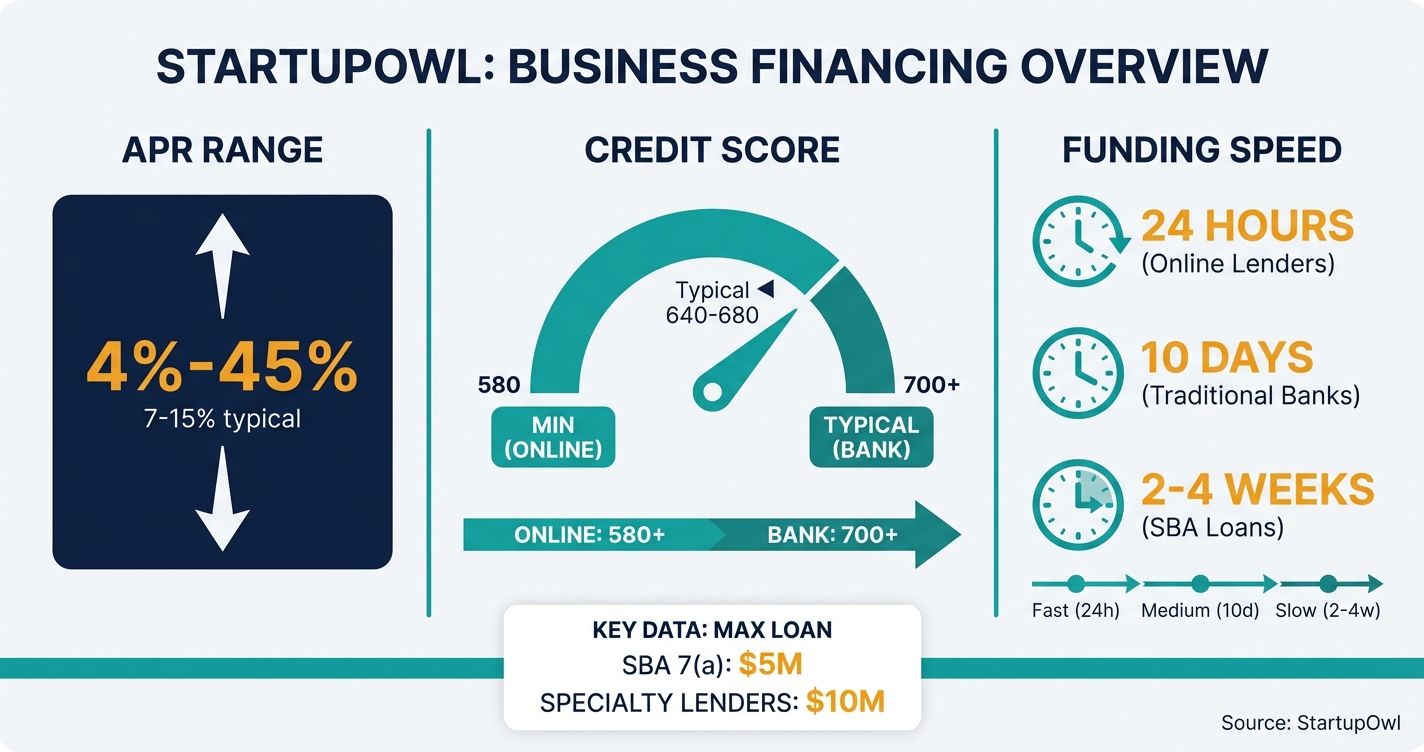

Equipment financing lets you spread the cost of business machinery, vehicles, and technology over 1 to 10 years while the equipment itself serves as collateral. Rates range from 4% to 45% APR depending on your credit profile, the lender type, and the equipment you are buying. Most established small businesses with credit scores of 620 or higher land in the 7-15% APR range.

You can finance anything from a $5,000 laptop setup to a $10 million fleet of construction equipment. Unlike unsecured working capital loans, the built-in collateral means lower rates and easier approval, even for newer businesses.

The 2026 rate environment favors planning over speculation. The Federal Reserve cut rates three times in late 2026 and held steady in January 2026, bringing the prime rate to 6.75%. If you have been waiting for a dip, this is a reasonable entry point to lock in fixed-rate equipment financing.

How Do I Finance Business Equipment

Four routes exist. Financing business equipment means picking one. An equipment loan spreads the cost over 1 to 10 years. The machine itself is the collateral. Rates run 7% to 15% for most qualified borrowers in 2026. A lease keeps payments lower and hands you a buyout choice at the end. An SBA 7(a) loan is the cheapest route for big purchases, up to $5 million. It takes 2 to 4 weeks. Buying the whole business that owns the machines? Our laundromat buyer guide shows how equipment age moves a purchase price, and our gas station guide does the same for pumps and tanks. Rolling stock buyer instead? Semi truck financing has its own tier math. And a working capital loan covers equipment adjacent costs when the purchase itself is small. The fastest online route funds in about 24 hours. Banks want a 700 credit score. Online lenders approve from 580. Zero down deals are common for established businesses because the collateral is built in.

Check your equipment financing rate at National Funding. Approval runs about 24 hours.

What Equipment Financing Is and When to Use It

Equipment financing is a type of asset-backed loan where the equipment you purchase acts as collateral. The lender holds a security lien on the asset until you pay off the balance, but you own and operate the equipment from day one. This structure means lower risk for the lender, which translates to lower APRs for you compared to unsecured business lines of credit.

There are two main structures. An Equipment Finance Agreement (EFA) gives you ownership immediately and lets you claim tax benefits like Section 179 deductions. An equipment lease lets you use the equipment with lower monthly payments, but you do not build equity and typically pay more over the total agreement.

Use equipment financing when you plan to keep the asset for 3+ years, when the equipment holds its value well (heavy machinery, commercial vehicles), or when you want to claim the Section 179 deduction. If you need to upgrade technology every 2-3 years, leasing may make more sense.

Who Qualifies for Equipment Financing

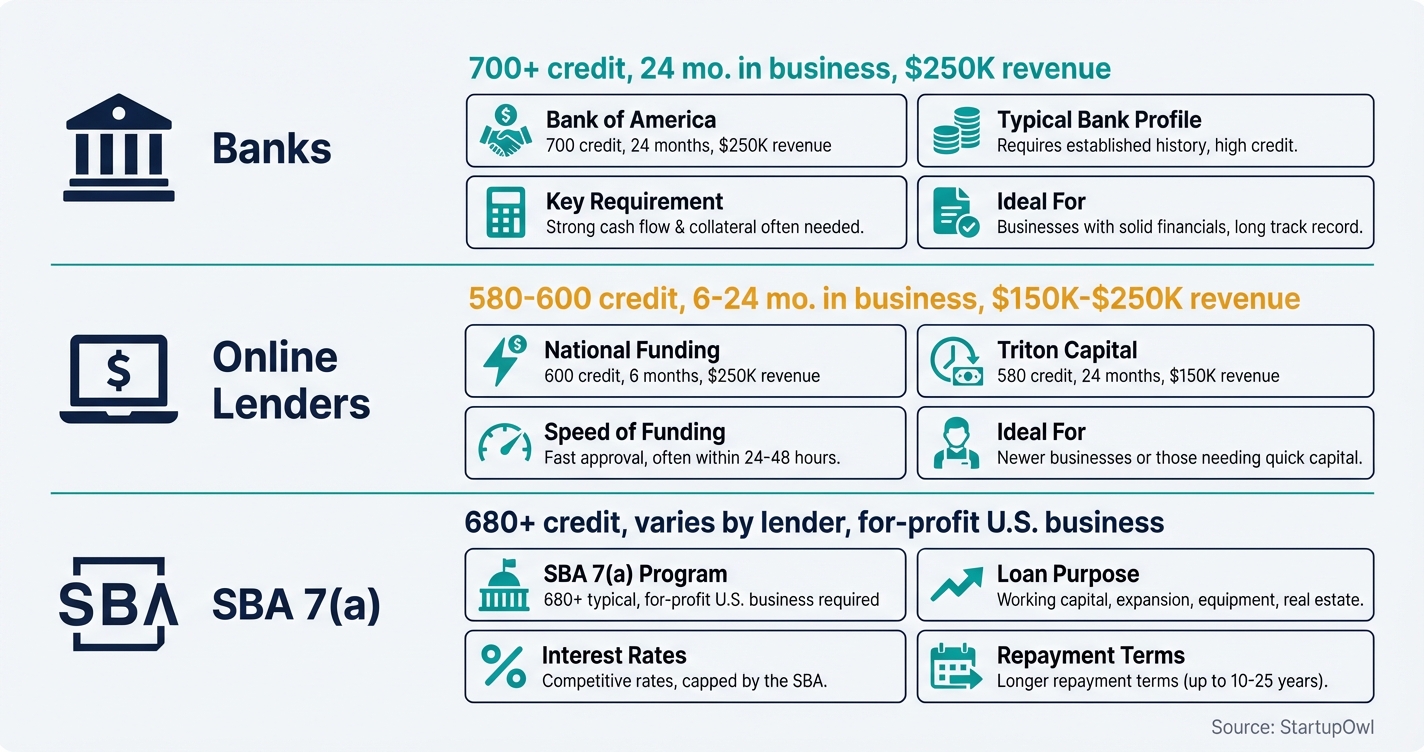

Eligibility varies widely by lender type. Online lenders accept credit scores as low as 580 (Triton Capital) to 600 (National Funding), while traditional banks like Bank of America require a minimum of 700. Time in business matters too. National Funding wants 2 years for its equipment product (the 6 month floor applies to its working capital loans), and Bank of America and Triton Capital both want 24 months.

Annual revenue requirements range from $150,000 (Triton Capital) to $250,000 (National Funding, Bank of America). If your revenue is below $150,000, consider an SBA microloan (up to $50,000) or microloans for small business from nonprofit lenders.

For SBA 7(a) equipment loans, you must operate a for-profit business in the U.S. and demonstrate that you cannot access credit on reasonable terms from non-government sources. SBA lenders typically want a personal credit score of 680+ and a debt service coverage ratio of at least 1.15x. The SBA does not publish a fixed minimum credit score, so individual lender requirements vary.

How to Apply for Equipment Financing

The application process for equipment financing follows five steps, from identifying your equipment needs to closing the loan. The timeline ranges from 24 hours with online lenders to 2-4 weeks with traditional banks and SBA lenders.

Start by getting a written vendor quote that includes soft costs (delivery, installation, taxes). Next, pull your credit score and gather your financial documents: 2 years of tax returns, 3-6 months of bank statements, and a current profit-and-loss statement. Compare at least 3 lender offers before choosing.

Online lenders like National Funding offer 24-hour approval and next-day funding for straightforward applications. Bank of America funds within 10 business days of approval. SBA 7(a) loans require the most paperwork, including SBA Form 1919 and a Personal Financial Statement, and typically close in 2-4 weeks.

If you are a startup, focus on lenders with low time-in-business requirements. National Funding accepts businesses with 6 months of history and a credit score of 600+, making it one of the most accessible options for newer businesses. For a broader look at startup-friendly options, see our guide to business loans for startups.

The Real Cost of Equipment Financing in 2026

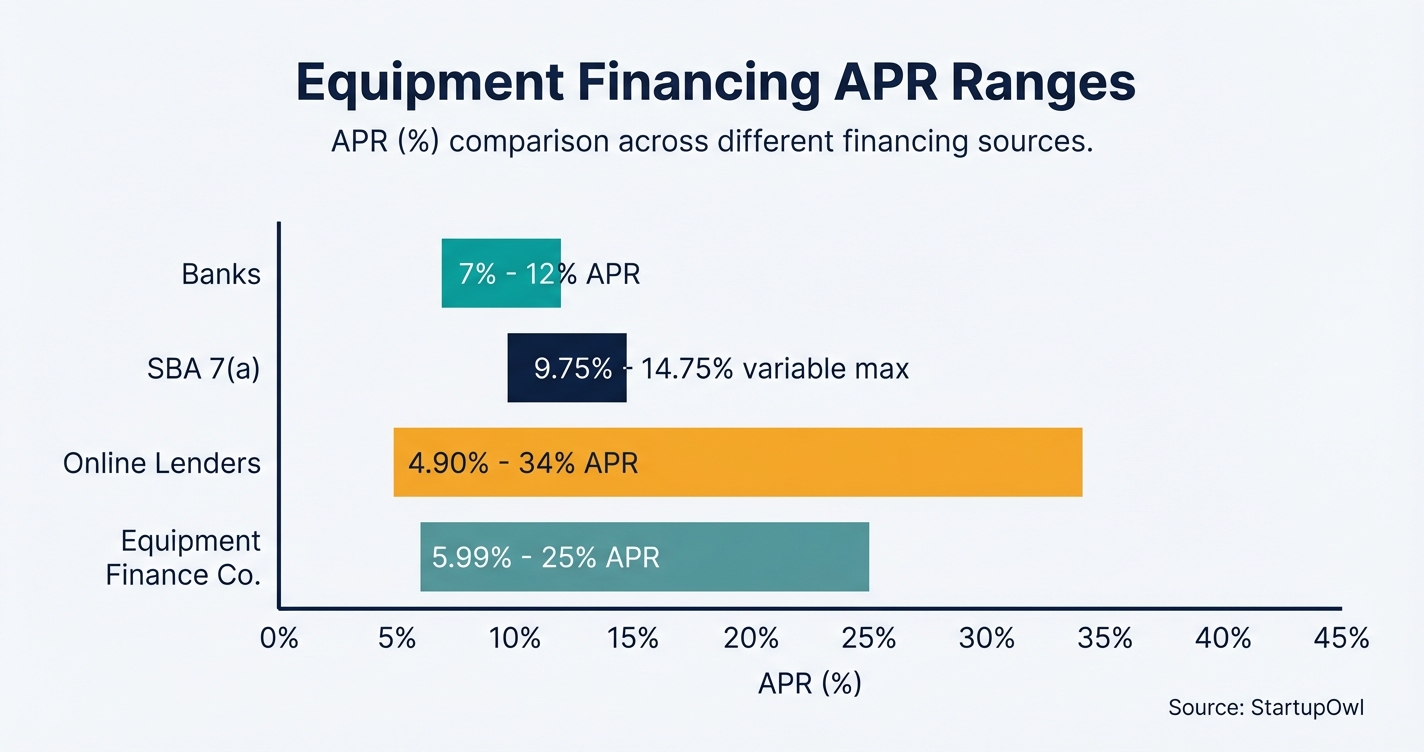

Your total cost of capital includes the APR, origination fees, any down payment, and potential prepayment penalties. Equipment financing APRs range from 4% to 45%, but the range tightens significantly based on lender type. Banks charge 6-12%, SBA 7(a) variable rates currently run 9.75% to 14.75% (as of February 2026, per Lendio), and online lenders range from 4.90% to 34%.

Origination fees add 0.5% to 4% of the loan amount to your upfront cost. SBA 7(a) loans also carry a guarantee fee of 0.25% to 3.75% of the guaranteed portion, depending on loan size (per NerdWallet's FY2026 fee schedule). Many established businesses qualify for zero-down financing, but startups or borrowers with challenged credit may need to put up 1-2 months of payments in advance.

Here is the real impact on a $100,000 equipment purchase at 10% APR over 5 years: you will pay roughly $27,480 in total interest, bringing your all-in cost to about $127,480 before fees. Add a 2% origination fee ($2,000), and your true cost is approximately $129,480. Run these numbers for your specific scenario before signing.

Want a fast quote to weigh against a bank offer? National Funding quotes in about a day. Our National Funding review covers what to check before signing.

Top Equipment Financing Lenders Compared

Bank of America is the best option if you have strong credit. Rates start at 7% APR, and Preferred Rewards members get an additional 0.25%-0.75% discount. Loans go up to $750,000 with terms up to 60 months. You will need a credit score of 700+, 24 months in business, and at least $250,000 in annual revenue. Funds arrive within 10 business days of approval.

National Funding is the fastest route we have tested. Their equipment financing goes to $150,000. No down payment. New or pre-owned equipment, approval inside 24 hours with next-day funding available. You need a 600 credit score and two years in business for the equipment product. Younger than that, their working capital loan starts at six months of history. It can cover smaller equipment needs. The trade off stays real, speed costs more than a bank. Check your rate at National Funding.

Triton Capital accepts the lowest credit scores among major lenders at 580 and offers customized repayment schedules (monthly, quarterly, semi-annual, or seasonal). Loans go up to $250,000 with terms of 3-96 months. You will need 24 months in business and $150,000 in annual revenue.

U.S. Bank stands out for its 125% financing option, which covers soft costs like installation, tax, and freight on top of the equipment cost. Loans go up to $1,000,000 with flexible payment schedules (monthly, quarterly, or annually). You can even finance multiple pieces of equipment on a single contract.

SBA 7(a) Loans are your best bet for large equipment purchases. The maximum is $5 million with terms up to 10 years, and rates are capped by the SBA at prime plus 2.25%-4.75% depending on loan size and term. The application process takes longer (2-4 weeks), but the combination of low rates and long terms makes SBA equipment loans the cheapest option over the life of the loan. See our full SBA loan guide for more details.

Equipment Financing by Industry

Some equipment gets its own market. Food trucks price differently than dental chairs. We keep dedicated guides where the niche changes the math, and this page holds the fundamentals that apply everywhere.

- Food truck financing, the build out and the truck itself.

- Dental practice loans, chairs, imaging, and practice equipment.

- Invoice factoring, when the equipment gap is really a cash flow gap on unpaid invoices.

- Revenue based financing, inventory and equipment for ecommerce brands that repay from sales.

Section 179 Can Slash Your Effective Cost by Thousands

In 2026, the Section 179 deduction lets you write off up to $2,560,000 of qualifying equipment in the year you place it in service. The phase-out begins when total qualifying purchases exceed $4,090,000. On top of that, 100% bonus depreciation (reinstated by the One Big Beautiful Bill Act of 2025) lets you deduct even more. At a 35% tax bracket, a $200,000 equipment purchase could save you roughly $70,000 in taxes in the first year. Yes, you can claim Section 179 even if you financed the equipment. Talk to your CPA before year-end to maximize this benefit.

What to Do If You Do Not Qualify

If your credit score is below 580 or your business is brand new, equipment financing becomes harder to access at reasonable rates. Here are your best alternatives:

- Merchant cash advance can fund equipment purchases within 24-48 hours with no minimum credit score, but expect effective APRs of 40-150%. Use this only for revenue-generating equipment that will pay for itself quickly.

- Invoice factoring lets you unlock cash from outstanding invoices to buy equipment outright. Fees run 1-5% per invoice, and there is no debt on your balance sheet.

- Small business grants do not need to be repaid. USDA grants, state economic development programs, and SBA-funded Community Advantage lenders sometimes offer equipment-specific grant funding.

- Vendor financing is available from many equipment manufacturers and dealers. Terms vary widely, but some offer 0% promotional APR for 6-12 months on new equipment. Always compare the vendor's rate to a third-party lender.

- Business credit cards can work for smaller equipment purchases under $25,000. Some cards offer 0% intro APR for 12-15 months, giving you an interest-free financing window.

5 Equipment Financing Mistakes That Cost You Money

1. Accepting the first offer without comparing. Equipment financing rates vary by 10-20 percentage points across lender types. A $100,000 loan at 7% vs. 17% APR over 5 years means a difference of roughly $28,000 in total interest. Compare at least 3 offers every time.

2. Ignoring the total cost of leasing. Leasing has lower monthly payments, but you pay more overall and own nothing at the end. A $50,000 piece of equipment leased over 5 years at typical lease rates will cost you 20-30% more than financing the same equipment, and you will have no resale value at the end.

3. Skipping the Section 179 deduction. The 2026 Section 179 deduction lets you write off up to $2,560,000 of qualifying equipment purchases. At a 25% effective tax rate, that is $640,000 in potential tax savings you leave on the table if you depreciate the asset over its useful life instead. File IRS Form 4562 with your tax return to claim it.

4. Timing equipment purchases on rate speculation. Waiting for rates to drop another quarter-point while your business loses revenue from outdated or missing equipment is almost always a losing trade. Match your purchase timeline to operational need, not to Federal Reserve announcements.

5. Overlooking prepayment penalties. Some lenders charge 2-5% of the remaining balance if you pay off your equipment loan early. If you plan to sell or upgrade the equipment within 2-3 years, confirm the prepayment terms before signing. Building strong business credit now gives you better terms on your next equipment purchase.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Two niches get their own pages here. Food truck financing covers the mobile kitchen split, and our Clicklease review reads the instant dealer lease everyone meets at checkout.

Step-by-Step Process

- 1

Determine the equipment you need and its total cost

Get a specific quote from your equipment vendor or dealer before approaching any lender. Include soft costs like delivery, installation, freight, and taxes in your total. U.S. Bank, for example, offers 125% financing to cover these soft costs on a single contract.

Decide whether you need new or used equipment. Used equipment financing typically comes with shorter terms and may require an inspection report. New equipment often qualifies for better rates and longer repayment periods.

Tips

- Request quotes from at least 3 vendors to establish fair market value for the equipment.

- Factor in installation, shipping, and warranty costs since some lenders will finance these.

Common Mistakes

- Underestimating total cost by forgetting freight, setup, and training fees.

- 2

Check your credit score and gather financial documents

Most online equipment lenders accept personal credit scores of 580 to 600, while traditional banks like Bank of America require 700+. Pull your free annual credit report at AnnualCreditReport.com before you apply.

Prepare your last 2 years of tax returns, 3-6 months of bank statements, a current profit-and-loss statement, and a vendor quote for the equipment. SBA loans require additional forms including Form 1919 and a Personal Financial Statement.

Tips

- Dispute any credit report errors at least 30 days before applying to give bureaus time to investigate.

- If your score is below 620, consider a cosigner to access lower rates.

Common Mistakes

- Applying to multiple lenders on the same day without realizing each hard inquiry can ding your score 5-10 points.

- 3

Compare at least 3 lenders and get pre-qualified

Start with your existing bank relationship, then compare against at least 2 online lenders. Bank of America offers rates starting at 7% APR with Preferred Rewards discounts of 0.25%-0.75%. Online lenders like National Funding approve loans up to $150,000 in as little as 24 hours.

For purchases above $350,000, get an SBA 7(a) quote. SBA equipment loans go up to $5 million with terms up to 10 years, and variable rates currently range from 9.75% to 14.75% as of February 2026. Use Lendio or a similar marketplace to compare multiple offers in one application.

Tips

- Always ask for APR (not just the interest rate) so you can compare total costs including fees.

- Request a full amortization schedule from each lender before committing.

- Ask whether the rate is fixed or variable and what the rate cap is.

Common Mistakes

- Accepting the first offer without comparing at least 2 other lenders, which can cost you 2-5% in APR.

- 4

Decide between financing and leasing

Equipment financing (buying) means you own the asset from day one and can claim Section 179 deductions of up to $2,560,000 in 2026. The lender holds a security lien until you pay off the loan, but the equipment is yours.

Leasing works better if the equipment needs upgrading every 2-3 years (think technology or medical devices). Lease payments are typically lower per month, but you will pay more over the total life of the agreement and you will not build equity. If you plan to use the same equipment for 5+ years, financing almost always costs less.

Tips

- Run the Section 179 calculator at Section179.org to see your first-year tax savings from buying.

- Ask your CPA whether a true tax lease or conditional sales lease fits your situation.

Common Mistakes

- Leasing equipment you plan to use for 5+ years, which typically costs 20-30% more than financing.

- 5

Submit your application and close the loan

Online lenders like National Funding can approve your application within 24 hours and fund the next business day. Bank of America typically takes about 10 business days after approval to release funds. SBA 7(a) loans take 2-4 weeks from application to closing.

Review the loan agreement carefully before signing. Confirm the APR, origination fee (0.5%-4%), any prepayment penalties, and the exact repayment schedule. Once funded, the lender places a UCC lien on the equipment until the loan is repaid in full.

Origination fee of 0.5%-4% of loan amount 1 day to 4 weeks depending on lender type bankofamerica.comTips

- Ask the lender if the origination fee can be rolled into the loan balance.

- Get written confirmation of any prepayment discount or penalty terms before signing.

Common Mistakes

- Signing without reading the prepayment penalty clause, which can cost you 2-5% of the remaining balance.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Interest (APR) | 4% - 45% APR | Most qualified borrowers pay 7-15%. Online lenders range 4.90%-34%. Banks start around 7%. |

| Origination Fee | 0.5% - 4% of loan amount | Can be a flat fee or percentage. Some online lenders waive it for strong applicants. |

| Down Payment | 0% - 20% | Many lenders offer 100% financing for established businesses. Startups may need 1-2 advance payments. |

| SBA Guarantee Fee | 0.25% - 3.75% | For SBA 7(a) loans only. Based on guaranteed portion of loan amount. FY2026 schedule. |

| Late Payment Fee | Varies by lender | Typically 5% of overdue payment amount or a flat fee of $25-$50. |

| Prepayment Penalty | 0% - 5% of remaining balance | Not all lenders charge this. Always confirm before signing. |

Frequently Asked Questions

Online lenders approve equipment loans with personal credit scores as low as 580 (Triton Capital) to 600 (National Funding). Traditional banks like Bank of America require 700+. A higher score gets you lower rates, so check your business credit score and personal score before applying.

Finance if you plan to use the equipment for 3+ years and want to build equity and claim Section 179 tax deductions. Lease if you need to upgrade frequently (every 2-3 years) or want lower monthly payments. Over a 5-year term, leasing typically costs 20-30% more than financing the same equipment because you do not own the asset at the end.

Online lenders like National Funding approve applications in 24 hours and can fund the next business day. Bank of America typically releases funds within 10 business days of approval. SBA 7(a) equipment loans take 2-4 weeks from application to funding. The fastest approvals go to applicants who have all financial documents ready.

Yes. National Funding requires just 6 months in business and a credit score of 600. You will pay higher rates than established businesses, and some lenders may require 1-2 advance payments instead of zero down. See our guide to business loans for startups for additional options.

Yes. Under Section 179, you can deduct up to $2,560,000 of qualifying equipment placed in service during the 2026 tax year. The interest you pay on the equipment loan is also deductible as a business expense. You can claim the deduction even if you financed 100% of the purchase price.

SBA 7(a) loans allow up to $5 million for equipment purchases with terms up to 10 years. JR Capital offers equipment financing up to $10 million, and First Citizens Bank goes to $3 million. For most small businesses, equipment loans range from $5,000 to $750,000 depending on the lender.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA 7(a) Loan Terms, Conditions, and Eligibility

- Current SBA Loan Interest Rates (February 2026) - Lendio

- SBA Loan Rates 2026 - NerdWallet

- Best Equipment Financing and Loans of 2026 - NerdWallet

- Bank of America Equipment Loans

- Best Equipment Business Loans (February 2026) - Bankrate

- 2026 Section 179 Tax Deduction Limits - Section179.org

- IRS Form 4562 Instructions (Depreciation and Amortization)

- SBA 7(a) Fees for Fiscal Year 2026 - NerdWallet

- Equipment Financing Rates in 2026-2026 - Crestmont Capital

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Equipment Financing for Small Business in 2026

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment