SBA EIDL Loan: Current Status, Eligibility and How to Apply in 2026

The COVID-19 EIDL program closed January 1, 2022. Over 1.3 million borrowers are in default. Learn your repayment options, rates, and alternatives for 2026.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What You Need to Know About EIDL Loans in 2026

- How the Two EIDL Programs Work

- Who Qualifies for an EIDL Loan

- How to Apply for an Active Disaster EIDL

- What an EIDL Loan Actually Costs

- Where to Get Help With Your EIDL

- What to Do If You Do Not Qualify for an EIDL

- 5 Costly Mistakes EIDL Borrowers Make

- FAQ

$0–$2,000,000

Est. Loan Cost

20 minutes

Timeline

4

Total Steps

What You Need to Know About EIDL Loans in 2026

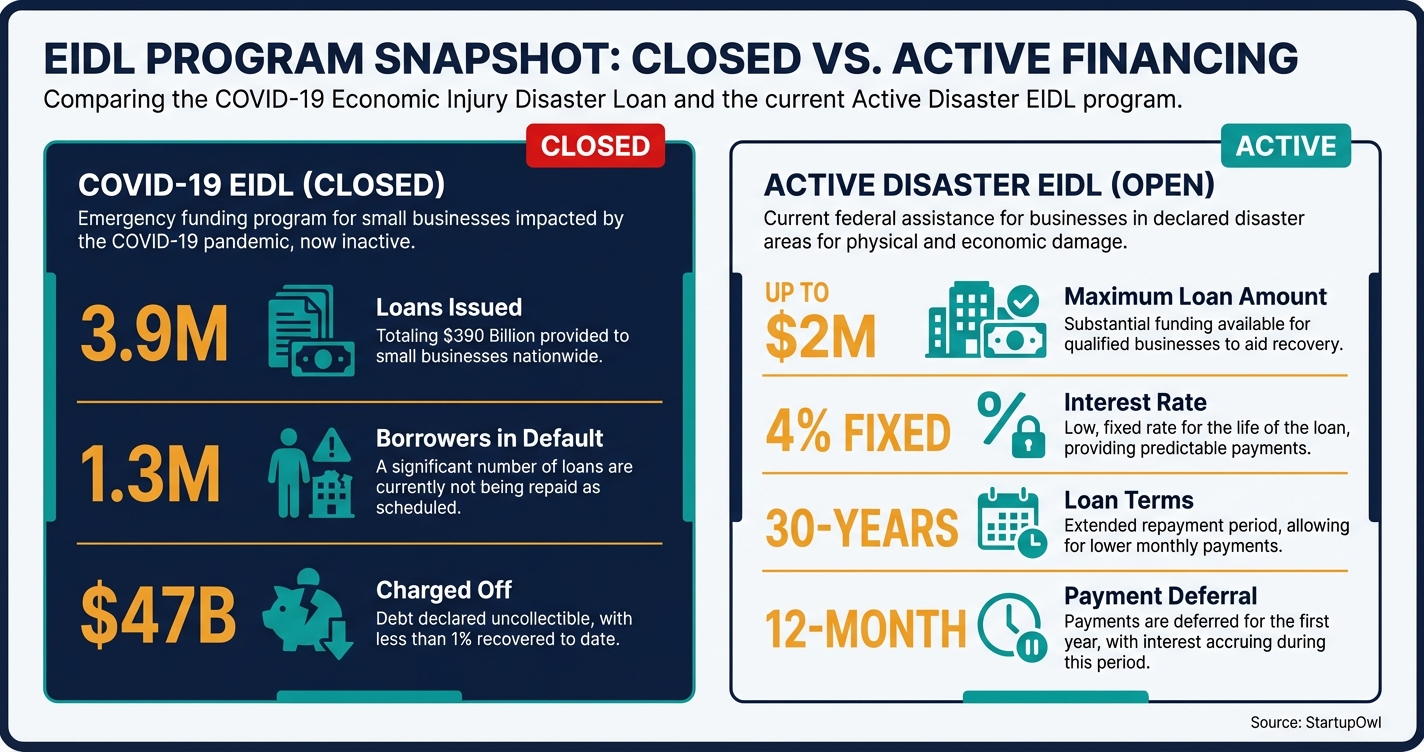

The COVID-19 Economic Injury Disaster Loan program issued approximately 3.9 million loans totaling nearly $390 billion between 2020 and 2022, making it one of the largest federal lending programs in U.S. history. As of January 1, 2022, the SBA stopped accepting new COVID-19 EIDL applications. If you are searching for an EIDL loan in 2026, you are likely in one of two situations.

First, you may already hold a COVID-19 EIDL and need help managing repayment (or dealing with default). Over 1.3 million borrowers are currently in default, and the SBA has charged off more than $47 billion in these loans. Second, your business may have been hit by a recent natural disaster and you are looking at the SBA's still-active disaster EIDL program.

This guide covers both programs in full. You will find current rates, eligibility rules, step-by-step application instructions for active disaster EIDLs, and every repayment and relief option available for existing COVID-19 EIDL borrowers. If you need working capital outside of a disaster context, check out our how to get a business loan guide or our SBA loan guide for active programs.

COVID-19 EIDL Program Is Permanently Closed

The SBA stopped accepting new COVID-19 EIDL applications on January 1, 2022, and stopped processing increase requests and reconsiderations on May 6, 2022. The application portal (covid19relief1.sba.gov) was shut down on May 16, 2022. You cannot apply for a new COVID-19 EIDL. If you need non-disaster financing, explore an SBA 7(a) loan, business line of credit, or SBA microloan instead.

How the Two EIDL Programs Work

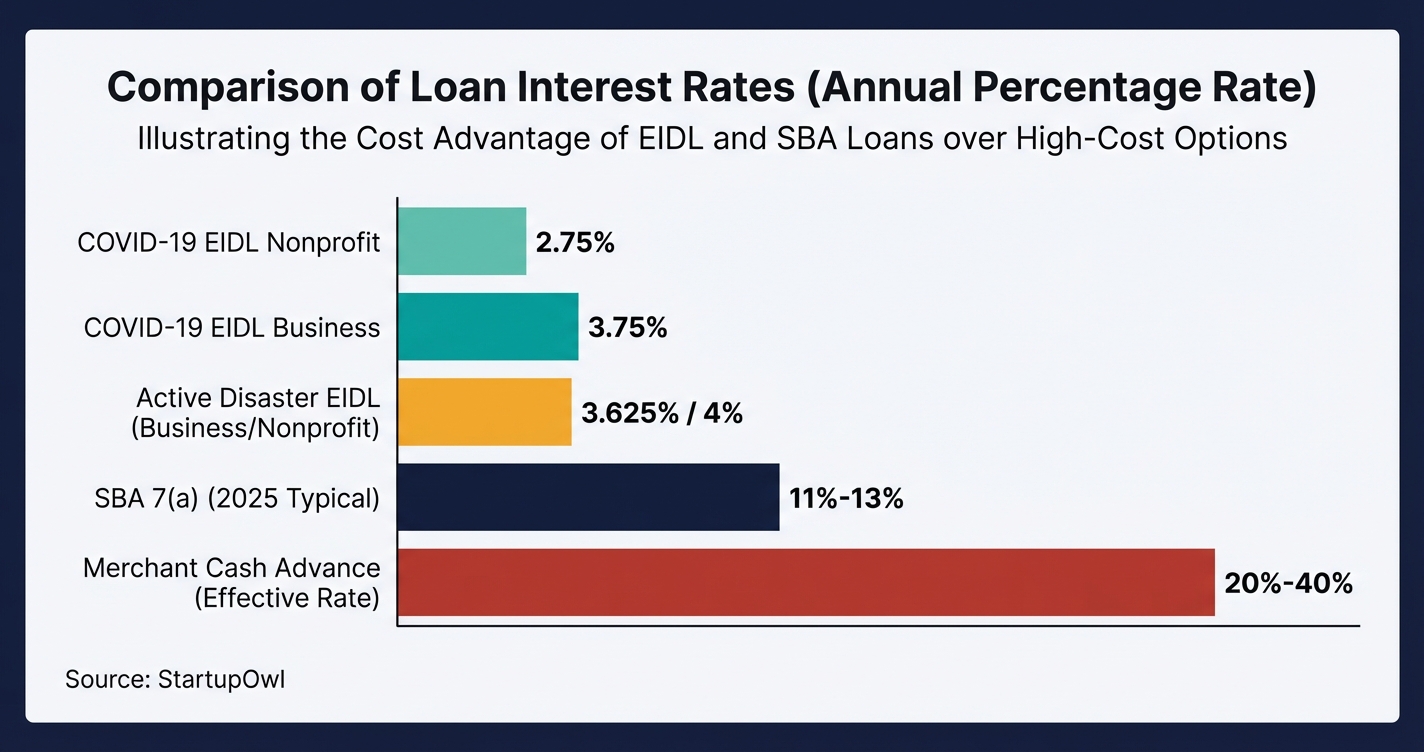

There are two separate Economic Injury Disaster Loan programs, and confusing them is a common mistake. The COVID-19 EIDL was a one-time pandemic response program that provided up to $2 million at a fixed rate of 3.75% for businesses (or 2.75% for nonprofits) over 30 years. It is closed permanently, but nearly 4 million borrowers are still repaying these loans.

The regular disaster EIDL is a standing SBA program that activates whenever the SBA declares a disaster for a specific area. As of 2026, current rates are as low as 4% for businesses and 3.625% for nonprofits, with terms up to 30 years and a maximum of $2 million. Interest does not accrue and payments are not due until 12 months from the date of first disbursement.

Both programs are direct SBA loans (not made through private banks). EIDL funds can be used for working capital (fixed debts, payroll, accounts payable, rent, utilities) but cannot fund business expansion, replace lost profits, or pay dividends. The SBA may request receipts showing at least 80% of funds went toward approved uses.

Who Qualifies for an EIDL Loan

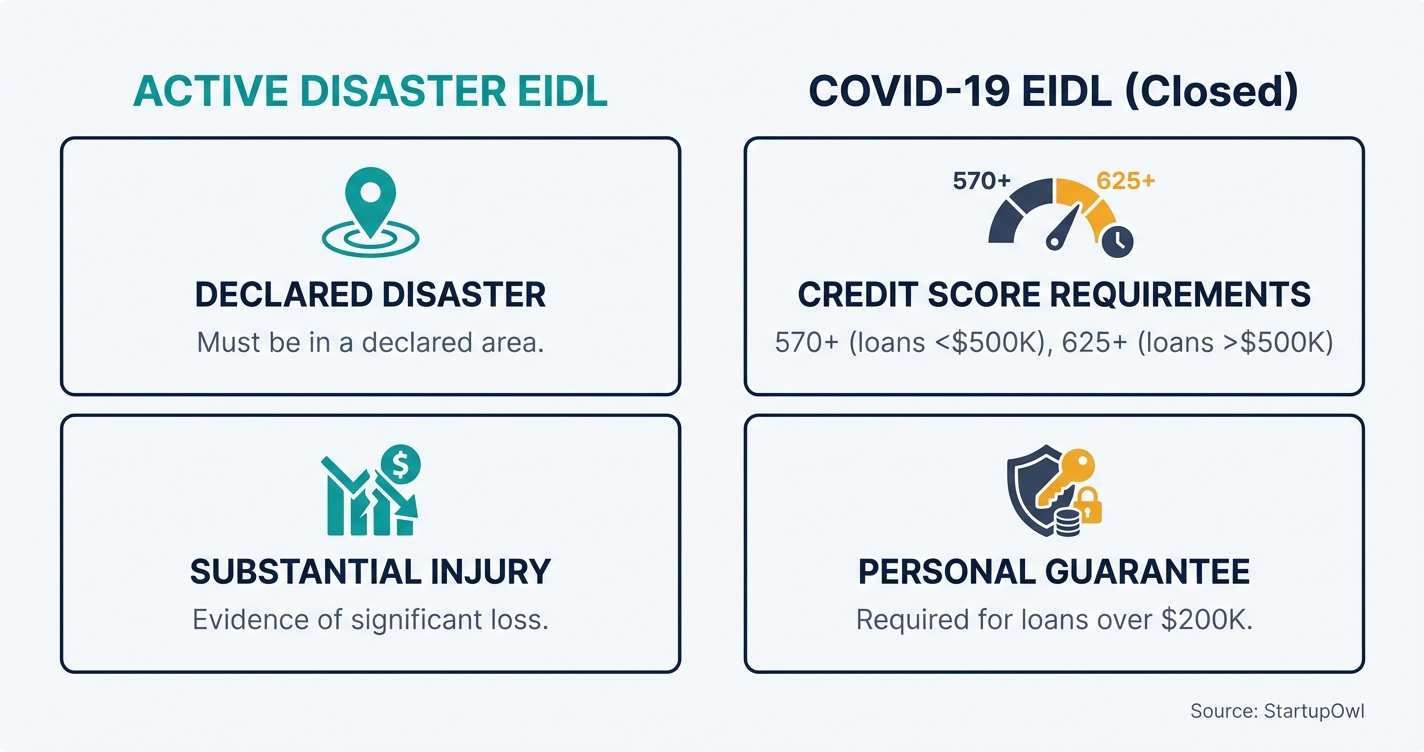

Active Disaster EIDL (Available Now). Your business must be located in a declared disaster area, must have suffered substantial economic injury because of the disaster, and must be unable to obtain credit elsewhere. Eligible entities include small businesses, small agricultural cooperatives, nurseries, and most private nonprofit organizations. Agricultural producers, farmers, and ranchers (except aquaculture) are not eligible.

COVID-19 EIDL (Closed, Historical Reference). When the program was active, applicants needed fewer than 500 employees, must have been in operation before January 31, 2020, and needed a minimum credit score of 570 for loans under $500,000 or 625 for loans above $500,000. A personal guarantee was required for loans exceeding $200,000. Collateral was required for loans greater than $25,000.

For the active disaster program, the SBA will not decline a loan solely for lack of collateral but requires you to pledge whatever collateral is available. Real estate is the preferred collateral. Loans of $200,000 or less do not require your primary residence as collateral if you have other qualifying assets.

How to Apply for an Active Disaster EIDL

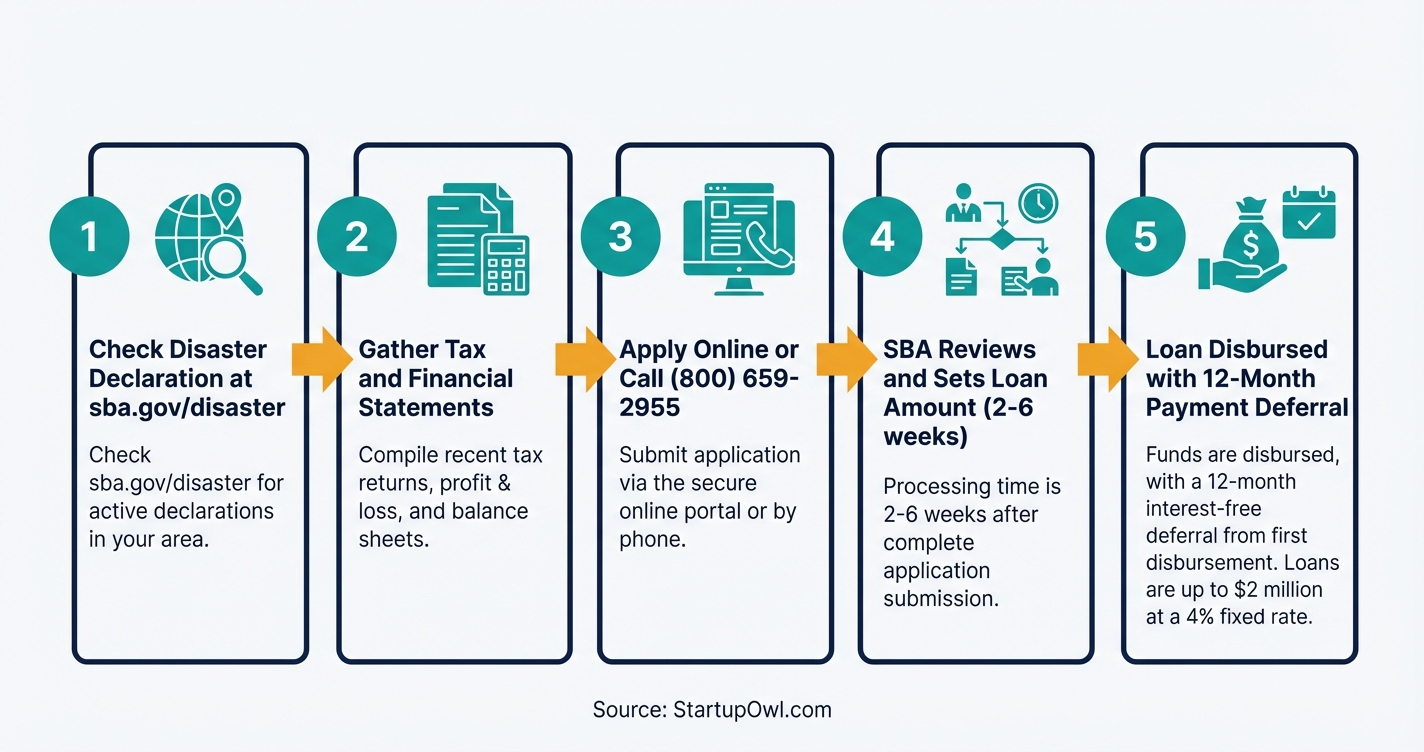

You can only apply for a disaster EIDL when the SBA has issued a formal disaster declaration for your county. Check the SBA Disaster Assistance page for current declarations. Recent declarations have covered storms in California, Oregon, West Virginia, New York, and Florida, among other states.

To apply, visit sba.gov/disaster and submit your application online. You will need your most recent business tax returns, a personal financial statement, and a schedule of liabilities. The SBA sets your loan amount and terms based on your actual financial condition, not a standard formula. You can also call the SBA Customer Service Center at (800) 659-2955 or email [email protected].

Processing typically takes 2-6 weeks after a complete application is submitted. Deadlines are strict: physical damage applications are due roughly 60 days after the declaration, while economic injury applications are typically due 6-9 months later. After the deadline passes, there is generally a 60-day grace period in which the SBA will still accept applications.

What an EIDL Loan Actually Costs

EIDL loans are among the lowest-cost business financing options available from the federal government. There are no application fees, no origination fees, and no prepayment penalties on either the COVID-19 or the active disaster version.

Active disaster EIDL rates (as of 2026): Interest rates are as low as 4% fixed for businesses and 3.625% fixed for nonprofits, with terms up to 30 years. Interest does not accrue for the first 12 months from disbursement. On a $100,000 loan at 4% over 30 years, your monthly payment would be approximately $477.

COVID-19 EIDL rates (historical, for existing borrowers): All COVID-19 EIDLs carry a 3.75% fixed rate for businesses and 2.75% fixed rate for nonprofits. The original deferment was 24-30 months from origination, but interest accrued during deferment. This means your remaining balance is higher than your original loan amount. By comparison, an SBA 7(a) loan currently runs 11%-13% interest, making your EIDL rate extremely favorable if you can stay current.

EIDL Rate Comparison at a Glance

| Type / Provider | Rate | Notes |

|---|---|---|

| COVID-19 EIDL (Businesses) | 3.75% fixed, 30-year term | Program closed Jan 1, 2022. Rate applies to all existing borrowers. |

| COVID-19 EIDL (Nonprofits) | 2.75% fixed, 30-year term | Program closed Jan 1, 2022. Rate applies to all existing nonprofit borrowers. |

| Active Disaster EIDL (Businesses) | Up to 4% fixed, 30-year term | As of 2026 declarations. Rate set per disaster. 12-month payment deferral. |

| Active Disaster EIDL (Nonprofits) | 3.625% fixed, 30-year term | As of 2026 declarations. 12-month interest-free deferral from first disbursement. |

| SBA 7(a) Loan (for comparison) | 11%-13% variable (2026 typical) | Active program. Prime + 2.75% to 6% depending on loan size and term. |

| Treasury Collection Surcharge | 30% added to balance | Applied to defaulted COVID-19 EIDLs referred to U.S. Treasury. |

Where to Get Help With Your EIDL

Because EIDLs are direct SBA loans (not made through private banks), your primary contact points are all within the federal government. Here are the key resources.

- SBA Disaster Assistance Portal (sba.gov/disaster) is for new disaster EIDL applications. This is where you apply online when your county has an active declaration.

- MySBA Loan Portal (sba.gov/manage-your-eidl) is for existing COVID-19 EIDL borrowers. You can check your balance, make payments, request servicing actions, and submit hardship accommodation requests here.

- COVID EIDL Servicing Center in Fort Worth, TX can be reached by emailing [email protected] or [email protected]. This team handles change of ownership requests, collateral releases, subordination requests, and hardship applications.

- SBA Customer Service Center at (800) 659-2955 handles general inquiries and disaster loan application assistance. For TTY, dial 7-1-1.

- SBA Secure Payment Portal at (833) 853-5638 handles phone-based payments on existing loans.

If you need working capital outside of a disaster situation, consider an SBA 7(a) loan through a private lender, or check out working capital loans and business lines of credit for faster funding.

What to Do If You Do Not Qualify for an EIDL

If your business is not in a declared disaster area and you cannot access the active EIDL program, you still have options. For low-cost government-backed financing, the SBA 7(a) loan program provides up to $5 million at rates of 11%-13% (as of early 2026). You will typically need a personal credit score of 680+ and at least 2 years in business.

If you are a startup or a business with a shorter track record, an SBA microloan offers up to $50,000 at 8%-13%. For even smaller needs, microloans for small business through nonprofit intermediaries can fund amounts as low as $500. If you need cash fast (within days rather than weeks), invoice factoring or a merchant cash advance can provide working capital, but expect effective rates of 20%-40% or higher.

Do not overlook free money options. Small business grants from federal, state, and private sources do not require repayment. And if you are building your business foundation, building business credit and setting up proper accounting software will strengthen your financing applications across the board.

5 Costly Mistakes EIDL Borrowers Make

1. Ignoring SBA collection notices. Every month you wait, interest accrues and you move closer to Treasury referral. At 120 days delinquent, your loan is automatically referred to the Treasury Offset Program, which adds a 30% collection fee to your outstanding balance. On a $150,000 loan, that is an extra $45,000 you suddenly owe.

2. Assuming your COVID-19 EIDL will be forgiven. Unlike PPP loans, EIDLs were never designed to be forgiven. Congress has not passed any EIDL forgiveness legislation, and the SBA has stated clearly that "these loans are not forgivable and must be repaid." Do not wait for a bailout that is not coming.

3. Paying a third-party company to "settle" your SBA debt. The SBA's Offer in Compromise program technically exists, but it has not approved any compromises for COVID-19 EIDL borrowers as of early 2026. Any company charging you fees to settle your EIDL is taking your money for a service that has a near-zero success rate.

4. Selling business assets without SBA authorization. If your EIDL is secured by a UCC filing on your business assets, you are contractually required to get SBA approval before transferring or selling those assets. Doing so without permission can turn a debt problem into potential federal fraud.

5. Not understanding your personal guarantee status. COVID-19 EIDLs under $200,000 generally required no personal guarantee, which means the SBA's collection ability against your personal assets is limited to business assets only. If your loan was over $200,000, you signed a personal guarantee, and the Treasury can garnish your wages (up to 15%), seize your tax refunds, and offset your Social Security benefits. Know which category you fall into before deciding on a strategy.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor, CPA, or attorney before making borrowing or repayment decisions. EIDL program details and interest rates reflect publicly available SBA data as of February 2026 and may change without notice. If you are in default on an EIDL, consult an attorney experienced with SBA debt before taking any action.

Step-by-Step Process

- 1

Determine which EIDL program applies to your situation

You need to understand the difference between two programs. The COVID-19 EIDL is permanently closed and only affects existing borrowers managing repayment. The regular disaster EIDL remains active and available when the SBA issues a disaster declaration for your area.

If you already have a COVID-19 EIDL, skip ahead to Step 3 for repayment strategies. If your business was recently hit by a federally declared disaster (floods, storms, drought, wildfire), proceed to Step 2 to apply for an active disaster EIDL.

Tips

- Check the SBA disaster declarations page to see if your area has an active declaration before applying.

- Regular disaster EIDLs are only available when the SBA has formally declared a disaster for your specific county.

Common Mistakes

- Confusing the closed COVID-19 EIDL with the active disaster EIDL program and assuming no disaster loans are available.

- 2

Apply for an active disaster EIDL through the SBA portal

If you are in a declared disaster area, apply online at sba.gov/disaster. You can borrow up to $2 million at interest rates as low as 4% for businesses and 3.625% for nonprofits, with terms up to 30 years, as of 2026.

Interest does not accrue and payments are not due until 12 months from the date of first disbursement. You will need to provide your business tax returns, a personal financial statement, and a schedule of liabilities. Collateral is required for loans over $50,000.

Tips

- Apply as early as possible after a disaster declaration since deadlines are strict (typically 60 days for physical damage, longer for economic injury).

- You do not need to wait for an insurance settlement before applying for an SBA disaster loan.

- Call the SBA Customer Service Center at (800) 659-2955 if you need help with the application.

Common Mistakes

- Missing the economic injury application deadline, which is typically 6-9 months after the disaster declaration.

- Attempting to use EIDL funds for business expansion or replacing lost profits, which is not allowed.

- 3

Log into MySBA Loan Portal to review your existing COVID-19 EIDL

If you already hold a COVID-19 EIDL, your first action is to log into the MySBA Loan Portal and check your current loan status, payment history, and whether your account has been flagged for delinquency. The SBA has documented widespread processing errors where payments made on time were never recorded, resulting in wrongful default referrals.

Verify your monthly payment obligation. Payments began 30 months from your disbursement date. If interest accrued during deferment (which it did), your final balloon payment at maturity will be larger than your original principal.

Tips

- Download and save all payment confirmation records as proof in case the SBA misapplies your payments.

- Email [email protected] with your loan number and a description of any discrepancy you find.

Common Mistakes

- Ignoring SBA notices and letting your loan drift past 120 days delinquent, which triggers automatic Treasury referral and a 30% surcharge.

- 4

Request hardship relief or explore repayment alternatives before Treasury referral

The SBA's Hardship Accommodation Plan officially ended on March 19, 2026, but some borrowers may still qualify for a one-time 50% payment reduction for six months. To request this, submit a written explanation of your financial difficulty through the MySBA Loan Portal or email [email protected].

If you cannot resume full payments and your loan has not yet been referred to Treasury, act immediately. Once referred, the U.S. Treasury adds a 30% collection fee to your outstanding balance and can garnish up to 15% of your disposable income, intercept tax refunds, and offset Social Security benefits without a court order. Consider consulting a bankruptcy attorney experienced with SBA debt, particularly about Subchapter V bankruptcy, which can restructure EIDL debt while keeping your business open.

$0 for SBA hardship request; $3,000-$10,000+ for bankruptcy attorney 2-4 weeks for SBA hardship response; 3-6 months for bankruptcy proceedings SBA.govTips

- Contact the SBA disaster loan servicing center at 1-800-659-2955 proactively if you are falling behind on payments.

- Gather documentation of your financial hardship (bank statements, profit-and-loss statements) before requesting accommodation.

- Do not sell or transfer business assets without SBA authorization, as this can escalate a debt problem into a federal fraud issue.

Common Mistakes

- Waiting until after Treasury referral to seek help, which adds 30% to your balance and severely limits your options.

- Paying a third-party company to 'settle' your SBA debt when the SBA's own Offer in Compromise program has approved no COVID EIDL compromises as of 2026.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| COVID-19 EIDL Interest Rate (Businesses) | 3.75% fixed | Historical rate for all COVID-19 EIDLs issued 2020-2022. Program closed. |

| COVID-19 EIDL Interest Rate (Nonprofits) | 2.75% fixed | Historical rate for all COVID-19 EIDLs issued to nonprofits. Program closed. |

| Active Disaster EIDL Interest Rate (Businesses) | Up to 4% fixed | Current rate as of 2026 for businesses that cannot obtain credit elsewhere. |

| Active Disaster EIDL Interest Rate (Nonprofits) | 3.625% fixed | Current rate as of 2026 for private nonprofit organizations. |

| Application and Origination Fees | $0 | No fees for either COVID-19 or disaster EIDL programs. |

| Prepayment Penalty | $0 | No penalty for early repayment on any EIDL. |

| Treasury Collection Surcharge (if defaulted) | 30% of outstanding balance | Added automatically once loan is referred to U.S. Treasury for collection. |

Frequently Asked Questions

You cannot apply for a COVID-19 EIDL because that program closed on January 1, 2022. However, the regular disaster EIDL program is active and available if the SBA has declared a disaster in your area. Check sba.gov/disaster for current declarations. If your area is covered, you can borrow up to $2 million at rates as low as 4% fixed.

No. Unlike PPP loans, COVID-19 EIDLs were structured as repayable 30-year loans, not forgivable grants. The SBA has stated these loans must be repaid, and Congress has passed no forgiveness legislation as of 2026. Your best option if you cannot pay is to contact the SBA at 1-800-659-2955 to discuss repayment alternatives or consult a bankruptcy attorney about Subchapter V restructuring.

At 30 days past due, the SBA sends collection notices. At 90 days, the SBA issues a formal default notice and can accelerate the entire loan balance. At 120 days, your loan is referred to the Treasury Offset Program, which adds a 30% collection fee to your balance. Treasury can then garnish 15% of your disposable income, intercept your tax refunds, and offset your Social Security benefits, all without a court order.

COVID-19 EIDLs carry a 3.75% fixed rate for businesses and 2.75% for nonprofits over 30 years. Active disaster EIDLs (as of 2026) are as low as 4% for businesses and 3.625% for nonprofits, also with 30-year terms. Both programs charge zero application fees, zero origination fees, and zero prepayment penalties.

For COVID-19 EIDLs under $200,000, no personal guarantee was required. This means the SBA can only pursue your business assets, not your personal property, bank accounts, or wages. For loans over $200,000, you signed a personal guarantee, which gives the Treasury the power to garnish wages, seize tax refunds, and offset Social Security without a court order.

Contact the SBA immediately at [email protected] or through the MySBA Loan Portal. You may qualify for a one-time 50% payment reduction for six months. Other options include the SBA's Offer in Compromise (though none have been approved for COVID EIDLs), refinancing with a private lender, or Subchapter V bankruptcy, which can restructure SBA debt into affordable payments over 3-5 years while keeping your business operating.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor, CPA, or attorney before making borrowing or repayment decisions. APR ranges and program details reflect publicly available SBA data as of 2026 and may change without notice. EIDL loan terms are set by the SBA and the U.S. federal government.

Sources & References

- About COVID-19 EIDL (SBA.gov)

- Economic Injury Disaster Loans (SBA.gov)

- Manage Your EIDL (SBA.gov)

- SBA Disaster Assistance (SBA.gov)

- SBA OIG Report 25-23: Collection Efforts on Delinquent COVID-19 EIDLs

- EIDL Loan Repayment in 2026 (Merchant Maverick)

- SBA Disaster Loan Interest Rates (Congressional Research Service)

- Current SBA Loan Rates (Nav.com)

- SBA Offers Disaster Assistance to California (SBA.gov, Feb 2026)

- SBA Loan Default and Forgiveness Explained (Nav.com)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about SBA EIDL Loan

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment