Business Emergency Fund: How Much to Save and Where to Keep It

Build a business emergency fund with 3-6 months of expenses. Compare high-yield savings accounts earning up to 4% APY and protect your reserves with FDIC coverage.

In This Article

- Key Takeaways

- Step-by-Step

- What a Business Emergency Fund Is and Why You Need One

- How Much You Should Save (With Specific Targets)

- How to Build Your Business Emergency Fund Step by Step

- Where to Keep Your Emergency Fund (Best Accounts for 2026)

- Emergency Funding Alternatives If Your Reserve Falls Short

- What to Do If You Cannot Save Right Now

- 5 Emergency Fund Mistakes That Cost Real Money

- FAQ

Free

Est. Loan Cost

30 minutes

Timeline

5

Total Steps

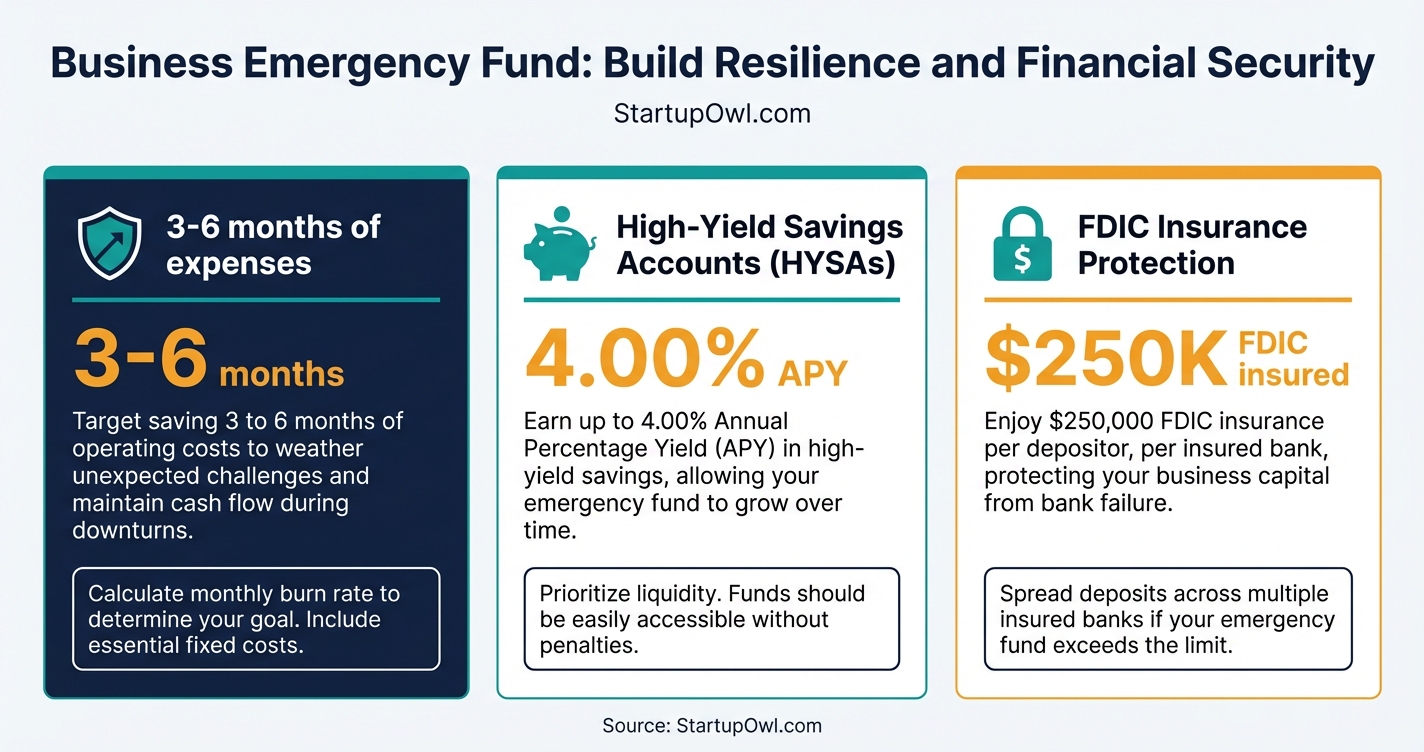

One lost contract, a broken HVAC system, or a cyberattack can drain your operating account in days. The standard recommendation is to hold 3 to 6 months of operating expenses in a separate business emergency fund, yet most small businesses operate with less than 2 weeks of cash reserves.

The good news: you do not need six figures on day one. With high-yield business savings accounts paying up to 4.00% APY as of early 2026, even a modest reserve earns meaningful interest while staying liquid and FDIC-insured.

This guide covers exactly how much you should save, the best places to park your cash, and what to do if you need emergency capital before your fund is fully built. If you are also exploring outside financing options, see our full how to get a business loan guide.

What a Business Emergency Fund Is and Why You Need One

A business emergency fund is a dedicated cash reserve held in a liquid, interest-bearing account that you tap only during genuine financial emergencies. It covers events like declining revenues from lost clients, equipment breakdowns, natural disasters, cyberattacks, legal disputes, or supply chain disruptions.

Without a reserve, you are forced into high-cost emergency borrowing. A business line of credit from an online lender like Bluevine can carry an effective APR of 20% to 50%, and a merchant cash advance can cost even more. Your own savings account costs you nothing in interest and keeps you in full control of your business decisions.

Beyond crisis protection, a well-funded reserve gives you strategic flexibility. If a product unexpectedly goes viral or a competitor closes, you can ramp up spending without waiting for loan approval. Cash in the bank also strengthens your negotiating position with suppliers, landlords, and lenders.

How Much You Should Save (With Specific Targets)

The most widely recommended benchmark is 3 to 6 months of operating expenses. If your monthly overhead is $5,000 (rent, payroll, utilities, insurance, software), that translates to $15,000 to $30,000 in your emergency fund. If your overhead is $10,000/month, aim for $30,000 to $60,000.

Businesses with higher risk profiles should target 6 to 12 months of expenses. This includes seasonal businesses (tourism, landscaping, holiday retail), companies dependent on a single client for more than 30% of revenue, and startups in their first 3 years. An alternative rule of thumb is 10% of annual revenue, though the expense-based calculation is more precise.

Do not include revenue in your calculation. Focus exclusively on your fixed and semi-variable costs: compensation, rent or lease payments, utilities, subscription software, insurance premiums, and minimum loan payments. Pull your last 12 months of bank statements or run a profit-and-loss report from your accounting software to get an accurate number.

How to Build Your Business Emergency Fund Step by Step

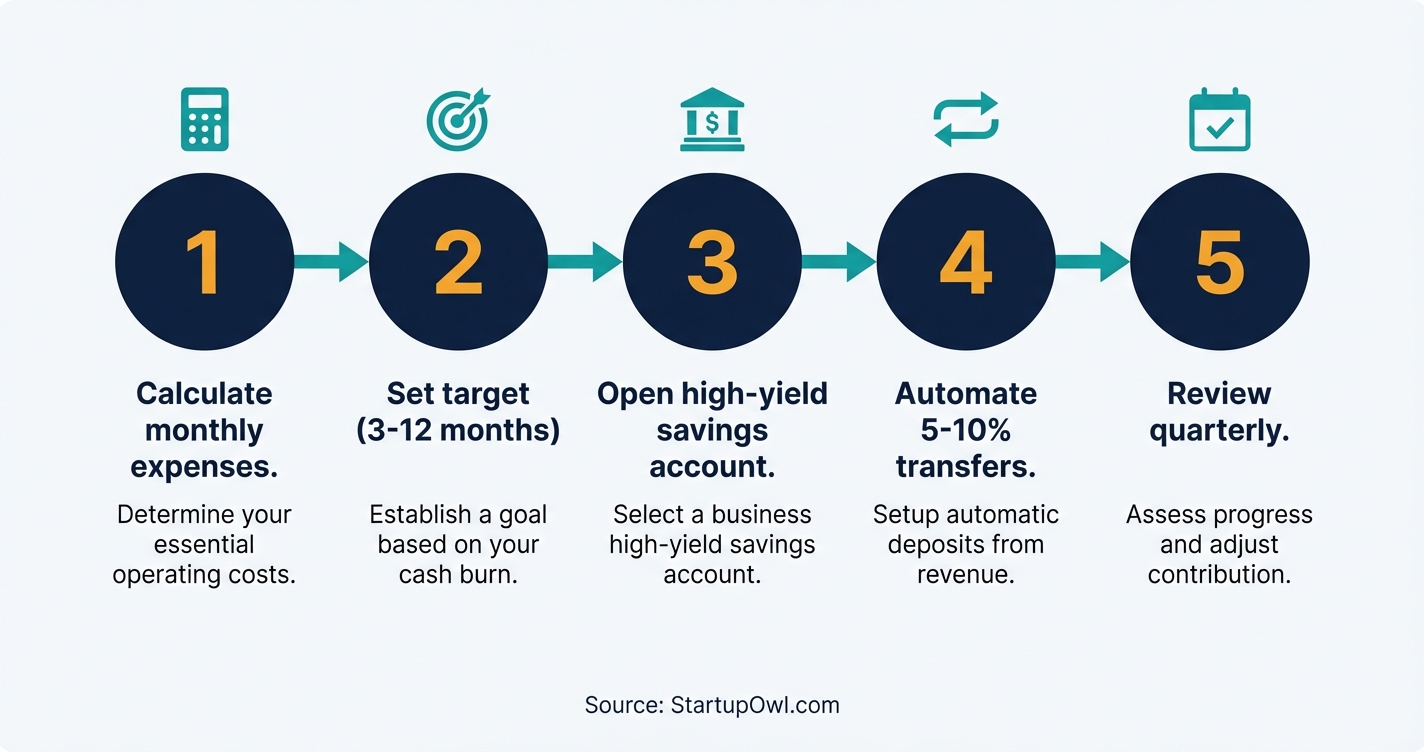

Building a business emergency fund is not about finding a lump sum overnight. It is about setting up a system that grows your reserve automatically. Follow these steps to go from zero to a fully funded safety net.

Step 1. Calculate your total monthly operating expenses using your bank statements or accounting reports. Every recurring cost counts.

Step 2. Multiply that number by your target months (3 for low-risk, 6-12 for high-risk) to set your savings goal. Write this number down and post it where you will see it.

Step 3. Open a separate high-yield business savings account (details in the next section). Keep emergency funds in a different institution from your operating account to avoid casual dipping.

Step 4. Set up automatic transfers on the same day each month. Start with 5-10% of gross revenue. On $20,000/month in revenue, that is $1,000 to $2,000 transferred automatically each month.

Step 5. Review your fund balance and target quarterly. As your business grows, your expenses grow, and your target must grow with them. After any withdrawal, create a 90-day replenishment plan.

At $1,500/month in automatic transfers, you will build a $18,000 reserve (enough for 3 months at $6,000/month overhead) in just 12 months. If you also work on building your business credit, you will have both cash reserves and credit access for true resilience.

Where to Keep Your Emergency Fund (Best Accounts for 2026)

Your emergency fund must be liquid (accessible within 1-2 business days), FDIC-insured, and earning a competitive yield. The worst place for it is your operating checking account at 0.01% APY. The best options as of early 2026 are high-yield business savings accounts and business money market accounts.

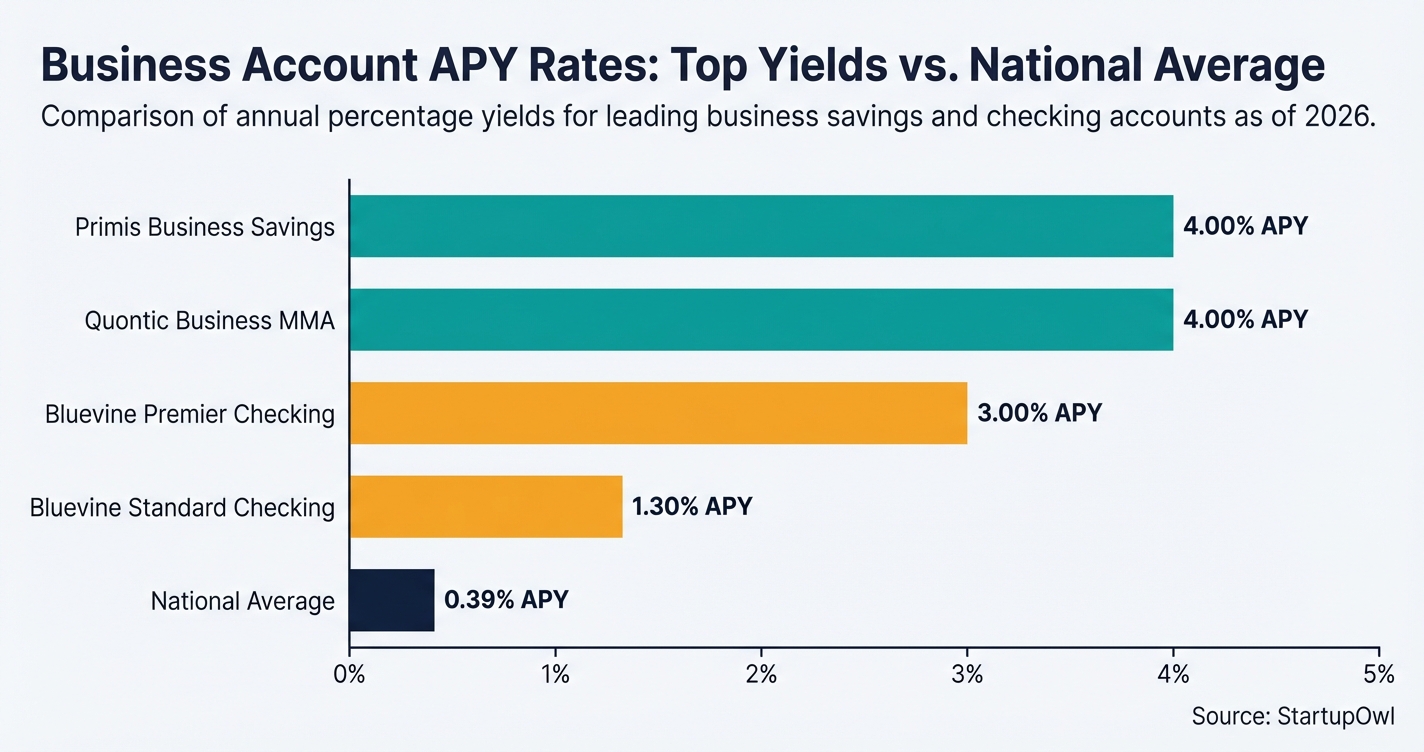

High-yield business savings accounts currently pay between 3.85% and 4.00% APY at top online banks. On a $30,000 emergency fund, that earns you roughly $1,155 to $1,200/year in passive interest, compared to $3 at a big-bank checking rate. Business money market accounts offer similar yields (up to 4.00% APY at banks like Quontic) and add check-writing or debit card access for faster withdrawals during a real emergency.

The Bluevine Business Checking account pays 1.3% APY on the Standard plan (balances up to $250,000) and up to 3.0% APY on the Premier plan (balances up to $3 million), making it a hybrid option if you want checking-level access with above-average interest. However, pure savings accounts from Primis Bank (4.00% APY, $1 minimum, no monthly fee) will typically earn more for dedicated reserves.

All deposits should be FDIC-insured. The standard limit is $250,000 per depositor, per bank, per ownership category. If your combined balances at one institution exceed that threshold, consider an Insured Cash Sweep (ICS) account or spread deposits across multiple banks. Bluevine offers up to $3 million in FDIC coverage through its program banks.

Business Emergency Fund Account Comparison (February 2026)

| Type / Provider | Rate | Notes |

|---|---|---|

| Primis Business Savings | 4.00% APY | $1 minimum to open, no monthly fees, no minimum balance for APY, FDIC-insured, online only |

| Quontic Business Money Market | Up to 4.00% APY | $100 minimum opening deposit, debit card and check access, FDIC-insured |

| Bluevine Standard Business Checking | 1.30% APY | No monthly fees, $0 minimum, must meet monthly activity goal, FDIC-insured up to $3M via ICS |

| Bluevine Premier Business Checking | 3.00% APY | $95/month fee (waived with $100K+ balance and $5K card spend), up to $3M FDIC, on balances up to $3M |

| National average savings rate | 0.39% APY | FDIC-reported average as of early 2026; use as a baseline for comparison |

Keep Your Emergency Fund in a Separate Bank

Parking your emergency fund at a different institution from your operating account serves two purposes. First, it removes the temptation to "borrow" from your reserve for routine expenses. Second, if your primary bank experiences an outage or failure, you still have immediate access to emergency cash at the backup bank. This dual-bank strategy also doubles your FDIC coverage to $500,000 across two institutions.

Emergency Funding Alternatives If Your Reserve Falls Short

Even with the best savings plan, emergencies sometimes arrive before your fund is fully built. Here are the fastest backup options, ranked from cheapest to most expensive.

- Business line of credit (set up in advance). A business line of credit from Bluevine offers up to $250,000 with a minimum credit score of 625, at least 12 months in business, and $10,000/month in revenue. Repayment terms are 6 to 12 months. Effective APR ranges from roughly 20% to 50%, so this is expensive compared to savings but far cheaper than a merchant cash advance. Apply before you need it; approval takes as little as 5 minutes online.

- SBA Microloan. The SBA Microloan program offers up to $50,000 at rates typically between 8% and 13%. It is the cheapest borrowing option for most small businesses, but funding takes 30-90 days, so it is not ideal for same-week emergencies.

- Business credit card. A business credit card with a 0% intro APR offer can bridge a short-term gap interest-free for 12-15 months. After the intro period, rates jump to 18-26% APR.

- Invoice factoring. If you have outstanding invoices, invoice factoring converts them to cash within 24-48 hours at a cost of roughly 1-5% per month of the invoice value.

The single best strategy is to have both a growing emergency fund and a pre-approved line of credit. The fund covers small disruptions interest-free, and the credit line backstops larger events while you rebuild.

What to Do If You Cannot Save Right Now

If your cash flow is too tight to save $1,000/month, start smaller. Even $200/month builds to $2,400 in a year, enough to cover one payroll cycle or a critical equipment repair. The goal is consistency, not size.

Consider these accelerators to jumpstart your fund:

- Direct one-time windfalls (tax refunds, client overpayments, rebates) straight into the emergency account.

- Cut one discretionary subscription or vendor contract and redirect the savings.

- Apply for a small business grant to cover a specific capital expense, then redirect the cash you would have spent into your reserve.

- If you are pre-revenue, explore pre-seed funding or microloans for small business to cover launch costs so you can keep personal savings as your emergency backstop.

The biggest mistake is waiting until you "can afford it." Businesses that start with $100/month build the habit that carries them to a fully funded reserve. Businesses that wait for the perfect time rarely start at all.

5 Emergency Fund Mistakes That Cost Real Money

1. Keeping the fund in your operating checking account. If your emergency cash sits at 0.01% APY mixed with your daily spending, you will spend it. A $30,000 fund at 0.01% earns $3/year. The same amount at 4.00% APY earns $1,200. Over 5 years, that is nearly $6,000 in lost interest.

2. Setting a target and never adjusting it. If you set your target at $15,000 when your overhead was $5,000/month but your expenses have since grown to $8,000/month, your "3-month fund" now covers less than 2 months. Review quarterly.

3. Using the emergency fund for non-emergencies. A slow sales month is not an emergency. A new hire is not an emergency. A broken delivery truck or a ransomware attack is an emergency. Write a short "withdrawal policy" defining what qualifies.

4. Ignoring FDIC limits. If you hold $300,000 across checking and savings at the same bank under the same ownership category, $50,000 is uninsured. The 2023 failures of Silicon Valley Bank and Signature Bank proved that uninsured deposits can be inaccessible for days or weeks.

5. Not having a replenishment plan. Drawing $10,000 from your fund and then taking 2 years to replace it leaves you exposed. Create a 90-day refill plan every time you make a withdrawal, even if it means temporarily increasing your auto-transfer rate.

Step-by-Step Process

- 1

Calculate your monthly operating expenses

Add up every predictable outflow your business has each month. Include rent, payroll, utilities, software subscriptions, insurance premiums, and loan payments. If your monthly overhead is $5,000, your baseline emergency target is $15,000 to $30,000 (3-6 months).

Factor in seasonal swings. If your revenue drops 40% during slow months, target the higher end of the range or push to 6-12 months of expenses.

Tips

- Pull your last 12 months of bank statements to identify every recurring expense.

- Include business-specific costs like supplies, replacement parts, and contractor payments.

- Use your accounting software's expense report to catch subscriptions you may have forgotten.

Common Mistakes

- Forgetting quarterly expenses like insurance premiums or annual software renewals.

- Using revenue instead of expenses as the baseline, which inflates the target and delays your start.

- 2

Set a realistic savings target and timeline

Start with 3 months of expenses as your first milestone. If your overhead is $8,000/month, aim for $24,000. Businesses with seasonal revenue, a single major client, or high-risk industries should aim for 6-12 months.

An alternative benchmark is 10% of annual revenue, which can work if your margin structure is thin. Set up automatic monthly transfers of 5-10% of your gross revenue to build your fund steadily.

Tips

- Automate transfers on the same day you receive your largest recurring revenue.

- Use a separate sub-account or bank to prevent co-mingling emergency funds with operating cash.

Common Mistakes

- Setting the target too high and never starting because the number feels impossible.

- 3

Open a high-yield business savings or money market account

Your emergency fund should earn interest, not sit at 0.01% APY in a traditional checking account. As of February 2026, the best business savings accounts pay up to 4.00% APY with no monthly fees and low minimums. On a $30,000 balance, that is roughly $1,200/year in passive interest versus $3 at a big-bank checking rate.

Business money market accounts offer similar yields (around 3.65-4.00% APY) with added check-writing or debit card access, which can be useful during an actual emergency. Look for FDIC-insured accounts with no transaction penalties for withdrawals.

Tips

- Compare at least 3 accounts before opening. Rates vary by hundreds of dollars annually.

- Choose an online bank for higher APY; online-only banks consistently beat brick-and-mortar rates.

- Confirm the account is FDIC-insured (not just the parent company) before depositing.

Common Mistakes

- Picking an account with a high promotional rate that drops after 6 months.

- Ignoring transaction limits on money market accounts, which typically cap at 6 withdrawals per month.

- 4

Verify your FDIC coverage and consider Insured Cash Sweep

Standard FDIC insurance covers up to $250,000 per depositor, per insured bank, per ownership category. If your emergency fund plus operating deposits exceed that threshold at one bank, the overage is uninsured. The 2023 bank failures proved that uninsured deposits can be frozen for weeks.

An Insured Cash Sweep (ICS) account distributes your deposits across a network of FDIC-insured banks behind the scenes, extending your coverage to $3 million or more. Bluevine, for example, offers up to $3 million in FDIC coverage through its program banks. You manage one account while getting multi-bank protection.

Tips

- Use the FDIC's free Electronic Deposit Insurance Estimator (EDIE) tool at fdic.gov to check your coverage.

- LLCs and corporations get separate FDIC coverage from their owners' personal accounts at the same bank.

Common Mistakes

- Assuming sole proprietor business accounts are covered separately from personal accounts (they are not).

- 5

Review and adjust your fund every quarter

Your emergency fund is a living number, not a one-time project. Review it every quarter alongside your business accounting setup. If your monthly overhead has grown from $5,000 to $8,000, your 3-month reserve needs to jump from $15,000 to $24,000.

After each withdrawal, create a replenishment plan within 30 days. Treat the fund like a mandatory business expense, not a discretionary line item. Businesses that fail to replenish after an emergency draw are significantly more vulnerable to the next disruption.

Tips

- Add a recurring quarterly calendar reminder to recalculate your target and check the balance.

- If you draw from the fund, increase your monthly auto-transfer temporarily to rebuild faster.

Common Mistakes

- Setting it and forgetting it; a fund that was adequate at launch may cover only 6 weeks two years later.

Frequently Asked Questions

The standard recommendation is 3 to 6 months of operating expenses. If your monthly overhead is $5,000, aim for $15,000 to $30,000. Seasonal businesses or those relying on a single large client should target 6 to 12 months of expenses for additional security.

A high-yield business savings account is the best option for most businesses. As of February 2026, top accounts like Primis Business Savings pay 4.00% APY with no monthly fees, no minimum balance, and full FDIC insurance. Business money market accounts at banks like Quontic offer similar rates with added check-writing access.

No. Money you set aside in a savings account is not a tax-deductible expense because it is still your asset. However, the interest you earn on the account is taxable income that you must report. Consult a CPA for guidance on how to handle emergency fund interest on your business tax return.

A line of credit is a useful backup, but it should not replace savings. A business line of credit from Bluevine carries an effective APR of 20% to 50%, meaning a $10,000 draw could cost you $2,000 to $5,000 in interest. Your own savings costs $0 in interest and actually earns you money. The best approach is to have both.

At $1,500/month in automatic transfers, you will reach a $18,000 reserve (3 months at $6,000/month overhead) in 12 months. Starting at $500/month, the same target takes 3 years. Accelerate the timeline by directing tax refunds, client windfalls, and cost savings directly into the fund.

FDIC insurance covers up to $250,000 per depositor, per bank, per ownership category. If your fund exceeds that, spread deposits across multiple FDIC-insured banks or use an Insured Cash Sweep (ICS) account that automatically distributes your funds across a bank network. Bluevine offers up to $3 million in FDIC coverage through ICS.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- SBA.gov - Manage Your Finances

- FDIC - Deposit Insurance FAQs

- FDIC - Your Insured Deposits

- Primis Bank - Business Savings Account

- Bluevine - Business Line of Credit

- Bluevine - Business Checking Interest Rate

- NerdWallet - Best High-Yield Savings Accounts (Feb 2026)

- NerdWallet - Best Money Market Accounts (March 2026)

- NerdWallet - FDIC Insurance for Business Accounts

- Bankrate - Best Business Lines of Credit (Feb 2026)

- AdvancePoint Capital - Bluevine Line of Credit Review 2026

- WalletHub - Best Bank Accounts for Small Businesses (Feb 2026)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Business Emergency Fund

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment