Revenue-Based Financing, How It Works and Whether It Is Right for Your Business

Revenue-based financing costs 1.1x to 1.5x in factor rates with 5-15% revenue share. Learn eligibility, top providers, and whether RBF fits your business.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Revenue-Based Financing Is and When to Use It

- Who Qualifies for Revenue-Based Financing

- How to Apply for Revenue-Based Financing

- What Revenue-Based Financing Actually Costs

- The Providers We Actually Recommend

- What to Do If You Do Not Qualify for RBF

- 5 Costly Mistakes to Avoid with Revenue-Based Financing

- FAQ

$1,000–$500,000

Est. Loan Cost

48 hours

Timeline

5

Total Steps

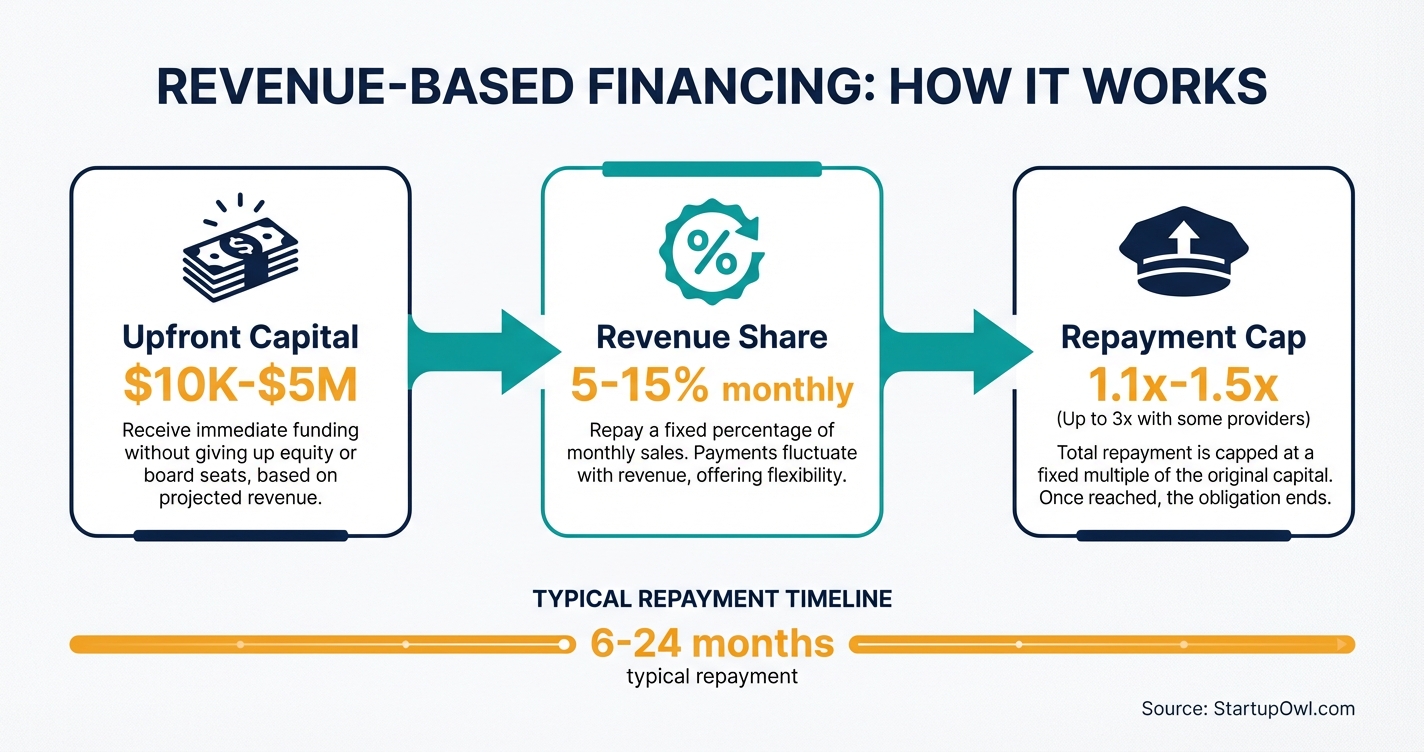

Revenue-based financing gives you upfront capital in exchange for a fixed percentage of your future monthly revenue, typically 5% to 15%, until you repay a predetermined cap. That cap usually runs 1.1x to 1.5x your original funding amount, though some providers go as high as 3x. Unlike a traditional loan, your payments flex with your sales volume (higher in strong months, lower in slow ones) and you keep full ownership of your business. When you are ready to compare actual providers, our tested ranking of revenue based financing companies shows what each really costs.

The RBF market grew from $5.78 billion in 2024 to an estimated $9.8 billion in 2026, according to industry research. For SaaS companies, e-commerce brands, and subscription businesses with steady revenue, RBF fills the gap between expensive equity rounds and hard-to-qualify-for bank loans.

This guide walks you through exactly how revenue-based financing works, what it costs, who qualifies, and the mistakes that can make it far more expensive than you expect. If you are exploring all your options, check out our full guide to how to get a business loan or our comparison of the best small business loans.

What Revenue-Based Financing Is and When to Use It

Revenue-based financing is a funding model where a provider gives you a lump sum of capital and you repay it by sharing a set percentage of your monthly revenue until the agreed-upon repayment cap is reached. Payments automatically adjust: you pay more in strong months and less during slow periods. Once you hit the cap, payments stop entirely.

RBF is built around three core components. The funding amount is the capital you receive upfront. The revenue share (also called the royalty rate) is the monthly percentage you pay back, usually 5% to 15%. The repayment cap is the maximum total repayment, expressed as a multiple of your advance (for example, 1.2x means you repay $120,000 on a $100,000 advance).

RBF works best for businesses that already generate revenue and need capital fast. Common uses include funding marketing campaigns, purchasing inventory for a peak season, bridging the gap between equity rounds, or expanding into new markets. If you are a pre-revenue startup, RBF will not work for you, but business loans for startups or pre-seed funding might.

Who Qualifies for Revenue-Based Financing

Eligibility varies by provider, but most RBF companies focus on your revenue history rather than your personal credit score. Here are the typical requirements you should expect as of 2026.

- Monthly revenue ranges from $7,500 to $100,000+ depending on the provider. accessible small business providers start around $7,500 a month, while ecommerce focused platforms look for $100,000 or more in monthly recurring revenue.

- Annual recurring revenue (ARR) of at least $100,000 to $200,000 is the usual threshold at SaaS focused providers.

- Time in business varies from 3 months at the accessible end to 6 months at most providers, with some wanting 2+ years.

- Credit score requirements are generally low. Floors across the market run from the mid 500s to about 650, and our tested pick Credibly accepts scores as low as 500. Some providers have no credit score minimum at all.

- Gross margin of 60%+ is preferred, especially for SaaS-focused providers, because higher margins mean more cash available to cover the revenue share.

Unlike traditional bank loans, most RBF providers do not require collateral, personal guarantees, or a detailed business plan. The application process is usually completed online in minutes, and you connect your financial accounts (bank, accounting software, payment processor) so the provider can verify your revenue directly.

How to Apply for Revenue-Based Financing

The application process for RBF is significantly faster than a traditional bank loan. Most providers follow a straightforward 4-step process that takes 1 to 5 business days from application to funding, though some complete the process in as little as 24 hours.

Step 1: Submit your application. You will fill out a short online form with basic business information (legal name, EIN, industry, monthly revenue estimate). At most online providers this takes about 10 minutes.

Step 2: Connect your financial data. You will securely connect your business bank accounts, accounting systems (QuickBooks, Xero), and billing platforms (Stripe, Shopify). The provider uses this data to verify your revenue history and assess repayment capacity.

Step 3: Review your offer. The provider will present a financing offer that includes the funding amount, the repayment cap (for example, 1.15x), the revenue share percentage (for example, 5%), and the repayment frequency (daily, weekly, or monthly). Compare this offer against other providers before accepting.

Step 4: Accept and receive funds. Once you sign the agreement, funds are deposited directly into your business bank account. At most providers, this happens within 24 to 48 hours. Repayment begins automatically via ACH deductions based on the agreed percentage of your revenue.

If you want to compare this process to traditional lending, see our step-by-step guide on how to get a business loan.

What Revenue-Based Financing Actually Costs

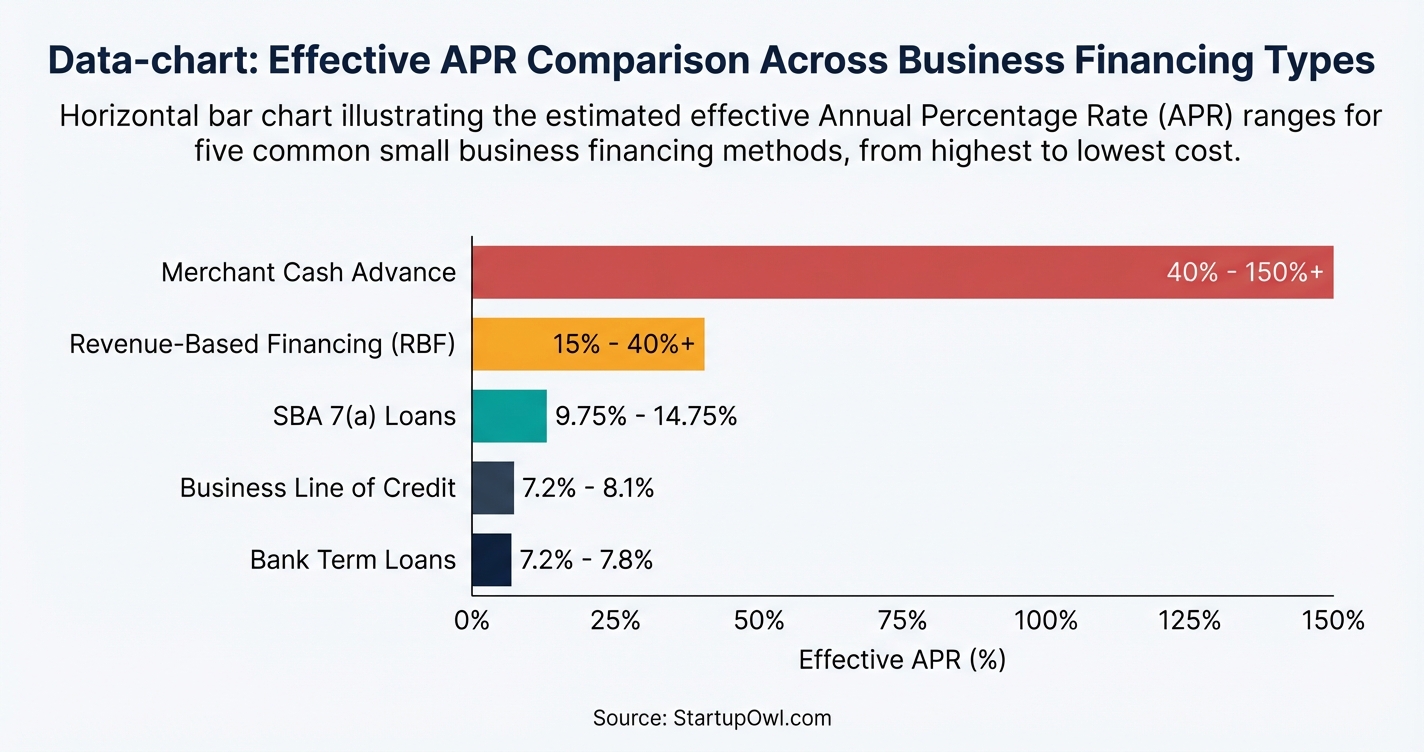

RBF does not use a traditional interest rate. Instead, you pay a flat fee expressed as a factor rate (for example, 1.2x). If you receive $100,000 at a 1.2x factor rate, you repay $120,000 total, regardless of how quickly or slowly you pay it back. That fixed cost structure sounds simple, but the effective APR can range from 15% to 40%+ depending on how fast your revenue (and therefore your payments) grows.

Here is where RBF gets tricky. If your revenue grows faster than expected, you repay the cap sooner, which compresses the cost into a shorter timeframe and drives your effective APR higher. A deal that looks like a 20% APR at moderate growth could turn into a 40%+ APR if your business takes off. Always ask providers for the implied IRR under multiple growth scenarios before committing.

For comparison, traditional bank term loans average about 7.2% to 7.8% APR, and SBA 7(a) loans run 9.75% to 14.75% APR as of 2026. RBF trades that lower rate for faster approval, easier qualification, and no equity dilution. If you qualify for an SBA loan, it will almost always be cheaper. If you do not, RBF can be a practical alternative.

RBF Cost Compared to Other Financing Options

| Type / Provider | Rate | Notes |

|---|---|---|

| Revenue-Based Financing | 15% to 40%+ effective APR | Factor rate of 1.1x to 1.5x; varies by growth speed. No equity dilution. |

| Bank Term Loans | 7.2% to 7.8% APR | Requires 680+ credit score, 2+ years in business, and collateral. |

| SBA 7(a) Loans | 9.75% to 14.75% APR | Lower rates but 30-90 day approval timeline and extensive documentation. |

| Business Line of Credit | 7.2% to 8.1% APR | Revolving access; good for ongoing working capital needs. |

| Merchant Cash Advance | 40% to 150%+ effective APR | Similar to RBF but based only on card sales. Typically more expensive. |

The Providers We Actually Recommend

We removed the usual list of venture backed RBF platforms from this section in July 2026. The market moved under it. Several of the best known names stopped taking direct applications from founders. And we only send readers to providers we have tested ourselves.

Our tested picks live in the ranking of the best revenue based financing companies. Wayflyer joined the roster in July 2026. It leads for ecommerce now. One fixed fee, funding in 24 to 48 hours, and our full Wayflyer review holds the honest APR math. The short version on the rest. Credibly runs a true revenue based product with factor rates from 1.11 and same day funding. Lendio reaches 75 plus lenders with one form. National Funding fits fair credit backed by strong revenue. OnDeck is the transparent APR alternative, a price you can compare without algebra. Ecommerce and SaaS pure plays are in our testing pipeline and will join that page as they pass.

Selling on Shopify or Amazon? We broke down the platforms' own 2026 offers too. See the Shopify Capital review and alternatives, plus the Amazon seller loans guide.

Check Your State's Disclosure Requirements Before Signing

As of 2026, at least 9 states (including California, New York, Virginia, Connecticut, Florida, Georgia, Kansas, Utah, and Missouri) have enacted commercial financing disclosure laws that require RBF and MCA providers to give you standardized cost disclosures similar to TILA disclosures for consumer credit. If your provider does not give you a disclosure document in one of these states, that is a red flag. The CFPB has also proposed excluding revenue-based financing from its small business lending data collection rule, which means federal oversight of RBF remains limited. Protect yourself by requesting a full breakdown of all fees and the estimated APR equivalent before you sign.

What to Do If You Do Not Qualify for RBF

If you do not meet the revenue thresholds for RBF, or if the effective cost is too high for your margins, several alternatives may be a better fit.

- SBA microloans provide up to $50,000 at rates around 8% to 13% APR, even for newer businesses. They do require more documentation and a longer approval timeline (30-90 days).

- Invoice factoring lets you sell outstanding invoices for immediate cash at a discount of 1% to 5% per month. This works well if you have B2B customers on net-30 or net-60 terms.

- Merchant cash advances are similar to RBF but are based on credit card sales rather than total revenue. MCAs are typically more expensive (effective APRs often exceed 40%), so use them only as a last resort.

- Business credit cards offer revolving credit up to $50,000+ with introductory 0% APR periods of 12 to 15 months. They work well for smaller capital needs.

- Angel investors or small business grants can provide capital with no repayment obligation (grants) or in exchange for equity (angels).

Your best move is to build your business credit while using shorter-term financing, so you can eventually qualify for lower-cost products like SBA loans or bank lines of credit.

5 Costly Mistakes to Avoid with Revenue-Based Financing

1. Ignoring hidden fees. Setup fees, servicing fees, platform fees, and legal fees can quietly increase your true cost of capital well beyond the stated factor rate. Always ask for a complete fee schedule in writing before you sign.

2. Not modeling different growth scenarios. RBF feels affordable at moderate growth rates. But if your revenue grows 50%+ year over year, you repay the cap much faster, and the implied IRR on the deal can exceed 40%. Run the numbers at slow, moderate, and fast growth before you commit.

3. Missing catch-up mechanisms in the contract. Some RBF contracts include minimum monthly payment floors or revenue baselines with catch-up provisions. These clauses effectively convert your flexible repayment into semi-fixed payments, removing the key benefit of RBF.

4. Overlooking the maturity date. Many RBF agreements have a maturity date (often 18 to 36 months). If you have not reached the repayment cap by that date, the remaining balance may become due as a lump sum. Clarify this before signing.

5. Confusing RBF with a merchant cash advance. MCAs are based on credit or debit card sales and typically carry higher costs. RBF considers your total revenue. If a provider is only looking at your card transactions, you may be getting an MCA deal with MCA pricing, not true RBF. Know the difference by reading our merchant cash advance guide.

Step-by-Step Process

- 1

Assess your revenue and determine how much capital you need

Calculate your monthly recurring revenue (MRR) and annual recurring revenue (ARR) before approaching any provider. Most RBF providers will finance 20% to 50% of your ARR for new customers, and sometimes up to 70%+ for repeat borrowers. Match your capital need to a realistic percentage of your revenue so you can sustain the repayment share without straining operations.

Tips

- Model at least three scenarios (slow, moderate, and rapid growth) to see how different revenue trajectories affect your total repayment cost.

- Calculate your gross margin first. Providers prefer margins of 60% or higher because they leave room for the revenue share deduction.

Common Mistakes

- Requesting more capital than your revenue can comfortably support, which leads to cash flow strain during slow months.

- Ignoring the implied IRR under high-growth scenarios, where RBF becomes surprisingly expensive.

- 2

Gather your financial data and connect your accounts

RBF providers use your bank statements, accounting software, and payment processor data to underwrite your deal. Prepare 4 to 6 months of recent business bank statements, connect platforms like Stripe, QuickBooks, or Xero, and have your EIN and formation documents ready. Unlike traditional bank loans, you typically will not need a detailed business plan or pitch deck.

Tips

- Keep your accounting software current with at least a monthly refresh so providers see accurate, up-to-date financials.

- Ensure your bank statements show consistent deposits rather than large irregular lumps, which signal revenue volatility.

Common Mistakes

- Submitting incomplete or outdated financial records, which delays approval or results in a lower offer.

- 3

Compare providers and evaluate their offer terms

Submit applications to at least 2 to 3 providers to compare terms side by side. Focus on the factor rate (typically 1.1x to 1.5x), the revenue share percentage (5% to 15%), and the repayment timeline (6 to 24 months). Ask each provider for the total repayment cap, any origination or platform fees, and whether catch-up or true-up mechanisms exist in the contract.

Tips

- Ask every provider for the implied IRR under your specific growth scenario so you can compare apples to apples.

- Check whether the repayment cap includes fees or if fees are charged separately on top of the cap.

- Confirm whether repayment frequency is daily, weekly, or monthly, as daily deductions can strain cash flow more than monthly ones.

Common Mistakes

- Comparing only the factor rate without calculating the total cost of capital including all fees.

- Accepting the first offer without negotiating terms or shopping alternatives.

- 4

Review the contract and sign the agreement

Before signing, read the full agreement carefully. Pay close attention to the revenue definition (gross vs. net), the maturity date, default language, and any personal guarantee requirements. Some contracts include minimum monthly payment floors or catch-up provisions that effectively convert your flexible repayment into semi-fixed obligations. Have an attorney or CPA review the terms if the deal exceeds $100,000.

Tips

- Verify whether the contract uses gross revenue or net revenue as the basis for calculating your payment percentage.

- Check whether early repayment triggers any penalties or if prepayment discounts are available.

Common Mistakes

- Signing a contract with a catch-up mechanism that imposes minimum payments during slow revenue periods.

- Overlooking the maturity date clause, which may require a lump-sum balloon payment if the cap is not reached.

- 5

Receive funding and begin repayment

After signing, most providers deposit funds into your business bank account within 24 to 48 hours. Repayment starts immediately via automatic ACH deductions based on the agreed-upon revenue share percentage. Track your repayment progress monthly so you know how quickly you are approaching the cap and how the payments affect your working capital.

Varies by deal (1.1x to 1.5x of funded amount is typical total repayment) 24-48 hours for funding; 6-24 months for repayment biz2credit.comTips

- Set up a separate tracking spreadsheet or dashboard to monitor cumulative payments against your repayment cap.

- Use your accounting software to categorize RBF payments properly so you can deduct eligible costs at tax time.

Common Mistakes

- Failing to budget for the revenue share deduction and then running short on operating cash during a slow month.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Factor rate (repayment multiple) | 1.1x to 1.5x (some providers up to 3x) | This is the total amount you repay. A $100K advance at 1.2x costs $120K total. |

| Revenue share percentage | 5% to 15% of monthly revenue | Higher revenue share means faster repayment but more cash flow strain. |

| Effective APR equivalent | 15% to 40%+ | Varies significantly based on repayment speed and growth rate. Fast growth increases effective APR. |

| Origination or setup fees | $0 to 3% of funded amount | Some providers charge no origination fee; others add platform or servicing fees. |

| Legal and closing costs | $0 to $20,000 | SaaS focused lenders estimate closing costs up to $20K on larger deals. Smaller RBF deals often have zero closing costs. |

Frequently Asked Questions

The total cost is determined by your factor rate (repayment multiple), which typically ranges from 1.1x to 1.5x the funded amount. On a $100,000 advance at 1.2x, you repay $120,000 total. The effective APR equivalent usually falls between 15% and 40%, depending on how quickly your revenue grows and how fast you reach the cap.

No. Most RBF providers weigh your revenue history far more heavily than your credit score. Our tested pick Credibly accepts scores as low as 500. Floors across the market run from the mid 500s up. A few set no credit minimum.

Many providers fund in 24 to 48 hours after you apply and connect your financial accounts. Same day funding exists at the fastest small business providers. SaaS focused lenders with deeper underwriting can take 3 to 4 weeks for new clients. Repeat clients move faster.

They are similar but not identical. An MCA is based specifically on your credit and debit card sales, while RBF considers your total business revenue (including invoices, ACH payments, and subscriptions). RBF typically offers broader eligibility and sometimes lower costs. Read our full merchant cash advance guide for a detailed comparison.

No. RBF requires existing revenue to underwrite the deal and structure repayments. If you are pre-revenue, explore alternatives like pre-seed funding, small business grants, or SBA microloans up to $50,000 that are available to newer businesses without established revenue streams.

It depends on the contract structure. Many RBF agreements are technically structured as purchases of future receivables (not loans), so they may not appear as traditional debt on your balance sheet. However, the obligation to repay is real, and lenders reviewing your financials will factor it in. Consult your CPA to determine the correct accounting treatment for your specific agreement.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. APR ranges reflect industry averages as of 2026 and may change without notice.

Sources & References

- Credibly, Revenue Based Business Loans (verified 2026-07-11)

- Lendio, What is Revenue Based Financing

- Investopedia, Revenue Based Financing Definition

- Wikipedia, Revenue Based Financing

- American Bar Association, State Survey of Commercial Financing Disclosure Laws

- FTC, Small Business Financing Staff Perspective

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Revenue-Based Financing, How It Works and Whether It Is Right for Your Business

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment