Business Insurance Types Explained

General liability insurance protects your business from customer injury and property damage claims. Here is what it costs, what it covers, and how to buy it.

In This Article

Definition

General liability insurance pays for third-party bodily injury, property damage, and advertising injury claims so your business does not cover those costs out of pocket.

General liability insurance protects your business from third-party claims of bodily injury, property damage, and advertising injury. Most small businesses pay $42 to $85 per month for a policy with $1 million per occurrence and $2 million aggregate limits. You can get a quote and start coverage within 24 hours through online providers like Insureon, The Hartford, or NEXT Insurance.

General liability insurance costs a median of $42 to $45 per month (about $500 per year) for most small businesses, according to data from Insureon as of 2026. It is typically the first insurance policy you buy after forming your business, and most commercial leases and client contracts require at least $1 million in coverage before you can sign. If you skip it, a single slip-and-fall claim averaging $20,000 to $45,000 could come straight out of your pocket.

No legitimate free option exists for general liability insurance.

Free Option

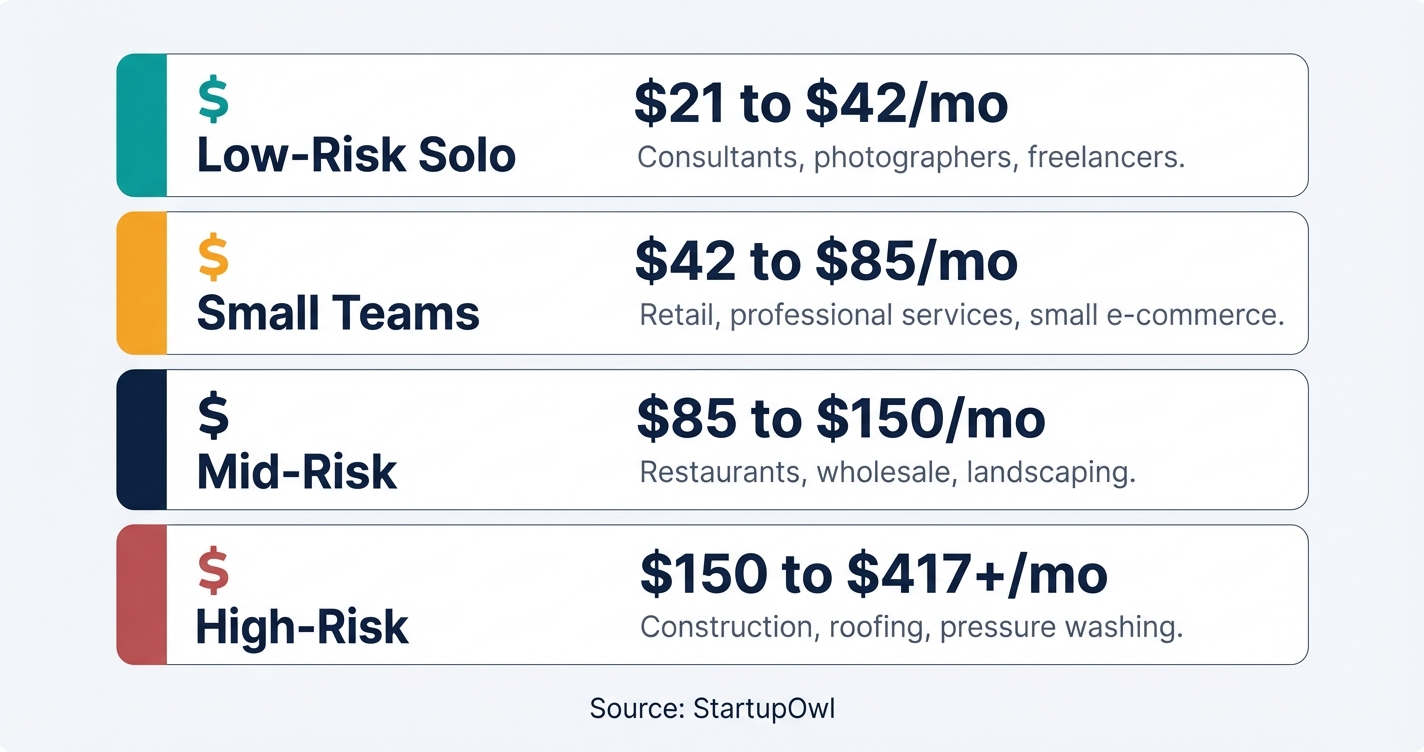

$21 to $42 per month ($250 to $500 per year) for solo, low-risk businesses like consultants or photographers.

Low-End

$45 to $85 per month ($500 to $1,000 per year) for small teams in moderate-risk industries like retail or professional services.

Mid-Tier

$100 to $417+ per month ($1,200 to $5,000+ per year) for high-risk industries like construction, restaurants, or wholesale trade.

Premium

General liability insurance (sometimes called commercial general liability or CGL) is a policy that covers your business when a third party (someone outside your company) claims you caused them bodily injury, property damage, or advertising injury. Think of it as a financial shield between your business bank account and the lawsuits that can arise from everyday operations.

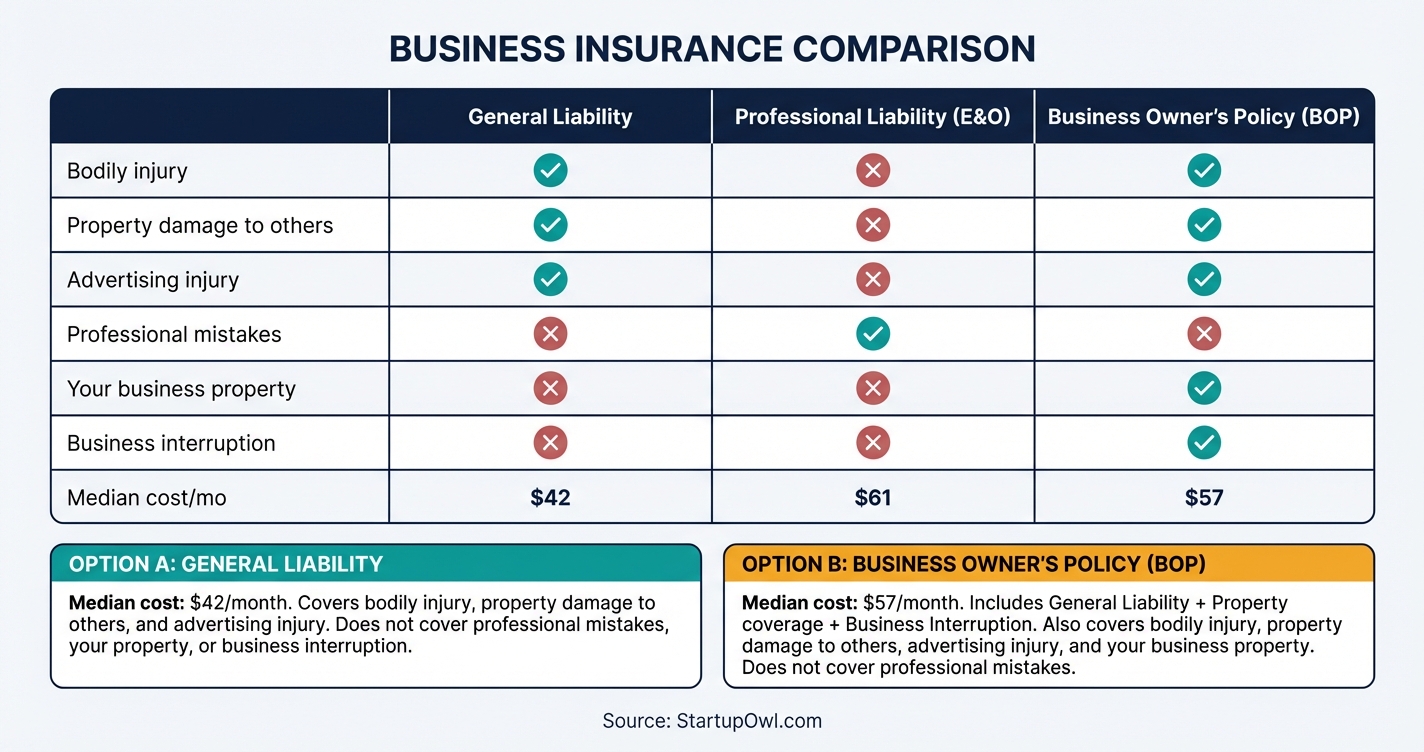

A standard general liability policy covers three main areas. First, bodily injury, which includes medical expenses and legal fees if a customer slips on your floor or gets hurt at your location. Second, property damage, which pays to repair or replace a client's property that your business accidentally damages. Third, personal and advertising injury, which covers claims of libel, slander, copyright infringement, and false advertising.

Here is a real-world example. You run a small cleaning business. While working at a client's office, your employee accidentally knocks over an expensive monitor and cracks a glass partition. The client bills you $4,500 for repairs. Your general liability policy covers the full amount minus your deductible (typically $500), so you pay $500 instead of $4,500.

General liability does not cover employee injuries (that is workers' compensation), professional mistakes (that is professional liability or E&O insurance), damage to your own property (that is commercial property insurance), or auto accidents involving company vehicles (that is commercial auto insurance). For a full overview of all insurance types you may need, see our guide to best business insurance.

The stakes of operating without general liability insurance are high. According to a 2026 study by The Hartford, 4 out of 10 small businesses will face a property or general liability claim within a 10-year period. The average bodily injury claim (like a customer slip-and-fall) costs about $45,000, and reputational harm claims average $35,000, per NerdWallet's analysis of Hartford data as of 2026.

Without a policy, you pay every dollar of that yourself. A single lawsuit with legal fees, medical bills, and a potential settlement can easily exceed $75,000. For a small business with $200,000 in annual revenue, that is more than a third of your gross income wiped out by one incident.

Beyond the financial risk, many business relationships require proof of coverage. Most commercial landlords will not sign a lease without seeing a certificate of liability insurance showing at least $1 million in coverage. Many clients, especially larger companies and government agencies, require contractors and vendors to carry general liability before signing a contract. If you cannot produce a certificate of insurance (COI), you lose the deal. Learn more about related requirements in our guide to registered agent requirements.

General liability insurance operates on a per-occurrence and aggregate limit structure. The standard policy most small businesses purchase is $1 million per occurrence (the maximum the insurer pays for a single claim) and $2 million aggregate (the total the insurer pays across all claims in one policy year). About 91% of businesses choose this limit structure, according to marketplace data from Insureon as of 2026.

When a covered incident happens, you file a claim with your insurer. You pay the deductible (typically $500 for most small businesses), and the insurer covers the rest up to your policy limit. This includes legal defense costs, medical payments, settlements, and judgments. If a claim is filed, most insurers assign an adjuster who evaluates the damages and works toward resolution.

You select your coverage limits and deductible when purchasing the policy. Higher limits cost more per month but protect you from larger claims. Higher deductibles reduce your monthly premium but increase your out-of-pocket cost if something happens. For example, raising your deductible from $500 to $2,500 can reduce premiums by 15% to 25%, but you need to keep that extra $2,000 in reserve.

Your premium is recalculated at renewal (usually annually). Insurers look at your claims history, revenue changes, employee count, and industry risk. A clean claims history keeps premiums low, while filing even one claim can increase rates by 25% to 50% for the following 3 to 5 years.

Getting general liability insurance is fast. Most small business owners can complete the process in under 30 minutes and have coverage active within 24 hours.

Step 1: Gather your business information. You will need your legal business name, EIN (see our EIN application guide), business address, industry type, annual revenue, number of employees, and claims history.

Step 2: Get quotes from multiple providers. Use an online marketplace like Insureon (compares quotes from The Hartford, Chubb, Hiscox, Liberty Mutual, and others with a single application), or go directly to carriers like The Hartford, NEXT Insurance, or Progressive Commercial. Compare at least 3 quotes.

Step 3: Compare coverage, not just price. Check the per-occurrence limit, aggregate limit, deductible amount, and exclusions. One policy at $50/month with a $2,500 deductible may cost you more out of pocket than a $60/month policy with a $500 deductible if you file a claim.

Step 4: Purchase and download your COI. Once you select a policy, you can typically download your certificate of insurance (COI) immediately. You will need this document for lease applications, client contracts, and licensing in some states.

If you also need property coverage, consider a Business Owner's Policy (BOP), which bundles general liability with commercial property insurance. A BOP typically costs about $57 per month (per Insureon data as of 2026), saving 10% to 20% compared to buying the policies separately. For your complete business setup, visit our complete business setup guide.

General liability insurance costs vary widely, but here is what you can realistically expect to pay as of 2026.

- Median premium (Insureon data): $42 to $45 per month, or about $500 per year.

- Average premium (MoneyGeek study): $104 per month, or about $1,242 per year for a business with 2 employees and $1M/$2M limits.

- The Hartford customers: About $68 per month, or $810 per year.

- Progressive customers: Median of $60 per month; average of $85 per month.

Why the range? The median reflects what most small businesses actually pay, while averages get pulled up by high-risk industries like construction and pressure washing. If you run a consulting firm, you will likely pay toward the lower end. If you run a restaurant, expect to pay more.

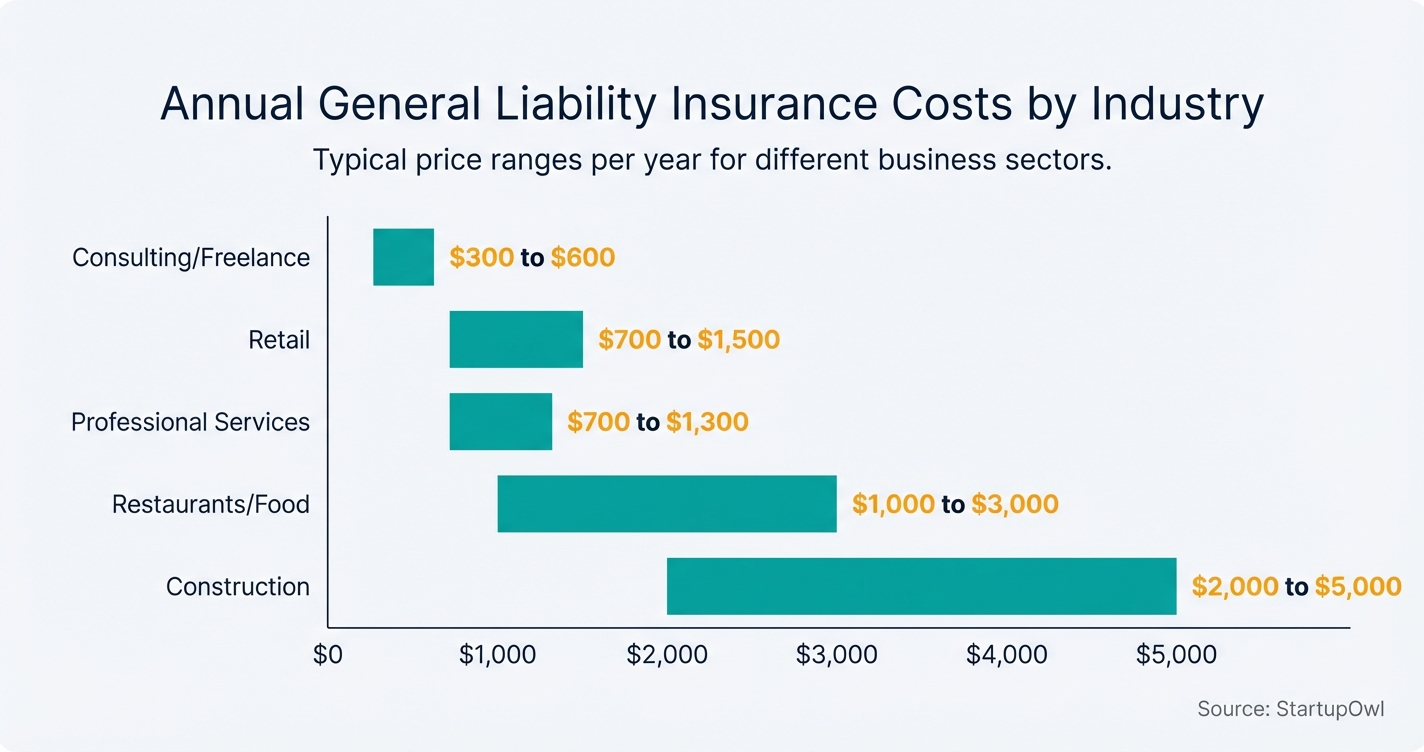

Industry-specific cost ranges (for businesses under $1M revenue, per Coverdash/NerdWallet 2026 data):

- Retail businesses: $700 to $1,500 per year

- Professional and technical services: $700 to $1,300 per year

- Wholesale trade: $700 to $2,500 per year

- Restaurants and food services: $1,000 to $3,000 per year

- Construction: Up to $5,000 per year

Hidden costs to watch for: Monthly payment plans typically add 8% to 12% in financing fees compared to paying annually. Endorsements (adding an additional insured, product liability riders, etc.) increase your premium. Filing a claim can raise renewal rates by 25% to 50%. For a detailed breakdown, see our guide on business bank account fees to understand all the operational costs of running a new business.

Freelancers and solo consultants typically pay $300 to $600 per year for general liability. If you work from home with no client visits, your risk is low and premiums reflect that. You may still need coverage for client contracts or co-working space agreements. Pair it with professional liability (E&O) insurance if you provide advice or deliverables.

E-commerce businesses face product liability risk. Your general liability policy usually includes some product liability coverage, but if you sell physical products, verify the policy covers product-related claims. Premiums range from $500 to $1,500 per year depending on your product type and revenue.

Brick-and-mortar retail businesses with customer foot traffic should budget $700 to $1,500 per year. Slip-and-fall claims are the single most common type of liability claim for retail. A BOP is often the most cost-effective option since you also need commercial property coverage for your storefront.

Restaurants and food service businesses pay more, typically $1,000 to $3,000 per year, because of elevated slip-and-fall risk, food contamination exposure, and high customer volume. You will also need workers' compensation if you have employees, and you may want liquor liability coverage if you serve alcohol.

Professional services (lawyers, accountants, architects) need general liability plus professional liability. General liability alone runs about $700 to $1,300 per year for these businesses. Professional liability adds another $1,000 to $3,000 per year depending on your specialty. Most client contracts require both.

LLCs have specific considerations. A single-member LLC typically pays $500 to $1,000 per year for basic general liability. Multi-member LLCs with employees should budget $2,000 to $5,000 for comprehensive protection including liability, property, and workers' comp. Learn about structuring your LLC at best LLC formation services and compare tax implications at LLC vs S Corp tax comparison.

1. Choosing the cheapest policy without reading exclusions. A policy that costs $25/month may exclude product liability, completed operations, or advertising injury. If you sell products or run advertising, those exclusions can leave you completely exposed. Always compare exclusions across quotes, not just premiums.

2. Carrying only $100,000 in coverage to save money. A basic $100,000 limit costs $200 to $400 per year, but a single slip-and-fall claim can exceed $100,000 when you include legal fees and a settlement. Upgrading to $1 million in coverage typically costs only 30% to 50% more for 10 times the protection. The math strongly favors higher limits.

3. Confusing general liability with professional liability. General liability covers physical injury and property damage. It does not cover mistakes in your professional work, missed deadlines, or bad advice. If a client sues because your consulting recommendations lost them money, general liability will not help. You need a separate professional liability (E&O) policy.

4. Assuming your homeowner's policy covers business activities. It almost certainly does not. Most homeowner's policies explicitly exclude business-related claims. If a client visits your home office and trips on your stairs, your homeowner's insurance will likely deny the claim. You need a standalone general liability policy.

5. Not updating your policy as revenue grows. Your premium is partly based on your annual revenue. If you quoted your policy at $100,000 in revenue and your business grew to $500,000, your insurer may deny a claim or charge back-premiums during a premium audit. Review your coverage annually and update your revenue figures. For help tracking your finances accurately, check out our guide to how to set up small business accounting.

Where AI sits in your policy, and why nobody can tell you yet

AI does not arrive with insurance attached. We checked Hiscox's professional liability page on 30 July 2026 and artificial intelligence appears 0 times on it, in the covered list and in the exclusions alike. So if you use AI in work you deliver to clients, one question is worth asking early. Will your professional liability policy respond when AI assisted work causes a client a loss.

No guide can answer it. Anyone who does is guessing. That silence on the carrier's own page is the finding. It means the answer sits in your own policy wording rather than in a product page, and it may differ between two carriers selling what looks like the same cover.

So treat it as a question for your insurer, in writing, naming what you actually do. Something like this. If I use an AI tool to produce part of a deliverable and the client suffers a loss from an error in it, does this policy respond. Ask whether the answer changes if the tool is one you built rather than one you licensed. Ask whether disclosing AI use to clients affects it either way.

Get the reply in writing and keep it with the policy. Renewal is the moment to raise it again, because wordings are being revised and an answer from last year may not hold. None of this is urgent enough to buy something new today. It is worth ten minutes at renewal.

Frequently Asked Questions

Most small businesses pay between $42 and $85 per month for general liability insurance as of 2026. The median is about $42 to $45/month (roughly $500/year) according to Insureon. Low-risk businesses like consultants can pay as little as $21/month, while high-risk industries like construction can pay $400+/month.

No, general liability insurance is not required by any state law for most businesses. However, some states require it for licensed contractors, and most commercial leases, client contracts, and loan agreements require at least $1 million in coverage. Practically speaking, you will struggle to lease office space or sign contracts without it.

A BOP bundles general liability insurance with commercial property insurance (and usually business interruption insurance) into one policy. A BOP costs about $57/month on average, which is only $15 more per month than standalone general liability, but adds property and income-loss coverage. If you rent or own a business location, a BOP is usually the better deal.

You can get covered in under 24 hours. Online providers like Insureon and NEXT Insurance let you complete an application in 10 to 20 minutes, receive quotes instantly, and download your certificate of insurance (COI) the same day.

General liability does not cover employee injuries (you need workers' comp), professional mistakes or bad advice (you need professional liability or E&O), damage to your own property (you need commercial property insurance), or auto accidents involving business vehicles (you need commercial auto). Think of it as covering injuries and damage you cause to other people and their stuff only.

Yes. General liability insurance premiums are considered a cost of doing business and are typically 100% tax-deductible as a business expense. Consult a licensed CPA or tax professional to confirm how it applies to your specific tax situation.

Sources & References

- General Liability Insurance Cost (Insureon)

- Best General Liability Insurance for Small Businesses (NerdWallet, 2026)

- Average General Liability Insurance Cost (MoneyGeek, 2026)

- General Liability Insurance Cost (The Hartford)

- General Liability Insurance (Progressive Commercial)

- Get Business Insurance (U.S. Small Business Administration)

- General Liability Insurance Requirements (Insureon)

- Small Business Insurance Cost Guide (Homebase, 2026)

- When Is Liability Insurance Needed (The Hartford)

About the Author

Senior Legal Researcher & Business Analyst

Eliot combines decades of boots-on-the-ground small business management with deep expertise in legal consulting. Building his career in New Jersey, he spent years helping local, brick-and-mortar startups navigate the complex web of municipal, state, and federal regulations. He isn't a high-tower academic; he's a street-smart consultant who has personally walked hundreds of entrepreneurs through the structural and legal growing pains of running a business.

Was this article helpful?

Questions about Business Insurance Types Explained

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment