Seed Funding for Startups: How Rounds Work, Typical Amounts and Investor Expectations

Seed funding rounds average $2.5M to $3.5M at $14M-$17M pre-money valuations, with 15-25% dilution. Learn how rounds work and what investors expect.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Seed Funding Is and When to Raise It

- What You Need to Qualify for Seed Funding

- How to Raise a Seed Round in 5 Steps

- The Real Cost of a Seed Round

- Top Seed Funding Sources and What They Offer

- What to Do If You Are Not Ready for Seed Funding

- 5 Seed Funding Mistakes That Can Sink Your Startup

- FAQ

$5,000–$50,000

Est. Loan Cost

90 days

Timeline

5

Total Steps

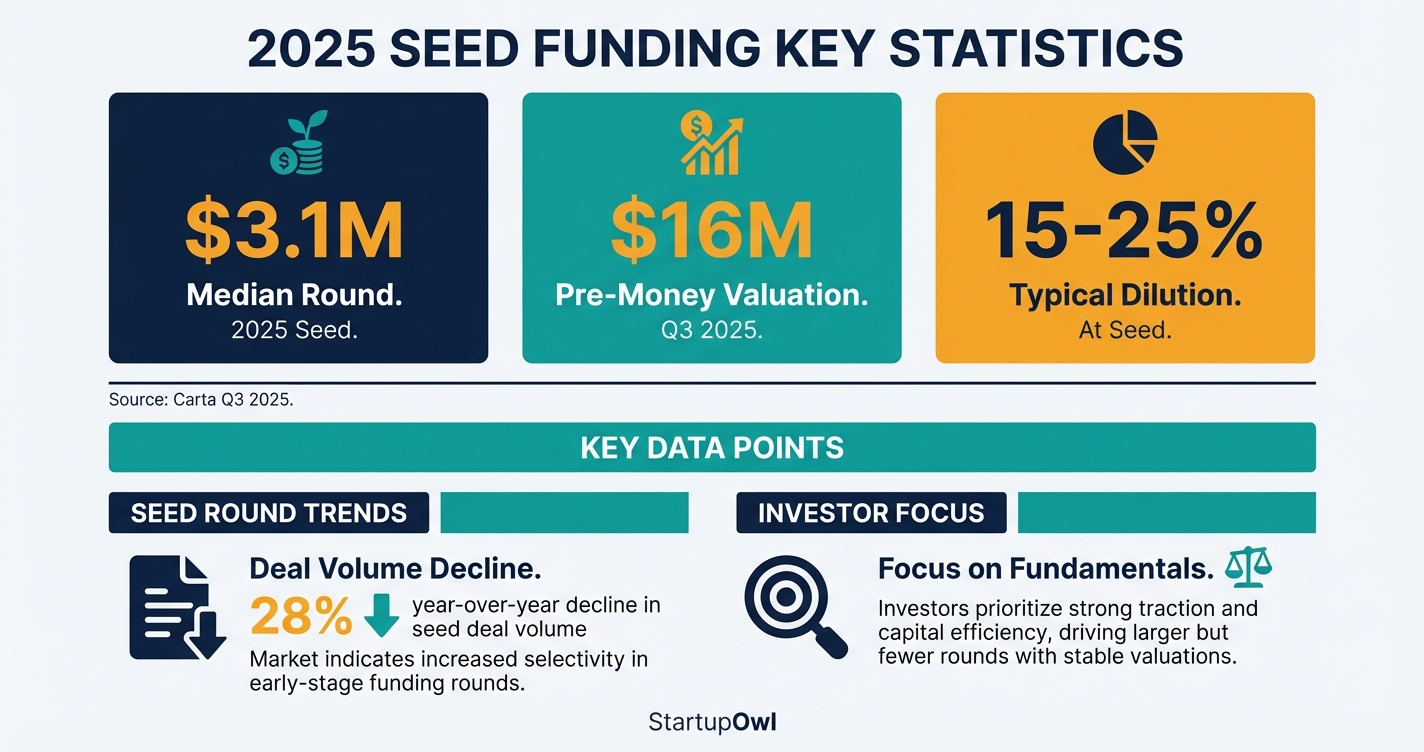

The median seed round in the United States reached $3.1 million in 2026, according to Carta data, while pre-money valuations climbed to $16 million. At the same time, seed deal volume dropped 28% year over year, meaning fewer startups are getting funded but those that close are raising more capital at higher valuations.

Seed funding is equity investment (not a loan) where you trade ownership in your company for capital. You will not repay this money. Instead, your investors profit only if your company grows in value. If you are exploring debt-based alternatives, check our guides on business loans for startups and SBA loans.

This guide walks you through how seed rounds actually work in 2026, including typical amounts by sector, deal structures (SAFEs vs. priced rounds), what investors expect, and a five-step process to close your round.

What Seed Funding Is and When to Raise It

Seed funding is the first significant round of institutional capital you raise after bootstrapping or a pre-seed round. It sits between pre-seed (typically $100K-$1M) and Series A (typically $5M-$15M). The money is used to achieve product-market fit, build your initial team, acquire early customers, and reach the milestones needed for a Series A within 12-24 months.

Seed investors get preferred stock or the right to future preferred stock (via a SAFE or convertible note) in exchange for their capital. Unlike business loans, there are no monthly payments, no interest charges, and no personal guarantees. The trade-off is permanent dilution of your ownership stake.

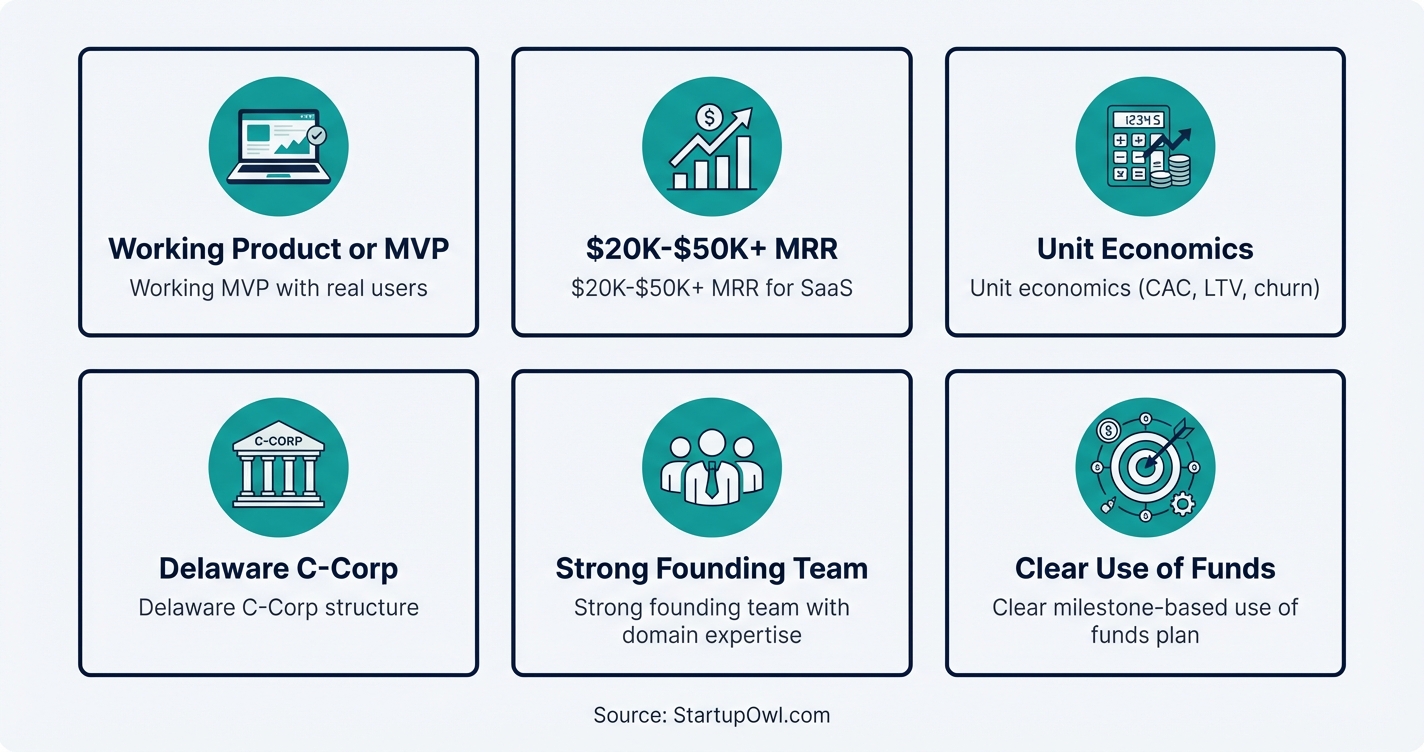

Timing matters. You should raise seed funding when you have a working product and early evidence that customers want what you are building. Seed investors in 2026-2026 expect to see validated retention metrics, early revenue (ideally $300K-$500K ARR for SaaS), and realistic financial projections grounded in real data. The era of raising seed on a pitch deck alone is largely over.

What You Need to Qualify for Seed Funding

Seed funding does not have credit score requirements or revenue minimums the way a bank loan does. Instead, investors evaluate a combination of factors, and the bar has risen significantly since 2021. Here is what seed investors typically expect in 2026.

- Working product or MVP with real users (not just a prototype). Only about 4% of startups that launch ever reach the seed stage.

- Early traction measured by revenue, user growth, or retention. For SaaS, that means $20K-$50K+ MRR. For consumer, show strong week-over-week user growth.

- Unit economics that demonstrate a path to profitability. Investors scrutinize customer acquisition cost, churn rate, and customer lifetime value.

- Delaware C-Corp structure (or willingness to convert). Most institutional investors will not invest in an LLC or sole proprietorship.

- A strong founding team with relevant domain expertise. Second-time founders with prior exits can command larger rounds and higher valuations.

- A clear use of funds tied to specific milestones (e.g., reaching $500K ARR, hiring 3 engineers, launching in 2 new markets).

If you do not yet meet these benchmarks, consider pre-seed funding, small business grants, or microloans to bridge the gap.

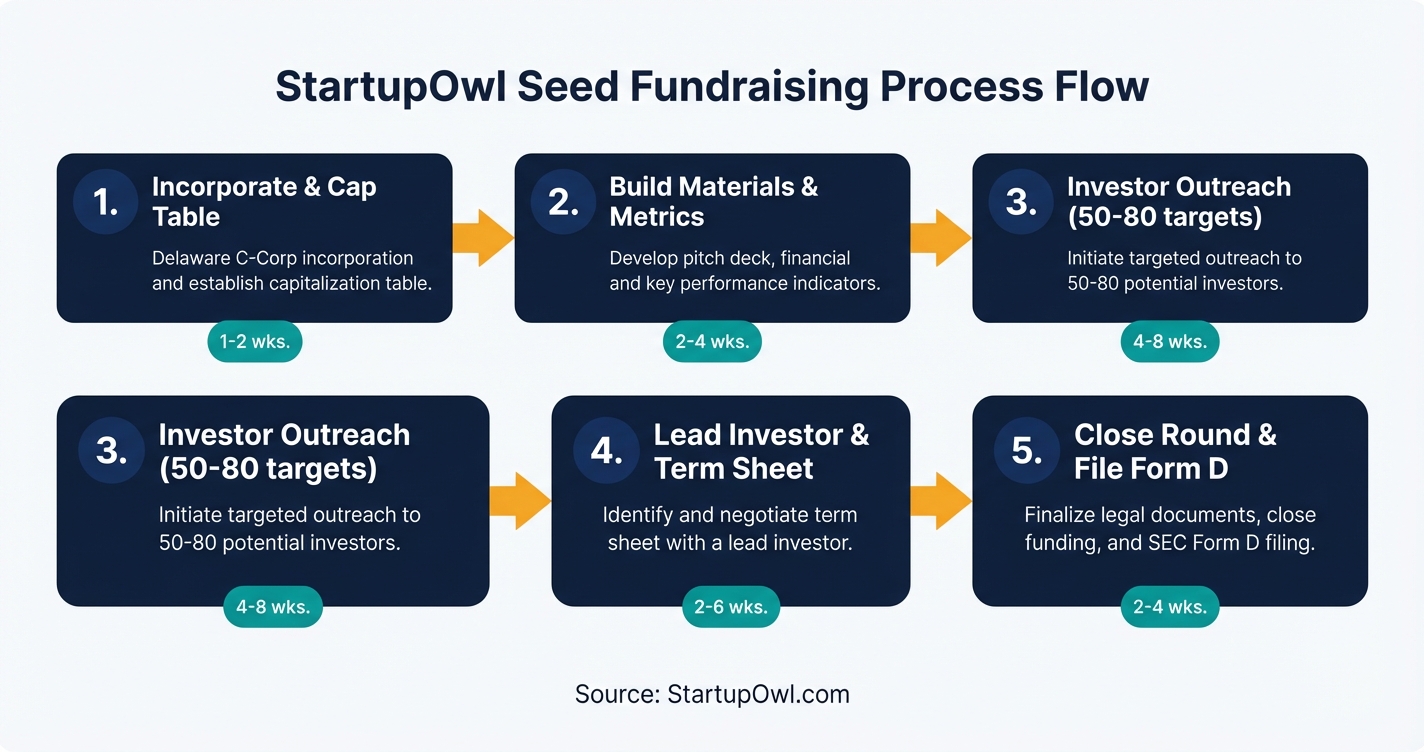

How to Raise a Seed Round in 5 Steps

Raising seed funding is not like applying for a loan. There is no single application form. Instead, you pitch multiple investors, negotiate terms, and close a round over several weeks or months. The five steps below outline the standard process.

See the detailed steps section above for timelines, costs, tips, and common mistakes for each stage. On average, the entire process from first pitch to money in the bank takes 3-6 months, though well-prepared founders with strong traction can close in as little as 4-6 weeks.

If you want to strengthen your financial foundation before raising, our guides on business accounting setup and how to build business credit cover the basics investors expect to see in order.

The Real Cost of a Seed Round

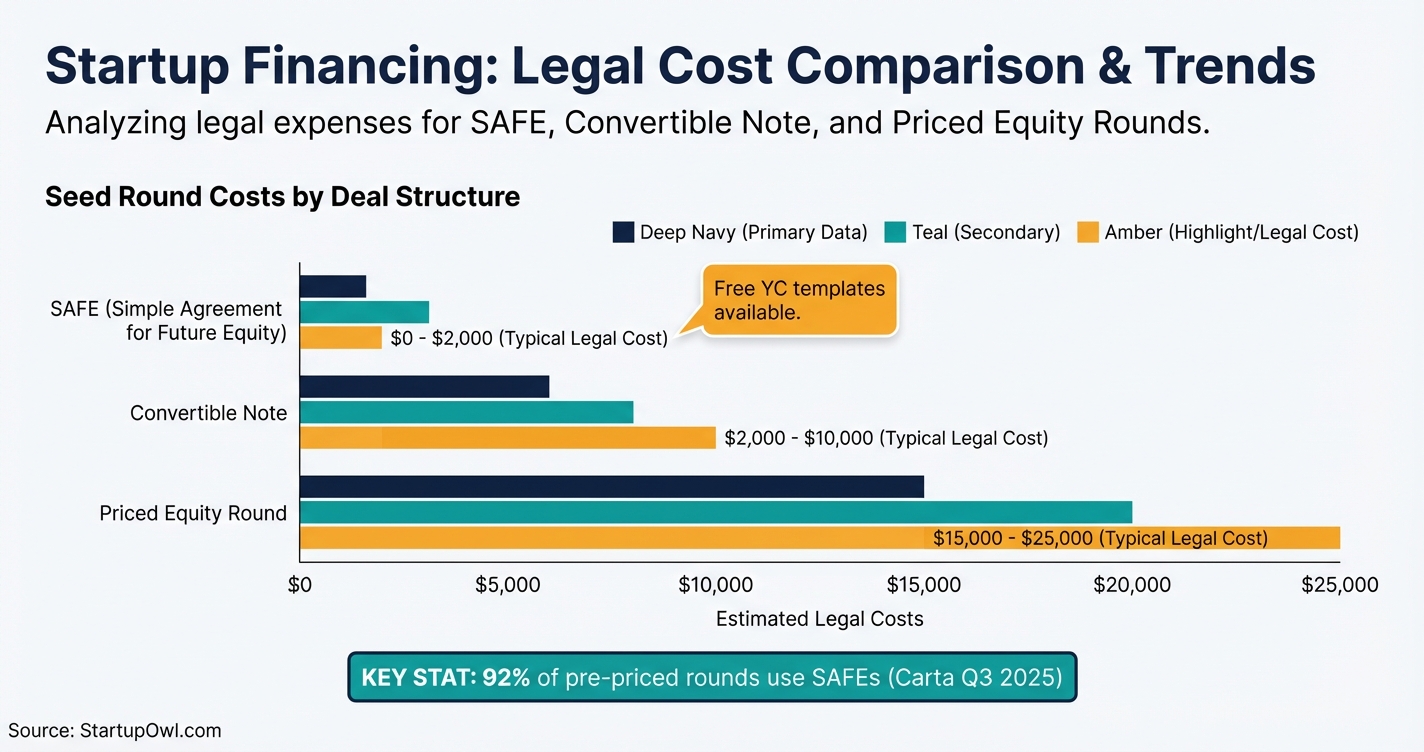

Seed funding has two types of costs: the out-of-pocket expenses to close the round (legal fees, filing costs) and the equity you give up permanently. The out-of-pocket costs range from $5,000 to $25,000, depending on whether you use a SAFE or a priced equity round. The equity cost is the bigger number.

At the median pre-money valuation of $16 million, raising $3 million means giving up roughly 15.8% of your company. If your valuation is lower (say $10 million), that same $3 million raise costs you 23% equity. This is why valuation negotiation matters so much. Every million dollars of valuation cap directly affects how much of your company you keep.

SAFEs (Simple Agreements for Future Equity) are the cheapest deal structure to execute. Legal costs for a SAFE-based round run $0-$2,000 if you use Y Combinator's free templates. Priced equity rounds require more legal work and typically cost $15,000-$25,000 in attorney fees, but they give both you and investors clearer ownership stakes from day one.

Convertible notes sit in between. They accrue interest (typically 4-8% annually) and have a maturity date (usually 12-24 months), adding a debt-like element that SAFEs avoid. The discount rate on convertible notes runs 10-25%, rewarding early investors when the note converts to equity.

Seed Round Deal Structures Compared

| Type / Provider | Rate | Notes |

|---|---|---|

| SAFE (most common under $4M) | No interest, no maturity date | 92% of pre-priced rounds use SAFEs as of Q3 2026 per Carta data. Fastest and cheapest to execute. |

| Convertible note | 4-8% interest, 12-24 month maturity | Functions as debt until conversion. Includes valuation cap and 10-25% discount rate. |

| Priced equity round (preferred stock) | $15,000-$25,000 in legal fees | Best for rounds over $3M or complex cap tables. Sets exact ownership on day one. |

| Typical valuation cap (SAFE/note) | $8M-$20M pre-money | AI startups command $20M+; traditional SaaS typically $8-$12M for seed. |

| Typical dilution at seed | 15-25% equity | Aim to retain at least 60-70% ownership after seed to have room for Series A dilution. |

Top Seed Funding Sources and What They Offer

Unlike traditional lenders, seed capital comes from investors who take equity rather than charging interest. Here are the main sources and what to expect from each in 2026.

- Seed-stage VC firms (First Round Capital, Initialized Capital, Boldstart Ventures) write checks of $500K-$2M as lead investors. They typically want a board seat or board observer rights and expect to see a path to 10x+ return.

- Accelerators like Y Combinator invest $500,000 for 7% equity plus an uncapped MFN SAFE, plus mentorship and Demo Day access. Techstars invests $120,000 for 6% equity.

- Angel investors and super angels write individual checks of $25K-$500K. They are often former founders who bring operational experience and industry connections along with capital.

- Angel syndicates on platforms like AngelList pool capital from multiple angels, with a syndicate lead writing a single check of $100K-$1M on behalf of the group.

- Micro-VCs (Precursor Ventures, Hustle Fund, Contrary Capital) focus exclusively on pre-seed and seed, writing $100K-$500K checks with founder-friendly terms and faster decisions.

In practice, most seed rounds are filled by a combination of these sources. You typically secure one lead investor (a seed VC or well-known angel) who sets the terms, then fill the remaining allocation from angels, syndicates, and smaller funds.

Seed Round Sizes Vary Dramatically by Sector

AI startups command a median seed deal size of $4.6 million (a 1.3x premium over the broader market), while traditional SaaS startups raise $2-$3M and consumer apps raise $1.5-$2.5M. Healthcare startups also raise larger rounds (median $4.6M) due to regulatory requirements and longer development cycles. If you are in a capital-intensive vertical, benchmark against your specific sector, not the overall median.

What to Do If You Are Not Ready for Seed Funding

If investors tell you it is too early, or you do not yet have the traction metrics described above, you have several alternatives that can bridge you to seed readiness.

- Pre-seed funding ($50K-$1M). Raise a smaller round from angels, friends and family, or specialized pre-seed funds like Precursor Ventures or Hustle Fund. Read our pre-seed funding guide for current benchmarks.

- Accelerator programs. Y Combinator, Techstars, and 500 Global provide capital plus mentorship. Y Combinator's $500K investment is enough to reach seed-stage milestones for many startups.

- Small business grants. Non-dilutive capital from government programs (SBIR/STTR grants offer up to $1.5M) and private foundations. See our small business grants guide.

- Revenue-based financing or merchant cash advance. If you already have revenue, you can borrow against it without giving up equity. These options work well alongside an eventual seed round.

- Business credit cards. For very small expenses, a business credit card with a 0% intro APR can provide 12-15 months of float on purchases.

- Bootstrapping. Growing from revenue alone keeps you at 100% ownership. Some startups use a "seed strapping" approach, raising a tiny round for runway then growing primarily from revenue.

5 Seed Funding Mistakes That Can Sink Your Startup

1. Setting your valuation too high. An inflated seed valuation (say, $25M with minimal traction) makes Series A fundraising brutal. If your Series A valuation cannot exceed your seed valuation, you trigger a "down round" that damages investor confidence and founder equity. About 19% of all rounds on Carta in Q1 2026 were down rounds.

2. Giving away more than 30% equity at seed. If you give up 25% at pre-seed and another 25% at seed, you enter Series A negotiations with only 50% ownership. After Series A dilution (another 15-25%), you could drop below 35%, which makes it hard to retain control and motivate future hires with meaningful equity grants. Target 60-70% founder ownership after seed.

3. Stacking SAFEs with different caps and no MFN clause. Multiple SAFEs at different valuation caps create cap table complexity that surprises you at conversion. Post-money SAFEs are especially dilutive when stacked. Run pro forma cap tables modeling every SAFE converting at Series A before you sign anything.

4. Pitching before you have retention data. Seed investors now demand the data maturity that was previously reserved for Series A. If you cannot show user retention curves, cohort analysis, or at least 3-6 months of revenue data, you are pitching too early.

5. Ignoring SEC compliance. Seed rounds are securities transactions governed by SEC Regulation D. You must file Form D within 15 days of your first securities sale and verify that your investors meet accredited investor requirements. Failure to comply can result in rescission (returning all funds plus interest) and "bad actor" disqualification from future Reg D raises.

Protect Yourself Against Down Rounds

If you raise at a $20M valuation but your company only grows to a $15M valuation by Series A, your existing investors get diluted and your next round will include painful anti-dilution provisions. Price your seed conservatively enough that you can show genuine valuation growth in 12-18 months. A realistic $12M seed valuation that grows to $40M at Series A is far better for everyone than a $25M seed valuation that triggers a down round.

Step-by-Step Process

- 1

Incorporate as a Delaware C-Corp and set up your cap table

Most seed investors will only write a check to a Delaware C-Corporation because of its investor-friendly legal framework and predictable court system. If you have not yet incorporated, do this first. Set up a cap table tool (Carta, Pulley, or AngelList Stack) so you can model dilution before any conversations with investors.

Allocate a 10-15% employee option pool before your seed raise. Investors will expect this, and baking it in now prevents painful renegotiation later.

$500-$2,000 for incorporation and registered agent; $0-$100/month for cap table software 1-2 weeks Y CombinatorTips

- Use an online service to incorporate in Delaware for under $500, then register as a foreign entity in your home state.

- Set your authorized shares to 10 million to give yourself room for future rounds.

- Get 83(b) elections filed for any restricted founder stock within 30 days of issuance.

Common Mistakes

- Incorporating as an LLC instead of a C-Corp, which forces an expensive conversion before any VC will invest.

- Skipping the option pool, which means investors will insist on carving it from your shares at term-sheet stage.

- 2

Build your investor-readiness materials and validate key metrics

Seed investors in 2026 expect data, not just vision. Prepare a 10-12 slide pitch deck, a two-page executive summary, and a financial model covering 18-24 months of projections. The deck should lead with your traction slide (MRR, user growth, retention curves).

Target the metrics that move seed checks. For SaaS, that means $20K-$50K MRR at minimum, with month-over-month growth of 15-20%+. For consumer apps, show strong user growth and retention. Investors now demand proof of unit economics, including customer acquisition cost and lifetime value.

Tips

- Put your strongest metric on the title slide or slide two. If investors see traction immediately, they stay engaged.

- Build your financial model bottom-up from unit economics, not top-down from TAM percentages.

Common Mistakes

- Pitching before you have validated retention data. Investors now reject vision-only pitches at the seed stage.

- Over-projecting revenue by 5-10x without data to support the assumptions.

- 3

Build a target list of 50-80 seed investors and start warm outreach

Create a ranked list of 50-80 investors who actively write seed checks in your industry. Prioritize seed-stage VC firms (like First Round Capital, Initialized Capital, and Boldstart Ventures), micro-VCs, super angels, and accelerators like Y Combinator and Techstars.

Warm introductions convert at 5-10x the rate of cold emails. Work your network methodically: ask existing advisors, other founders, and LinkedIn connections for intros. Batch your meetings into a 2-3 week sprint so you can create urgency and compare term sheets.

$0-$500 for CRM tools and databases 2-3 weeks for list building; 4-8 weeks for active meetings signal.nfx.comTips

- Use AngelList, Crunchbase, and Signal by NFX to filter investors by stage, sector, and check size.

- Send no more than 15-20 cold emails per week. Focus your energy on getting warm intros.

- Track every interaction in a CRM or spreadsheet with columns for stage, next action, and follow-up date.

Common Mistakes

- Approaching Series A or growth-stage funds that do not write seed checks, wasting weeks of time.

- Trickling meetings over 3-4 months instead of compressing them, which kills urgency.

- 4

Secure a lead investor and negotiate your term sheet

Your lead investor sets the valuation, commits the largest check (typically 25-50% of the round), and signals credibility to other investors. Without a lead, filling the rest of your round becomes much harder.

For rounds under $4M, most leads will propose a SAFE (Simple Agreement for Future Equity) with a valuation cap. For larger rounds or rounds with complex cap tables, expect a priced equity round with preferred stock. Negotiate your valuation cap carefully. The median pre-money seed valuation is $16 million as of Q3 2026, but your number will depend on traction, sector, and team.

$0-$5,000 for legal review of term sheet 2-6 weeks from first meeting to signed term sheet Y CombinatorTips

- Download YC's free SAFE templates from ycombinator.com/documents to avoid unnecessary legal fees.

- Run dilution scenarios with at least three different valuation caps before agreeing to terms.

Common Mistakes

- Accepting a valuation cap that is too low out of urgency. A $6M cap on a $2M raise means giving up 25% immediately.

- Stacking multiple SAFEs with different caps and no MFN clause, which creates cap table confusion at Series A.

- 5

Close the round and file required SEC paperwork

Once your lead is committed, fill the remainder of the round by sharing the lead's term sheet with other interested investors. Most seed rounds close within 2-4 weeks after a lead commits, though some can take up to 8 weeks for the final checks.

After your first securities are sold, you must file Form D with the SEC within 15 days under Regulation D. Most seed rounds rely on the Rule 506(b) exemption, which lets you raise unlimited capital from accredited investors without public advertising. Work with a startup attorney to ensure compliance with both federal and state "blue sky" laws.

$3,000-$15,000 in legal fees for closing documents and SEC filing 2-4 weeks to close after lead commits; Form D due within 15 days of first sale SEC.govTips

- Wire instructions and signed documents should be ready before you send the closing email to all investors.

- File your Form D electronically through EDGAR. It is free and typically takes under an hour with attorney guidance.

- Send a closing update email to all investors within 48 hours of closing to start the relationship on a strong note.

Common Mistakes

- Missing the 15-day Form D filing deadline, which can jeopardize your Regulation D exemption status.

- Publicly advertising your raise on social media before closing, which violates Rule 506(b) restrictions.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| Legal fees (incorporation, SAFE/term sheet, closing) | $5,000-$25,000 | SAFEs cost $0-$2,000 using free YC templates; priced rounds cost $15,000-$25,000 in legal fees |

| Cap table management software | $0-$1,200/year | Carta, Pulley, and AngelList Stack offer free tiers for early-stage startups |

| Pitch deck design | $0-$5,000 | DIY with free templates or hire a designer for $2,000-$5,000 |

| SEC Form D filing | $0 (filing is free) | Attorney time for preparation is typically included in closing legal fees |

| Equity dilution (the real cost) | 15-25% of your company | At a $16M pre-money valuation, a $3M raise equals roughly 16% dilution |

Frequently Asked Questions

Plan to give up 15-25% of your company in a seed round. The median dilution at seed has been declining, with Carta reporting lower dilution percentages across stages in 2026. Aim to retain at least 60-70% total founder ownership after seed so you have room for Series A dilution (another 15-25%) and employee option grants.

A SAFE (Simple Agreement for Future Equity) has no interest rate, no maturity date, and is not debt. A convertible note is a loan that converts to equity, typically carrying 4-8% annual interest and a 12-24 month maturity date. SAFEs dominate seed rounds in 2026 (accounting for 92% of pre-priced rounds on Carta). Both use valuation caps and discount rates to determine how much equity the investor receives at conversion.

Most seed rounds take 3-6 months from first investor meeting to money in the bank. Well-connected founders with strong traction can close in 4-6 weeks. The fundraising timeline breaks down roughly as: 2-4 weeks for preparation, 4-8 weeks of active investor meetings, 2-6 weeks to negotiate and close with a lead, and 2-4 weeks to fill the remaining allocation.

Revenue is not technically required, but it dramatically improves your odds. In 2026-2026, most seed investors expect at least $300K-$500K ARR from SaaS startups, or strong user growth metrics for consumer companies. If you are pre-revenue, accelerators and pre-seed funds are better targets. Our pre-seed funding guide covers what investors look for at that stage.

The median pre-money seed valuation in the U.S. reached $16 million in Q3 2026, up 14% year over year according to Carta. AI startups can justify $20M+, while traditional SaaS typically lands at $8-$12M. Your specific valuation depends on traction, team strength, market size, and competitive dynamics.

Yes, but it is harder. Investors prefer teams of 2-3 co-founders because solo founders carry higher key-person risk. If you are raising solo, compensate by showing exceptionally strong traction, a track record of execution, and a clear plan for early hires that fill your skill gaps. Some accelerators (like Y Combinator) do accept solo founders.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Seed funding terms, valuations, and investor expectations vary by market conditions, sector, and individual circumstances. Consult a licensed financial advisor, CPA, or securities attorney before making equity or fundraising decisions. Data reflects industry benchmarks as of late 2026 and early 2026 and may change without notice.

Sources & References

- Carta: State of Private Markets Q1 2026

- Carta: State of Private Markets Q3 2026

- Carta: State of Pre-Seed Q3 2026

- Crunchbase: Seed Rounds Got Larger Through The Downturn

- Y Combinator: The Standard Deal

- Y Combinator: Guide to Seed Fundraising

- Pitchwise: Median Seed Round Size by Industry (2026)

- Metal: US SaaS Seed-Round Benchmarks 2026

- Flowjam: Seed Round Valuation 2026 Guide

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Seed Funding for Startups

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment