Business Credit Monitoring: Best Services and Why Every Owner Needs It

Business credit monitoring services start at $0/month. Compare Nav, Experian, and D&B plans with real pricing, score ranges, and step-by-step setup instructions.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What Business Credit Monitoring Actually Does

- Who Can Sign Up and What You Need

- How to Set Up Business Credit Monitoring Step by Step

- What Business Credit Monitoring Costs in 2026

- Top 5 Business Credit Monitoring Services Compared

- What to Do If Paid Monitoring Is Not in Your Budget

- 5 Business Credit Monitoring Mistakes That Cost Real Money

- FAQ

$0–$1,800

Est. Loan Cost

20 minutes

Timeline

5

Total Steps

Your business credit reports are public. Lenders, vendors, insurance companies, and even your competitors can pull them without asking your permission. Unlike personal credit (where the Fair Credit Reporting Act guarantees you free annual reports), no federal law requires free access to your business credit data.

Business credit monitoring tracks your scores and reports across the three major commercial bureaus (Dun & Bradstreet, Experian, and Equifax) so you can catch errors, spot identity theft, and protect your financing eligibility. Services range from $0 to $1,800+ per year depending on how many bureaus and features you need.

If you are working on building business credit, monitoring is the feedback loop that tells you whether your efforts are actually working. Without it, you are flying blind, and a single unreported error can cost you thousands in higher interest rates or denied applications.

What Business Credit Monitoring Actually Does

Business credit monitoring watches your company's credit files at one or more commercial bureaus and sends you alerts when something changes. This includes new credit inquiries, changes to your payment history, new accounts opened in your business name, legal filings (liens, judgments, UCC filings), and score fluctuations.

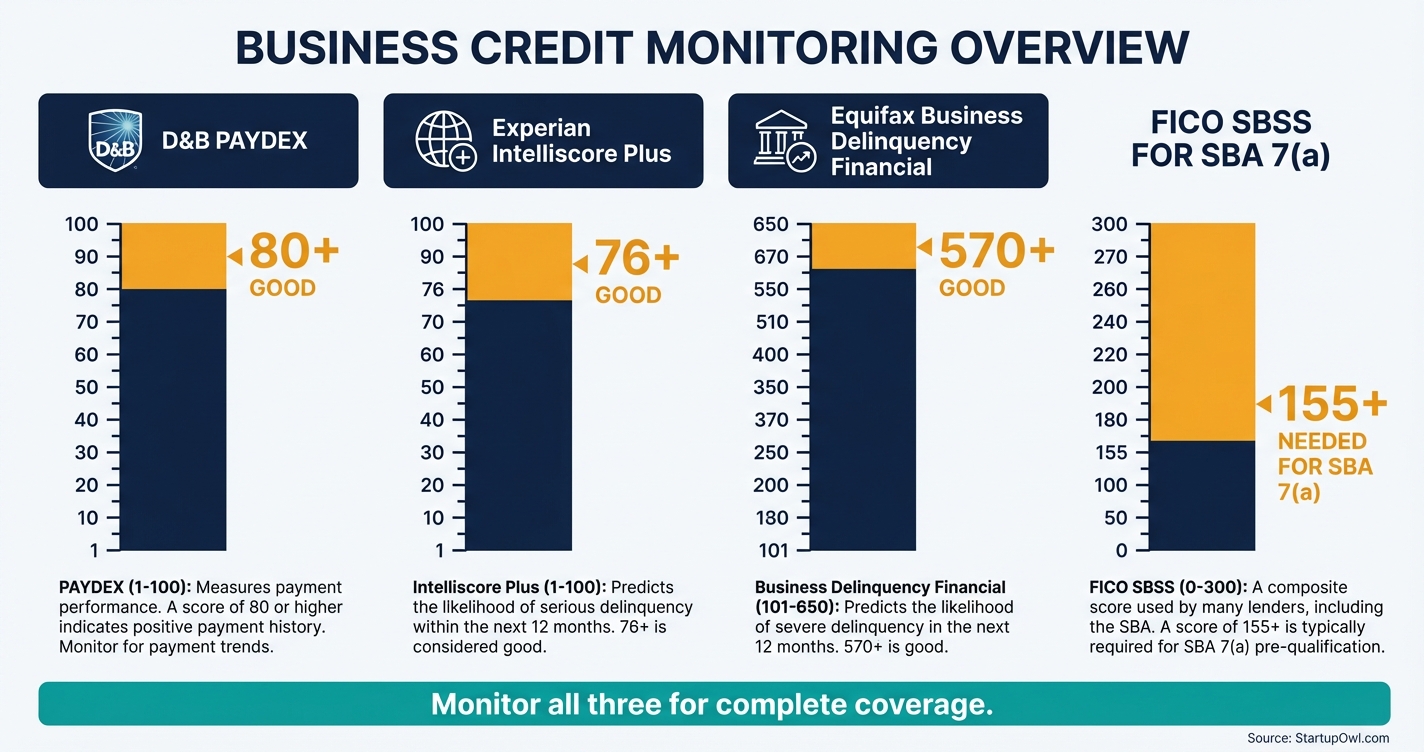

The three major business credit bureaus are Dun & Bradstreet (which issues the PAYDEX score), Experian (which issues the Intelliscore Plus), and Equifax (which issues the Business Delinquency Score). Each bureau collects different data and uses its own scoring model, so your scores can vary across all three.

Lenders use your business credit to decide whether to approve a business loan, set your interest rate, or determine your credit limit. Vendors use it to decide whether to extend trade credit (like net-30 payment terms). Insurance companies may also check it when setting premiums. A weak or inaccurate business credit file can cost you real money on every financial transaction your company makes.

Who Can Sign Up and What You Need

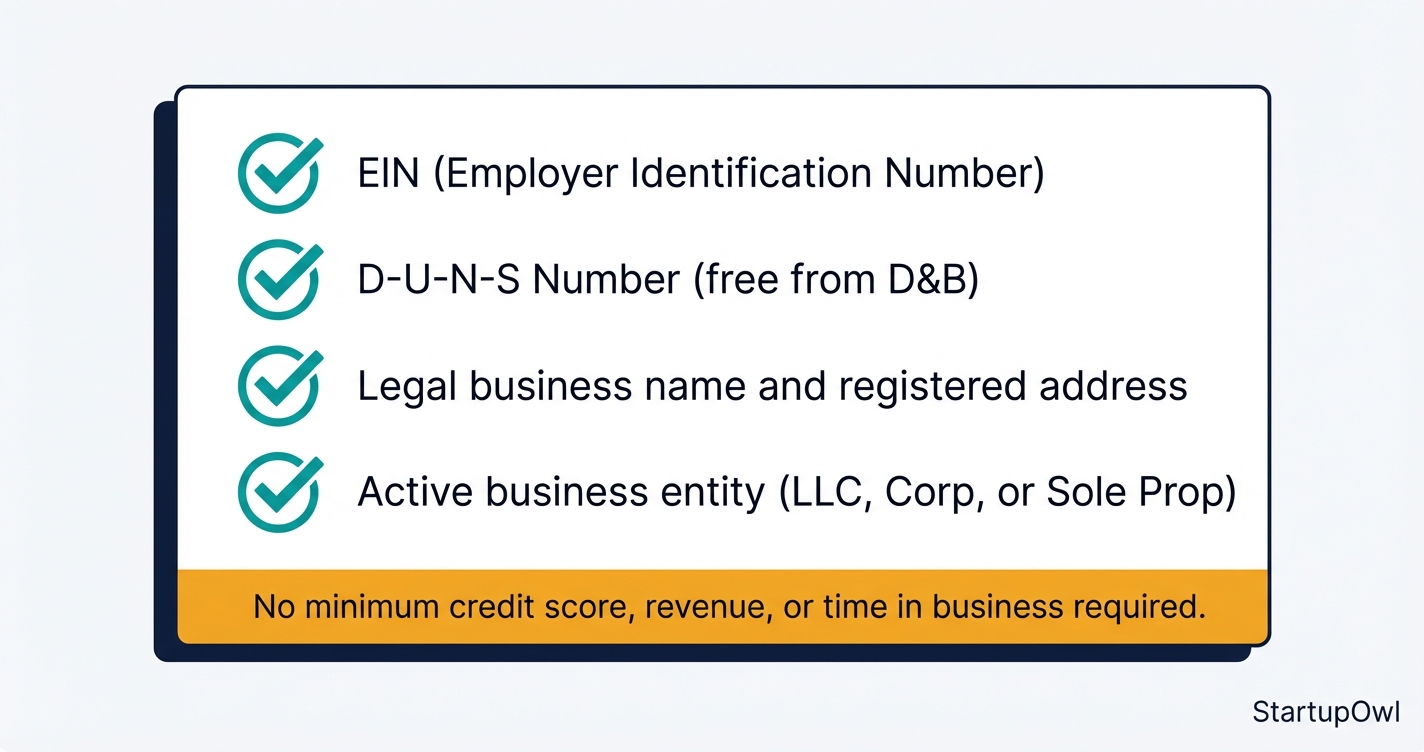

Any registered business with an Employer Identification Number (EIN) can sign up for business credit monitoring. You do not need a minimum credit score, revenue threshold, or time in business. Even brand-new businesses can (and should) start monitoring from day one.

To get the most value, you will need your legal business name, registered address, EIN, and (for D&B) your D-U-N-S Number. If you do not have a D-U-N-S Number yet, you can request one for free at Dun & Bradstreet, though it takes up to 30 days to process.

Sole proprietors can also monitor business credit, but your business credit score may be thinner since fewer accounts report under a sole proprietorship. If you have formed an LLC or corporation, your business entity is more likely to have a separate file at each bureau.

How to Set Up Business Credit Monitoring Step by Step

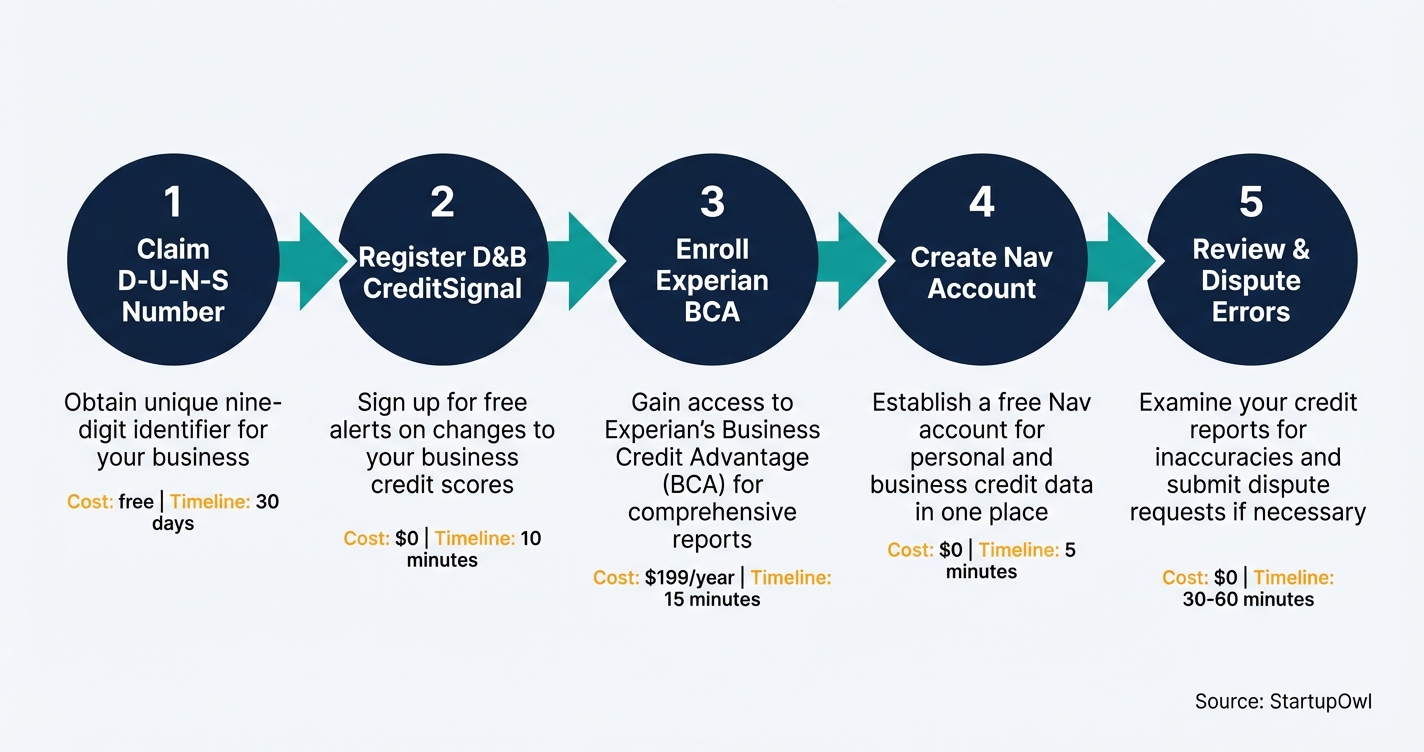

Getting started takes about 20 to 30 minutes spread across three to four platforms. The goal is to have at least basic monitoring on all three bureaus so nothing slips through the cracks. Here is the process:

Start by claiming your free D-U-N-S Number at dnb.com if you do not already have one. Then register for D&B CreditSignal (free) to get alerts on your PAYDEX, Delinquency Predictor, Financial Stress, and Supplier Evaluation scores.

Next, create a free Nav account to see summary reports from Experian and Equifax in one place. If you want exact numerical scores and detailed data, upgrade to Nav Prime starting at $39.99/month.

For the deepest Experian-specific coverage (including dark web surveillance), enroll in Experian Business Credit Advantage at $199/year. Finally, review every report for errors and file disputes directly with each bureau at no cost.

What Business Credit Monitoring Costs in 2026

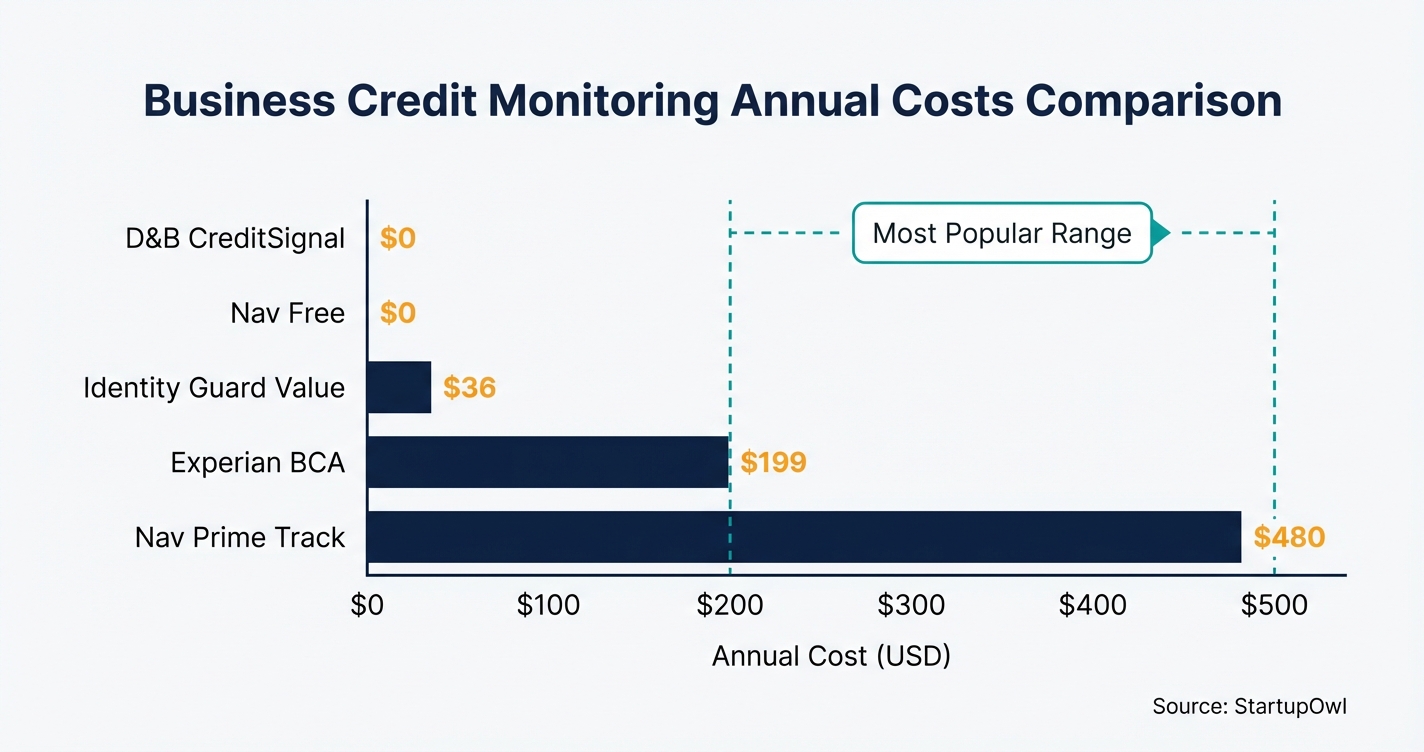

You can monitor your business credit for $0 if you combine Nav's free tier with D&B CreditSignal. The trade-off is that you get summary grades and directional alerts rather than exact numerical scores or detailed reports.

For full coverage, expect to spend $200 to $500/year. That typically means Experian Business Credit Advantage ($199/year) plus a D&B paid tier or Nav Prime. Purchasing individual reports directly from each bureau could cost more than $250/month, so bundled monitoring plans save you significantly.

At the premium end, D&B Credit Insights Plus runs $149/month (or $1,499/year) and Nav Prime Expand costs $79.99/month. Combined with Experian BCA, that pushes total monitoring spend above $1,800/year. Most small businesses do not need this level of coverage unless they are actively managing credit with multiple large vendors or lenders.

Business Credit Monitoring Service Pricing Comparison

| Type / Provider | Rate | Notes |

|---|---|---|

| D&B CreditSignal (Free) | $0/year | 14-day score preview, then directional change alerts only |

| D&B Credit Insights Basic | $499/year | Five D&B scores, legal events, dark web monitoring |

| D&B Credit Insights Plus | $1,499/year | Basic features plus competitor insights and extended history |

| Experian Business Credit Advantage | $199/year | Intelliscore Plus, inquiry alerts, CyberAgent dark web scan |

| Nav Free | $0/year | Summary grades from Experian and Equifax, personal VantageScore |

| Nav Prime Track | $480/year | Detailed multi-bureau scores, tradeline reporting |

| Nav Prime Build | $600/year | Track features plus charge card, checking, bookkeeping |

| Nav Prime Expand | $960/year | Build features plus FICO SBSS score and credit coach |

| Identity Guard Breach Response Value | $36/year | $1M identity theft insurance, dark web alerts |

| Identity Guard Breach Response Total | $120/year | Value features plus business bureau monitoring |

Top 5 Business Credit Monitoring Services Compared

1. Nav (Best Free Option for Multi-Bureau Access)

Nav is the only platform that shows you free business credit summaries from multiple bureaus in one dashboard. The free account gives you summary grades from Experian and Equifax, plus a personal VantageScore. Over 340,000 small businesses have used Nav Prime to build business credit, as of 2026. Nav Prime starts at $39.99/month (Track) and tops out at $79.99/month (Expand) for the FICO SBSS score and a dedicated credit coach. Visit Nav.

2. D&B CreditSignal / Credit Insights (Best for PAYDEX Monitoring)

D&B's free CreditSignal tool shows your PAYDEX, Delinquency Predictor, Financial Stress, and Supplier Evaluation scores for 14 days, then provides directional change alerts at no cost. The paid Credit Insights Basic tier ($49/month) unlocks five actual scores plus legal event data. Visit D&B CreditSignal.

3. Experian Business Credit Advantage (Best for Intelliscore Monitoring)

At $199/year, this plan gives you unlimited access to your Experian Intelliscore Plus, daily monitoring, weekly inquiry alerts, and CyberAgent dark web surveillance. The annual-only billing is a downside if cash flow is tight. Visit Experian BCA.

4. Identity Guard (Best Budget Business Identity Protection)

Identity Guard's Breach Response Value plan costs just $36/year and includes $1 million in identity theft insurance, breach alerts, and dark web monitoring. The Breach Response Total plan ($120/year) adds bank account and business bureau monitoring. Visit Identity Guard.

5. Creditsafe (Best for Monitoring Multiple Companies)

Creditsafe tracks D&B, Equifax, and its own proprietary scores with real-time alerts, competitor monitoring, and portfolio creation tools. Pricing is custom and typically suited for businesses that need to monitor their own file plus the files of clients or vendors they extend credit to. Visit Creditsafe.

Know Your Target Score Thresholds

A D&B PAYDEX score of 80+ signals on-time payments (1-100 scale). An Experian Intelliscore Plus of 76+ is low risk (1-100 scale). The FICO SBSS (0-300 scale) no longer carries an SBA minimum. SBA retired it for 7(a) small loans on March 1, 2026, and lenders that still pull it set their own cutoff. Check your scores against these benchmarks first.

What to Do If Paid Monitoring Is Not in Your Budget

If you cannot afford paid monitoring right now, start with the two free options: Nav's free tier (multi-bureau summaries) and D&B CreditSignal (PAYDEX change alerts). Together, these cover all three major bureaus at $0/year, though you will not get exact numerical scores after D&B's 14-day preview ends.

You can also pull a one-time Experian business credit report for about $40 to $100 (depending on the report type) without committing to the annual plan. If you are focused on personal credit first, explore free tools like AnnualCreditReport.com and work on building business credit with net-30 vendor accounts that report to the commercial bureaus.

If your goal is access to startup funding, check out our guides on business loans for startups, small business grants, and microloans for small business. Each of these options evaluates business credit differently, and understanding your file before applying improves your approval odds.

5 Business Credit Monitoring Mistakes That Cost Real Money

1. Ignoring your business credit entirely. Business identity theft can go undetected for months or even years because there is no requirement for bureaus to notify you of changes. One fraudulent account opened in your company's name could tank your PAYDEX from 80+ to below 50, moving you from low risk to high risk overnight.

2. Monitoring only one bureau. Each bureau collects different data and uses different scoring models. Your Experian Intelliscore might be 85 while your D&B PAYDEX sits at 65 because a vendor only reports to one bureau. If you only watch Experian, you will never see the D&B problem.

3. Never disputing errors. Incorrect addresses, outdated payment records, and misattributed UCC filings are common in business credit reports. An unresolved lien that does not belong to you can lower your scores and trigger automatic rejections on small business loan applications.

4. Confusing personal and business credit. Some scores (like the FICO SBSS and Experian Intelliscore) blend personal and business data. If your personal credit drops, your business scores can follow. Monitor both simultaneously, and keep your personal utilization below 30%. Our business credit score guide explains how these scores interact.

5. Paying for premium tiers you do not need. A brand-new sole proprietor with two vendor accounts does not need D&B Credit Insights Plus at $1,499/year. Start free, see what data exists on your business, and upgrade only when you have a specific reason (like preparing for an SBA loan or onboarding a major vendor).

Step-by-Step Process

- 1

Claim your free D-U-N-S Number from Dun and Bradstreet

Your D-U-N-S Number is a unique nine-digit identifier that anchors your business credit file at Dun & Bradstreet. You can request one for free at dnb.com, and it typically arrives within 30 days (or you can pay to expedite it).

Without this number, D&B cannot generate a PAYDEX score for your business, and many government contracts and large vendors require it. Make sure you enter your legal business name, address, and EIN exactly as they appear on your formation documents.

$0 (free request; expedited options available for $50-$250) 5 minutes to apply; 30 days to receive dnb.comTips

- Use your exact legal entity name and registered address to avoid duplicate files.

- Save your D-U-N-S Number somewhere secure because you will need it for every bureau check and government contract application.

Common Mistakes

- Applying with a DBA name instead of your legal entity name, which creates a second (orphan) credit file.

- 2

Register for D&B CreditSignal for free score change alerts

D&B's CreditSignal product lets you see your PAYDEX Score, Delinquency Predictor Score, Financial Stress Score, and Supplier Evaluation Risk Rating free for 14 days. After that, you get directional change alerts (up, down, or no change) at no cost.

If you want actual score numbers beyond day 14, you will need to upgrade to D&B Credit Insights Basic at $49/month (or $499/year), which gives you 24/7 access to five D&B scores and detailed legal event data.

$0 for CreditSignal; $49/month for D&B Credit Insights Basic 10 minutes to set up businesscredit.dnb.comTips

- Set a calendar reminder for day 12 of your free trial so you can screenshot your actual scores before they switch to directional-only.

- Check if your industry code (SIC/NAICS) is correct in the D&B file because errors here can skew your benchmarking data.

Common Mistakes

- Assuming CreditSignal gives you ongoing access to actual scores when it only shows them for 14 days.

- 3

Set up Experian Business Credit Advantage

Experian's Business Credit Advantage plan costs $199/year (roughly $16.58/month) and gives you unlimited access to your Experian Intelliscore Plus, email alerts on credit inquiries, and CyberAgent dark web surveillance, as of 2026.

This is an annual-only plan with no monthly payment option. You will receive weekly inquiry alerts every Tuesday and real-time change notifications. The plan also includes custom score improvement tips based on your specific credit profile factors.

Tips

- Verify that your SIC and NAICS codes are correct in Experian's file because your score is partly calculated relative to your industry average.

- Review your inquiry alerts each week to spot unauthorized pulls from companies you do not recognize.

- If $199 upfront is too steep, start with Nav's free tier to see your Experian summary first.

Common Mistakes

- Forgetting the plan auto-renews annually; set a reminder 30 days before your renewal date to cancel or keep.

- Expecting three-bureau coverage when Experian only shows you your Experian file.

- 4

Create a free Nav account for multi-bureau monitoring

Nav is the only platform that provides free business credit summaries from multiple bureaus in a single dashboard. Your free account includes summary credit reports from Experian and Equifax, a personal VantageScore, and basic financing recommendations.

If you want exact numerical scores, detailed bureau reports, and tradeline reporting, Nav Prime starts at $39.99/month for the Track plan. The Build plan ($49.99/month) adds the Nav Prime Card and bookkeeping tools. The Expand plan ($79.99/month) includes a dedicated credit coach and your FICO SBSS score.

$0 for free tier; $39.99 to $79.99/month for Nav Prime 5 minutes for free account; 10 minutes for Prime setup NavTips

- Start with the free tier to see where your business stands, then upgrade to Prime only if you need exact scores or tradeline building.

- If purchased separately, individual bureau reports could cost up to $250, so Nav Prime can be a better deal.

Common Mistakes

- Signing up for the most expensive tier before understanding what your free account already reveals.

- 5

Review your reports and dispute any errors

Once all your monitoring accounts are active, pull each report and look for incorrect business details, unfamiliar accounts, wrong addresses, or outdated information. Errors in business credit reports are not uncommon, and no federal law mandates free annual business credit reports the way AnnualCreditReport.com does for personal credit.

File disputes directly with each bureau. For Experian, visit BusinessCreditFacts.com. For D&B, use D-U-N-S Manager to request corrections free of charge. For Equifax, visit the Equifax small business portal. Plan to repeat this review monthly.

$0 (disputes are free) 30-60 minutes for initial review; 30-90 days for dispute resolution experian.comTips

- Keep documentation (invoices, bank statements) handy to support any disputes you file.

- Set a recurring monthly calendar event to review your business credit, just like you review your bank statements.

Common Mistakes

- Only checking once and never following up; disputes can take 30-90 days and sometimes require additional documentation.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| D&B CreditSignal (Free Tier) | $0 | Directional score change alerts only after 14-day preview period |

| D&B Credit Insights Basic | $49/month or $499/year | Five actual D&B scores, detailed legal events, dark web monitoring |

| D&B Credit Insights Plus | $149/month or $1,499/year | Everything in Basic plus insights on other businesses and extended data |

| Experian Business Credit Advantage | $199/year | Unlimited Intelliscore access, inquiry alerts, CyberAgent dark web scan |

| Nav (Free Tier) | $0 | Summary credit grades from Experian and Equifax, personal VantageScore |

| Nav Prime (Track Plan) | $39.99/month | Detailed multi-bureau scores, tradeline reporting, credit alerts |

| Nav Prime (Build Plan) | $49.99/month | Track features plus Nav Prime Card, business checking, bookkeeping tools |

| Nav Prime (Expand Plan) | $79.99/month | Build features plus FICO SBSS score and dedicated credit coach |

| Identity Guard (Breach Response Value) | $36/year | $1M identity theft insurance, breach alerts, dark web monitoring |

| Identity Guard (Breach Response Total) | $120/year | Value features plus monitoring of bank accounts and major business bureaus |

Frequently Asked Questions

You can monitor your business credit for $0/year using Nav's free tier and D&B CreditSignal together. For detailed scores and reports, expect to pay $199 to $600/year depending on which bureaus and features you select. Experian Business Credit Advantage is $199/year, and Nav Prime starts at $39.99/month.

Nav offers free summary credit reports from Experian and Equifax. D&B CreditSignal shows your PAYDEX and three other scores free for 14 days, then switches to directional change alerts. Unlike personal credit, there is no federal law that requires free business credit reports.

A D&B PAYDEX score of 80 or higher (on a 1-100 scale) signals on-time payments and low risk. An Experian Intelliscore Plus of 76 or higher is good. The FICO SBSS is different now. SBA retired its minimum for 7(a) small loans on March 1, 2026, so lenders that still use the score set their own bar.

Check your business credit reports at least once a month. If you have active monitoring with alerts enabled, you can review in real-time when changes occur. Before applying for any financing, pull fresh reports from all three bureaus so you know exactly what lenders will see.

Yes. Even sole proprietors can have business credit files, especially if you have an EIN, vendor accounts, or business credit cards. Monitoring helps you catch errors and build a stronger credit profile. If you plan to apply for a business loan, lenders may check your business credit regardless of your entity type.

Personal credit monitoring tracks your consumer files at TransUnion, Equifax, and Experian, which are governed by the FCRA. Business credit monitoring tracks your commercial files at D&B, Experian Business, and Equifax Business. Business credit reports are public (anyone can buy them), while personal credit reports require a permissible purpose to access.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. Pricing for monitoring services reflects publicly available data as of early 2026 and may change without notice.

Sources & References

- SBA Procedural Notice 5000-876777, Sunset of SBSS Score

- Nav Business Credit Monitoring

- Dun & Bradstreet CreditSignal

- D&B Credit Insights

- Experian Business Credit Advantage FAQ

- Experian Business Credit Monitoring

- FTC Fair Credit Reporting Act

- D&B PAYDEX Score and Business Credit Scores

- Business.org Best Business Credit Monitoring

- OptinMonster Best Credit Monitoring Services for Small Businesses

- Nav Prime Review (Credit Suite)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Business Credit Monitoring

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment