Contractor vs Employee Classification (1099 vs W-2)

How to classify workers correctly under IRS rules, avoid misclassification penalties, and understand the real cost difference between 1099 and W-2 hiring.

In This Article

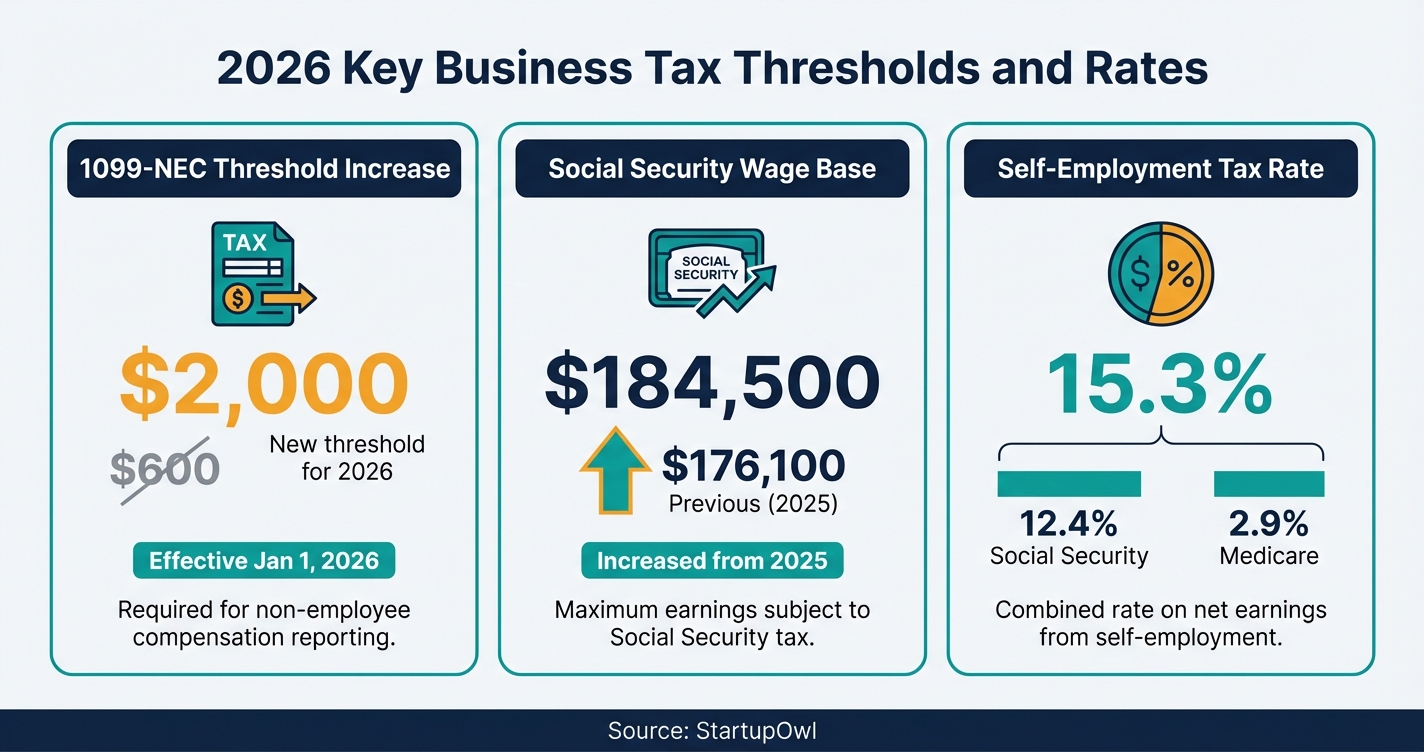

The IRS uses a 3-factor test (behavioral control, financial control, and type of relationship) to determine whether a worker is a W-2 employee or 1099 contractor. You cannot choose the classification for tax convenience. For 2026, the 1099-NEC reporting threshold increases from $600 to $2,000, and the Social Security wage base rises to $184,500. Misclassification penalties range from 1.5% to 3% of wages plus 40% of unpaid FICA taxes.

7

Total Steps

$0–$500

Est. Cost

1-3 hours per worker

Timeline

Medium

Difficulty

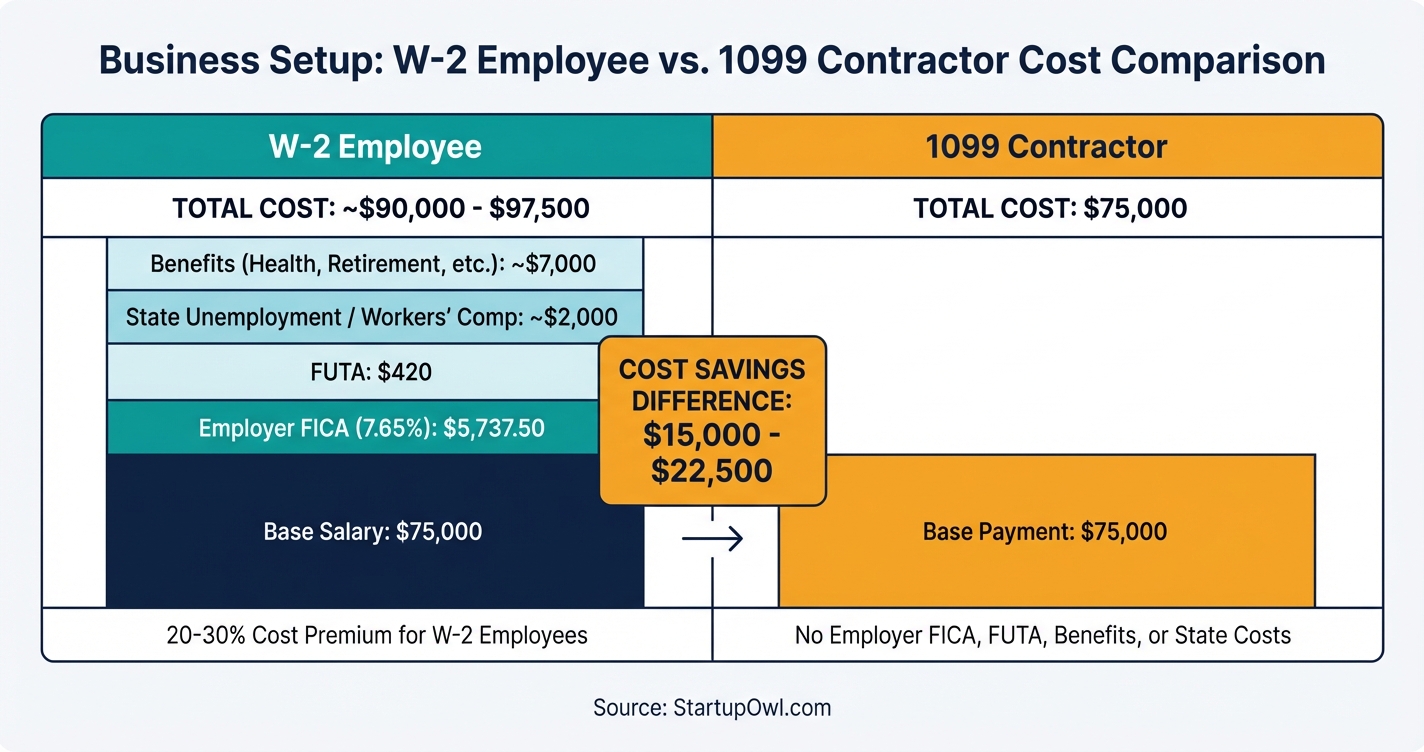

Hiring a $75,000 W-2 employee actually costs you $90,000 to $97,500 once you add employer FICA, unemployment insurance, workers' comp, and benefits. A 1099 contractor at the same rate costs exactly $75,000. That 20-30% difference tempts many founders to default to contractor status, but the IRS does not let you choose the classification that saves the most money.

Misclassification penalties start at 1.5% of wages under IRC Section 3509 and can climb to $1,000 per worker for intentional violations. This guide walks you through the IRS classification test, the 2026 reporting threshold changes under the One Big Beautiful Bill Act, and each step you need to take to classify and pay workers correctly from day one.

Before you classify your first worker, gather these items:

- Your EIN (Employer Identification Number). You need this for all tax filings. If you do not have one, apply free at IRS.gov (see our EIN application guide).

- A payroll system or accounting software. You will need a way to track payments, generate tax forms, and (for W-2 employees) calculate withholding. See our picks for best payroll services and best accounting software.

- Your business entity documents. Your LLC operating agreement or corporate bylaws may affect how you pay yourself. S Corp owners must take a reasonable W-2 salary before distributions.

- State-specific contractor rules. California, New Jersey, and Massachusetts use the ABC test, which is stricter than the federal IRS test. Check your state's labor department website.

If you plan to hire 5 or more workers in ambiguous roles, budget $200 to $500 for a one-time CPA consultation to review your classification decisions before onboarding.

Classifying a single worker takes 30 to 60 minutes if the role is clear-cut (a freelance designer on a 3-month project vs. a full-time office manager). Ambiguous cases can take weeks or months if you file Form SS-8 with the IRS, which has a processing time of 6 months or longer.

The hardest part is not the paperwork. It is being honest about the working relationship. Many founders want the cost savings of a 1099 contractor but the control of a W-2 employee. The IRS specifically looks for this mismatch. If you tell someone when to show up, how to do the work, and provide all the tools, that person is an employee regardless of what your contract says.

Expect to revisit classifications as your business grows. A contractor who starts with a 10-hour-per-week project may gradually shift to 40 hours of exclusive work. That transition often crosses the line into employee territory. Build an annual classification review into your December compliance checklist.

Step-by-Step Process

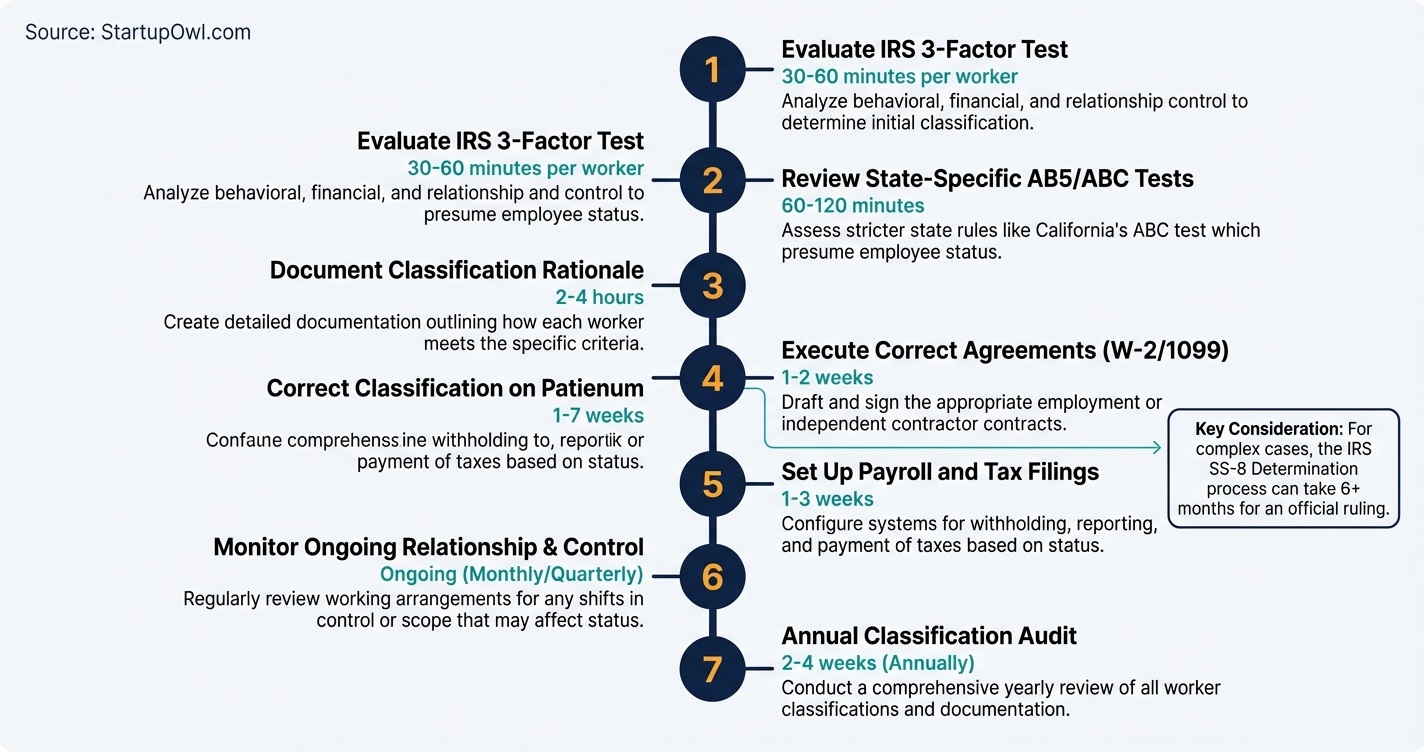

- 1

Evaluate the Working Relationship Using the IRS 3-Factor Test

Before you issue a single payment, run through the IRS classification framework. The IRS evaluates three categories: behavioral control (do you direct how, when, and where the work is done?), financial control (does the worker bear their own expenses and have opportunity for profit or loss?), and type of relationship (is this project-based or ongoing with benefits?).

No single factor decides classification. If you control the worker's schedule, provide their equipment, and expect them to work exclusively for you, the IRS will likely consider that person a W-2 employee. If the worker sets their own hours, uses their own tools, serves multiple clients, and delivers a defined project, they are more likely a 1099 contractor.

Review the IRS's independent contractor definition page for the full list of evaluation factors. Common myths to avoid: signing a contractor agreement does not override behavioral control, having an LLC does not determine classification, and worker preference is irrelevant to the IRS.

Tips

- Document your analysis in writing for every worker you classify, so you have a record if audited.

- Compare the role to similar positions at other companies using the IRS SS-8 database at irs.gov.

- If the worker only serves your company full-time and you provide all their tools, they are almost certainly a W-2 employee.

Common Mistakes

- Assuming a signed contractor agreement overrides the IRS behavioral control test.

- Letting the worker choose their own classification based on tax preference.

- 2

File Form SS-8 If the Classification Is Unclear

If you have reviewed the IRS guidelines and still cannot determine whether a worker is an employee or contractor, file Form SS-8 to request a formal IRS determination. Both businesses and workers can submit this form. There is no fee to file.

The IRS will review the facts of your working relationship and send you an official determination letter classifying the worker as either an employee or an independent contractor. Be aware that it can take at least 6 months to receive a decision. Do not wait for the determination to file your tax returns or make payments.

Filing Form SS-8 does invite IRS scrutiny on your classification practices, so weigh that risk. If you hire the same type of worker repeatedly, one SS-8 determination can cover the entire class. For details on completing the form, refer to the IRS instructions for Form SS-8.

$0 (IRS filing fee), $200-$500 if you use a CPA or attorney to help complete the form 6+ months for IRS determination IRS.govTips

- Search the IRS SS-8 database for determinations in your industry before filing your own.

- File your tax returns by the deadline regardless of whether you have received the SS-8 determination.

Common Mistakes

- Waiting for the SS-8 determination before filing your tax return or paying taxes owed.

- 3

Collect the Correct Onboarding Paperwork

The paperwork you collect depends entirely on the classification. For a 1099 contractor, collect a completed Form W-9 before you issue the first payment. The W-9 provides their legal name, address, and taxpayer identification number (TIN). You need this information to file 1099-NEC forms at year end.

For a W-2 employee, collect three forms: Form W-4 (for federal income tax withholding elections), Form I-9 (employment eligibility verification, required within 3 days of the hire date), and your state's withholding form if applicable. Set the worker up in your payroll system and begin withholding federal income tax, Social Security, and Medicare from the first paycheck.

If you are converting a contractor to employee status, have the worker complete the W-4 and I-9 immediately. Stop paying by invoice and begin running their compensation through payroll with proper withholding.

Tips

- Never issue a payment to a contractor without a completed W-9 on file first.

- Store W-9s and W-4s digitally in your payroll or accounting software for easy retrieval at tax time.

- For employees, the I-9 must be completed within 3 business days of the hire date.

Common Mistakes

- Paying a contractor $5,000 or more without collecting a W-9, then scrambling at tax time for their TIN.

- Failing to complete the I-9 within the 3-day window for new employees.

- 4

Set the Correct Compensation Structure

W-2 employees and 1099 contractors have fundamentally different cost structures. If you are converting a W-2 role to a contractor role (or vice versa), you must adjust the rate. A worker earning $100,000 as a W-2 employee needs approximately $130,000 as a 1099 contractor to maintain equivalent take-home pay, because they now absorb the full 15.3% self-employment tax, lose employer-sponsored benefits, and handle their own health insurance.

For contractors, set a flat project rate or hourly rate. Do not provide benefits, PTO, or equipment (doing so signals employee status to the IRS). For employees, account for the total cost: base salary plus 7.65% employer FICA, FUTA (up to $420/year), state unemployment taxes, workers' comp premiums, and any benefits you offer.

The 2026 Social Security wage base is $184,500, meaning both employer and employee pay 6.2% on earnings up to that cap, plus 1.45% Medicare on all earnings with no cap. If you use a payroll service, the software handles these calculations automatically.

$0 (no filing cost, but compensation adjustments affect your budget) 30 minutes to calculate ssa.govTips

- Use a total cost calculator to compare the actual cost of a W-2 employee vs. a contractor at the same output level.

- For contractors, build in a 30%+ rate premium over the equivalent W-2 salary to account for their added tax burden and lack of benefits.

Common Mistakes

- Offering a contractor the same flat rate as a W-2 salary without adjusting for their additional tax burden.

- Providing a contractor with company equipment, office space, or benefits, which signals employee status to the IRS.

- 5

Set Up Tax Withholding and Payment Processing

For W-2 employees, withhold federal income tax (per the employee's W-4), Social Security (6.2% up to the $184,500 wage base), and Medicare (1.45% on all wages) from every paycheck. You also pay the employer share: matching 6.2% Social Security, 1.45% Medicare, and FUTA at 6% on the first $7,000 of wages (reduced to 0.6% with the standard credit). Most states also require state income tax withholding and state unemployment contributions.

For 1099 contractors, do not withhold any taxes. Pay the contractor's invoice in full. The only exception is backup withholding at 24% if the contractor failed to provide a valid TIN on their W-9.

A payroll service like Gusto (starting at $46/month plus $6/employee) or QuickBooks Payroll handles withholding calculations, tax deposits, and year-end form generation. If you have both employees and contractors, look for a platform that manages W-2 and 1099 payments in one place. See our guide to setting up payroll for full setup instructions.

Tips

- Use payroll software to automate withholding calculations and avoid manual errors that trigger IRS penalties.

- Set up direct deposit for both employees and contractors to maintain clear payment records.

- Deposit withheld employment taxes on time (monthly or semi-weekly, depending on your deposit schedule) to avoid IRS late deposit penalties.

Common Mistakes

- Withholding taxes from a 1099 contractor's pay (this signals misclassification).

- Missing employment tax deposit deadlines, which triggers penalties starting at 2% of the unpaid amount.

- 6

File Year-End Tax Forms (1099-NEC and W-2)

For the 2026 tax year, file Form 1099-NEC for every contractor you paid $2,000 or more during the calendar year. This threshold increased from $600 to $2,000 under the One Big Beautiful Bill Act (OBBBA), effective for payments made in 2026. The 1099-NEC deadline is January 31, 2027, with no extensions available.

For employees, file Form W-2 for every person who received any wages during the year (there is no minimum threshold for W-2 filing). The W-2 filing deadline is also January 31, 2027. Send copies to workers, the Social Security Administration, and applicable state agencies.

You can file 1099-NEC forms for free using the IRS IRIS Taxpayer Portal. If you file 10 or more information returns of any type, electronic filing is mandatory. Your accounting software or payroll service can generate and e-file both W-2s and 1099s automatically.

Tips

- Collect W-9s from all new contractors before the first payment to avoid a scramble at filing time.

- Mark January 31 on your calendar now. The 1099-NEC deadline is firm with no extensions.

- Even if a contractor falls below the $2,000 threshold, the income is still taxable to them and you should maintain records.

Common Mistakes

- Using the old $600 threshold for 2026 payments, which creates unnecessary 1099 filings.

- Missing the January 31 deadline, which triggers late filing penalties starting at $60 per form (as of 2026 rates).

- 7

Audit Your Classifications Annually and Correct Mistakes Early

Worker relationships evolve. A contractor who started doing one-off projects may now work 40 hours per week exclusively for your company. Review every worker classification at least once per year. If a contractor's role has shifted to look more like an employee under the IRS 3-factor test, reclassify them and begin proper payroll withholding.

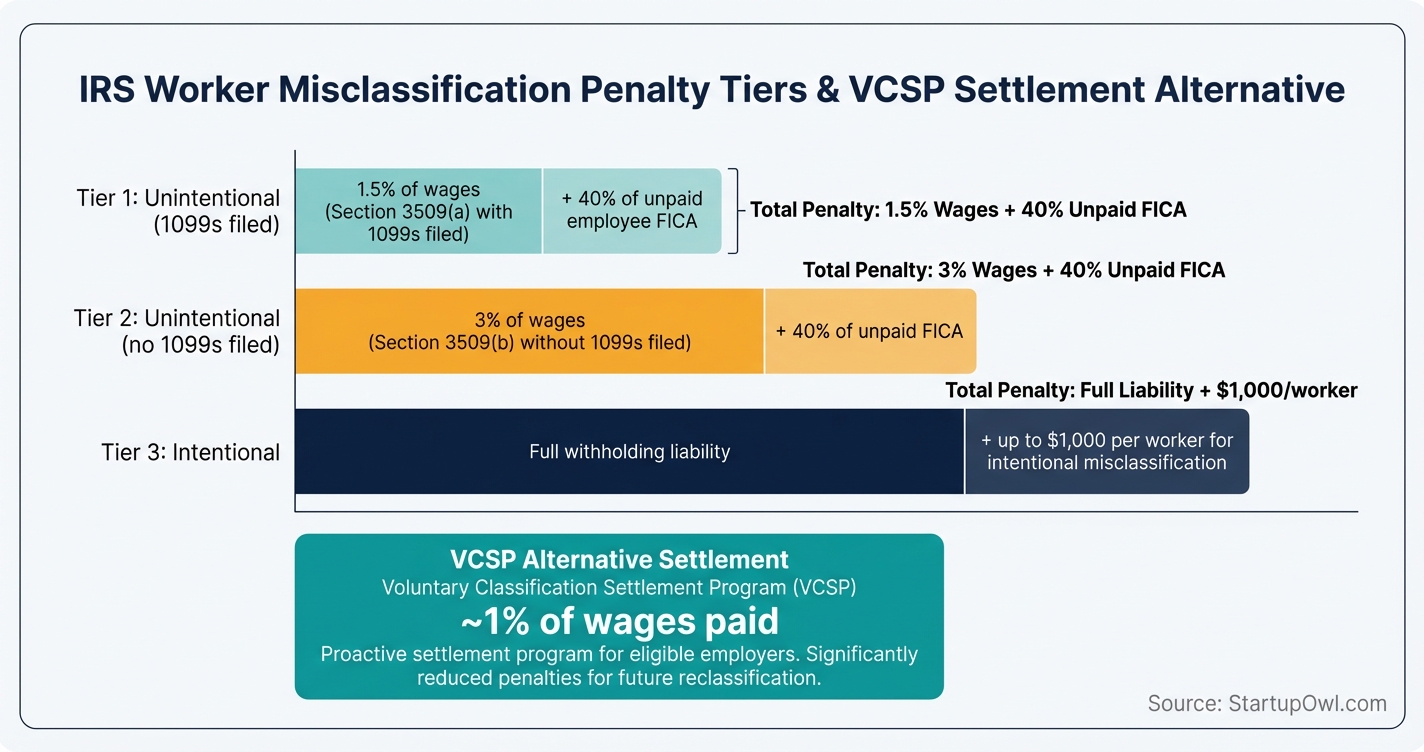

If you discover you have been misclassifying workers, the IRS Voluntary Classification Settlement Program (VCSP) lets you correct the error with minimal penalties. Through the VCSP, you pay just 10% of one year's employment tax liability (calculated at the reduced Section 3509 rates), with no penalties, no interest, and no audit of prior years for the reclassified workers. You must file Form 8952 at least 60 days before you start treating the workers as employees.

Without the VCSP, misclassification penalties include 1.5% of wages for income tax liability, 40% of the employee's unpaid FICA taxes, and potentially $1,000 per worker for intentional misclassification. States like California, New Jersey, and Massachusetts use the stricter ABC test, which presumes employee status unless you prove all three prongs. Consult a licensed CPA or employment attorney before converting worker classifications.

$0 for self-review; $200-$500/hour for CPA or attorney consultation 1-2 hours for annual review; VCSP process takes 60+ days IRS.govTips

- Schedule an annual classification audit every December before year-end filing deadlines.

- Keep written records of every classification decision, including the factors you considered.

- If you operate in California, New Jersey, or Massachusetts, apply the ABC test in addition to the IRS 3-factor test.

Common Mistakes

- Ignoring classification drift when a contractor gradually takes on employee-like responsibilities over time.

- Trying to correct misclassification on your own without consulting a CPA, which can trigger additional audit risk.

The direct cost of classifying workers is $0 if you do the analysis yourself. The real costs are in the ongoing payroll infrastructure and the potential penalties for getting it wrong.

For W-2 employees, employer-side costs add 20-30% on top of salary. On a $75,000 salary, expect to pay roughly $5,737 in employer FICA (7.65%), up to $420 in FUTA, state unemployment premiums (varies by state), workers' comp, and any benefits. Total employer cost: approximately $90,000 to $97,500.

For 1099 contractors, your cost is exactly what you pay them. But if you are converting a W-2 role to contractor status, increase the rate by at least 30% to give the worker equivalent take-home pay after their 15.3% self-employment tax burden.

Payroll software runs $40 to $100 per month for most small businesses. Free 1099 filing is available through the IRS IRIS portal. CPA consultations for classification reviews typically cost $200 to $500 per hour.

Once you have classified your workers and set up proper payment systems, take these next steps:

- Link payroll to your accounting software. Make sure employee wages and contractor payments flow automatically into your books. See our guide to setting up small business accounting.

- Set up workers' compensation insurance for W-2 employees. Most states require it. Review our business insurance guide for provider comparisons.

- Configure quarterly estimated tax reminders for 1099 contractors. While contractors handle their own taxes, you can help by providing payment summaries quarterly.

- Draft clear contractor agreements. Include scope of work, payment terms, deliverables, and intellectual property clauses. A well-written contract supports (but does not determine) your classification.

- Review your LLC vs S Corp tax comparison if you are paying yourself. S Corp owners must take a reasonable W-2 salary, and distributions above that salary avoid the 15.3% self-employment tax.

- Classifying someone as an employee starts a record keeping clock. Employees carry a Form I-9 and payroll records with retention rules that outlast the job, which contractors do not. The employee offboarding checklist sets out what you keep and for how long.

The Complete Checklist

- Review the IRS 3-factor classification test for each worker01

Evaluate behavioral control, financial control, and type of relationship before making any payment.

30-60 minutes per worker$0 - File Form SS-8 for any ambiguous classifications02

Request a formal IRS determination if the 3-factor test does not clearly resolve the worker's status.

6+ months for response$0 - Collect Form W-9 from every 1099 contractor03

Obtain the contractor's legal name, address, and TIN before issuing the first payment.

5 minutes per contractor$0 - Collect Form W-4, Form I-9, and state withholding forms from every W-2 employee04

Complete I-9 within 3 business days of hire and store all forms securely.

15 minutes per employee$0 - Set the correct compensation rate for each worker type05

Adjust contractor rates 30%+ above equivalent W-2 salary to account for self-employment tax and lost benefits.

30 minutes$0 - Set up payroll withholding for W-2 employees06

Configure your payroll system to withhold federal and state income tax, Social Security, and Medicare.

1-2 hours$40-$100/month for software - Establish contractor payment process (no withholding)07

Pay contractor invoices in full without withholding unless backup withholding applies.

30 minutes$0 - File 1099-NEC forms for contractors paid $2,000+ (2026 threshold)08

File by January 31 of the following year with no extensions available.

1-3 hours at year end$0-$10 per form - File W-2 forms for all employees09

File by January 31 of the following year to employees, SSA, and state agencies.

1-2 hours at year end$0-$10 per form - Conduct annual classification audit10

Review every worker's actual working relationship against the IRS test at least once per year.

1-2 hours$0-$500 (CPA optional)

These classification mistakes cost real money. Here is what to avoid:

Classifying all workers as 1099 to save on payroll taxes. The IRS estimates that 10-30% of employers misclassify workers. If caught, you owe back employment taxes at the Section 3509 reduced rate of 1.5% of wages for income tax withholding, plus 40% of the employee's unpaid FICA. Intentional misclassification removes the reduced rate and can trigger penalties up to $1,000 per worker.

Relying on a contractor agreement to determine status. A contract does not override the facts of the working relationship. The IRS evaluates what actually happens, not what the paperwork says. Labels do not override behavioral control.

Using the old $600 reporting threshold for 2026 payments. The 1099-NEC threshold increased to $2,000 for payments made in 2026 under the OBBBA. Filing unnecessary 1099s is not penalized, but using the wrong threshold could cause confusion and wasted effort.

Failing to adjust compensation when converting W-2 to 1099. A worker earning $100,000 as a W-2 employee needs approximately $130,000+ as a 1099 contractor to achieve the same take-home pay. Skipping this adjustment means your best contractors leave for better-paying gigs.

Ignoring state-specific classification tests. California, New Jersey, and Massachusetts use the ABC test, which presumes worker-employee status unless you prove all three prongs. State penalties stack on top of federal penalties.

Not using the VCSP when you discover a mistake. The Voluntary Classification Settlement Program lets you resolve misclassification by paying roughly 1% of wages owed, with no interest, no penalties, and no audit of prior years. Waiting until an IRS audit catches the error costs exponentially more.

Frequently Asked Questions

A W-2 worker is an employee whose taxes are withheld by the employer, who pays the 7.65% employer share of FICA. A 1099 worker is an independent contractor who handles their own taxes and pays the full 15.3% self-employment tax. The IRS determines classification based on behavioral control, financial control, and type of relationship.

The threshold increased from $600 to $2,000 for payments made in 2026, under the One Big Beautiful Bill Act (OBBBA). You only need to file a 1099-NEC for contractors you paid $2,000 or more during the calendar year. Starting in 2027, the threshold will adjust annually for inflation.

For unintentional misclassification with 1099s filed, the IRS applies Section 3509 reduced rates: 1.5% of wages for income tax plus 40% of unpaid employee FICA. Intentional misclassification can trigger penalties up to $1,000 per worker plus full employment tax liability. The DOL can also pursue back wages and overtime under the Fair Labor Standards Act.

A W-2 employee typically costs 20-30% more than the equivalent 1099 contractor rate. On a $75,000 salary, expect to pay roughly $90,000 to $97,500 after adding employer FICA ($5,737), FUTA ($420), state unemployment, workers' comp, and benefits. A 1099 contractor at $75,000 costs exactly $75,000.

Only if the working relationship genuinely changes to meet the IRS contractor criteria. You must stop controlling how, when, and where the work is done. Increase the pay rate by at least 30% to compensate for the worker's added 15.3% self-employment tax and lost benefits. Simply relabeling an employee as a contractor without changing the working relationship is misclassification.

The 2026 Social Security wage base is $184,500, up from $176,100 in 2026. Both employer and employee pay 6.2% on earnings up to this cap, for a maximum of $11,439 each. Medicare tax of 1.45% applies to all earnings with no cap.

Form SS-8 asks the IRS to make an official determination on whether a worker is an employee or contractor. It is free to file, but the response takes 6+ months. File it if you genuinely cannot determine classification using the IRS 3-factor test. Be aware that filing may invite additional IRS scrutiny on your classification practices.

The VCSP lets you correct past misclassification by paying approximately 1% of wages (10% of one year's employment tax liability at Section 3509 reduced rates), with no penalties, no interest, and no audit of prior years. File Form 8952 at least 60 days before you start treating the workers as employees.

Sources & References

- IRS - Independent Contractor Defined

- IRS - About Form SS-8

- IRS - Voluntary Classification Settlement Program

- IRS - Reporting Payments to Independent Contractors

- IRS IRIS Taxpayer Portal - E-File 1099 Forms

- Social Security Administration - Contribution and Benefit Base

- Littler - Tax Bill Changes 1099 Reporting Thresholds

- 26 U.S. Code § 3509 - Employer Liability for Employment Taxes

- IRS - Instructions for Form SS-8

About the Author

Senior Editor, Operations & HR

Mary has a background in human resources and organizational psychology. She spent years working in HR for rapidly scaling mid-western manufacturing and tech firms. She has seen firsthand how a lack of proper HR infrastructure can destroy a growing company from the inside out.

Was this article helpful?

Questions about Contractor vs Employee

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment