Self-Employment Tax for LLC Owners

The 2026 self-employment tax rate is 15.3% on net income. Here is exactly how it works, what you owe, and how to reduce it.

In This Article

Definition

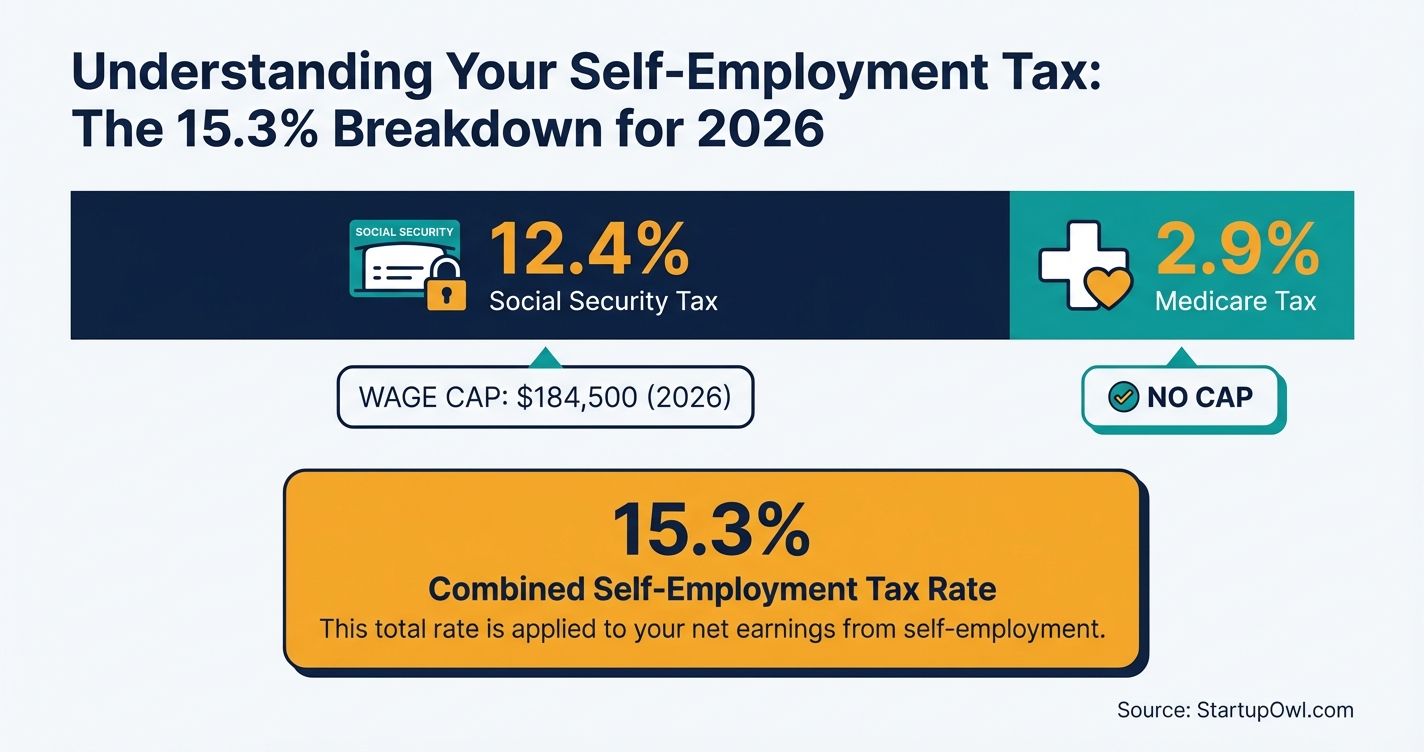

Self-employment tax is the 15.3% Social Security and Medicare tax you pay on your business profits when you work for yourself.

Self-employment tax is 15.3% of 92.35% of your net self-employment income. It covers Social Security (12.4%, capped at $184,500 in 2026) and Medicare (2.9%, no cap). You can deduct 50% of it on your Form 1040.

Self-employment tax costs you 15.3% of your net business income in 2026, and it is completely separate from federal income tax. On $100,000 in net profit, that is roughly $14,130 before you even calculate your income tax bill. This guide breaks down the rates, the math, and the specific strategies (including S Corp election) that can cut your SE tax by $5,000 to $8,000 per year.

$0 if net SE earnings are under $400 for the year

Free Option

$2,119 on $15,000 net SE income

Low-End

$14,130 on $100,000 net SE income

Mid-Tier

$28,222 on $200,000 net SE income (includes 0.9% Additional Medicare Tax above $200,000)

Premium

Self-employment tax is the Social Security and Medicare contribution you owe when nobody else is withholding those taxes from your paycheck. If you have an employer, you each pay 7.65% of your wages. When you are self-employed, you pay both halves, which totals 15.3%.

Think of it like this: the IRS sees your LLC profits the same way it sees wages from a job, except there is no employer splitting the bill with you. The 12.4% Social Security piece stops once your combined wages and SE income hit $184,500 in 2026. The 2.9% Medicare piece has no cap and applies to every dollar of net earnings.

A single-member LLC taxed as a sole proprietorship (the default) pays the exact same SE tax rate as an unincorporated sole proprietor. The LLC structure gives you liability protection, not a different tax rate. If you want to change how you are taxed, you need to file an LLC vs S Corp tax comparison election with the IRS.

On $100,000 of net business income, your self-employment tax alone is approximately $14,130. Add federal income tax (roughly $7,200 for a single filer at 2026 brackets after standard deduction), and you are looking at about $21,300 in combined federal taxes, an effective rate of roughly 21.3%. That number climbs to about $49,600 at $200,000 in net income.

Underpaying or ignoring SE tax is one of the most expensive mistakes new LLC owners make. The IRS expects quarterly estimated payments on this tax throughout the year. Miss those payments and you will owe penalties plus interest on top of the tax itself.

The good news: you can deduct 50% of your SE tax as an above-the-line adjustment on your Form 1040. That deduction lowers your adjusted gross income (AGI), which can reduce your income tax and affect eligibility for other tax benefits. But the deduction does not reduce the SE tax bill itself.

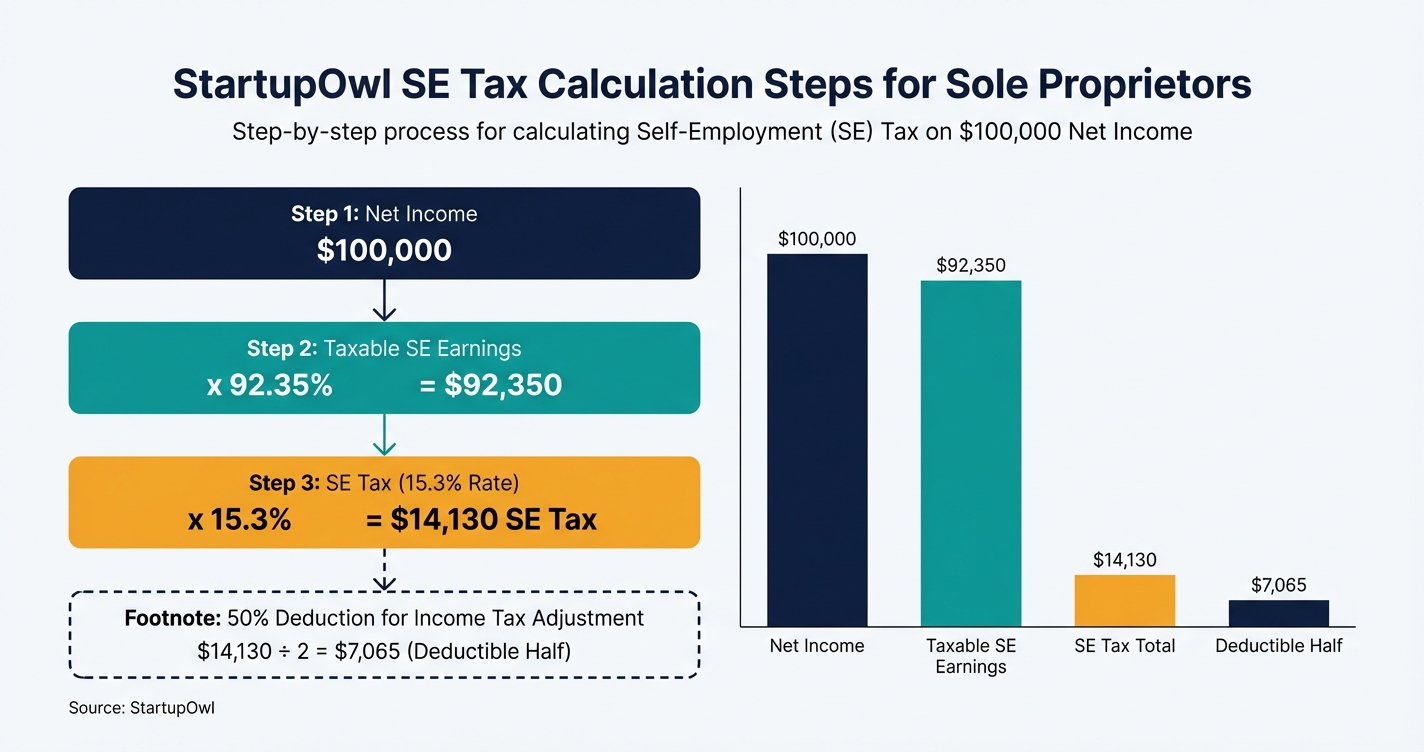

The calculation has three steps. First, take your net self-employment income from Schedule C (your revenue minus business expenses). Second, multiply that number by 92.35% (0.9235) to get your taxable SE earnings. This adjustment mimics the fact that employers can deduct their half of payroll taxes. Third, multiply that result by 15.3% (up to the Social Security cap).

Here is the math on $100,000 net income: $100,000 x 0.9235 = $92,350 in taxable SE earnings. Then $92,350 x 0.153 = $14,130 in SE tax. You can then deduct half of that ($7,065) when calculating your adjusted gross income on your 1040.

If your combined wages and SE income exceed $184,500, the 12.4% Social Security portion stops applying. You only owe the 2.9% Medicare tax on earnings above that cap. An additional 0.9% Medicare surtax kicks in for single filers above $200,000 ($250,000 for married filing jointly), bringing the Medicare rate to 3.8% on income above that threshold.

You report and calculate your SE tax on Schedule SE (Form 1040). Quarterly estimated payments are made using Form 1040-ES. For the 2026 tax year, those quarterly deadlines are April 15, June 16, September 15, 2026 and January 15, 2027.

You do not "sign up" for self-employment tax the way you open a bank account. If your net self-employment earnings exceed $400 in a tax year, you are required to pay it. Here is how to stay compliant:

- Step 1: Get your EIN from the IRS EIN online application (free, takes 10 minutes). You will need this for tax filings even if you have no employees. Our EIN application guide walks you through it.

- Step 2: Set up small business accounting to track income and expenses from day one. Accounting software like QuickBooks Self-Employed ($15/month) or Wave (free) will generate the numbers you need for Schedule C.

- Step 3: Estimate your quarterly tax payments using IRS Form 1040-ES. A rough shortcut: multiply your expected annual net profit by 30% to cover both SE tax and income tax, then divide by four.

- Step 4: Make payments by each deadline. You can pay at IRS.gov/payments using direct pay, EFTPS, or credit/debit card. The 2026 due dates are April 15, June 16, September 15 and January 15, 2027.

- Step 5: File Schedule SE with your annual Form 1040 to calculate the final SE tax amount and reconcile with your quarterly payments.

If you expect to earn more than $60,000 in net profit, talk to a CPA about whether an S Corp election makes sense. The potential savings of $5,000+ per year often outweigh the added accounting cost of $1,500 to $2,500 for tax return preparation and payroll processing.

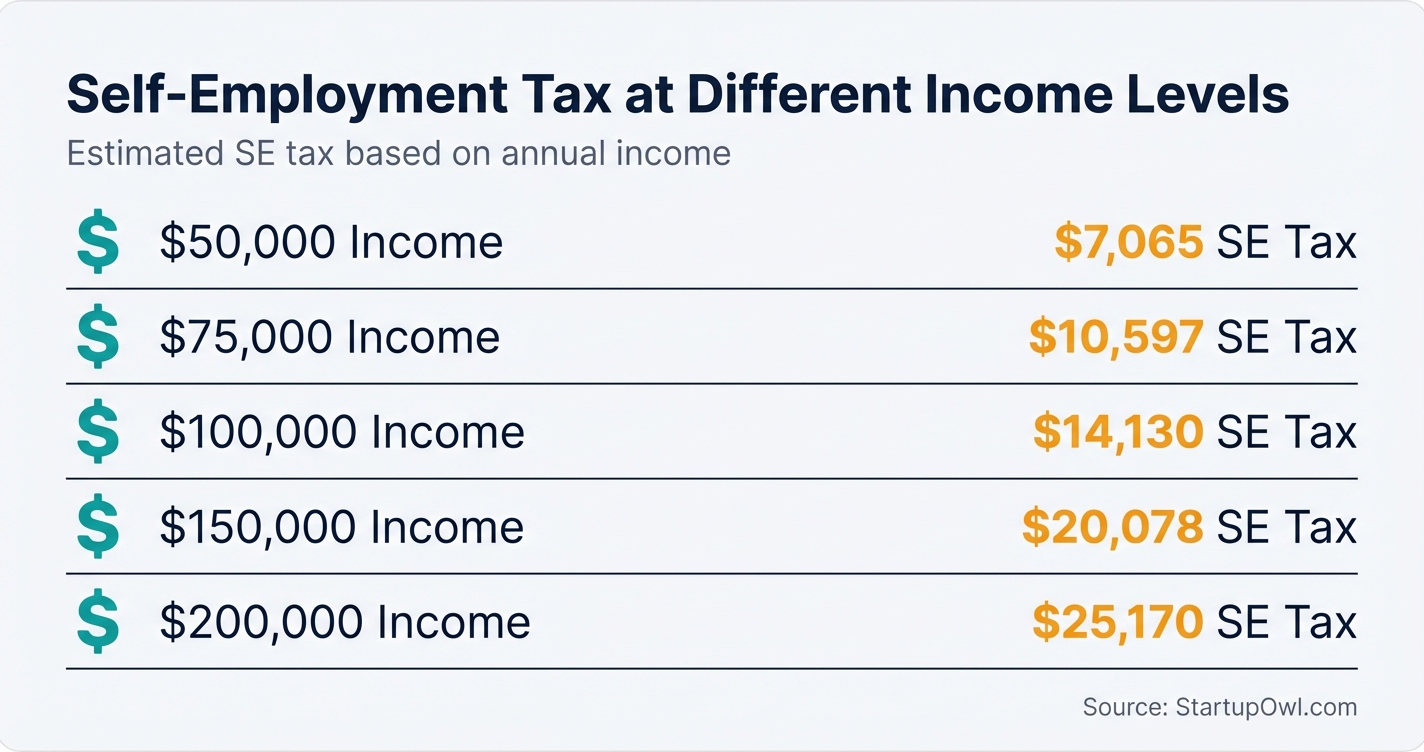

Your SE tax bill scales directly with your net profit. Here is what you can expect at common income levels (as of 2026):

- $50,000 net income: approximately $7,065 in SE tax

- $75,000 net income: approximately $10,597 in SE tax

- $100,000 net income: approximately $14,130 in SE tax

- $150,000 net income: approximately $20,078 in SE tax

- $200,000 net income: approximately $25,170 in SE tax

Those numbers represent SE tax only. Your federal income tax bill is on top of that. At $100,000, expect to pay roughly $21,300 total in combined SE and federal income taxes (for a single filer). At $200,000, that combined total approaches $49,600.

The biggest lever for reducing SE tax is how your LLC is taxed. Electing S Corp tax treatment lets you split income into salary (subject to payroll tax) and distributions (not subject to SE tax). At $100,000 net income, this strategy typically saves $5,000 to $8,000 per year. The tradeoff is added complexity: you will need to run payroll, file Form 1120-S, and pay yourself a reasonable salary that can withstand IRS scrutiny.

Freelancers and consultants: You pay SE tax on 100% of your Schedule C net profit. If your only income is freelance income, you are typically the best candidate for S Corp election once net profit consistently exceeds $60,000 to $75,000. Track every deductible expense (home office, software, professional development) because every $1,000 in deductions saves you roughly $141 in SE tax plus your marginal income tax rate.

E-commerce sellers: Your cost of goods sold (COGS) reduces net profit before SE tax applies. High-revenue, low-margin e-commerce businesses may have relatively modest SE tax bills. If your margins are above 20% and net profit exceeds $75,000, evaluate S Corp election.

Multi-member LLCs (partnerships): Each partner pays SE tax on their share of net partnership income shown on Schedule K-1. A two-member LLC with $200,000 in net income means each partner owes SE tax on their $100,000 share. Converting to an S Corp can potentially save the partnership $10,000 to $14,000 combined per year.

S Corp LLCs: If you have already elected S Corp tax treatment, you do not pay traditional SE tax. Instead, your reasonable salary is subject to standard payroll taxes (same 15.3% rate split between employer and employee portions). Distributions beyond your salary are not subject to payroll or SE tax. The key risk is setting your salary too low, which triggers IRS scrutiny.

Side-business owners with W-2 income: Your W-2 wages count toward the $184,500 Social Security cap. If your day job pays $150,000 in wages, only the first $34,500 of your SE income faces the 12.4% Social Security portion. The remaining SE income only owes the 2.9% Medicare tax. In this scenario, keeping your side business as a sole proprietorship (rather than electing S Corp) may actually make more financial sense.

1. Not making quarterly estimated payments. The IRS charges an underpayment penalty (currently tied to the federal short-term rate plus 3%) if you do not pay as you go. On a $14,000 SE tax bill, the penalty for missing all four quarterly payments can exceed $500.

2. Forgetting the 50% SE tax deduction. This above-the-line deduction reduces your adjusted gross income and your income tax. On $14,130 in SE tax, you would deduct $7,065. At a 22% marginal rate, that is roughly $1,554 in income tax savings you are leaving on the table.

3. Confusing SE tax with income tax. Many new LLC owners budget for a 22% to 24% income tax rate and forget that SE tax adds another 14% to 15% on top. Budget at least 30% of net profit for combined taxes to avoid a cash crunch at filing time.

4. Not tracking deductible business expenses. Every dollar of legitimate business expense reduces the net income subject to SE tax. Missing $5,000 in deductions costs you about $700 in SE tax plus your marginal income tax rate on that amount. Use accounting software and connect your business bank account to capture everything.

5. Ignoring the S Corp election for too long. At $100,000 in net profit, the difference between sole proprietorship SE tax and S Corp payroll tax is roughly $5,000 to $8,000 per year. Every year you delay that evaluation is potentially thousands of dollars lost. The election deadline is within 2 months and 15 days of the start of the tax year (by March 15 for calendar-year filers) using IRS Form 2553.

Frequently Asked Questions

The rate is 15.3% on 92.35% of your net self-employment income. On $100,000 in net profit, your SE tax is approximately $14,130. The Social Security portion (12.4%) caps at $184,500 in combined wages and SE income for 2026.

Yes, if your LLC is taxed as a sole proprietorship (the default for single-member LLCs) or a partnership (the default for multi-member LLCs). You can avoid traditional SE tax by electing S Corp status, which requires paying yourself a reasonable W-2 salary subject to payroll taxes instead.

The four deadlines are April 15, June 16, September 15, 2026 and January 15, 2027. You must pay if you expect to owe at least $1,000 in tax for the year after subtracting withholding and refundable credits.

At $100,000 in net profit, an S Corp election typically saves $5,000 to $8,000 per year by allowing you to split income between a reasonable salary (taxed at 15.3%) and distributions (not subject to SE tax). The savings increase as income rises, but so does the IRS scrutiny on your salary level.

The Qualified Business Income (QBI) deduction lets you deduct up to 20% of your qualified business income from your federal income tax. For 2026, the full deduction is available to single filers below roughly $200,000 in taxable income ($400,000 married filing jointly). The QBI deduction reduces income tax but does not reduce self-employment tax.

You can deduct 50% of your SE tax as an above-the-line adjustment on your Form 1040, Schedule 1, Line 15. This reduces your adjusted gross income and your income tax. It does not reduce the SE tax itself.

Sources & References

- IRS - Self-Employment Tax (Social Security and Medicare Taxes)

- IRS Form 1040-ES (2026) - Estimated Tax for Individuals

- IRS Publication 509 (2026) - Tax Calendars

- Social Security Administration - Contribution and Benefit Base

- MJC PA - Social Security Wage Base 2026 and Self-Employment Tax

- SDO CPA - Self-Employment Tax 2026 Rates, Calculation and How to Reduce

- 1800Accountant - FICA Tax Rates in 2026

- Millan CPA - 2026 IRS Tax Calendar Deadlines and Forms

- Millan CPA - 2026 Business and Pass-Through Tax Rules (QBI, SALT)

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Self-Employment Tax

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment