How to Make Quarterly Estimated Tax Payments in 2026

Calculate what you owe, pick a payment method, and file on time. This step-by-step guide covers deadlines, safe harbor rules, and how to avoid the 7% underpayment penalty.

In This Article

Your 2026 quarterly estimated tax payments are due April 15, June 15, September 15, and January 15, 2027. The easiest way to calculate your payment is to take 100% of last year's total tax liability (110% if your AGI exceeded $150,000) and divide by four. Pay for free through IRS Direct Pay or EFTPS.

6

Total Steps

$0–$50

Est. Cost

1-3 hours (first time); 15-30 minutes per quarter after that

Timeline

Medium

Difficulty

If you expect to owe $1,000 or more in federal taxes for 2026, you need to make quarterly estimated tax payments. Missing even one payment triggers the IRS underpayment penalty, which currently runs at 7% annually (compounded daily) on the shortfall. This guide walks you through every step, from calculating your quarterly amount to submitting your payment through IRS Direct Pay or EFTPS.

Before you calculate your first quarterly payment, you need three things on hand.

- Your 2026 federal tax return (Form 1040). You will need the total tax (line 24), your AGI (line 11), and the total withholding (line 25a). These numbers power the safe harbor calculation.

- An estimate of your 2026 income. If you use accounting software, pull a year-to-date profit-and-loss report. If this is your first year, project monthly revenue and subtract expected expenses.

- Your EIN or Social Security number. You will need one of these to make a payment through IRS Direct Pay or EFTPS. If you have not applied for an EIN yet, see our EIN application guide.

You should also check whether your state requires separate estimated tax payments. Most states with an income tax (California, New York, Illinois, etc.) follow similar quarterly schedules but may have different thresholds. Texas, Florida, Wyoming, and a handful of other states have no individual income tax.

Your first quarterly tax calculation takes 1 to 3 hours if you work through the Form 1040-ES worksheet from scratch. After that, each quarter takes 15 to 30 minutes because you are only adjusting numbers and submitting a payment.

The trickiest part for new business owners is estimating income accurately. In year one, you will almost certainly over- or underpay. That is normal. The safe harbor method protects you from penalties even if your estimate is off, as long as you pay 100% of your prior-year tax (110% if AGI exceeded $150,000). If you overpay, the IRS issues a refund when you file your annual return (typically within 21 days of e-filing).

Expect to receive confirmation numbers from each payment. Save these. If the IRS ever questions whether you paid on time, your confirmation number is your proof. EFTPS stores 15 months of payment history in your account; IRS Direct Pay does not store history, so take a screenshot or request the email confirmation.

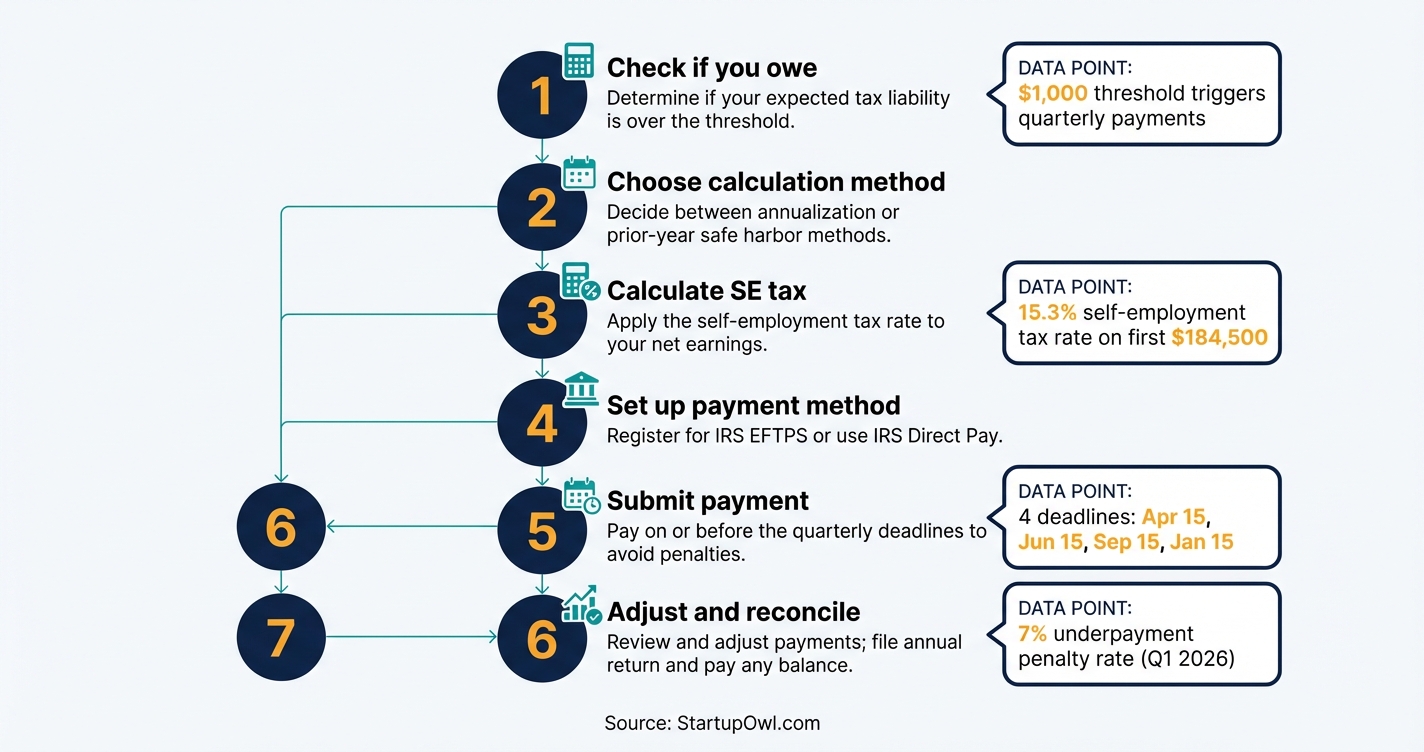

Step-by-Step Process

- 1

Determine Whether You Must Pay Estimated Taxes

The IRS requires quarterly estimated tax payments if you expect to owe $1,000 or more in federal taxes after subtracting withholding and refundable credits. If your withholding and credits will cover at least 90% of your 2026 tax liability (or 100% of your 2026 liability), you are safe. For higher earners with an adjusted gross income above $150,000 ($75,000 if married filing separately), the prior-year threshold jumps to 110%.

You do not owe estimated taxes if you had zero tax liability for the full 12-month 2026 tax year and were a U.S. citizen or resident alien for all of 2026. Common situations that trigger quarterly payments include self-employment income, freelance or gig work, rental income, and significant investment gains. If you earn $400 or more from self-employment, your earnings are subject to the 15.3% self-employment tax in addition to income tax.

Tips

- If this is your first year in business with no prior-year return, use the current-year method (90% of projected 2026 tax) to estimate your payments.

- S corporation owners who pay themselves a reasonable salary via payroll can often cover most of their tax liability through W-2 withholding, reducing or eliminating the need for quarterly payments.

Common Mistakes

- Assuming you only owe income tax. Self-employment tax (15.3% on the first $184,500 of net earnings for 2026) is a separate obligation included in your estimated payment.

- Forgetting state estimated taxes. Most states with an income tax also require quarterly payments with their own thresholds and deadlines.

- 2

Choose Your Calculation Method (Safe Harbor or Current Year)

You have two calculation methods. The prior-year safe harbor method is the simplest and guarantees you avoid the underpayment penalty. Take your total tax from last year's Form 1040, multiply by 100% (or 110% if your AGI exceeded $150,000), and divide by four. If you owed $20,000 last year with an AGI under $150,000, each quarterly payment is $5,000. With an AGI over $150,000, it becomes $5,500 per quarter.

The current-year annualized method is more accurate if your income varies significantly. Estimate your total 2026 income (business profit, dividends, interest, capital gains, rental income), subtract expected deductions, calculate the tax, subtract any withholding, and divide the remainder by four. Download Form 1040-ES for the IRS worksheet that walks you through this calculation line by line.

Tips

- The prior-year safe harbor method works best when your income is stable or growing. You will get a refund if you overpay, so think of it as forced savings.

- If your income swings quarter to quarter (common for seasonal businesses), use Form 2210 Schedule AI (Annualized Income Installment Method) to align payments with when income was actually earned.

Common Mistakes

- Using last year's numbers for the current-year method without updating for 2026 tax bracket thresholds and the new $184,500 Social Security wage base.

- 3

Calculate Your Self-Employment Tax Component

If you are a sole proprietor, single-member LLC, or partnership member, self-employment (SE) tax is a major part of your quarterly payment. The SE tax rate is 15.3% on the first $184,500 of net self-employment income for 2026 (12.4% Social Security + 2.9% Medicare). Income above that threshold is subject only to the 2.9% Medicare tax. If your total earnings exceed $200,000 (single) or $250,000 (married filing jointly), an additional 0.9% Medicare surtax applies.

To calculate, multiply your net business profit by 0.9235 (this adjustment mirrors the employer-side FICA deduction). Then multiply the result by 0.153 for the SE tax amount. You can deduct half of your SE tax as an above-the-line deduction on Schedule 1, which reduces your AGI. For example, if your net profit is $80,000, your SE tax is roughly $11,304 (about $2,826 per quarter), and your income tax comes on top of that.

Tips

- An S Corp election can save $5,000 to $8,000 per year in SE tax if your net income is around $100,000, because only your reasonable salary (not distributions) is subject to payroll tax. See our LLC vs S Corp tax comparison for details.

- Track business expenses carefully. Every deductible dollar reduces both your income tax and your SE tax.

Common Mistakes

- Treating SE tax as optional. The IRS considers self-employment tax part of your total estimated tax obligation, and underpaying it triggers the same 7% penalty.

- Forgetting the 0.9235 multiplier. Applying 15.3% to your full net profit will overstate your SE tax.

- 4

Set Up Your Payment Method Before the First Deadline

The IRS offers several free and paid ways to submit your quarterly payment. IRS Direct Pay is the fastest option for individuals. It pulls funds directly from your bank account with no fee, and you can schedule a payment up to 30 days in advance. EFTPS (Electronic Federal Tax Payment System) allows you to schedule payments up to 365 days ahead and is required for business entity payments. Enrollment takes about 5 to 7 business days because the IRS mails a PIN to your address.

You can also pay by credit or debit card through IRS-approved processors (Pay1040 and ACI Payments), but you will pay a processing fee of 1.75% to 2.95% on credit cards or about $2.50 on debit cards. Mailing a check with a Form 1040-ES voucher still works but offers no confirmation and risks postal delays. For most business owners, IRS Direct Pay or EFTPS is the best combination of free, fast, and trackable.

$0 (Direct Pay/EFTPS); 1.75%-2.95% fee per payment (credit card) 10 minutes (Direct Pay); 5-7 business days for EFTPS enrollment IRS.govTips

- Register for EFTPS early, even if you do not need it yet. Having the account ready means you can schedule all four quarterly payments at once.

- If you use EFTPS, set calendar reminders for 2 business days before each due date. EFTPS requires at least 1 business day lead time for ACH processing.

Common Mistakes

- Waiting until the deadline day to enroll in EFTPS. The PIN arrives by mail in 5-7 days, so you will miss the payment window if you start on the due date.

- 5

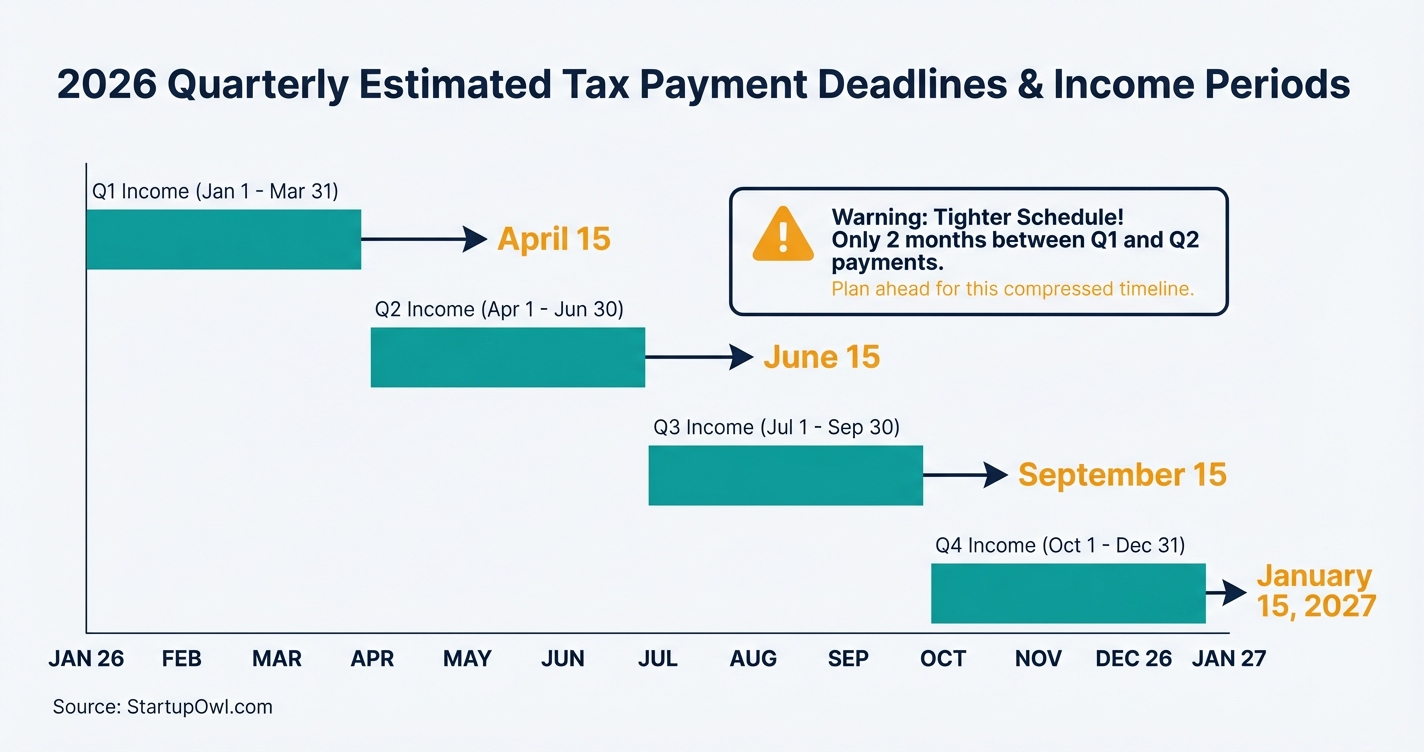

Submit Your First Quarterly Payment by April 15

Your 2026 quarterly payment deadlines are April 15, June 15 (note: only 2 months after Q1), September 15, and January 15, 2027. If any date falls on a weekend or federal holiday, the deadline shifts to the next business day. For 2026, June 15 falls on a Monday, so no adjustment is needed. The Q2 deadline of June 15 for the 2026 tax year is confirmed at June 16 (Monday) since June 15 is a Sunday.

Log in to IRS Direct Pay or EFTPS, select "Estimated Tax" as the payment type, choose tax year 2026, and enter your calculated quarterly amount. Save or print your confirmation number. You can also pay all four quarters up front by the April 15 deadline if cash flow allows. The IRS accepts more frequent payments (monthly, biweekly, etc.) as long as the full quarterly amount is covered by each due date.

Tips

- Set up automatic monthly payments equal to 1/12 of your annual estimate. Twelve smaller payments are easier on cash flow than four large ones.

- Keep a spreadsheet or use your accounting software to track actual income each quarter. If your Q2 income spikes, you can increase your Q3 payment to avoid an underpayment for that period.

Common Mistakes

- Missing the June 15 deadline because you assumed all quarters are 3 months apart. Q2 is due only 2 months after Q1.

- Paying a lump sum in Q4 instead of spreading payments evenly. The IRS calculates the penalty per quarter, so late Q1-Q3 payments still trigger penalties even if your total for the year is correct.

- 6

Adjust Your Payments Each Quarter and Reconcile at Year-End

Review your actual income against your estimates at the end of each quarter. If your business earned significantly more (or less) than expected, recalculate using the Form 1040-ES worksheet and adjust your next payment. You can increase or decrease future quarterly payments at any time without filing anything extra with the IRS.

At year-end, your total estimated payments (plus any W-2 withholding) should equal at least 90% of your 2026 tax liability or 100% (110% for high earners) of your 2026 liability. When you file your annual return, report all estimated payments on Form 1040 line 26. If you overpaid, you can apply the excess to your 2027 estimated taxes or receive it as a refund. Use your accounting software to run a profit-and-loss report each quarter so your estimates stay accurate.

Tips

- If your income is wildly uneven, file Form 2210 with Schedule AI at tax time. This proves to the IRS that your payment pattern matched your income pattern, and it can eliminate or reduce penalties.

- Consider hiring a CPA for your first year of estimated taxes. A 1-hour consultation (typically $150 to $300) can prevent costly calculation errors.

Common Mistakes

- Never adjusting after the first quarter. If your income doubles in Q3, your Q1-Q2 payment amount will not be enough and you will owe a penalty on the shortfall.

Filing and paying your quarterly estimated taxes costs $0 when you use IRS Direct Pay or EFTPS. The IRS does not charge a fee to receive estimated tax payments. Credit card payments incur a 1.75% to 2.95% processing fee through third-party processors like Pay1040 or ACI Payments, so a $5,000 payment would cost an extra $87.50 to $147.50 in fees. Debit card payments carry a flat fee of about $2.50.

The real cost risk is the underpayment penalty. As of Q1 2026, the IRS charges 7% annual interest (compounded daily) on any underpaid amount for each quarter. If you missed a $5,000 Q1 payment and did not pay until Q3 (roughly 150 days late), the penalty would be approximately $144. That penalty applies even if you overpay later in the year or are owed a refund when you file your annual return.

After you submit your first quarterly payment, take these follow-up steps to stay on track for the rest of the year.

- Set calendar alerts for all four deadlines. April 15, June 15, September 15, and January 15 (2027). Add a reminder 7 days before each date so you have time to review your numbers.

- Connect your bank account to accounting software. Tools like QuickBooks, Wave, or FreshBooks can categorize income and expenses automatically, making your quarterly recalculation take minutes instead of hours.

- Open a dedicated tax savings account. Transfer 25% to 30% of every business payment you receive into a separate high-yield savings account. This ensures you always have cash on hand when the quarterly bill arrives. See our guide on how to open a business bank account for recommended options.

- Track estimated payments in your books. Record each payment as a draw or owner distribution (not a business expense) in your accounting system. Estimated taxes are personal tax payments, not deductible business expenses.

- Evaluate your entity structure annually. If your net self-employment income consistently exceeds $50,000 to $60,000, an S Corp election could reduce your self-employment tax by $5,000 to $8,000 per year by splitting income between salary and distributions.

The Complete Checklist

- Determine if you owe quarterly estimated taxes01

Check whether you expect to owe $1,000 or more after withholding and credits.

15 minutes$0 - Gather your prior-year tax return (Form 1040)02

You need last year's total tax liability, AGI, and withholding totals for the safe harbor calculation.

5 minutes$0 - Download Form 1040-ES from IRS.gov03

The form includes the worksheet, tax rate schedules, and payment vouchers for 2026.

2 minutes$0 - Choose your calculation method (safe harbor or current year)04

Use the prior-year safe harbor if your income is stable, or the annualized method if income varies.

10 minutes$0 - Calculate your quarterly payment amount05

Include both income tax and self-employment tax (15.3% on net earnings up to $184,500 for 2026).

30-60 minutes$0 - Register for EFTPS or set up IRS Direct Pay06

EFTPS enrollment takes 5-7 days by mail; Direct Pay works immediately with no registration.

10 minutes (Direct Pay) or 5-7 days (EFTPS)$0 - Submit Q1 payment by April 15, 202607

Covers income earned January 1 through March 31.

5 minutesVaries by income - Submit Q2 payment by June 15, 202608

Covers income earned April 1 through June 30. Only 2 months after Q1.

5 minutesVaries by income - Review and adjust estimates at mid-year09

Compare actual income to projections and recalculate if income changed significantly.

20 minutes$0 - Submit Q3 payment by September 15, 202610

Covers income earned July 1 through September 30.

5 minutesVaries by income - Submit Q4 payment by January 15, 202711

Covers income earned October 1 through December 31. Or file your full return by January 31, 2027 to skip this payment.

5 minutesVaries by income

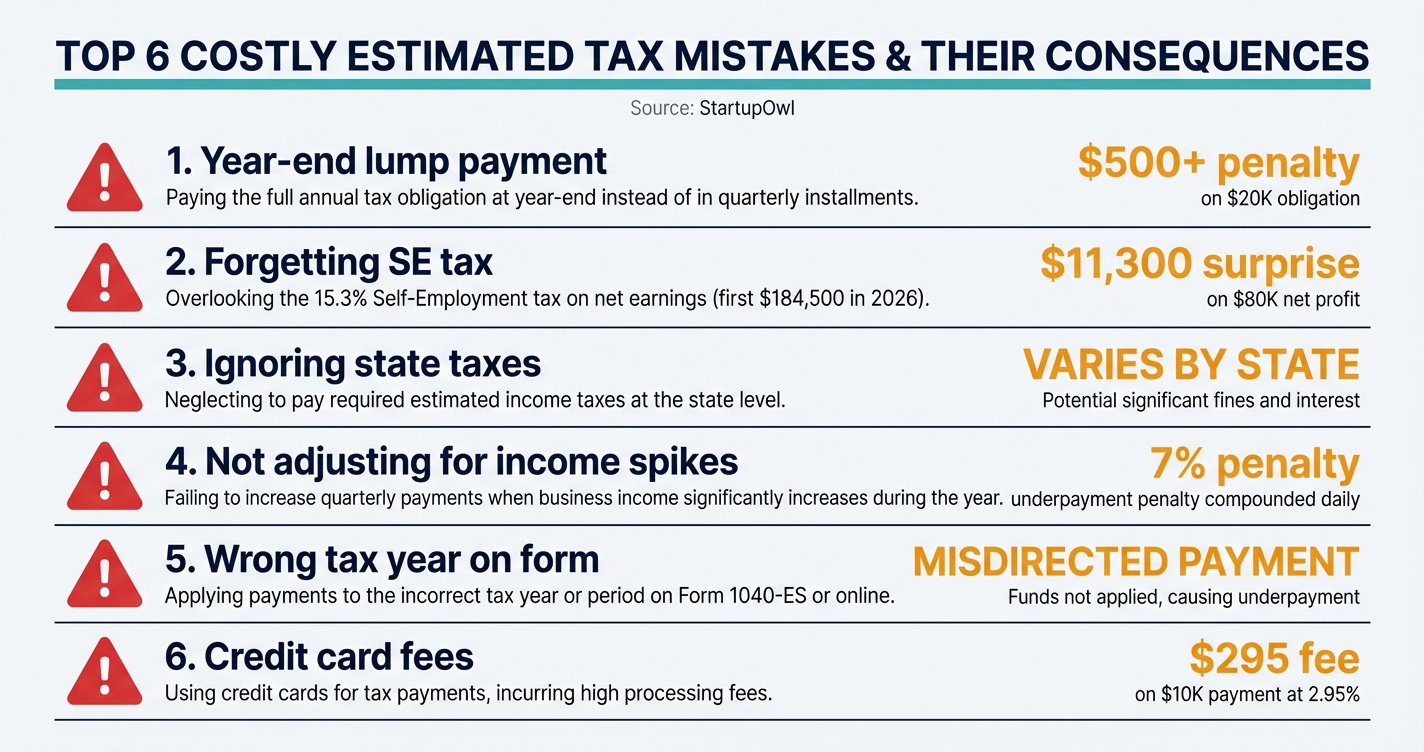

These are the most expensive mistakes business owners make with quarterly estimated taxes.

- Waiting until year-end to pay everything at once. The IRS calculates the underpayment penalty per quarter. Even if your total annual payment is correct, missing the Q1, Q2, or Q3 deadlines means you owe 7% annual interest on the shortfall for each late period. A $20,000 annual obligation paid entirely in Q4 could trigger $500 or more in penalties.

- Forgetting self-employment tax. New sole proprietors often calculate only their income tax and forget that self-employment tax adds 15.3% on the first $184,500 of net earnings for 2026. On $80,000 of net profit, that is roughly $11,300 in SE tax alone.

- Ignoring state estimated taxes. States like California, New York, and New Jersey have their own quarterly payment requirements. California's underpayment penalty rate is separate from the federal rate, and the threshold to trigger it can be as low as $500.

- Not adjusting payments when income spikes. If your Q3 revenue doubled, your Q1-sized payments will not be enough. The IRS checks each quarter independently. Increase your next payment or file Form 2210 Schedule AI with your annual return to demonstrate the annualized income installment method.

- Mixing up tax years on the payment form. When you submit payment in January 2027 for Q4 2026, make sure you select tax year 2026 on the form. Selecting the wrong year means the payment is applied to the wrong account, and you will receive an underpayment notice.

- Paying by credit card without doing the math. A 2.95% processing fee on a $10,000 payment is $295. Unless your credit card rewards exceed that amount, use the free IRS Direct Pay or EFTPS option instead.

Frequently Asked Questions

Your quarterly payment equals roughly 25% of your total annual tax liability. The simplest method is to take last year's total tax from your Form 1040, divide by four, and pay that amount each quarter. If your AGI was over $150,000, multiply your prior-year tax by 1.10 before dividing. For a sole proprietor earning $80,000 in net profit, you would owe approximately $20,000 to $22,000 for the year (income tax plus 15.3% SE tax), making each quarterly payment roughly $5,000 to $5,500.

The IRS charges an underpayment penalty at 7% annual interest (as of Q1 2026), compounded daily, on the amount you underpaid for each quarter. If you missed a $5,000 payment by 60 days, the penalty would be roughly $58. The penalty applies per quarter, so catching up with a larger payment later in the year does not eliminate the charge for the earlier missed period.

Yes. You can pay all four quarters up front with your Q1 payment on April 15. The IRS will apply it to the full year. This avoids the risk of missing later deadlines but requires you to have the full amount available in April. If your income is unpredictable, four equal installments are usually easier on cash flow.

If your W-2 withholding covers your full tax liability (including the side-business income), you may not need to make separate estimated payments. However, if the combined shortfall exceeds $1,000, you owe quarterly payments on the difference. You can also increase your W-4 withholding at your employer to cover the extra tax, which is simpler and avoids quarterly filings entirely.

The safe harbor rule protects you from the underpayment penalty if you pay at least 100% of your prior-year tax liability through withholding and estimated payments combined. If your prior-year AGI exceeded $150,000 ($75,000 if married filing separately), the threshold increases to 110%. Meeting the safe harbor means you will not owe a penalty, even if you end up owing additional tax when you file your annual return.

Single-member LLCs pay estimated taxes the same way as sole proprietors, using Form 1040-ES and your Social Security number (or EIN). Multi-member LLCs (partnerships) pass income through to individual partners, and each partner makes their own estimated payments on their share. LLCs taxed as S Corps handle most tax through payroll withholding on the owner's salary, with remaining distributions potentially requiring estimated payments. Use EFTPS if you need to make payments under your business EIN.

Sources & References

- IRS Estimated Taxes Overview

- IRS Form 1040-ES (2026)

- IRS Underpayment of Estimated Tax by Individuals Penalty

- IRS Quarterly Interest Rates (Q1 2026)

- IRS Publication 509 (2026 Tax Calendar)

- IRS EFTPS Information

- IRS Direct Pay

- IRS Self-Employment Tax Information

- Social Security Administration 2026 Wage Base

- IRS Credit/Debit Card Payment Options

About the Author

Senior Finance & Banking Editor

Richard is the veteran anchor of the site's financial content. Raised in the Midwest and starting his career in Chicago's commercial banking sector, he spent over a decade underwriting small business loans before moving into financial journalism. He doesn't get swept up in startup hype; he cares about unit economics, APYs, and fee structures.

Was this article helpful?

Questions about Quarterly Estimated Tax Payments Guide

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment