Business Plan Outline: Every Section Explained With Examples

A business plan outline includes 7-9 key sections. Learn what goes in each one, from executive summary to financial projections, with real examples and free templates.

In This Article

- Key Takeaways

- Step-by-Step

- Cost Breakdown

- What a Business Plan Outline Includes and When You Need One

- Who Needs Each Level of Business Plan

- How to Write Each Section of Your Business Plan

- What It Costs to Create a Business Plan

- Best Tools and Resources for Writing Your Plan

- What to Do If You Cannot Afford a Professional Plan

- 5 Business Plan Mistakes That Get Plans Rejected

- FAQ

$0–$15,000

Est. Loan Cost

72 hours

Timeline

7

Total Steps

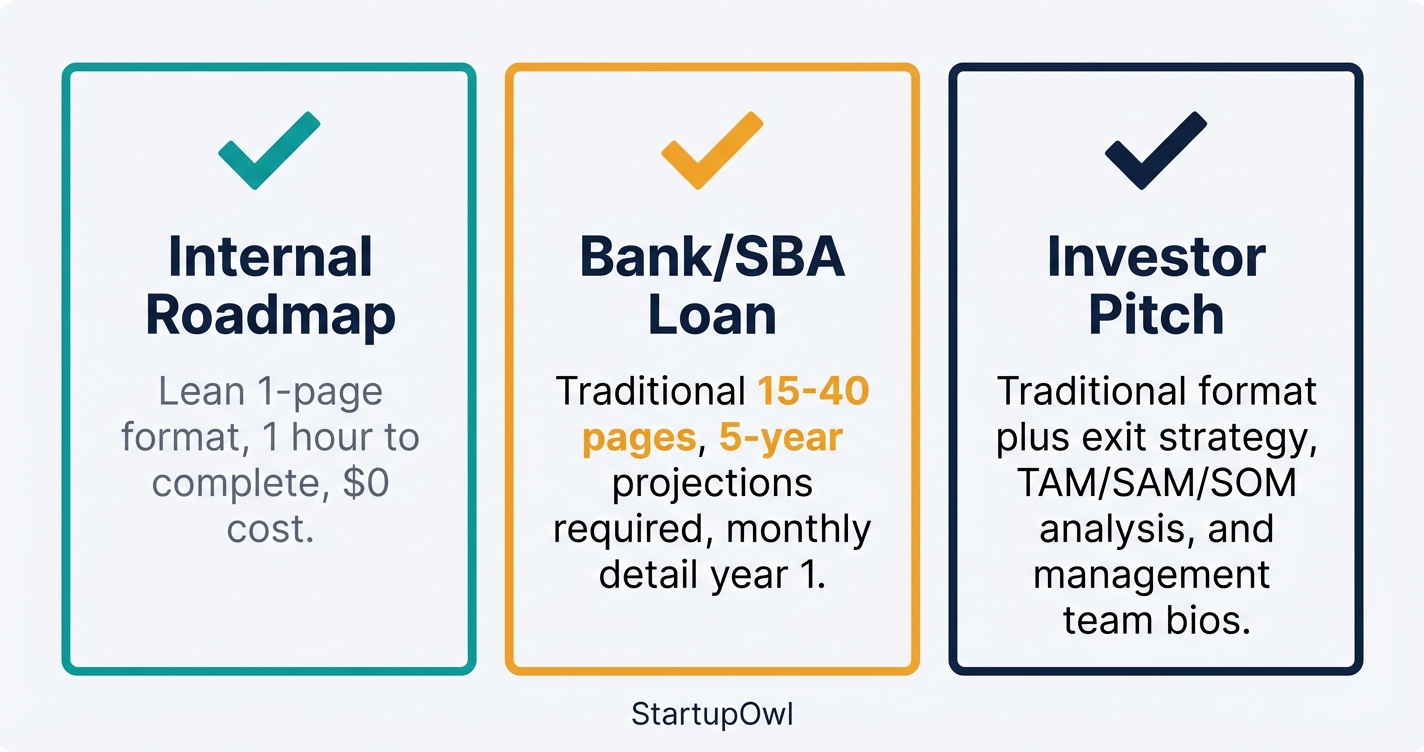

A complete business plan outline typically includes 7 to 9 sections, ranging from executive summary to financial projections. Whether you are applying for an SBA loan, pitching angel investors, or just building an internal roadmap, the structure stays largely the same. The difference is in how much detail each section requires.

Traditional plans run 15 to 40 pages and are required by most lenders and investors. Lean plans fit on a single page and take about an hour to complete. This guide covers every section in the traditional format, with specific guidance on what SBA lenders, bank officers, and investors expect to see in each one.

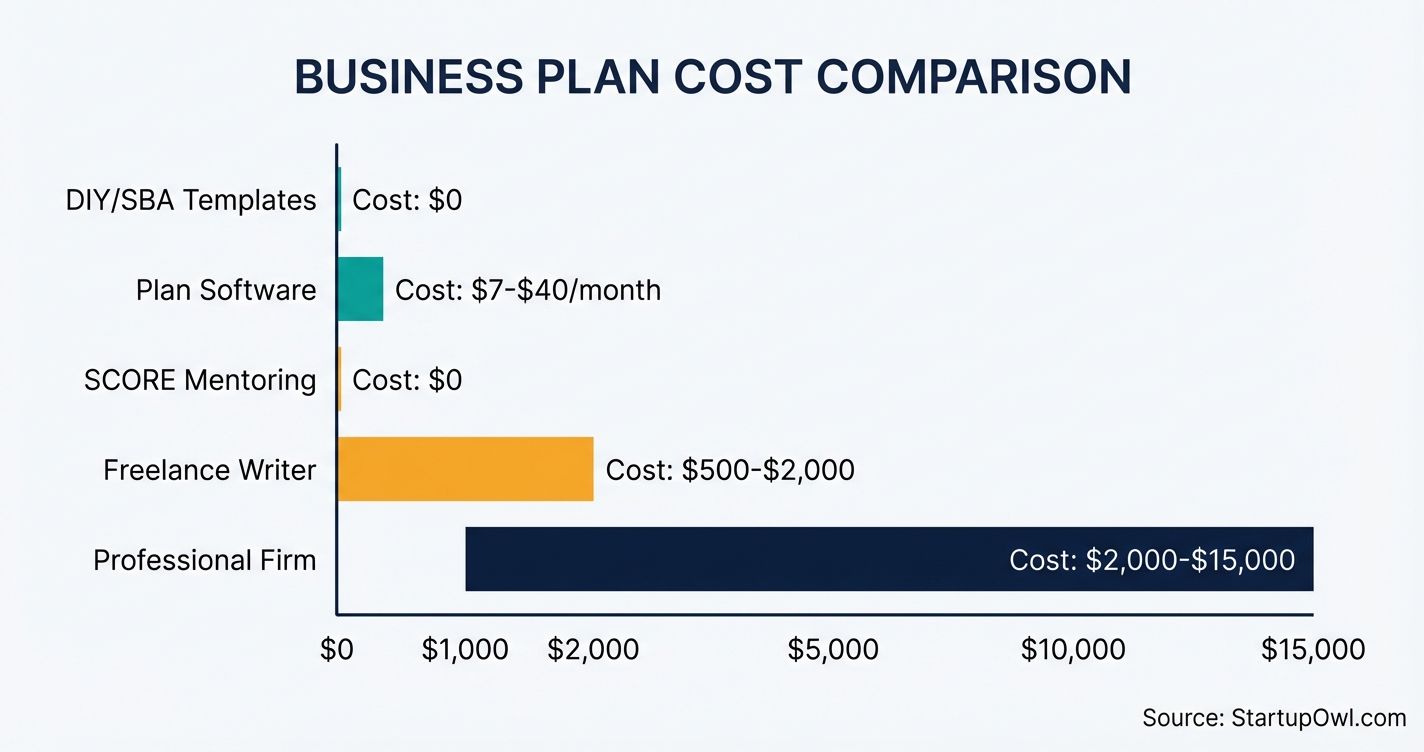

You can build your plan for $0 using free SBA templates, spend $20/month on software like LivePlan, or hire a professional writer for $2,000 to $15,000. No matter which path you choose, the outline below gives you the blueprint.

What a Business Plan Outline Includes and When You Need One

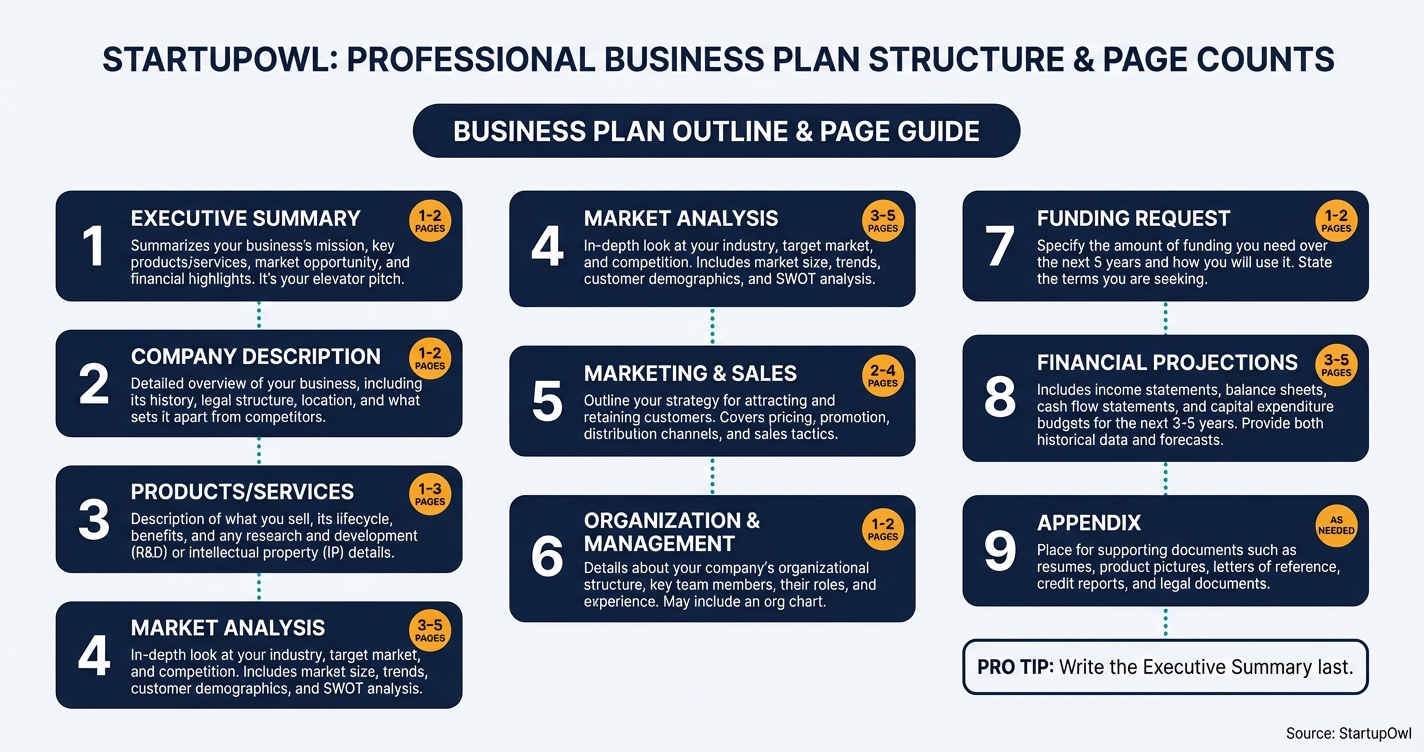

A business plan outline is the structural framework that organizes your company's story, market opportunity, and financial projections into a format lenders and investors can evaluate quickly. The SBA recommends 9 common sections for a traditional plan, though you can add or remove sections based on your needs.

The core sections are the executive summary, company description, market analysis, organization and management, products or services, marketing and sales strategy, funding request (if applicable), financial projections, and appendix. Each serves a specific purpose and builds on the one before it.

You need a business plan when applying for any business loan, raising investment capital, or entering a new market. Even if no one asks for it, writing one doubles your odds of success according to SCORE data. SCORE reports that small business owners who receive at least 3 hours of mentoring (often centered on business planning) report higher revenues and faster growth.

Who Needs Each Level of Business Plan

If you are applying for an SBA loan, your plan must include 5-year financial projections with monthly detail for year one. SBA lenders commonly request traditional plans with comprehensive financial documentation. Some may require 24 months of monthly projections and 3-5 years of historical financials for established businesses.

If you are seeking angel investment or pre-seed funding, your plan should emphasize market size, competitive advantage, team credentials, and a clear path to profitability. Investor-facing plans typically need an exit strategy section covering IPO, acquisition, or buyout scenarios.

If you just need an internal planning document, a lean one-page plan covers the essentials. The SBA's lean startup template is free and takes about 1 hour to complete. You can always expand it into a full traditional plan later when you need financing.

How to Write Each Section of Your Business Plan

Below is a walkthrough of every section in a standard business plan outline, in the order they appear in the finished document. Remember that the executive summary appears first but should be the last section you write.

1. Executive Summary (1-2 pages). Summarize your business concept, the problem you solve, your target market, team highlights, financial projections summary, and funding request. Keep it concise. This section determines whether the reader continues or stops.

2. Company Description. Explain what your business does, who it serves, and your business structure (LLC, S-corp, sole proprietorship). Include your mission statement, founding story, and core competitive advantages.

3. Products and Services. Lead with the customer problem, then describe your solution. Include intellectual property, patents, letters of intent, early traction, and product lifecycle details.

4. Market Analysis. Present your total addressable market, target demographics, industry trends, growth projections, and a competitive analysis of your top 3-5 competitors with their strengths and weaknesses.

5. Marketing and Sales Strategy. Cover market positioning, pricing strategy, customer acquisition channels, distribution methods, and sales process. Include projected marketing budgets and a SWOT analysis.

6. Organization and Management. Detail your team structure with an organizational chart. Include bios of key team members and positions you plan to hire. Lenders want proof your team can execute.

7. Funding Request. If raising capital, specify the exact dollar amount, whether you want debt or equity, the repayment timeline, and a detailed use-of-funds breakdown.

8. Financial Projections. Provide 5-year forecasts including income statements, balance sheets, cash flow statements, and break-even analysis. Year one should be monthly; years 2-5 can be annual.

9. Appendix. Include supporting documents such as resumes, detailed market research data, legal documents, product photographs, contracts, and additional financial detail.

What SBA Lenders Specifically Look For

SBA lenders focus on your ability to repay the loan, not just your market opportunity. Your financial projections must show realistic cash flow that covers loan payments. Include personal financial statements and any assets (home, car) that could serve as collateral. If your business is operating, provide 12-24 months of historical income statements and a current balance sheet. The funding request section should clearly state whether the money is for capital expenditures, working capital, debt retirement, or acquisition.

What It Costs to Create a Business Plan

Your total cost depends on how much help you need. A DIY plan using free SBA templates costs $0 but requires 20-40 hours of your time. Business plan software like LivePlan charges $20/month for the standard plan and $40/month for premium. Upmetrics starts at $7/month, and Bizplan costs about $21/month (or $349 for lifetime access).

Freelance business plan writers on Upwork charge a median rate of $40/hour, with most plans in the $500-$2,000 range. Professional writing firms charge $2,000 to $15,000 or more, with turnaround of 3-4 weeks. Larger or more complex plans (biotech, manufacturing, multi-location) run toward the higher end.

Free alternatives include SCORE mentoring, which pairs you with a retired business professional who can review your plan and provide feedback at no cost. SCORE has helped over 17 million small business owners since 1964 and operates 250+ chapters nationwide.

Business Plan Cost Comparison

| Type / Provider | Rate | Notes |

|---|---|---|

| DIY (free SBA templates) | $0 | Requires 20-40 hours of your time. Traditional and lean templates available. |

| LivePlan (Standard) | $20/month | Step-by-step guidance, 550+ sample plans, automated financials. |

| LivePlan (Premium) | $40/month | Adds QuickBooks sync, KPIs, and advanced forecasting. |

| Upmetrics (Starter) | $7/month | AI-powered, lower cost alternative with financial modeling. |

| Bizplan (Lifetime) | $349 one-time | Unlimited plans, 650+ masterclass videos, fundraising integration. |

| Freelance writer (Upwork) | $500-$2,000 | Median $40/hour. Quality varies widely. Ask for portfolio samples. |

| Professional writing firm | $2,000-$15,000+ | Full research, financial modeling, investor formatting. 3-4 week turnaround. |

| SCORE mentoring (plan review) | $0 | Free feedback from retired business professionals. SBA resource partner. |

Best Tools and Resources for Writing Your Plan

LivePlan is the most widely recommended business plan software, with over 1 million small businesses using it as of 2026. It includes 550+ sample plans, an AI writing assistant, financial forecasting with auto-generated statements, and an SBA-approved format. Plans start at $20/month with a 35-day money-back guarantee. Visit LivePlan.

Bizplan (by Startups.com) is especially strong for founders actively fundraising. It integrates with Fundable, an equity crowdfunding platform, and includes drag-and-drop plan building, financial tools, and access to 20,000+ mentors. Pricing is $29/month or $349 for lifetime access. Visit Bizplan.

Upmetrics offers AI-powered planning at a lower price point, starting at $7/month. It is a strong choice if you need financial modeling features but want to keep costs down. Visit Upmetrics.

SCORE.org provides free business plan templates and pairs you with a volunteer mentor who can help you write and review your plan at no cost. SCORE mentors provide guidance on business planning, financing, and market research. Find a SCORE mentor.

SBA.gov offers free traditional and lean business plan templates, including sample plans for a consulting firm (Rebecca's plan) and a toy company (Andrew's plan). These are the gold standard for SBA loan applications. Download SBA templates.

What to Do If You Cannot Afford a Professional Plan

If hiring a writer is not in your budget, start with the free SBA templates and work through them section by section. Pair that with free SCORE mentoring for feedback. SCORE mentors will not write your plan for you, but they will tell you what is missing and what needs improvement.

Business plan software in the $7-$20/month range gives you guided templates, auto-generated financials, and sample plans to reference. That is your best value option if you want professional-looking output without professional-level costs. AI tools like ChatGPT can help you draft individual sections, but always review and customize the output.

If you need funding but your plan is not ready, consider starting with a business line of credit or business credit card that does not require a formal plan. Microloans from community lenders sometimes require less documentation than traditional bank loans.

5 Business Plan Mistakes That Get Plans Rejected

1. Unrealistic financial projections. Projecting 300% revenue growth in year one without supporting data is the fastest way to lose credibility. Lenders compare your assumptions to industry benchmarks. Use realistic growth rates and show your math.

2. Missing or weak competitive analysis. Saying you have "no competitors" signals you have not done your research. Every business has competitors, even if they are indirect substitutes. Name them, analyze their strengths and weaknesses, and explain your differentiation.

3. No clear use of funds. Lenders want to see exactly where their money goes. A vague statement like "for business growth" is not enough. Break it down by category (equipment, inventory, payroll, marketing) with specific dollar amounts.

4. Skipping the management team section. Investors bet on people, not just ideas. If your leadership bios are missing or thin, it raises concerns about execution capability. Include relevant experience, past successes, and your business structure.

5. Writing the executive summary first and never updating it. Your summary should reflect the final version of every other section. If it contradicts your financial projections or market analysis, lenders will notice. Always write it last and proofread it against the rest of the plan.

Step-by-Step Process

- 1

Choose your business plan format

Pick between a traditional plan (15-40 pages, detailed sections, required by most lenders) and a lean startup plan (1 page, high-level summary, takes about 1 hour). If you plan to apply for an SBA loan or seek investor funding, go traditional. If you just need an internal roadmap, lean is fine.

The SBA provides free downloadable templates for both formats. You can also use business plan software like LivePlan (starting at $20/month) or Bizplan (starting at about $21/month) for guided step-by-step creation.

Tips

- Use a traditional format if you are applying for any bank loan or SBA financing.

- Download the SBA's free sample plans from Rebecca and Andrew to see what a finished product looks like.

- Consider Upmetrics (starting at $7/month) if LivePlan feels too expensive.

Common Mistakes

- Using a lean plan when applying for bank or SBA financing, which requires far more detail.

- Starting from scratch instead of using a proven template, which wastes time and often misses key sections.

- 2

Write your company description and products section

Start with a clear company description that covers what your business does, the problems it solves, who it serves, and your LLC formation or corporate structure. Include your mission statement, location, and founding story. A layperson should understand what you do after reading the first two sentences.

Then describe your products or services. Lead with the customer problem, then explain your solution. Include any intellectual property, patents, signed contracts, or early sales traction. If you have letters of intent from potential customers, add them here or reference them in the appendix.

Tips

- Describe your business structure (LLC, S-corp, sole proprietorship) and explain why you chose it.

- Include product lifecycle details, competitive differentiation, and pricing rationale.

Common Mistakes

- Writing in vague, jargon-heavy language instead of plain English that any reader can follow.

- Forgetting to explain your competitive advantage and how your product is different from existing alternatives.

- 3

Research and write your market analysis

This is where you prove there are paying customers for your product. Include your total addressable market (TAM), target market characteristics, industry growth trends, and customer purchasing behavior. Use real data from industry reports, census data, or trade associations.

Add a competitive analysis that names your top 3-5 competitors, their strengths, weaknesses, market share, and pricing. Show investors you understand who you are up against and how you plan to win. If your business depends on a few key customers, identify them here.

Tips

- Use free data from the U.S. Census Bureau, Bureau of Labor Statistics, and IBISWorld summaries for market sizing.

- Be specific about your target customer with demographics, psychographics, and buying habits.

- Include both direct competitors and indirect substitutes in your competitive analysis.

Common Mistakes

- Claiming your product has no competitors, which signals a lack of market research to investors.

- Using inflated market size numbers without explaining how you calculated your serviceable addressable market.

- 4

Build your marketing and sales strategy

Detail exactly how you will attract and convert customers. Define your market positioning (low-cost leader, premium option, niche specialist), unique value proposition, and your top 3 customer acquisition channels. Include a pricing strategy and how it compares to competitors.

Outline your sales process (self-serve, inside sales team, field sales), distribution channels (online, retail, wholesale), and projected marketing budget. If you have any early marketing results, customer testimonials, or conversion rates, include them. SBA lenders will refer back to this section when evaluating your financial projections.

Tips

- Include a SWOT analysis (strengths, weaknesses, opportunities, threats) to show you have considered all angles.

- Be specific about marketing costs per channel (e.g., $500/month on Google Ads, $200/month on social media).

Common Mistakes

- Listing marketing channels without attaching specific budgets, timelines, or expected results.

- Ignoring customer retention strategy and focusing only on acquisition.

- 5

Outline your organization and operations

Describe your management team, organizational structure, and key personnel. Include brief bios or resumes highlighting relevant experience. Lenders want to see that your team has the skills to execute the plan. An organizational chart helps lenders quickly understand reporting lines.

For operations, cover your location, facilities, technology, equipment, supply chain, and key partners. If you are using accounting software or other critical business tools, mention them. Show how you will maintain quality while scaling.

Tips

- Include key positions you plan to hire for in the next 12-24 months.

- Add an organizational chart, even if your team is just 2-3 people today.

Common Mistakes

- Omitting management team bios, which is one of the top things lenders and investors evaluate.

- Failing to address operational scalability, leaving lenders worried you cannot handle growth.

- 6

Create your financial projections and funding request

Include 5-year financial projections with income statements, balance sheets, cash flow statements, and a break-even analysis. Your first year should include monthly detail; years 2-5 can be annual summaries. Some SBA lenders require 24 months of monthly projections, so check with your bank before submitting.

If you are raising capital, add a funding request that specifies the exact amount you need, whether you want debt or equity, how you will use the funds, and your repayment timeline. For established businesses, include 3-5 years of historical financials as well. If you need help building financial models, SCORE offers free mentoring with retired finance professionals.

Tips

- Use LivePlan or similar software to auto-generate financial statements from your assumptions.

- Include a use-of-funds breakdown showing exactly where the money goes (equipment, payroll, inventory, marketing).

- Add graphs and charts for trend analysis to make financial data easier for lenders to digest.

Common Mistakes

- Using overly optimistic revenue projections without supporting assumptions or market data.

- Forgetting to include a clear repayment strategy and exit plan, which are critical for debt financing.

- 7

Write the executive summary last

Your executive summary appears first in the plan but should be the last section you write. Limit it to 1-2 pages. Summarize who you are, the problem you solve, your solution, the target market, your team, financial highlights, and your funding ask. This is the section that determines whether a lender or investor reads further.

For investor-facing plans, tailor your summary to emphasize return on investment. For SBA loan applications, focus on your ability to repay the loan and your business stability. Include your mission statement and high-level growth plans. Then compile an appendix with supporting documents (resumes, market data, legal documents, product photos).

Tips

- Write the executive summary after every other section is complete so you can accurately distill the highlights.

- Keep it to 1-2 pages maximum. Investors spend an average of 3-5 minutes on this section before deciding to read on.

Common Mistakes

- Writing the executive summary first and then failing to update it after the rest of the plan is finalized.

Cost Breakdown

| Item | Cost Range | Notes |

|---|---|---|

| DIY with free SBA templates | $0 | Requires your time (20-40 hours). SBA provides free traditional and lean templates. |

| Business plan software (LivePlan, Bizplan, Upmetrics) | $7-$40/month | Guided templates, auto-generated financials, 500+ sample plans. LivePlan starts at $20/month. |

| Freelance business plan writer | $500-$2,000 | Median rate of $40/hour on Upwork. Quality varies. Ask for samples and references. |

| Professional business plan writing firm | $2,000-$15,000 | Includes market research, financial modeling, investor-ready formatting. Turnaround is 3-4 weeks. |

| SCORE mentoring (plan review and feedback) | $0 | Free mentoring from retired business professionals through SBA-backed SCORE program. |

Frequently Asked Questions

A traditional business plan for lender or investor use typically runs 15 to 40 pages, depending on your industry and the complexity of your financials. A lean startup plan is 1 page and takes about an hour to create. If you are applying for an SBA loan, aim for 7 to 10 pages minimum of narrative plus financial statements.

Yes. The SBA provides free business plan templates in both traditional and lean formats. SCORE offers free mentoring to help you review and improve your plan. Expect to spend 20 to 40 hours researching and writing if you go the DIY route.

Freelance writers charge $500 to $2,000 for a basic plan, with a median hourly rate of $40/hour on Upwork. Professional writing firms charge $2,000 to $15,000 or more for a comprehensive, investor-ready plan. The price depends on your industry complexity, level of financial modeling needed, and turnaround time.

SBA lenders typically want 5-year financial projections that include income statements, balance sheets, and cash flow statements. Year one should have monthly detail, and some lenders require 24 months of monthly projections. If your business is established, you also need 3-5 years of historical financials.

Most banks and SBA lenders require a business plan as part of your loan application. Some online lenders and merchant cash advance providers do not, but their interest rates are significantly higher. Having a solid plan improves your approval odds and can help you negotiate better terms on any small business loan.

Write it last. The executive summary distills the key points from every other section. If you write it first, it will not accurately reflect your final market analysis, financial projections, or funding request. Draft all other sections first, then summarize the highlights into 1-2 pages.

This content is for informational purposes only and does not constitute financial, legal, or tax advice. Business financing terms, rates, and eligibility vary by lender, credit profile, and business characteristics. Consult a licensed financial advisor or CPA before making borrowing decisions. Pricing for business plan services and software reflects publicly available data as of 2026-2026 and may change without notice.

Sources & References

- Write Your Business Plan - U.S. Small Business Administration

- Sample Business Plans - U.S. Small Business Administration

- A Simple Business Plan Outline to Build a Useful Plan - Bplans / LivePlan

- SCORE - Free Small Business Mentorship and Resources

- Business Plan Writer Hourly Rates - Upwork

- How Much Do Business Plan Writing Services Cost - Growthink

- Best Business Planning Software - ZenBusiness

- How to Write a Business Plan for Investors 2026 - PrometAI

- How to Write an SBA Business Plan - LivePlan

- Business Plan Template: 10 Essential Sections for 2026 - Deliberate Directions

About the Author

Director of Entrepreneurial Strategy

Jennifer is a former founder who built and sold a boutique B2B logistics company in her thirties. She understands the emotional and strategic toll of building a business from the ground up without a massive safety net. She is deeply connected to the Atlanta startup ecosystem and is passionate about equitable funding.

Was this article helpful?

Questions about Business Plan Outline

No comments yet. Ask the first question and a member of our team will answer.

Leave a comment